Hello, my dears, welcome to a new overview of upcoming ex-dividend dates and dividend ideas in TEV’s ex-dividend calendar. Like every week, I want to show you some stocks that will go ex-dividend in the next days. I’ll also review a few companies that are currently in the focus of investors or that have an attractive fundamental valuation. Additionally, I’ll give you some insights into my retirement portfolio and/or share my thoughts and experiences about individual companies with you.

Why yields are a simple way to screen companies

Dividends are a great thing. Even in bad stock market times, they provide a juicy cash flow per month. If you want to benefit from dividend payments as quickly as possible, you must pay attention to the ex-dividend dates. This date is the day on which shares are traded without their subsequent dividend value. Only if you owned the stocks on this day are you entitled to receive the dividend.

Usually, there are always exciting dividend companies that are worth a second look. And the dividend yield is an excellent way to get an initial overview of companies that may be worth further due diligence. To help you get started, at the end of each week, I will publish the ex-dividend dates for the coming week of individual companies here in the TEV blog.

Why I handpick and double-check the upcoming ex-dividend dates next week

I have recently noticed that many databases do not indicate the respective numbers and dates correctly. Spontaneous dividend cuts, in particular, are only partially taken into account, or in some cases, not at all. As a result, the value of such overviews dwindles enormously.

Therefore, I’ve decided to select individual companies by hand and check the dates and dividend yields on the companies’ websites, which means more work for me but increases the value of this section enormously, so it is worth it 🙂

Because I’ve been asked about it by some of the readers: I don’t decide my investments based on whether a company goes ex-dividend or not. This overview is simply a way to screen companies regularly. By double-checking the current dividend yields, I scan the business development of companies more or less once a quarter and see if anything significant has changed in the companies. In the end, however, comprehensive due diligence always decides whether I invest or not.

Ex-Dividend Calendar (41th calendar week)

As always, you’ll find some handpicked exciting ex-dividend dates below.

| Company | Payment Date | Yield | In my retirement portfolio |

|---|---|---|---|

| Monday, October 05, 2020 | |||

| Agilent Technologies (A) | October 28, 2020 | 0.72% | NO |

| Bank of Nova Scotia (BNS) | October 28, 2020 | 6.55% | NO |

| Dollar General (DG) | October 20, 2020 | 0.7% | NO |

| John Wiley & Sons (JW) | October 21, 2020 | 4.37% | NO |

| JPMorgan Chase & Co. (JPM) | October 31, 2020 | 3.78% | NO |

| Sanderson Farms (SAFM) | October 20, 2020 | 1.52% | NO |

| Tuesday, October 06, 2020 | |||

| Brandywine Realty Trust (BDN) | October 13, 2020 | 0.25% | NO |

| Comcast Corp.(CMCSA) | October 28, 2020 | 2% | NO |

| New York Times (NYT) | October 22, 2020 | 0.57% | NO |

| Progressive (PGR) | October 15, 2020 | 2.81% | NO |

| Wednesday, October 07, 2020 | |||

| Campbell Soup (CPB) | November 02, 2020 | 2.9% | NO |

| City Office REIT Inc. (CIO) | October 22, 2020 | 8% | NO |

| Kinross Gold Corp. (KGC) | October 22, 2020 | 1.35% | NO |

| Oracle Corp. (ORCL) | October 22, 2020 | 1.61% | NO |

| Thursday, October 08, 2020 | |||

| AT&T (T) | November 02, 2020 | 7.35% | YES |

| Brady (BRC) | October 30, 2020 | 2.22% | NO |

| General Dynamics Corp. (GD) | November 13, 2020 | 3.2% | YES |

| General Mills (GIS) | November 02, 2020 | 3.41% | YES |

| Mastercard (MA) | November 09, 2020 | 0.5% | NO |

| Marvell (MRVL) | October 28, 2020 | 0.61% | NO |

| NetApp Inc. (NTAP) | October 28, 2020 | 4.36% | NO |

| Johnson Outdoors (JOUT) | October 23, 2020 | 1% | NO |

| Simon Property Group (SPG) | October 23, 2020 | 7.9% | YES |

| The Toronto-Dominion Bank (TD) | October 31, 2020 | 5.24% | NO |

| Toll Brothers (TOL) | October 23, 2020 | 0.93% | NO |

| Universal Corp. (UVV) | November 02, 2020 | 7.4% | NO |

| Verizon (VZ) | November 02, 2020 | 4.24% | NO |

| Waddell & Reed Financial Inc. (WDR) | November 02, 2020 | 6.8% | NO |

| Friday, October 09, 2020 | |||

| Accenture (ACN) | November 13, 2020 | 1.46% | NO |

| Oge Energy (OGE) | October 30, 2020 | 5.43% | NO |

Is John Wiley & Sons a long-term value play?

The company is a US-American publishing company that is primarily active in the field of academic literature. It is very old and was already founded in 1807. The founder was Charles Wiley, who founded the company in Manhatten. Initially, the company published literary books by authors such as Washington Irving, Herman Melville, and Edgar Allan Poe. Later, the company shifted its focus more and more into the scientific and academic fields. John Wiley & Sons has always increased its dividend over the last 22 years. The current yield is 4.32 percent.

What is the business of John Wiley & Sons?

John Wiley & Sons operates through three segments: Research & Platforms, Professional Development, and Education. The company pursues the following activities with the individual segments:

- In the Research & Platforms segment, John Wiley & Sons provides digital and print scientific, technical, medical, scholarly journals, reference works, database services, books, and advertising. In 2019, for example, the company published approximately 1,675 academic research journals. The sub-segment “Research Platforms” mainly includes Atypon. Atypon is a publishing software and service provider that enables scholarly and professional societies and publishers to deliver, host, enhance, market, and manage their content on the web.

- The Professional Development segment includes digital and print books, solutions for corporate learning, training and test prep services, employment talent solutions, and certification programs.

- The Education segment contains print and digital content and education solutions such as services for online program management for higher education institutions and course management tools for instructors and students.

The company is thus active in the scientific and academic fields. In itself, this is a great thing. Humanity is evolving more and more into data-driven knowledge societies. High market barriers also characterize these markets. Maybe you remember your school or study time. It was always the same books, in doubt, even the books your older siblings had already worked with. Nevertheless, there are some risks you should be aware of and which we will look at in more detail below.

The business-related risks

The share price already shows you that the market is not satisfied with the company, which is also true for the competitor Pearson.

The publishing world is struggling with serious problems. One problem is the long-term trend towards digital media consumption. Another problem is the short-term effects of the coronavirus. The general issues John Wiley & Sons is struggling with are explicitly mentioned in the last annual filing:

A common trend facing each of our businesses is the digitization of content and proliferation of distribution channels through the internet and other electronic means, which are replacing traditional print formats. New distribution channels, such as digital formats, the internet, online retailers, and growing delivery platforms (e.g. tablets and e-readers), combined with the concentration of retailer power, present both risks and opportunities to our traditional publishing models, potentially impacting both sales volumes and pricing.

As the market has shifted to digital products, customer expectations for lower-priced products have increased due to customer awareness of reductions in production costs, and the availability of free or low-cost digital content and products. As a result, there has been pressure to sell digital versions of products at prices below their print versions. Due to growing student demand for less expensive textbooks, many college bookstores, online retailers, and other entities offer used or rental textbooks to students at lower prices than new textbooks. The internet has made the used and rental textbook markets more efficient and has significantly increased student access to used and rental books.

The COVID-19 related risks

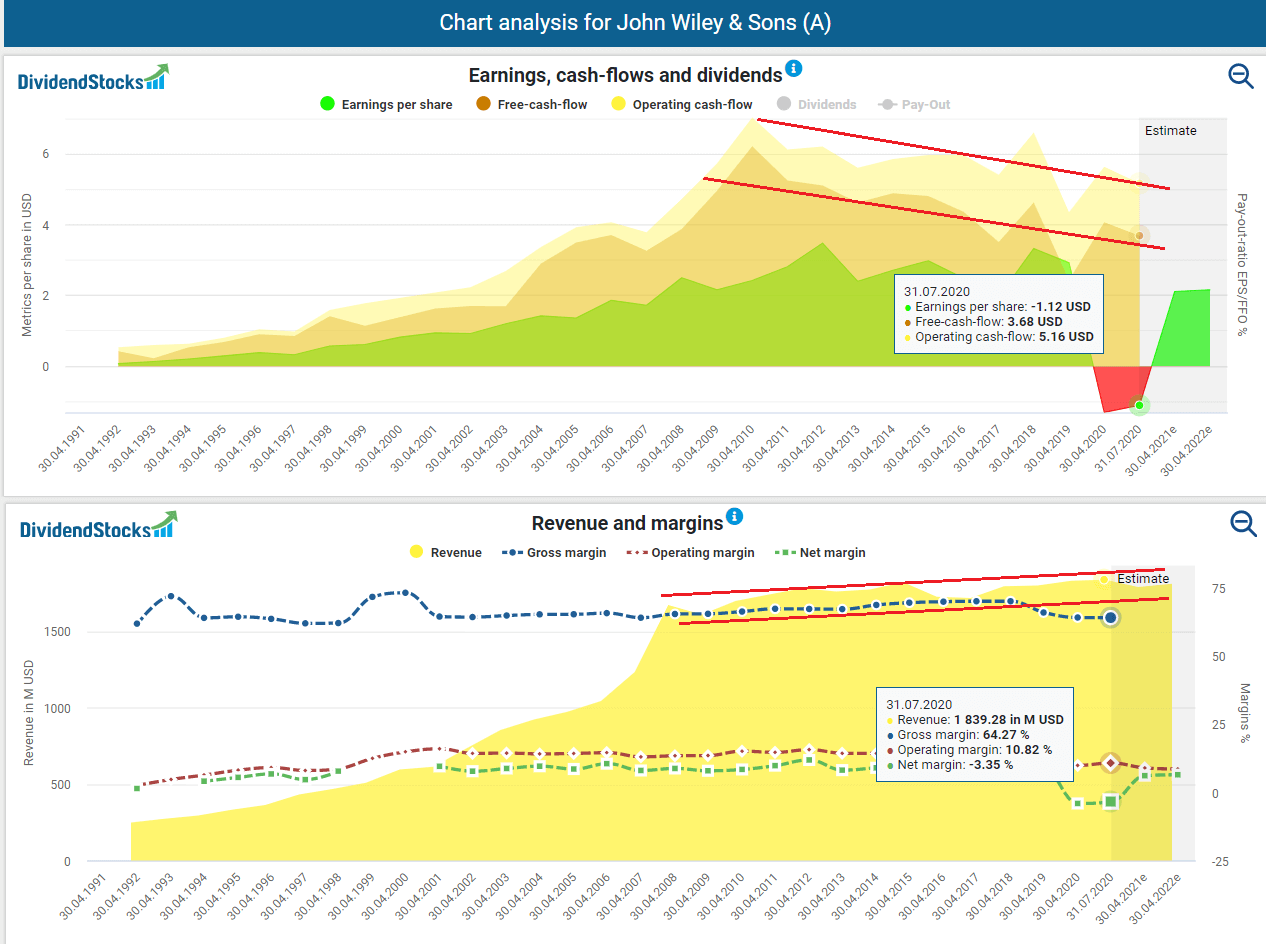

Of course, the coronavirus had (partly) also adverse effects on John Wiley & Sons. In the fourth quarter, adj. EPS was down 44 percent, and adj. EBITDA 23 percent. Revenue was down 2 percent. Concerning the operative business as a whole and according to the company’s filing, the coronavirus will have different effects for its fiscal year 2021:

- As far as the Research Publishing & Platforms is concerned, John Wiley & Sons anticipates (without any quantification) that COVID-related budget constraints at libraries will result in pricing pressure for 2021. This pressure is expected to be offset by continued strong growth in open access, research platforms, and corporate solutions. The company thinks that this positive development offsets this pressure.

- In Academic & Professional Learning, the company expects that print book sales will continue to be challenged by COVID lockdowns and enrollment declines. In contrast, digital content and courseware will continue to grow strongly. According to the company, the recovery in test prep and corporate training will be dependent on the reopening of physical sites.

- Concerning the Education Services, the company expects that universities continue to operate in a hybrid or virtual learning environment while dealing with financial shortfalls related to COVID-related enrollment declines.

Over the last 200 years, the company has often shown that it can adapt to changing events and upheavals. But that is, of course, no guarantee that it will happen again. What makes me feel uncomfortable here is that information, as such, has no legal protection. Open access and the easy distribution of information threaten the core foundation of the business.

Growth and profitability

Although the company had to face the rough fiscal year 2020, it managed to grow at least in revenue, which was up 3 percent. On the profit side, however, things are different. Here, adj. EPS was down 21 percent, and adj. EBITDA was down 8 percent. But even before the coronavirus appeared, the company was struggling with growth. Don’t get me wrong. The company did grow over the years, but the growth rates were not impressive. The margin has also deteriorated further recently. So this is where the threat facing the entire industry seems to materialize already.

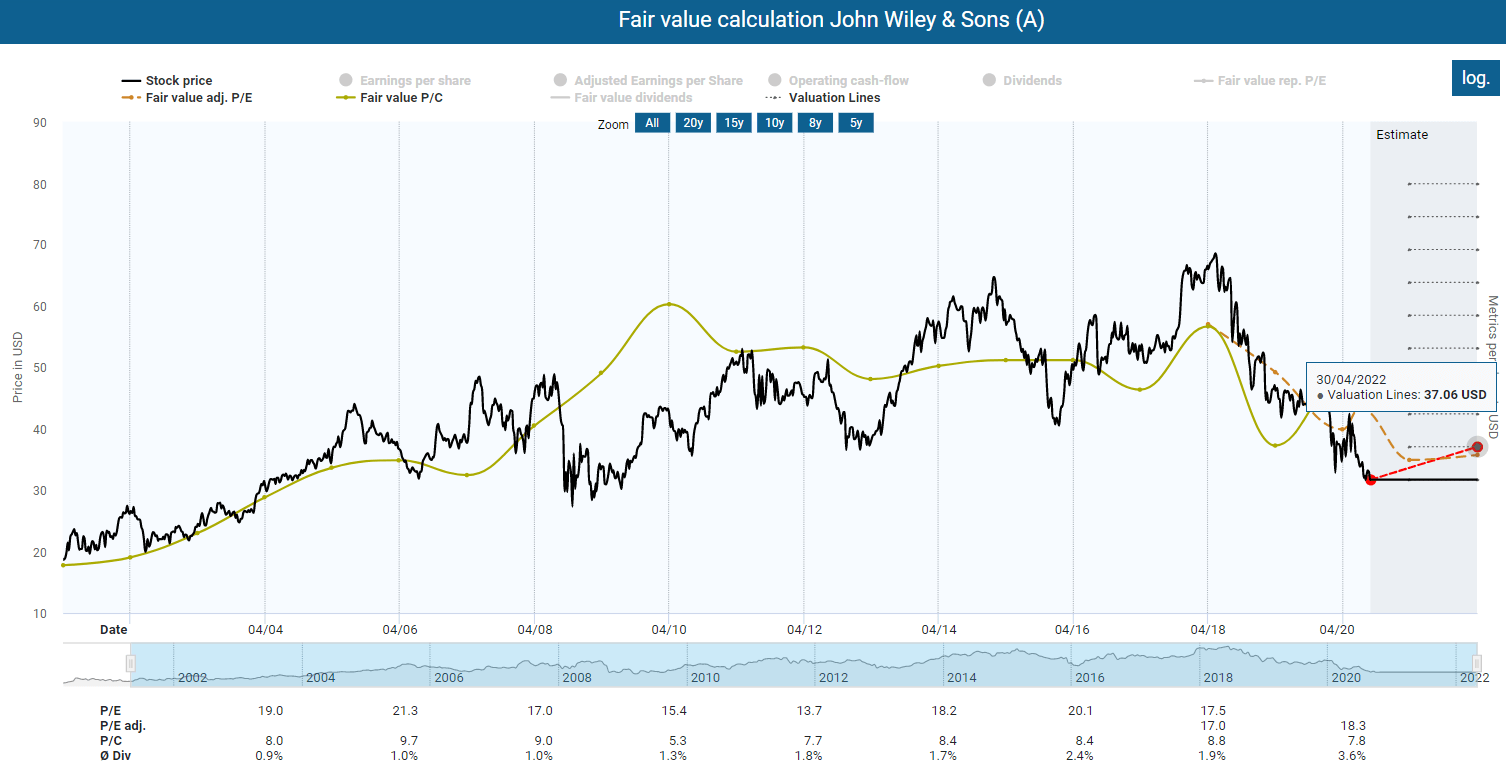

Fair value calculation of John Wiley & Sons

With all these problems, it is not surprising that the share is traded at a discount on the stock market. A fundamental analysis based on historical multiples shows an upside potential of 8 percent. Will this risk premium be sufficient? In my opinion, a still relatively high adj. P/E ratio of 18.3 speaks against an adequate margin of safety.

Nevertheless, it would help if you also consider the relatively high dividend yield. It amounts to over 4% and is also relatively safe, with a payout ratio of 70%. The company was once one of the growth sprinters. The 10 Year Growth rate of almost 10 percent is proof of this. But these times are over. Most recently, the annual increase was only 2 percent. I do not expect John Wiley & Sons to increase dividends in the coming years more than it has done recently.

The publishing house is, therefore, not an essential buy for me. I like companies like John Wiley & Sons, and it is quite possible that the company will be able to adapt to the changing digital world successfully. Investors would, thus, have the opportunity to acquire a company at a fair price, which is not a matter of course, in the current market situation. But I don’t need to have every company that has good prospects for a turnaround. Investing is not a race, and I try not to fall for fear of missing out. Against this background, the publishing house is not an inevitable buy for me. Maybe it will convince me. So far, it has repeatedly exceeded expectations. If it manages to do this several more times, it may even shift the market (and maybe even mine).

General Mills, the bear hunter?

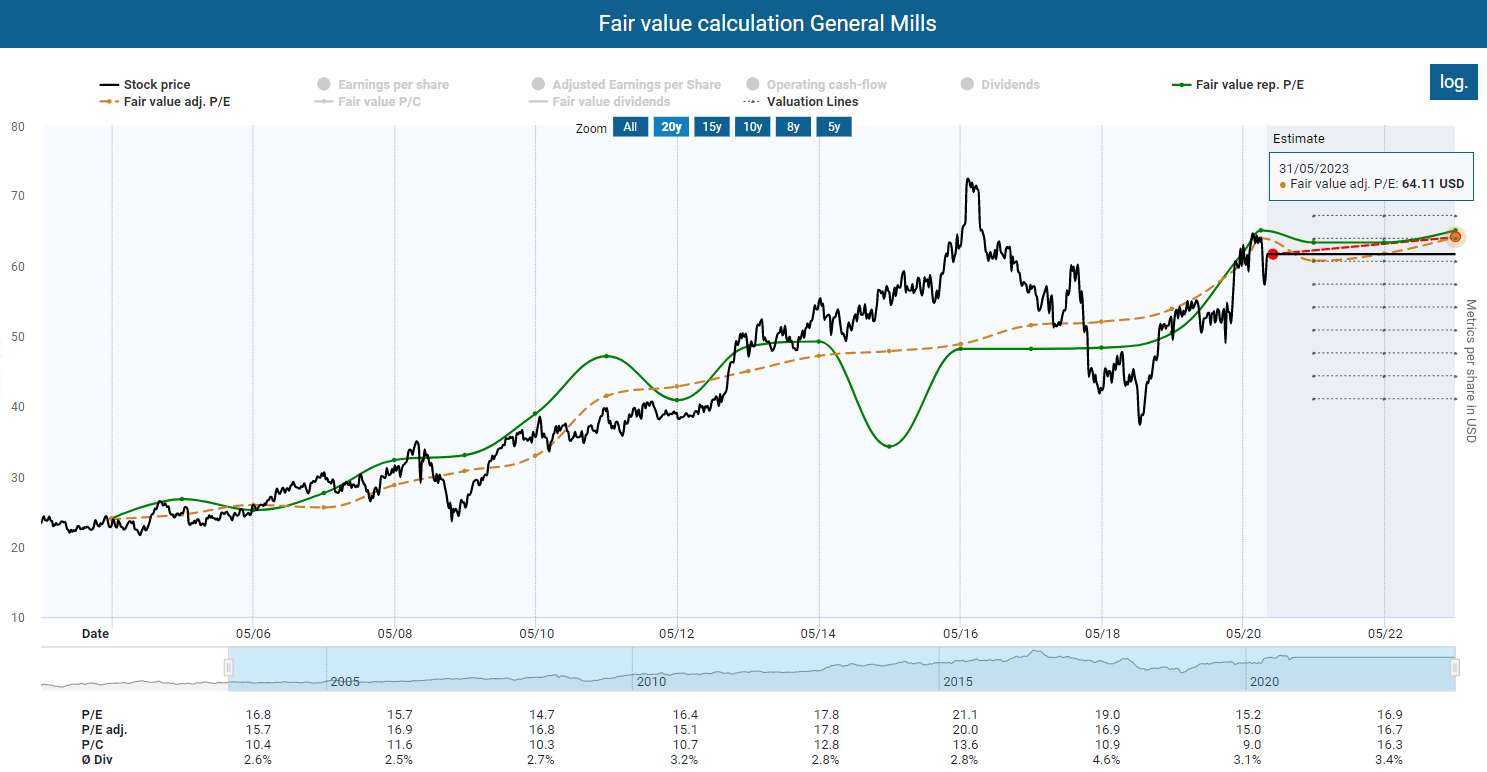

From one traditional company to the next: General Mills was one of the investors’ favorites for a long time until it lost almost half its value from 2016 onwards until the end of 2018. The company missed one or two trends, and especially the yogurt business first stagnated and then shrank. The growth machinery turned into a sluggish ship so that the share price continued to fall with every quarterly report. General Mills also announced the USD 8 billion acquisition of the organic pet food manufacturer Blue Buffalo Pet Products at the beginning of 2018, which was not only a very proud price, it also brought the company a debt ratio of over 60 percent. General Mills has therefore frozen the dividend and focused on debt repayment. With some success, it seems, because two weeks ago the company surprisingly announced that it was increasing its dividend by 4 percent.

The pleasant news was accompanied by a strong quarter. The company recorded organic growth of 10 percent (net sales were up 9 percent)! EPS (non-GAAP of USD 1) also exceeded expectations. Operating profit was up 29 percent and came in with USD 854 million, driven by higher sales and better profitability. So General Mills seems to continue as in the old days. The good thing is that the company is still reasonably valued.

Although I have bought additional shares from time to time in recent years, so that General Mills accounts for almost 2.5 percent of my total portfolio, I will probably increase my holdings again. It is still away from its highs (from before the Blue Buffalo takeover) and seems to be on the right path. Adj. P/E ratio and dividend are also in a historically reasonable range. Especially compared to John Wiley & Sons, the risk/reward ratio at General Mills is, in my opinion, more promising.

Time to do your due diligence

Has a company caught your interest? Attractive dividend yields should not be the only reason to buy shares of a company. Instead, you must carry out careful due diligence before every purchase. The Internet offers you excellent opportunities in this respect.

My analyses here on the TEV Blog are an excellent way to start (click here). You can also contact me here or ask the community in the comments if they can help with your due diligence.

Otherwise, I use tools like those from Dividendstocks.cash and Seeking Alpha to do further research. You can also find me and my analyses on these platforms. We also have a small but lovely group on Facebook that you can join. We share there only fundamental analyses of companies from various sources. So there is no spamming or anything like that.

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

That said, feel free to let us know if I have overlooked an attractive stock or you know of a stock that is particularly attractive and where the ex-dividend date is coming up.

Is a stock here attractive for you? If so, let the community also know and write a comment.

You can also share this post with your favorite network: