Welcome to a new episode of my Dividend Diary on the TEV Blog. Here, I report the development of a cash flow-oriented investment approach that focuses on generating a passive income through dividends. Against this background, the goal is not to outperform the market but to put food on the table through a regular income via dividends.

As you know, I take care of my wealth management. To keep things simple, I have built three pillars:

- Active income.

- Passive income.

- Conversion.

Dividends fall into the last two categories. They are passive because I no longer have to work to receive the payments. Furthermore, they also contribute to the conversion because I reinvest the dividends and thus increase my passive income through dividends for the future.

My monthly dividend income in April:

This month I have received payments from the following companies:

- Automatic Data Processing (6.03 EUR)

- Iron Mountain (14.72 EUR)

- Kimberly Clark (16.45 EUR)

- Merck & Co. (9.38 EUR)

- Deutsche Telekom (45.00 EUR)

- Diageo (20.29 EUR)

- GlaxoSmithKline (23.14 EUR)

- Realty Income (3.52 EUR)

- Leggett & Platt (11.10 EUR)

- Henkel (45.75 EUR)

- Swiss Re (65.84 EUR)

- Simon Property Group (5.49 EUR)

- Cisco Systems (10.61 EUR)

- Bayer (44 EUR)

- Altria (19.29 EUR).

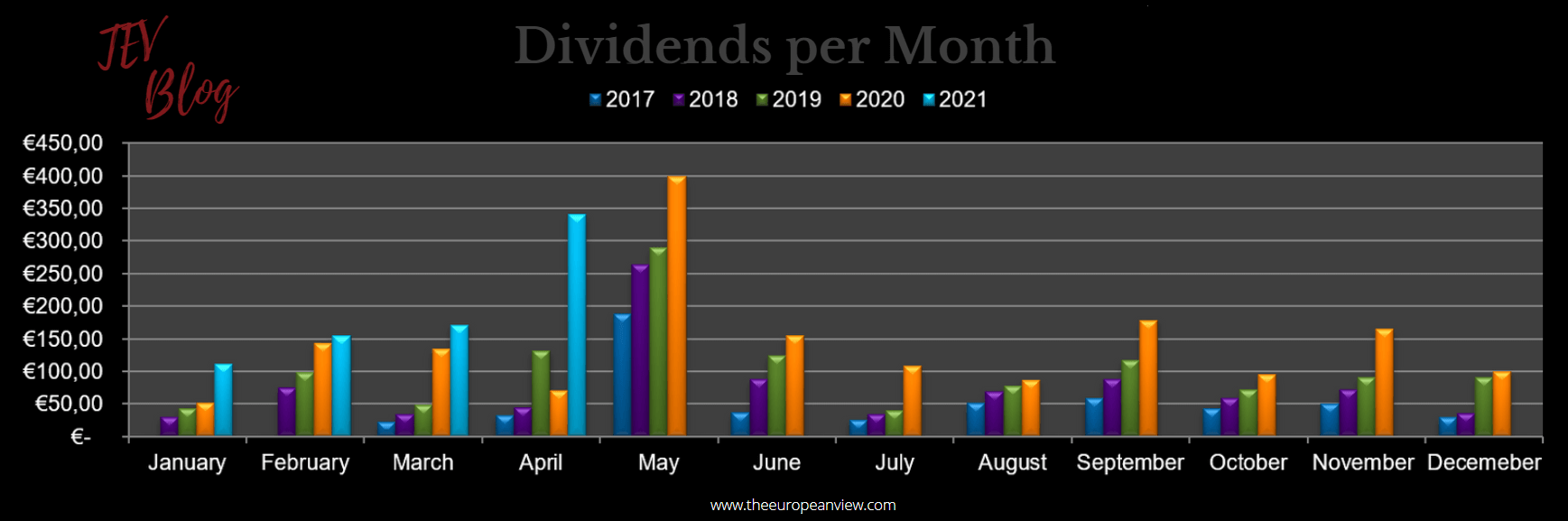

The total dividend income in April (after taxes) was: EUR 340.61/appr. 412 USD

Dividend income check

Now let’s see how this month performed compared to the previous year. Last year, I received only EUR 70.56 in dividends in April, representing an increase of almost 400 percent.

April was a melt-up month, and I appreciate the income hike. There were several reasons for this development. First, many European companies had postponed their dividends to later months last year. That’s why April 2020 was my only month below the previous year’s level. My stock purchases the previous year have also had a noticeable effect this year. Since many companies only pay their dividends once a year (especially in April, May, and June), the impact of such additional purchases is powerful in the respective months.

Accordingly and on sober reflection, there is little reason to burst out in joy. It is nonetheless good to see that my cash flow-oriented approach is slowly but steadily bearing fruit. While the last year’s recession was heavy, most companies maintained or even increased their payouts. I like not being dependent on share price developments, but building up a passive cash flow with a broad mix of company holdings.

So I am pleased with the positive development and hope that May and the other months of the year will also bring pleasant surprises. The journey of my dividend income throughout the years is as follows:

Stock purchases for more dividend income

So back to business as usual. Last month, I bought shares in three companies and additional shares of one of my existing EFT holdings:

- Amundi Index MSCI Emerging Markets UCITS ETF DR (D) (14 shares)

- Vonovia (15 shares)

- Johnson & Johnson (10 shares)

- AT&T (22 shares)

In the following, I will briefly explain why I bought these companies. Please do not expect a fundamental analysis. I will only mention some aspects per company that might be of interest to the readers. Maybe you will find inspiration for your investment. In case you disagree, feel free to write your opinion about my purchases in the comments.

In April, the first thing I did was to increase my portfolio’s exposure to emerging markets by buying more shares of my Emerging Markets ETF. The ETF seeks to replicate as closely as possible the performance of the MSCI Emerging Markets Index.

I am happy to be in line with my goal of continuously buying more shares of this ETF (the last purchase was in December 2020). I have also invested in the Chinese companies China Mobile and Ping An Insurance in recent months and still have my well-performing Tencent shares which I bought a few years ago. Emerging markets now account for about 8 percent of my portfolio.

In the future, I will try to increase my exposure to emerging markets a bit more. Investments in individual companies will remain the exception rather than the rule though. By the way, I was close to buying shares of Hengan International. The Chinese version of Procter & Gamble seems appealing when looking at the fundamentals. Nevertheless, there were good reasons to decide in favor of the ETF – at least from my point of view. Besides severe allegations against the company and its management, I was not impressed with the operating performance. I also published a longer article on this topic on Seeking Alpha (click here).

In April, I also bought further shares in Vonovia, which owns more than 400,000 apartments in Germany, Sweden, and Austria. The shares have been dormant in my portfolio for many years and have performed very well during that time. The company has increased its dividend for seven years now, and for 2021, the increase was just under 8 percent.

The company is benefiting from the ongoing trend of rising rents and house prices. I, too, am noticing the effects of ever-rising house prices. In some cities, those prices are ridiculously high. With my investment in Vonovia, I want to benefit at least indirectly from this development.

In addition, Germany’s Federal Constitutional Court has ruled that the rent cap in the German capital Berlin is unlawful. Vonovia has 40,000 apartments in Berlin and was also affected by the rent cap. However, this is still no reason for Vonovia shareholders to rejoice. The court merely ruled that the federal state of Berlin had no authority to implement the rent cap. At the federal level, Germany’s government can still implement such tools.

Noteworthy are the federal elections in Germany in September. Here, the decisive factor will be which party provides the next chancellor. The party “Grünen” (Greens), which currently has excellent poll ratings, is taking a somewhat more restrictive approach here than the current governing “CDU/CSU” party. Nevertheless, I think a federal rent cap is unlikely since that would require an alliance of the Greens with the social democrats from the SPD and the Left Party. Honestly, I am a little short on imagination for this coalition right now. Yet there is some uncertainty.

The share is currently in a consolidation phase and has even slipped below its historical adjusted P/FFO ratio. Nevertheless, the company is not a bargain from a fundamental point of view. An adjusted P/FFO ratio of 23 is still relatively high. At the current price level, I will therefore not make any further additional purchases. Price setbacks or more extensive corrections are thus quite welcome.

Probably 25 or 30 years from now, we’ll be saying that investors never needed anything other than a portfolio of Johnson & Johnson, Amazon, Apple, and Procter & Gamble to retire wealthy. Such an approach would be pure hara-kiri from a risk compliance perspective, though. Likewise, there are so many other great companies. And in any event, let’s not make the mistake of extrapolating past performance into the future.

Despite all this, Johnson & Johnson is simply a great company. It has delivered operationally continuously for decades. Yes, currently, it is overvalued. I still increased my share significantly. There was no real reason why just now. The markets are overpriced anyway, and it’s hard to find a bargain.

So before I always put capital into supposedly undervalued stocks (see AT&T, *ahem ahem* below), I also try to buy shares of solid companies that are somewhat more expensive. My purchase of 8 more Apple shares in October 2020 falls under this category. Although Apple was also highly overvalued back then, I wrote the following, and it also applies to Johnson & Johnson:

Of course, I could invest in rather lame crutches like Cisco or IBM (which I do), but why shouldn’t I increase my share in the best performers now and then? Diversification also includes making additional purchases not only in the weak but also in strong companies. If Apple’s share price falls, that’s no problem for me. I’ll buy more shares then. This is how the cost-average effect works.

I would also like to highlight Johnson & Johnson’s balance sheet. The company is brutally solid financial-wise. The interest-bearing debt of USD 36 billion is offset by a cash mountain of USD 25 billion. Furthermore, the company is sitting on a pile of treasury stocks worth almost USD 40 billion. Of course, I would prefer a lower share price, but conversely, Johnson & Johnson’s solid balance sheet, 2.5 percent dividend yield, and strong market position are worth the premium price.

Investors do not have to pay a premium price at AT&T. The balance sheet also looks terrible compared to Johnson & Johnson’s. C-Band financing and a USD 23 billion payment in March pushed net debt from USD 147.6 billion to almost USD 170 billion, resulting in a debt to adjusted EBITDA ratio of 3.1. Investors will have to wait until 2024 for AT&T to reach its long-term target of x2.5 (which is still relatively high).

In return, investors get a premium dividend yield of 6.6 percent. Is it worth it? I don’t know. What we know is that customer growth is promising and sustainable. Customer retention (churn rate of 0.86 percent) is also quite stable and shows that customers are satisfied with AT&T’s services. The company is historically cheap in any case.

Overall, I like AT&T’s fundamental focus as a content and distribution company. The cash flows it generates are massive and the business is slowly returning to a growth path. If management succeeds in getting its debts under control, shareholders will get their piece of cake via higher dividends or share buy-backs. The market will then probably also grant the company a higher price. I also shared my thoughts on the latest quarterly numbers in an article on Seeking Alpha (click here).

Watchlist for May

Next month, there will be some additional purchases of shares. I am relatively flexible here. Either I buy new positions, or I increase my shares in existing investments.

The following companies are on my watchlist in particular:

- Microsoft (MSFT)

- Bristol Meyers Squibb (BMY)

- Digital Turbine (APPS)

- Intel (INTC)

- Salesforce (CRM)

- Mayr-Melnhof Karton AG

- SAP (SAP)

- Bayer

- Hugo Boss

- Sysco (SYY)

If you look at my report from last month, you will see that none of the companies I bought were on my watchlist. Why is that? Is the watchlist nonsense, and in the end, I only do what I want anyway? Yeah, a little bit. I don’t have a fixed system for my stock purchases, and that’s one thing I have to consider changing.

However, I have an extensive overview of many companies that I look at from time to time. The watchlist companies are primarily companies that I have currently examined particularly carefully, where substantial changes are imminent or which are in my focus for other reasons.

They are present to me in some form, which is why I put them on the list and perhaps monitor them a little more closely than other companies. But it often happens that I invest in different companies, after all. And so it happens that I buy other companies because it seems convenient at that moment.

Have you received dividends this month? What’s on your watchlist? Let me know and write it in the comments.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

Hallo,

Wieder ein klasse Artikel. Kleiner Hinweis: in der Überschrift monthly dividend income steht march. Ich will grundsätzlich kein Klugscheißer sein. Ich hoffe, du nimmst es nicht quer. Ich war kurz davor Hengan zu kaufen. Dein Artikel hat mit geholfen. Ich habe es nicht getan. Vielen Dank dafür. Ich werde ca. 280€ erhalten. Erhalten deswegen, da mir noch die Verbuchung der Altria Dividende fehlt.

PS toller Blog und tolle Artikel auf den anderen Kanälen

VG & noch ein schönes WE!

Hallo Thorbjorn,

vielen Dank für den Hinweis und die weiteren netten Worte! Nein, das nehme ich natürlich nicht quer. Es ist bereits korrigiert. 🙂

Hengan war wirklich eine enge Kiste und die Dividende sehr verlockend, aber für mich persönlich kann ich dann mit PG, KMB oder gleich einem diversifizierten ETF mehr anfangen. Ich werde das Unternehmen aber weiter beobachten.

Viele Grüße und ebenfalls ein schönes WE!