Calling a thought or statement bullshit (BS) is a radical thing. It is arrogant because it implies supposed superior knowledge. It also indicates a high ground, a looking down on someone or something. And yet, I try to avoid as much of those BS thoughts as possible when making investment decisions. Because, let’s face it, we come into contact with such views, ideas, and their temptations every day. The Internet is full of them, and it’s sometimes hard to escape. So this article is about what I call “bullshit investing” and I apologize to my readers who find the language too radical.

Readers key takeaways:

- My investment world is a bubble that acts as an echo chamber. This bubble compounds the dangers of our cognitive limitations with its inherent filtering and amplifying mechanisms.

- Bullshit, in general, might be tolerable. But we should avoid bullshit investing at all costs. Unfortunately, the relevant bubbles show that many investors are not aware of the hazards that lie in these mechanisms.

- We proudly brand ourselves as frugal or long-term thinking, rational investors. But we are not as generous towards our future as we pretend to be. Instead, we send our future selves onto the uncertain and thin ice of our present state of knowledge.

- Yet, there is hope! Acceptance can release strength and create space for calm. The catharsis arises from the disillusion! That is what happened to me.

- This is a somewhat longer article and Part I of a series. So take some time and get a cup of coffee ready.

An important reason for all the BS lies in the way our world and information systems are organized. We live in huge echo chambers and social bubbles. Value systems and principles govern these worlds. These systems and principles act like filters and amplifiers. They sort out things that do not fit into the value framework. That means that specific thoughts, opinions, etc., do not find their way to us at all. Conversely, those systems amplify information that supposedly corresponds to the basic framework.

Echo chambers are nothing new

What gets less attention in the discussion is that these bubbles and echo chambers are as old as humans. We find them in all communities. Traditions, religions, all these are systems in which the filters and amplifiers mechanisms are at work. We can’t hide from it by not using Twitter or Facebook. Our thinking is part of these mechanisms.

Our ancestors benefited greatly from these. For one’s clan, a common set of fundamental values is a great advantage. While the filter blocks out disruptive elements that could harm the group’s unity, the amplifier emphasizes the common ground.

And indeed, every community has, explicitly or unconsciously, a set of values and is subject to its mechanisms. This also applies to the finance and investment community and the blogging community. I will give a few examples below to show how similar the individual members of this community act.

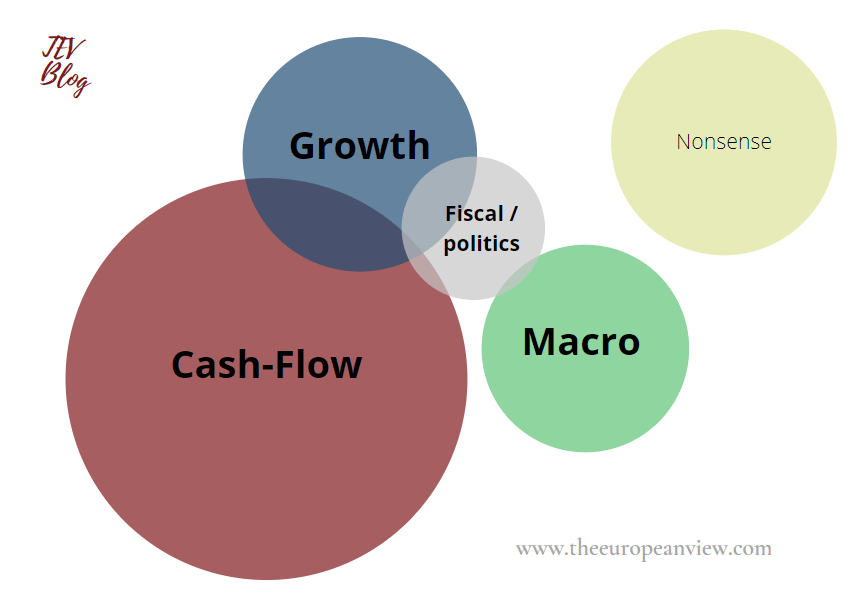

My bubble/bubbles

My bubble in the financial world consists primarily of investors buying dividend stocks. Some additional overlaps exist with growth companies, macroeconomic issues, general economic developments, fiscal issues, and nonsense such as GameStop, crypto, etc. Graphically, my financial world bubble would probably look like this:

Always the same stocks – we bow to aristocrats

We can easily observe how such mechanisms work, especially in the digital world. The network effects at work in platforms are particularly evident here. But I do not want to talk about such systems with this article. The topic has also been widely discussed and spotlighted. I will only touch on the subject as far as it is relevant. Therefore, you will find some short thoughts on the “investing” bubble below.

For example, in my bubble, I notice that we all discuss the same stocks all the time. Take the dividend aristocrats as an example. We use the fact that a company pays dividends for xy many years as a quality criterion. But not only that. We even go the other way around. We eye companies that aren’t aristocrats with suspicion, like our uncle, who we’re not sure if he’s in a good mood or drunk again.

I’m relatively sure that even someone who has no interest in finance will recognize the methodological flaw here. Strictly speaking, the list says nothing at all (we will see why below). My bubble (myself included) falls victim to many tricks that our brain plays on us here. The survival bias is just one of them.

So while I would almost say that many investors are aware of this, most of them do not accept the consequences. Yes, hardly any Dividend Growth Investor decides solely based on this criterion. But that is not enough.

We should stop even asking whether a company is a dividend aristocrat or not. It doesn’t matter. To stop this nonsense would remove a pointless exercise from our due diligence. We can then use the time saved to lie lazily on the couch or take a walk in the fresh air. Still, we don’t stop pointing out in our tweets or analyses that we have a new aristocrat in town. And that’s BS. It’s nothing but nonsense condensed by repetition.

Always the same presentation

The next peculiarity of my bubble is the way it expresses itself. Twitter is an interesting medium because there, we need to compress our thoughts and messages. Accordingly, we share news or views that are supposedly on point. Graphics, one-pager, or similar help us to express these thoughts. I don’t know how many times I’ve seen (or even uploaded myself) a one-pager about 3M, Apple, or Johnson & Johnson. And don’t get me wrong. This isn’t a blame game. I am fully aware that I am a part of it. I like to tweet screenshots of my fair value calculations.

But in the end, it is always the same information that is publicly available anyway. And we can see how the filters and amplifiers work. By sharing the same data always in the same way, we make sure that specific characteristics and patterns of looking at stocks manifest themselves in a group.

The FIRE movement

The FIRE movement shall be my last example. In this community, too, there are precise values and social codes. Consumers are seen as “consumer clowns.” Expensive cars are “clown cars”. A frugal lifestyle is described as desirable, while consumption is rather disgusting.

Followers of the FIRE movement are always reassuring themselves about how much annual return they can achieve with a stock investment. It is believed to be 7 +- 0.5 percent annually. With an investment horizon of 20 years, they say, little can happen. In this time, the amount of $/€125,000 easily grows to $/€1,000,000. Little do they seem to know that it took 25 years for the stock markets to recover after the 1929 crash.

My point here was to raise awareness that we all live in bubbles that affect how we perceive, process, and share information. I will leave it with the above examples. There are more, some of which I will discuss further below and in the following Parts of this series (the narrative “the corporate world is bad” is one).

Inconsistencies characterize our actions and thoughts

We know that we are trapped in bubbles that have their values and mechanisms. This reflection essentially addressed the interaction of individuals within a community and its common sense. Now I want to zoom into these communities a little bit to speak about their members. Among individuals and their ways of thinking, we see a variety of inconsistencies. I want to describe these inconsistencies below but will limit the scope to my financial bubble. As I already said above, I include myself in everything. If I criticize, then I criticize myself first and foremost.

We say we don’t know the future, but discount future cash flows

Knowing Socrates is a great achievement, but we would be even wiser to adapt his thinking. That’s said, we could also take Sir Karl Popper, but Socrates was Greek, and that sounds better than Austrian :).

What they both had in common was their assumption that we could only come close to the truth but never into its possession. So both were very modest (at least in their theory), which I find charming.

A Socratic view of the financial world implies the negation of a prediction. “We know nothing!”. Yes, we don’t know what will happen tomorrow. And we certainly don’t know what will happen in five or ten years. I think a lot of investors are aware of this issue. The full-bodied promise is then not to want to time the market, as this is impossible (that is me, by the way).

However, investors are not willing to take the second step. Why else would they make crazy calculations on future cash flow and discount it as well (that is also totally me)? So we say we don’t know the future but discount future cash flows. Well, that’s crazy… and BS.

I know what you may be saying or thinking now. At least, I would say that we investors somehow have to bring rationality into our investment decisions. Yes, indeed. This question affects the other examples as well, and I will return to it in Part II. I just wanted to disclose it here already so you wouldn’t think I’m overlooking the obvious.

We expect the impact of our decisions in the future but base our choices on today’s knowledge

This point is similar to the one above. As Socratians, we know that we cannot predict the future. This approach must inevitably also apply to the development of share prices. Nevertheless, a common narrative is that it is not we who benefit from our investments but our future selves. And with that, we break a bit with the Socratic logic that we are so proud of.

We also base our decision on today’s knowledge, although we cannot know whether our current assumptions are correct. Our decisions are therefore future-oriented, i.e., they will only take effect later. But we will only know then whether the basis for the decision was correct. And this is somewhat tricky, as you may notice. Because if it turns out in the end that our basis for decision-making was wrong, we can’t go back. So we are not as generous towards our future as we pretend to be. Instead, we send our future selves onto the thin ice of our present state of knowledge.

We reject consumption, but our future depends on the success of consumption – are we hypocrites?

Let’s move on to the next aspect that sometimes leaves me clueless. Especially in the FIRE movement, many investors reject consumption and prefer to invest their savings in stocks. They believe in stable dividend stocks and stocks of defensive consumer goods companies. In addition, they also rush into luxury goods company Louis Vuitton or premium smartphone company Apple. It’s the mentality of “you buy the bag, I’ll buy the stock.”

So we build our investment decisions on the dominance of a lifestyle that we internally reject. This is not necessarily hypocritical because people are free to live the lifestyle they want. But what kind of poor risk management is it when we base our investment on the hope that other people will continue not to live the same (supposedly better) lifestyle as we do? How do we know they won’t change their minds at any time?

We are slaves to our cognitive limits

The above inconsistencies all have a common origin that is deeply rooted in human nature. Humans and the human brain have their limits. One consequence is cognitive biases. My financial thinking and the bubbles in which I am active are full of such cognitive biases. And this is where we get into the BS area. Below I give an overview of some opinions and thoughts that I call BS and yet have myself.

Back-testing is BS – a dive into survival bias

First things first. Back-testing is BS. You will always find data to support your thesis. And so you can also randomly find a data series through back-testing that is supposed to prove a certain outperformance, for example. To understand why back-testing is BS, we need to get familiar with the survival bias.

10,000 apes eating bananas

Survival bias means a cognitive bias in which we tend to tune out the failed. The idea is simple and can be verified with a simple mental experiment. Imagine we give 10,000 apes each day in the morning two bananas.

One banana has a green mark, and one banana has a red mark. The banana stands for the share price prediction of a company XY. The red marking represents a short position, and the green position represents a long position. Each ape is assigned an investor. The investor will take either a short or a long position depending on which banana the monkey eats first. In the evening, each investor closes his position.

The following day, the whole game starts all over again. This time, however, only the ape-investor tandems that made a profit on the previous day are allowed to play, i.e., only those who were correct with their short or long position. Let’s assume that the apes have a 50:50 ratio with their choice of banana, so 50 percent each reach for the banana with the green marking and 50 percent for the banana with the red marking.

So with each run, we will eliminate 50 percent of all tandems from the game. They have failed and will no longer play a part in this experiment. After one round, we have 5,000 tandems left, then 2,500, then 1,250, and so on. In the end, we will have a handful of highly successful tandems. Would you nevertheless put money on one of the tandems? Why should you? The success was pure luck. A rather sad realization arises from this simple experiment, which we should already know but obviously constantly ignore.

The very, very sad consequence: Is outperformance based on luck?

The above thought experiment suggests that all our shining lights and role models like Bill Ackmann or Warren Buffett were, in the end, only those who were most fortunate not to be among the forgotten failures.

But we don’t need to look at individual investors; we can also look at strategies. The outperformance of a particular strategy is not indicative of its future superiority. The fact that tech stocks or dividend stocks have outperformed the S&P 500 in the last xy years does not indicate that they will do so in the following years.

The entire technical analysis, by the way, is based on the analysis of patterns that have survived over the years because of luck, coincidence, and self-fulfilling prophecy. Until a pattern becomes the forgotten failed (“sell in May”).

At this point, followers of a particular strategy often attach a graph that confirms the outperformance of their strategy. Let’s take the Dividend Growth Investing approach as an example. Advocates of this strategy, like me, say that they also use quantitative or qualitative criteria and not just the years of dividend payments. They then refer to a chart that proves that such a strategy outperforms in the long run. But this is circular reasoning and proves nothing.

Unfortunately, I have to admit that most attempts to justify this strategy end up being circular arguments (at least if our benchmark is outperformance).

10,000 apes vs. a professional soccer team

I resisted this conclusion for a long time. My argument was always the following thought: Suppose a professional soccer team plays against an old-men’s team. The professional team has already won 99 games out of 99. Would I not bet on the professional team for the 100th game only because past performance says nothing about future performance? No, I wouldn’t. That would probably be far too defensive even for me.

This comparison had a crucial pitfall. The keyword here is “ludic fallacy”, or “the misuse of games to model real-life situations,” as Nassim Nicholas Taleb would describe it. The mistake was that I applied the rules of a simple game in a well-defined world to the highly complex wealth management. I had compared two different worlds with different rules and mechanics.

A well-defined world vs. highly complex wealth management

In my soccer example, two teams with 11 individuals each face each other, whereby 11 individuals each pursue a mutual goal and act accordingly in a uniform manner. Furthermore, the rules are set, and the qualities are also known through measurable decisive criteria (age, speed, etc.). This was one world.

Investing and wealth management are more complicated and part of a much more complex and fragile world than a simple soccer game. So I had to accept that my soccer=investing analogy is BS. Since then, I have never tried again to find a rationale or narrative for why something or someone will outperform in the future.

Expectations are BS, and so are forecasts

We can only draw one conclusion from the above, and there is a reason why I am closing the first part of this series with this note. Expectations are BS, and so are forecasts!

With this, we can eliminate a vast number of narratives from our minds. The sad thing is that these narratives are sometimes the reason why we make investment decisions. It might be challenging, but we have to forget that stock markets bring a performance of 7 percent per year over the long term. We have to say goodbye to any extrapolation of past performance into the future. It is all BS. And we have to accept that any outperformance is most likely luck.

When disillusion becomes catharsis

I have adapted this thinking more and more in recent years and accepted my cognitive limitations. But this disillusionment felt like a catharsis. Acceptance can release strength and create space for calm. That is exactly what happened to me. And that’s where the hope lies. You can be sure that I will go into these aspects in more depth in the following articles of this series.

To be continued…

Thanks, this is a great article. Looking forward to the next part.

Thanks, Microscob!

Part II is in the making.

Best regards

I saw your post on Twitter. Well written piece although I disagree here and there. But it makes you think and that is worth a lot these days.

Thanks!

Thanks for coming by, Dennis, and leaving a comment! Well appreciated.

Hi TEV,

great article. I really appreciate your work!

Thanks a lot!

Hi Vic, thanks for coming by! Always well appreciated.

Best!

[…] Dividendenerhöhungen kein Qualitätsmerkmal ist und bei einer Investitionsentscheidung keine Rolle spielen sollte. Diese Ansicht vertritt auch Torsten Tiedt in einem neu veröffentlichten Video, in dem es um die […]