Even after more than 20 years, it is still challenging to analyze the Deutsche Telekom stock without partly mocking references to its IPOs in the 1990s. Deutsche Telekom was promoted with a lot of hype as a so-called share for the common people. In the end, however, a whole generation of shareholders had severely burnt their fingers. Driven by unprecedented hype, greed, and the fear of missing out on profits, the price climbed to almost EUR 105 between 1996 and spring 2000. High levels of debt due to failed takeovers (including a certain VoiceStream in the U.S.) and poor business in the wake of the bursting dotcom bubble ultimately led shareholders to turn their backs on the stock market and send Deutsche Telekom’s share price down to EUR 10.

With this introduction, I would like to welcome you to my latest stock analysis. In this analysis, we show you what you can expect when you put Deutsche Telekom in your portfolio and what you better not hope for.

If you don’t want to miss any new articles or analysis, you can easily follow me on

or Twitter.

Deutsche Telekom – few private investors, much state

Many years after Deutsche Telekom crashed badly, the company still does not attract any shareholders, but in the meantime, it has become a very solid company. It can be considered as an interesting component of a portfolio. Deutsche Telekom is one of the largest telecommunications companies in the world. In the course of the privatization of the Federal Post, which was decided in 1994, the Telecommunications and Telecommunications Division was liberated and promoted as a people’s share when it went public.

However, you can see from the current shareholder structure that Deutsche Telekom shares are far from being a stock for the common people today since private investors hold just 16 percent of the shares. The largest shareholder is still the Federal Republic of Germany, which, together with the federally owned KfW Bankengruppe (KfW banking group), holds one-third of the shares.

Keeping companies with such a high level of state ownership in your portfolio has advantages and disadvantages. A disadvantage is the danger of political interference in business decisions, manifested in the appointments to Deutsche Telekom’s Supervisory Board. For example, Dr. Rolf Bösinger is a State Secretary in the Federal Ministry of Finance. Dr. Günther Bräuning is also the Board of Managing Directors of the federally owned KfW Bank. For me, however, the advantages outweigh the disadvantages. For a telecommunications company that is subject to massive state regulation, it can be advantageous to have a close relationship with politicians to make one’ s concerns heard and understood. Besides, the high level of government shareholding has a stabilizing effect on the share price.

Deutsche Telekom stock analysis: How Deutsche Telekom makes money

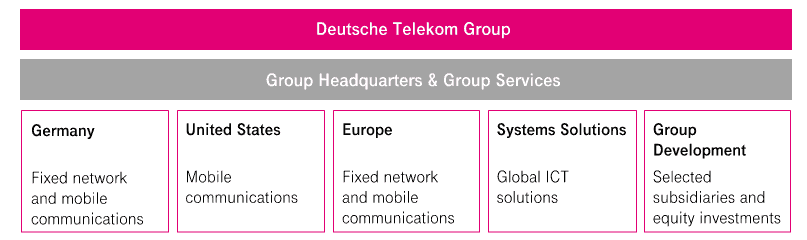

Deutsche Telkom is a traditional telecommunications company that offers its customers products and services in network/broadband, mobile communications, Internet and Internet-based television, and solutions in the field of information and communications technology (ICT). The company currently has 184 million mobile phone and 21 million broadband customers. It also has 28 million fixed-network lines. Deutsche Telekom divides its business into the following segments:

By far, the most important segment in terms of revenue is the “United States” segment, which contributes around half of the company’s revenue. In this analysis, I will deal with the United States segment and the Systems Solutions segment in detail.

The “United States” segment: T-Mobile US rocks

In the United States segment, Deutsche Telekom conducts its business primarily through its subsidiary T-Mobile US. T-Mobile US emerged from VoiceStream, which Deutsche Telekom acquired for DM 106 billion in 2000. Deutsche Telekom took a heavy beating for this costly takeover in the first few years, especially as the number of customers at the U.S. subsidiary continued to fall, and revenues plummeted. Several attempts to get rid of the distressed subsidiary by selling it to AT&T failed due to resistance from the US antitrust authorities. In retrospect, the failed attempts to sell were a stroke of luck for the company.

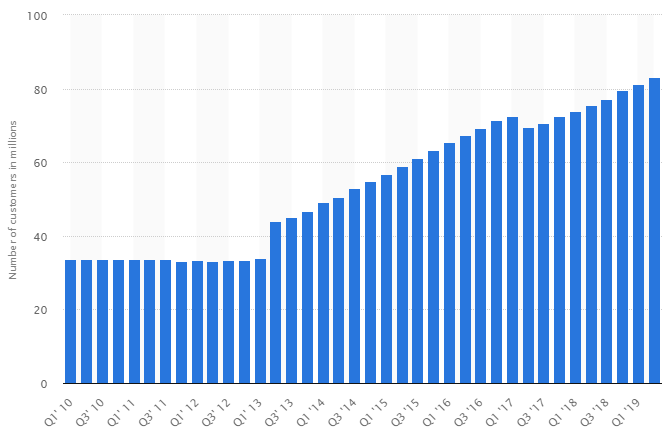

In 2012, John Legere took the wheel at T-Mobile US and developed the “un-carrier” strategy with the French marketing company Publicis. Carriers are the telecommunications giants in the U.S. who, until then, shared a bad reputation for customer service. With its un-carrier strategy, T-Mobile US stirred up the industry and attacked the much larger competitors AT&T and Sprint head-on. For example, rates and contract terms were radically simplified and made much more customer-friendly. One example is the Jump trade program introduced by John Legere in 2013, which allows customers to swap their smartphones for a new model for ten dollars every six months. The new customer orientation has resulted in a growing number of customers in almost every quarter:

Thanks to John Legere, who stepped down as CEO of T-Mobile US this spring, the once ugly duckling has become a magnificent swan and Deutsche Telekom’s most valuable asset. T-Mobile US’s business has also improved fundamentally from year to year. As you can see, revenue at T-Mobile US is growing in line with the number of customers. Earnings per share also rose significantly from 2014, contributing to Deutsche Telekom’s success.

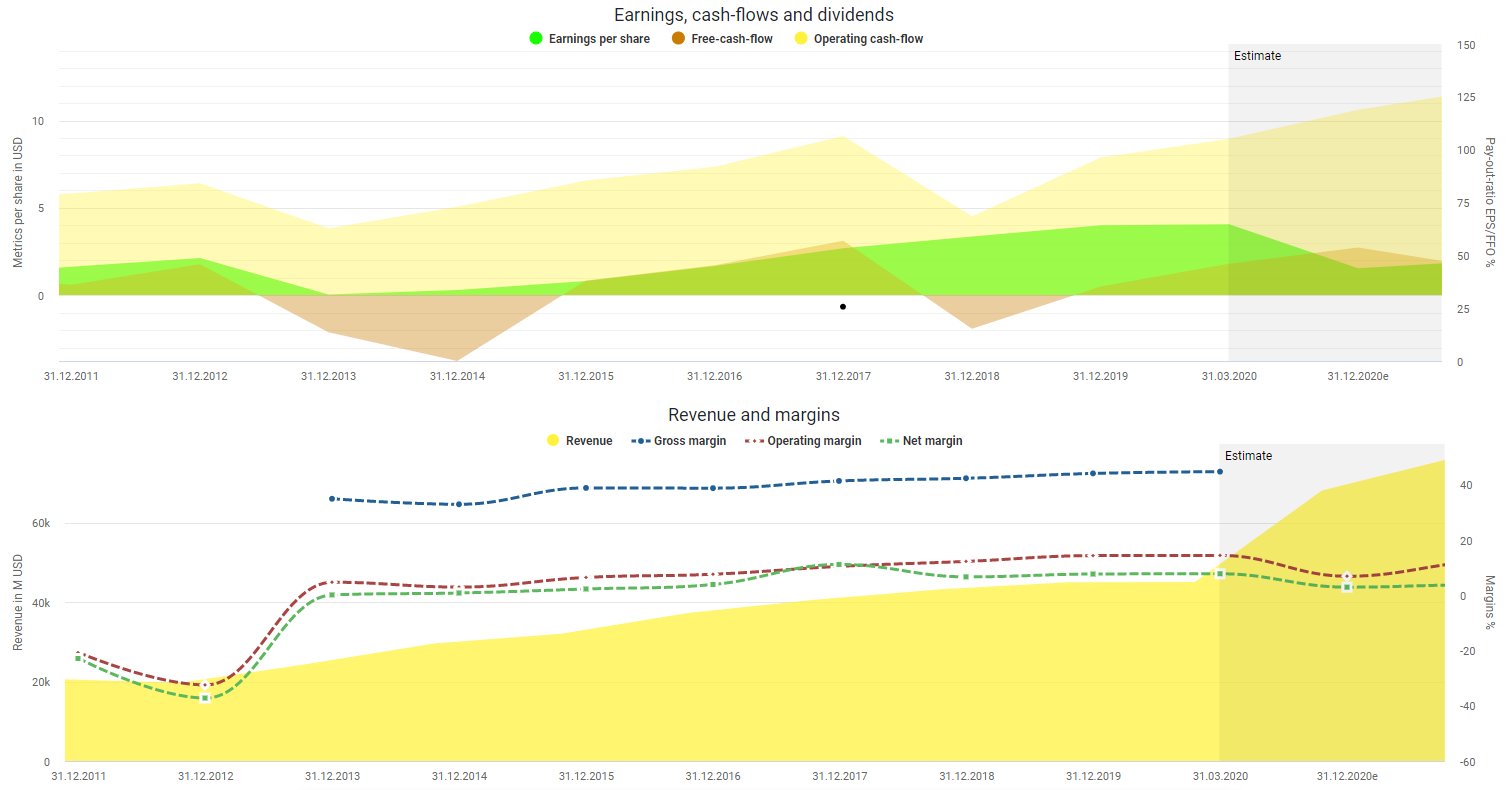

Thrilled by the success of its subsidiary, Deutsche Telekom changed its strategy. Instead of selling off the T-Mobile US, Deutsche Telekom provided the company with fresh capital on several occasions, such as the 2017 frequency auction. The masterpiece was most recently the marriage between T-Mobile US and its U.S. competitor Sprint. The sharp increase in revenue forecast, coupled with a simultaneous decline in margins and profits,is a direct result of T-Mobile US’s acquisition of former competitor Sprint.

In 2018, after some back and forth, Sprint’s parent company SoftBank and Deutsche Telekom announced their intention to merge. The plan was for Deutsche Telekom to receive 42 percent and SoftBank 27 percent of the shares in the new company. Through a voting rights agreement, Deutsche Telekom was to continue to control the new company. However, Deutsche Telekom will be able to increase its share in the new T-Mobile US due to an acute shortage of money at SoftBank. SoftBank has made a bad gamble with expensive investments such as its investments in Uber or WeWork (and ultimately Wirecard) and decided to obtain cash by selling T-Mobile US shares, which is why both companies have renegotiated the deal significantly.

The deal now provides for the following details: As SoftBank is disposing of its T-Mobile US shares at an early stage, Deutsche Telekom will receive not only a payment of $300 million but also extensive options on T-Mobile US shares, which will allow the company to acquire further shares within the next four years and thus obtain an absolute majority stake in the new company. 40 percent of these options are linked to a fixed price of USD 103 per T-Mobile US share.

From an economic perspective, the merger of T-Mobile and Sprint, which was paid for only with shares and not cash, makes perfect sense. Deutsche Telekom expects synergies with a total cash value of $43 billion and hopes to be able to attack the top dogs AT&T and Verizon more effectively. But first, Sprint has to be integrated into T-Mobile US, and that costs. Deutsche Telekom estimates the amount at around $15 billion.

The “Systems Solutions” segment: Deutsche Telekom’s problem child

While T-Mobile US became a valuable asset, the Systems Solutions segment remains a problem child for Deutsche Telekom. Within this segment, Deutsche Telekom offers products and services in information and communications technology through its subsidiary T-Systems. This includes the provision and maintenance of networks and IT equipment, as well as cloud infrastructure or security solutions.

T-Systems’ customers are, for example, Deutsche Post AG and DHL, Daimler, Volkswagen, Shell, Philips, and Airbus. The segment is currently in a state of upheaval after years of declining orders. The new CEO, Adel Al-Saleh, is to clean up the situation, make the business more profitable and get it back on track for growth. A small success was achieved recently. In the first quarter of 2020, the subsidiary recorded order growth of 3.4 percent compared with the same quarter of the previous year. EBITDA also increased by 8.7 percent. However, only the future will show whether this development will be sustainable.

Rising revenues and profits for Deutsche Telekom?

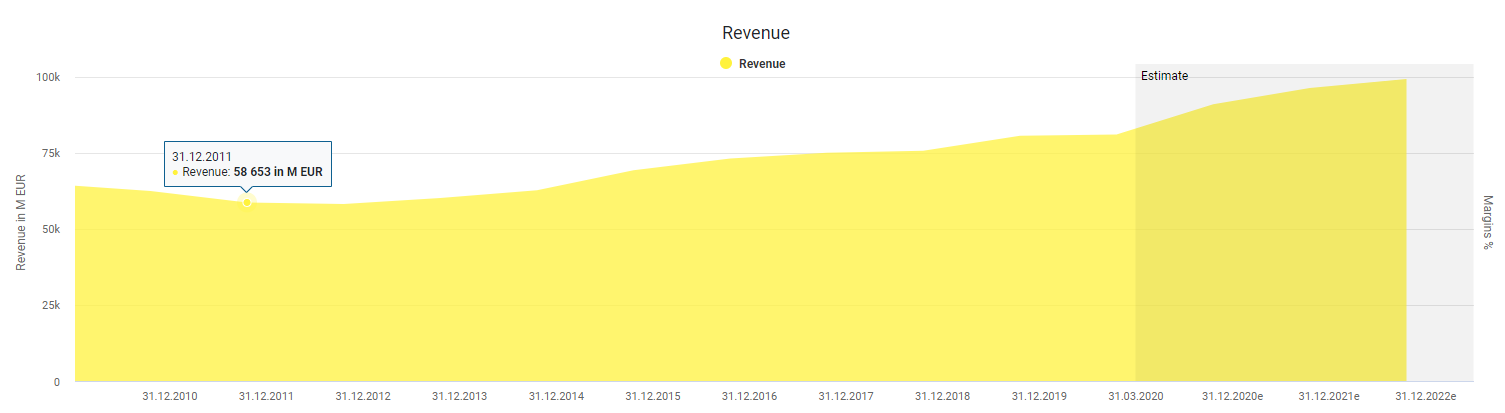

Deutsche Telekom can look back on the past few years with confidence. The company has increased its revenue from €58 billion in 2011 to over €80 billion in 2019.

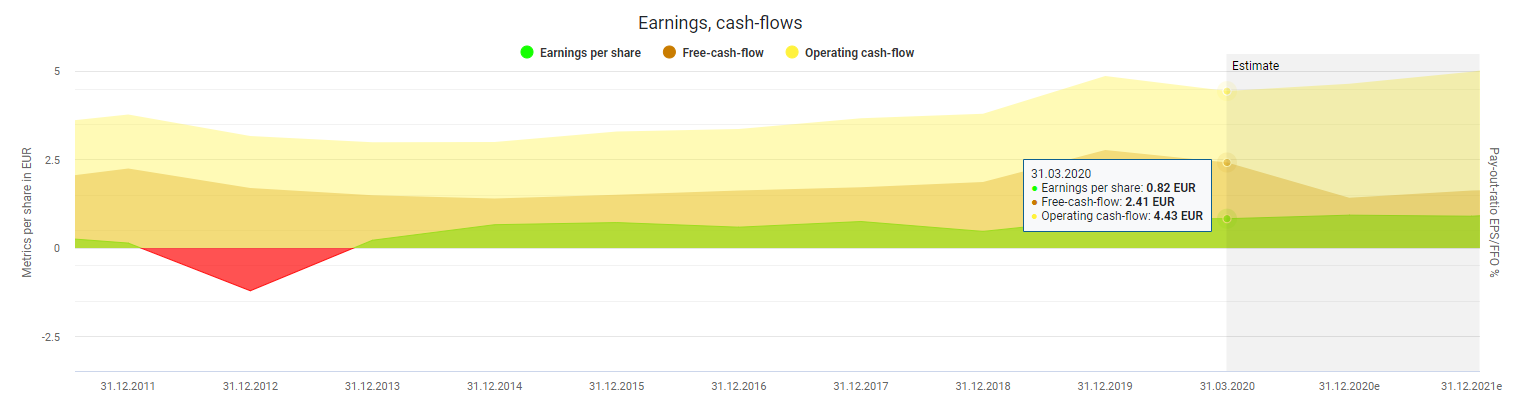

The T-Mobile US subsidiary is primarily responsible for this growth. The company is still growing strongly and has increased its revenue by a good 10 percent in 2019. As we have seen above, T-Mobile US now accounts for around 50 percent of total revenue, and the acquisition of Sprint is driving revenue growth. Thanks to positive margins, the rising revenues are contributing to Deutsche Telekom’s profit growth. There has not been a loss-making year since 2013. However, you shouldn’t expect explosive earnings growth in Deutsche Telekom shares. Presumably, it will continue with a leisurely positive profit increase. Accordingly, the management expects profit growth of between 2 and 4 percent. Cash flow is expected to increase by 10 percent per year.

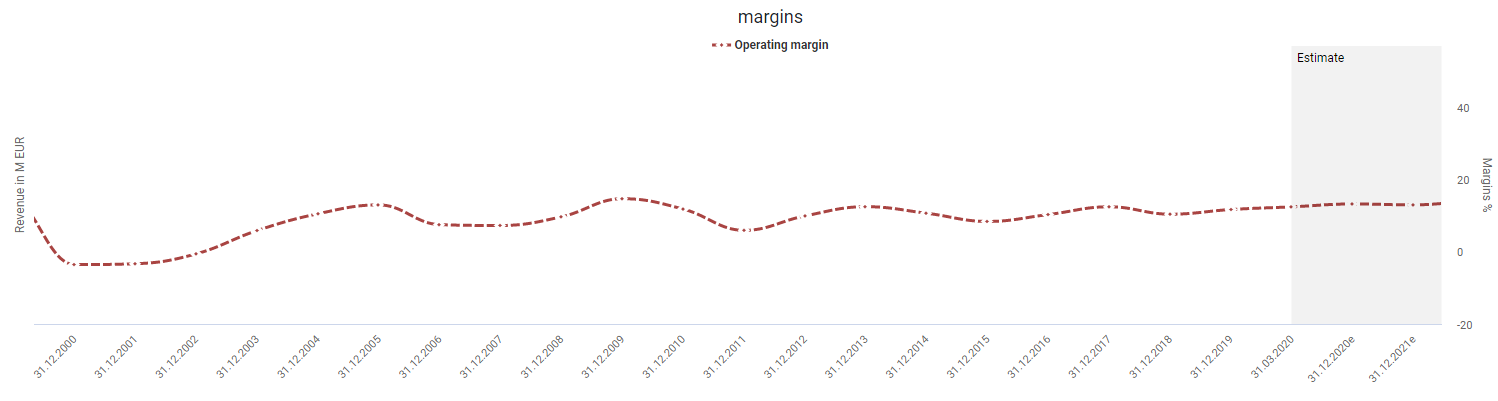

If you look at the margins, you can see the meager margins at the beginning of 2000, after which the operating margin fluctuated between 15 and 6 percent for years, only to settle between 10 and 12 percent in recent years. The low net margin is typical for capital-intensive companies, and Deutsche Telekom has to shoulder extremely high investments. For example, it finances the expensive 5G auctions for its subsidiaries worldwide and must also keep money available for infrastructure expansion. For example, in Germany, management has put more than two billion euros on the table for 5G frequencies. In Austria, Deutsche Telekom also plans to invest one billion euros in 5G expansion by 2021.

Deutsche Telekom stock analysis: How safe is the Deutsche Telekom dividend?

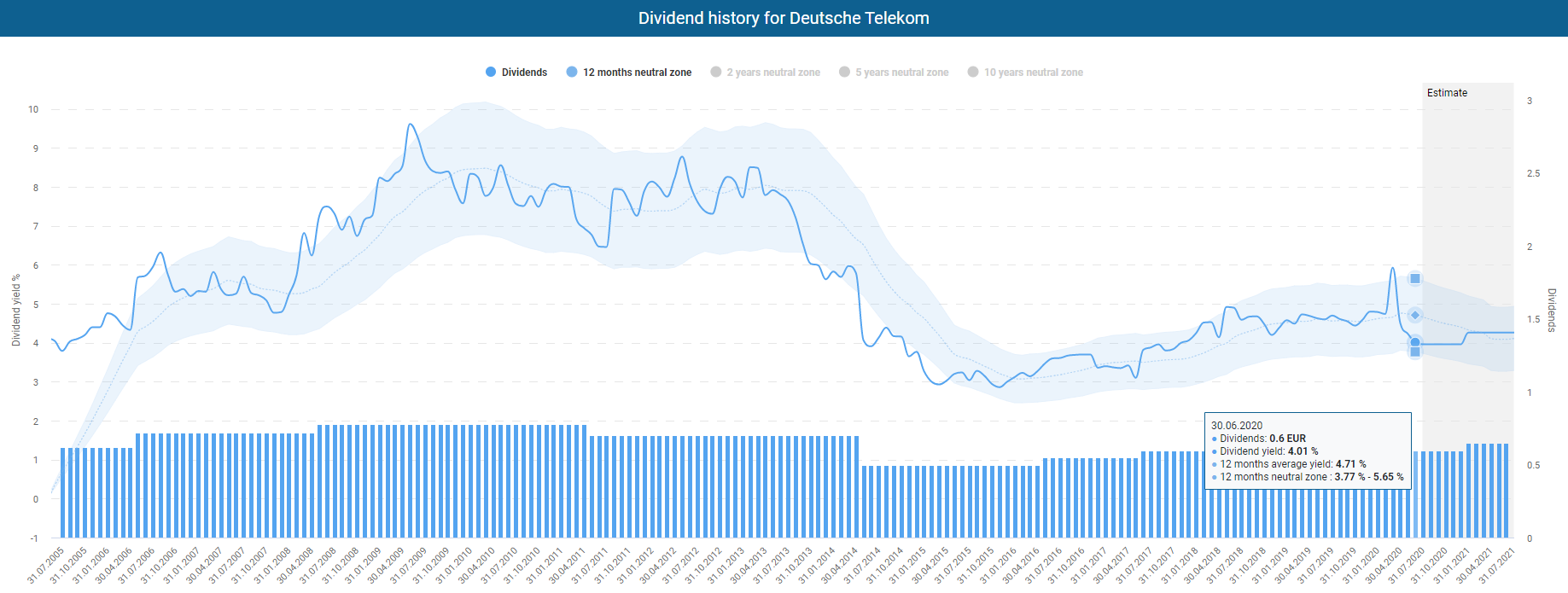

With all the necessary investments, you can get anxious and fearful about the dividend as a shareholder. Like many telecommunications companies, Deutsche Telekom is a reliable dividend payer with a traditionally high dividend yield. However, the amount can fluctuate. So you shouldn’t buy the stock if you hope that Deutsche Telekom will one day belong to the illustrious circle of dividend kings or aristocrats like his colleagues AT&T and Verizon from the USA.

Since 2005, the payouts have fluctuated between €0.50 and €0.78 per share. Most recently, management reduced the payout from €0.70 to €0.60 due to the merger with Sprint and heavy investment in 5G rollout. Despite the cut, this results in a handsome dividend yield of 4 percent. However, this puts Deutsche Telekom’s dividend at the lower end of its historical corridor.

Furthermore, the management plans to pay a minimum dividend of €0.60 for 2020 and 2021. In the future, the increase in the payout is to be based on the development of adjusted earnings. After several transitional years, management expects significant growth in profit after completing the merger of T-Mobile US and Sprint. Accordingly, I consider a dividend payment of EUR 0.60 per share and a return of 4 percent to be likely in the coming years.

Is the Deutsche Telekom stock reasonably valued?

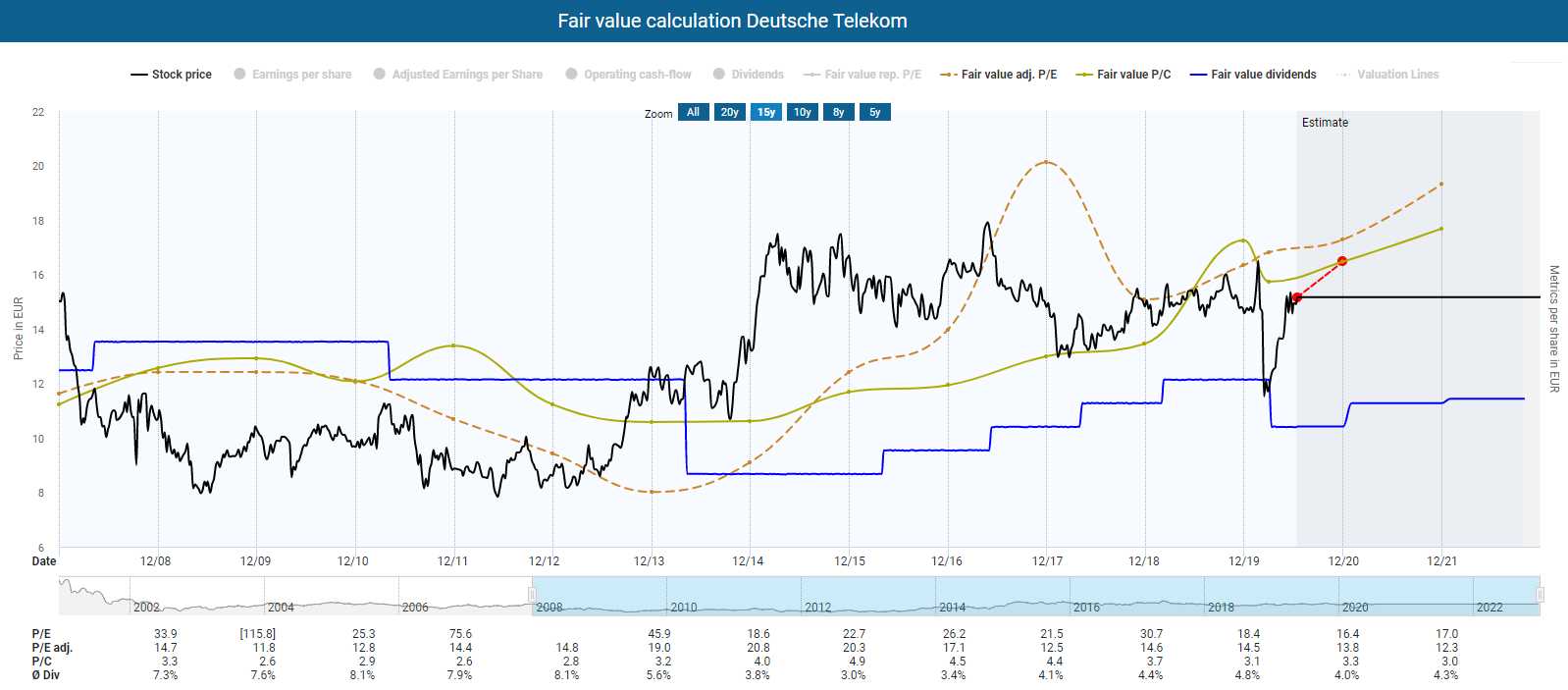

If you look at the Deutsche Telekom stock’s within a more extended valuation period, you will see that the stock moves in waves around its fair share price based on adjusted earnings. Currently, the share price is again below this fair value of just under EUR 17, which means that there is a short-term upward potential of 14 percent based on the current share price. The same applies if you look at the fair value based on the cash flow. As already mentioned, Deutsche Telekom’s current dividend is slightly below the historical average, which is reflected in an overvaluation of the share based on the fair value dividend. On the other hand, the reported profit is not suitable for the stock valuation because it is very susceptible to fluctuations, mainly due to depreciation and amortization, and is therefore unreliable.

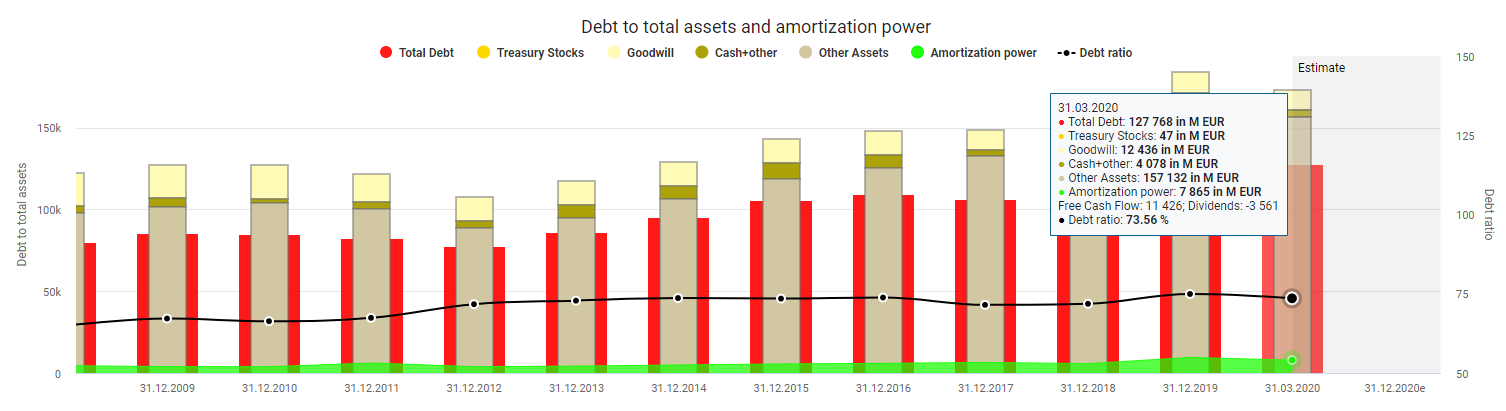

However, the market may be taking a discount on the share. Above all, the investments the company will have to make and the already relatively high level of debt of over 73 percent are a particular deterrent. Including all liabilities, Deutsche Telekom is sitting on a mountain of debt of almost EUR 130 billion, which is contrasted by an amortization power of just €8 billion.

Nevertheless, such high investments are not unusual for Deutsche Telekom as a telecommunications company. The company is also keen to maintainliquidity reserves that cover refinancing requirements for the next two years. With a stable A-/BBB rating and the Federal Republic of Germany as anchor shareholder, which holds two-thirds of the company, Deutsche Telekom comes close to the so-called high-grade bonds, which are bonds that receive high credit ratings from the rating agencies. I, therefore, like to compare Deutsche Telekom with a bond of this kind and believe that the share is currently fairly valued.

After all, with Deutsche Telekom shares you receive a relatively secure dividend of around 4 percent. Please bear in mind that the dividend cut was a strategic decision by management. You can add to the dividend yield another estimated 2 to 4 percent profit growth and 10 percent growth in cash flow per year on top of that. If we calculate conservatively, we can expect a return of 6 percent, maybe a bit more. If we look at the average annual return of various asset classes since 1995, Deutsche Telekom is currently offering you a higher yield than the aforementioned high-grade bonds.

Conclusion Deutsche Telekom stock analysis

When Deutsche Telekom went public, banks, the press, and small investors praised the stock to the skies. Investors who bought the stock with lofty prices had to learn the hard way. But these spectacular times are history. Deutsche Telekom is now a rock-solid company with good investor relations and a good management team. It all seems boring and probably won’t bring you a dream return like Amazon. However, if you compare Deutsche Telekom to a high-grade bond, it is worth buying. Besides, the Federal Republic as anchor shareholder should stabilize the share price if necessary. Furthermore, the merger of T-Mobile US and Sprint and the introduction of 5G should provide potential upside potential.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

Thanks for the analysis. I’ve been looking at DTE because of the dividend. I think they hold one third and not two thirds (17% + 14%) and general public 45%, the rest institutions. Never the less my concern is debt and the 5G. From recent press you know that “Europe’s largest telecom operator Deutsche Telekom faces political pushback in Germany over new reports about its close relationship with Chinese 5G vendor Huawei.”

This could be a big problem. Let us hearing them on the 13 August.

What do you think about the truck and e-bus company TRATON,WW subsidiary, good peg, good per, debt under control despite corona, just released H1 results and announced div of 1€ per share, just over 6% yield and will be approved at the AG on September.No news from Navistar deal yet.

Joao Luz

Hi João Luz,

many thanks for coming by. You’re absolutely right. I was color-blind for a moment 🙂 It’s fixed.

Indeed, I am curious myself how things will go with Huawei. This could complicate the roll-out of 5G in Europe. Nevertheless, revenue coming from Huawei is declining. Furthermore, DTE said that the share of Chinese equipment currently stands at 25 percent in Europe. But indeed, we will have to see. For the time being, I will hold my shares.

Concerning Traton, I have never been intensively involved with the company. The whole industry is too cyclical and too discontinuous for me. However, the company is probably worth a look. Thanks for the advice!

All the best,

TEV