Calling a thought or statement bullshit (BS) is a radical thing. It is somewhat arrogant because it implies supposed superior knowledge. It also indicates a high ground, a looking down on someone or something. And yet, there are some BS thoughts, and I try to avoid them when making investment decisions. This article is the second part of my short “bullshit investing” series. It deals with the risks that lurk for our investments when we move too far onto the ice of our cognitive limitations.

Readers key takeaways:

- Part I was mostly about echo chambers and our cognitive limits. In Part II, we speak about why those limits and echo chambers are dangerous for wealth management.

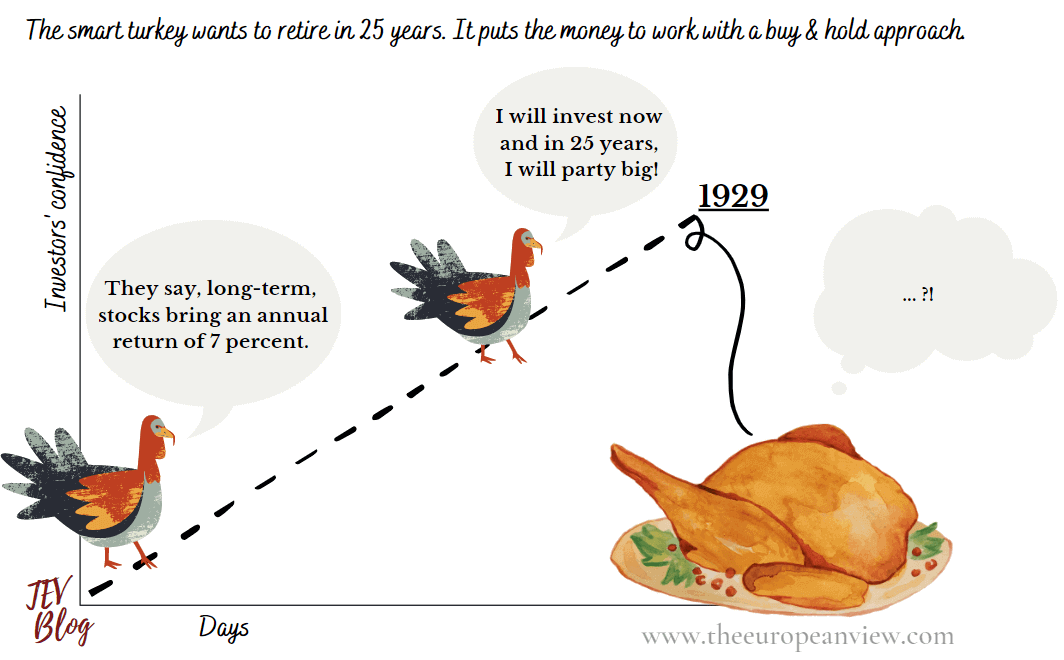

- We all know them, the big speeches about the average annual return of stock markets which is about 7 percent. And yes, looking back, we achieved that number. History, however, knows other, far worse chapters.

- In addition, the more often I am wrong, the more often I have to be correct, and the more capital I have to invest. That’s why, in my opinion, a low-risk-oriented approach is better in the long term than an opportunity-oriented approach.

- Other examples make me doubt that investors are always aware of the thin ice they are walking on. The FIRE movement or the “corporate world is bad” narrative shows that investors are willing to plan their future based only on specific assumptions about future events whose occurrence is highly uncertain.

- The question should be, “am I doing something today because I want to do it today?” and not “am I just doing something today because I know my future is secure because I expect a long-term return of 7 percent a year?”.

- Let’s not be turkeys.

Echo chambers and the inconsistencies of our thinking

In Part I, we briefly looked at echo chambers and their mechanisms. To catch you up, I summarize the most critical observations again below.

Communities and their echo chambers

One important observation was that communities benefit from mechanisms that amplify or filter information. What kind of mechanism comes into play depends on whether a piece of information is subject to the community’s common value framework ( then the info is amplified) or not ( then it is blocked/filtered).

I can well observe how these mechanisms work in my bubble. I am part of this bubble, and my actions mostly conform to the common patterns, thus cementing them as “social codes”. But in the end, these are primarily patterns of redundancies and repetitions (we could also describe it as “nonsense condensed by repetition”).

We can benefit from these mechanisms, but it’s not all sunshine

These mechanisms hold such systems in place or lay the foundation for them, which is not bad. From an evolutionary point of view, we have seen that such mechanisms are helpful for the maintenance of a clan. A shared understanding of common values creates solidarity and a compass for one’s actions. Eventually, ethics and morals were able to develop in the first place through this mechanism.

Still, it’s not all sunshine. Such systems are vulnerable. Their strength is also their greatest weakness. Amplifying or filtering mechanisms can be devastating if, for example, they block information that is essential for survival. A community must avoid this as much as possible.

Inconsistencies and cognitive limits

However, we saw that the members of these communities act and think inconsistently. We looked at this in Part I and noticed that we underestimate the role of luck and randomness but at the same time overestimate our ability to predict the future.

The traps here are hidden. We know that we cannot time the market. Nevertheless, we base our actions on particular assumptions, which result in the belief that certain events will occur. One concrete example was our assumption that stock markets rise by an average of 7 percent per year over the long term.

Cognitive biases lead us onto thin ice

The many cognitive biases and our intellectual limitations are human, but at the same time, dangerous. We are constantly walking on thin ice but often lull ourselves into a sense of security. Especially in financial matters, we should be careful not to let the ice get too thin. The following examples make me doubt that investors are always aware of the ice they are walking on.

We take results from the past and extrapolate them into the future

An inconsistency from Part I was that we invest in the present to profit from these investments in the future, although we cannot predict what lies ahead. By doing so, we are putting our planned passive income for retirement on thin ice. We all know them, the big speeches about the average annual return of stock markets which is about 7 percent. And yes, looking back, we achieved that number.

But we cannot simply extrapolate it into the future. It’s not always like it was in the COVID-19 crash. The February 2020 crash gave us a month or two of excellent buying opportunities before the stock markets soared to new all-time highs. But this crash was an absolute exception.

History knows other, worse chapters. After the 1929 crash, it took over 9,000 days (25 years) for the S&P 500 to recover fully. Looking at the 2000 stock market crash, it took over 4500 days (12.5 years) for the S&P 500 to finally break through its previous all-time high. So putting it in Nassim Taleb’s words, it is always good to be no turkeys.

The average return, therefore, only considers a specific period. It can be higher for our future, but also significantly lower. Building wealth management on supposedly fixed or expecting guaranteed long-term profits is, therefore, a dangerous gamble if the future depends on these profits.

Averaging down isn’t great

Another popular argument is that investors can put more capital into stocks in the event of a crash. Crashes, so the perspective, can lower the average purchase price for shares. This is why crashes are not only normal but also an event we should be thankful for.

Indeed, the idea of averaging down sounds tempting. Suppose I buy a stock for $/€100. It falls 50 percent. Ouch. Now it has to go up 100 percent to get back to $/€100.

Averaging down means buying an additional share at $/€50. This would have reduced my average price per share to $/€75 ($/€50+$/€100 / 2 purchases = $/€75). To be back in the profit territory with my total position, the share price only has to go up by 50 percent instead of 100 percent.

However, this doesn’t change anything for our first position (the $/€100 purchase). There is no shortcut. The return on invested money will still be negative (25 percent), also with a share price of $/€75 and even if our overall position is positive. The only decisive factor is that the second investment (the $/€50 purchase) performed well and compensated for the losses.

We only have two investment decisions here that balance each other out. I could have achieved the same result by investing in a completely different asset class. So I cannot reduce losses on invested capital by averaging down. At most, I can hide them.

Three years of averaging down

The above does not mean that I refuse to buy stocks whose prices have fallen. Prices are volatile. I like to take advantage of those price fluctuations and then purchase additional shares. Also, after the 1929 crash, things started to pick up again at some point. Investors who persistently and steadily bought more shares achieved nice returns of more than 600 percent until the full recovery (assumed they were lucky enough to pick the shares right at the bottom).

The same was true for the COVID-19 crash which was followed by a really nice rally. But again, keep in mind that the COVID-19 crash and the quick recovery may have been rare events. A bear market can last a long time. From the high in 1929, it took almost three years for the S&P 500 only to bottom.

Averaging down can consequently be a somewhat longer project. The question is whether investors always have the capital and the mindset to stay in the “I am averaging down” business for such a long period:

“Anyone can quote Warren Buffett. Very few have the guts to invest capital in times of crisis.” (Source: Article on Seeking Alpha)

And as I said: it is crucial to understand that averaging down does not reduce losses on invested capital. It only compensates them with a better performance of new invested capital.

So looking back at 1929, the recovery does not change the fact that the previously invested capital, for which someone had to work very hard, brought miserable results for 25 years. Yes, it took 25 years for the capital invested in 1929 to generate a nominal profit. The fact that the capital invested after that has performed better does not change the miserable performance of the initial investment.

To wrap things up, averaging down is not bad per se. But it should only be the consequence of investments, never the cause.

Buying upon price declines to lower the average price per share is BS. In falling for the “I average down” narrative, we ignore the risk to our invested capital. Thus, we’re talking about risk management and unbiased risk analysis.

The “corporate world is bad” narrative

Now it gets interesting. I know I’m standing up against a meaningful narrative that is firmly established in my bubble. I read very often how investors try to break out of their hamster wheel called the corporate world.

It is tempting to say “fuck it”

I also feel the desire just to quit and say “fuck it” sometimes. But after reflecting for a few minutes, I quickly abandon the idea. Ultimately, it’s crazy, and I would go so far as to call it BS. I mean, think about it. I want to invest in companies. But I also want to escape this world simultaneously, which is an apparent inconsistency in my thinking.

Do I hope that other people will fail to escape the wheel? Is it fair to bet on that? Anyway, my point here is not the inconsistency of my thinking (which is covered by Part I) but the danger that arises from it. Because even though it’s tempting to say goodbye to the corporate world, it’s not necessarily the best thing to do from several perspectives.

First, the financial leverage of a career is quite impressive. Second, the despised “corporate world” offers many advantages for developing the right skills and mindsets. These levers need energy, and I can only speak from my perspective. But I think it’s worth putting energy into these levers, especially at a young age.

Why not benefiting from the system I rely on?

My mindset is this: I invest in companies and am a fan of a liberal world. The two things are related. I would not invest in privately organized companies (i.e., the corporate world) if I assumed that a liberal system was terrible or if communism was in place. So my thinking and my capital are connected to these two worlds. Then why should I distance my everyday life and thinking from it and leave only my capital there?

I like the corporate world because it embodies why I invest in stocks. Mister Iron Fist will kick me in the butt if I don’t deliver, and Sir Sugar Carrot will roll out the red carpet if I do. It’s up to me.

And yes, I enjoy the insights I get into companies and personalities as a lawyer. No shareholders meeting in the world could give me the same experience I had as Legal Counsel in a FAANG company. Getting in touch with the DNA and culture of a company this size is a remarkable experience.

It’s stressful, yes, and often the corporate world itself is full of inconsistencies and hypocrisy (the home office debate is a good example). But overall, I benefit from the system, just as the system benefits from me and my time. It is a trade, and I try to make it as much in my favor as possible.

Passive income does not grow on a tree

Passive income does not grow on trees but must be earned. Either through a very high initial capital or a higher return. I have discussed this idea in another article in more depth:

Passive income does not grow on a tree. I have to build its fundament first. And here is the thing. The higher my initial investment, the better and less risky I can leverage my passive income. That is why the rich will become richer and richer. A 10 percent return on a billion is simply more than a 10 percent return on a thousand in absolute terms. Easy math.

Suppose I want to generate $/€5,000 per month by investing in dividend stocks that have a dividend yield of 5 percent. To generate such a return, I would need invested capital of $/€1.2 million. You can already see that there are some difficulties. The biggest challenge is probably where to get that amount of money.

So assuming I only have $/€600,000 which would already be pretty nice. But to achieve a monthly return of $/€5,000, I now need to look for a dividend yield of 10 percent. So what’s happening here is quite typical. I want to leverage the low initial capital with high returns. But the problem with this approach is evident as return always correlates with risk.

It would be much smarter to leverage the absolute return with a high initial capital. And this is where the leverage of active income comes into play.

Active income has a lot of good sides. It allows us the luxury to forego the risky “return lever” and to utilize the “initial capital lever fully”. This reduces the risk at the same time. A dream situation! In this light, the corporate world is no longer as negative as it tends to be.

It thus makes sense to increase the initial capital and accept a lower return or lower risk in return, rather than aiming for a high return or high risk to compensate for the meager initial money.

Side note: Many investors try to build up as many income opportunities as possible, which is also a misconception. Investors are then dancing at several weddings instead of specializing in one thing. And this approach does not even necessarily reduce the risk exposure, nor does a broad field of activity automatically increase the human capital.

The FIRE narrative

The prominence of the FIRE movement also raises the wrong incentives. FIRE in luxury is not possible for many people, as it requires leverage through a lot of capital or a lot of luck (see above). Therefore, many people try to buy FIRE status through frugalism. The victim of this approach is often hedonism and comfort.

Furthermore, FIRE through frugalism can quickly lead to excuses and justifications of one’s life path. Suddenly the higher-hanging grapes are sour and no longer desirable. All of a sudden, champagne doesn’t taste good, and caviar is overkill.

Conversely, I still have doubts that anyone would reject gift wealth. We see this hubris in blogger collogues who propagate FIRE yet convulsively try to market their blog and generate reach on Twitter, YouTube, etc. Of course, they also secretly dream of the millions in advertising revenue.

In the end, this life is a lot like the lives of all those lawyers at prestigious big law firms with their (no less embarrassing) networking efforts on LinkedIn. However, the difference with fellow bloggers is that these lawyers have accumulated a ton of human capital, get enormously high salaries, deal with managers from blue-chip companies, and consume caviar and champagne on a weekly basis.

Accordingly, FIRE adherents should instead focus on accumulating high human capital before focusing on FIRE. Convincing yourself for 50 years that the frugal lifestyle is precisely what you always wanted can be a long hard time, especially if your YouTube idols earn between $/€10,000 and $/€100,000 per month from your clicks.

What part III will be about

We all live in bubbles, and that’s not a bad thing at all. We need to be aware of the mechanisms. As I said in Part I, much is BS… nonsense condensed by repetition. Part II shows that sharing banalities or sayings and the multiple repetitions of subjective views have hazardous potential.

The only solution for me was to break away from the influence of this repetition and information overload and find my way. I am still part of that bubble and still participate in it. However, the difference from before is that I no longer get sidetracked, am more immune to BS, no longer want to lecture people, and don’t chase the Likes. It is all inner balance and living a life in (financial) harmony with the proper narratives.

In recent years I have adapted this thinking more and more and accepted my cognitive limitations. But this disillusionment felt like a catharsis. Acceptance can release power and create space for calm. That’s what happened to me. And that’s where the hope lies. You can be sure that I will detail these aspects in the following Part III of this series.