Like every week, I want to show you some stocks that will go ex-dividend in the next days. I’ll also review a few companies that are currently in the focus of investors or that have an attractive fundamental valuation. Additionally, I’ll give you some insights into my retirement portfolio and share my thoughts and experiences about individual companies with you. This week, we’ll take a closer look at AbbVie and Zoetis. Both are exciting companies. Zoetis is on my watch list, and as far as AbbVie is concerned, I am considering adding more stocks to my portfolio.

Why yields are a simple way to screen companies

Dividends are a great thing. Even in bad stock market times, they provide a juicy cash flow per month. If you want to benefit from dividend payments as quickly as possible, you must pay attention to the ex-dividend dates. This date is the day on which shares are traded without their subsequent dividend value. Only if you owned the stocks on this day are you entitled to receive the dividend.

Usually, there are always exciting dividend companies that are worth a second look. And the dividend yield is an excellent way to get an initial overview of companies that may be worth further due diligence. To help you get started, at the end of each week, I will publish the ex-dividend dates for the coming week of individual companies here in the TEV blog.

Why I handpick and double-check the ex-dividend dates

I have recently noticed that many databases do not indicate the respective numbers and dates correctly. Spontaneous dividend cuts, in particular, are only partially taken into account, or in some cases, not at all. As a result, the value of such overviews dwindles enormously.

Therefore, I’ve decided to select individual companies by hand and check the dates and dividend yields on the company websites, which means more work for me but increases the value of this section enormously, so it is worth it 🙂

Ex-dividend dates calendar for the third week of July

Well, let’s not waste any time. As always, you’ll find some handpicked interesting ex-dividend dates below.

| Company | Payment Date | Yield | In my retirement portfolio |

|---|---|---|---|

| Monday, July 13, 2020 | |||

| Apogee (APOG) | July 29, 2020 | 3.5% | NO |

| Tuesday, July 14, 2020 | |||

| AbbVie Inc. (ABBV) | August 14, 2020 | 4.8% | YES |

| Abbott Laboratories (ABT) | August 17, 2020 | 1.5% | NO |

| Oracle Group (ORCL) | July 28, 2020 | 1.7% | NO |

| Campbell Soup Co. (CPB) | August 03, 2020 | 2.87% | NO |

| Danone (DANOY) | July 16, 2020 | 3.49% | NO |

| Wednesday, July 15, 2020 | |||

| Watsco Inc. (WSO) | July 31, 2020 | 3.8% | NO |

| Thursday, July 16, 2020 | |||

| Global Water (GWRS) | July 31, 2020 | 2.83% | NO |

| Zoetis (ZTS) | September 01, 2020 | 0.6% | NO |

| Patterson Companies (PDCO) | July 31, 2020 | 4.57% | NO |

| Friday, July 17, 2020 | |||

| Caterpillar Inc.(CAT) | August 20, 2020 | 3.27% | YES |

| Colgate-Palmolive Co. (CL) | August 14, 2020 | 2.41% | NO |

| Main Street Capital (MAIN) | August 14, 2020 | 8.85% | NO |

| ConocoPhilips (COP) | September 01, 2020 | 4.3% | NO |

What’s interesting this week?

We have some great companies going ex-dividend in the third week of July. Caterpillar is one of them. I recently added my first shares of this dividend aristocrat to my diversified retirement portfolio. Colgate Palmolive is also a consumer goods giant and a popular stock among dividend hunters.

I used Colgate toothpaste for years but eventually switched to Sensodyne from GSK (UK based GSK is a good dividend payer as well). Colgate-Palmolive is nevertheless a great company with an experienced management team, and the dividend of 2.4 percent is not outstanding but not to be scoffed at in times of low-interest rates. Nonetheless, I found the company too expensive and too weak in growth, so I don’t have any shares in my portfolio. That being said, today I want to take a look at two other companies, namely AbbVie and Zoetis.

AbbVie

AbbVie is a biopharmaceutical company. The company is still quite young and was only founded in 2013. It was a spin-off from Abbott Laboratories that goes ex-dividend the same day. Abbvie’s top-selling blockbuster-product is the Adalimumab (“Humira”). Humira was one of the top-selling and most successful medical products and was mostly responsible for AbbVie’s success.

The disadvantages of dependence

However, this dependency also has its downsides, in particular, because the patent for the drug is expiring, and there are already biosimilars on the market. To reduce its dependence, AbbVie announced its intention to buy the pharmaceutical company Allergan (the original manufacturer of Botox) for USD 63 billion in June 2019. Competition authorities approved the transaction in 2020. Due to the acquisition, Humira’s share of total turnover and profit decreases from approx. 60% to approx. 40%.

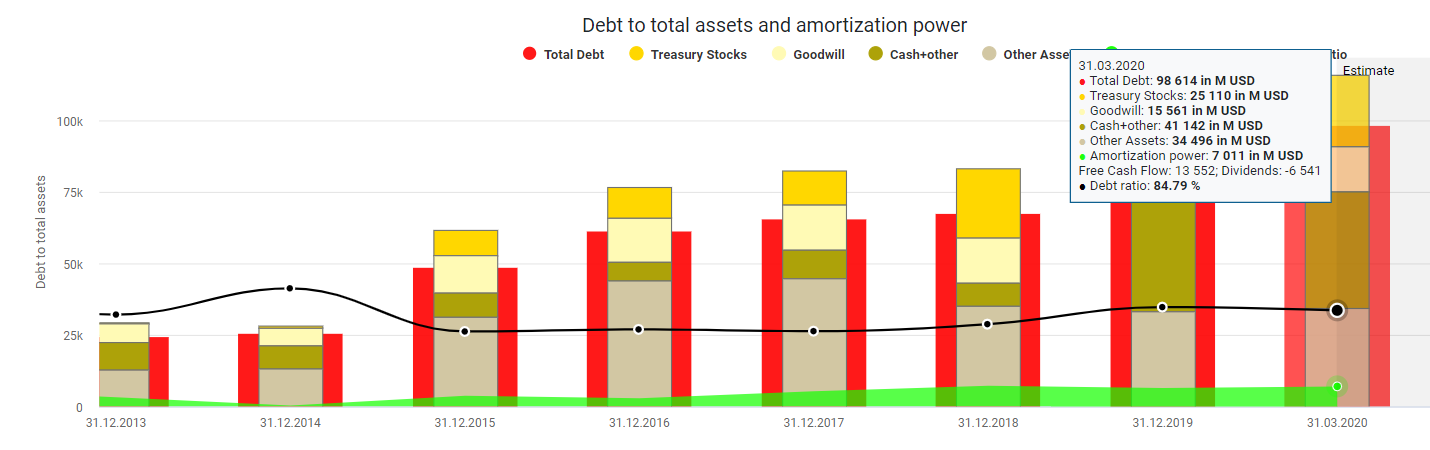

Debt as a solution

The debts have now grown extremely through the takeover. And many investors see a problem here. However, only a few years ago, Pfizer also wanted to buy Allergan, at a price of about USD 160 billion(!). AbbVie now has a debt ratio of just under 85 percent and has total debt (including liabilities) of USD 100 billion. However, this is offset by a current cash flow of USD 7 billion, which could fall in the future as the turnover and cash flow with Humira will decrease. AbbVie has to rely on the pipeline of new drugs here.

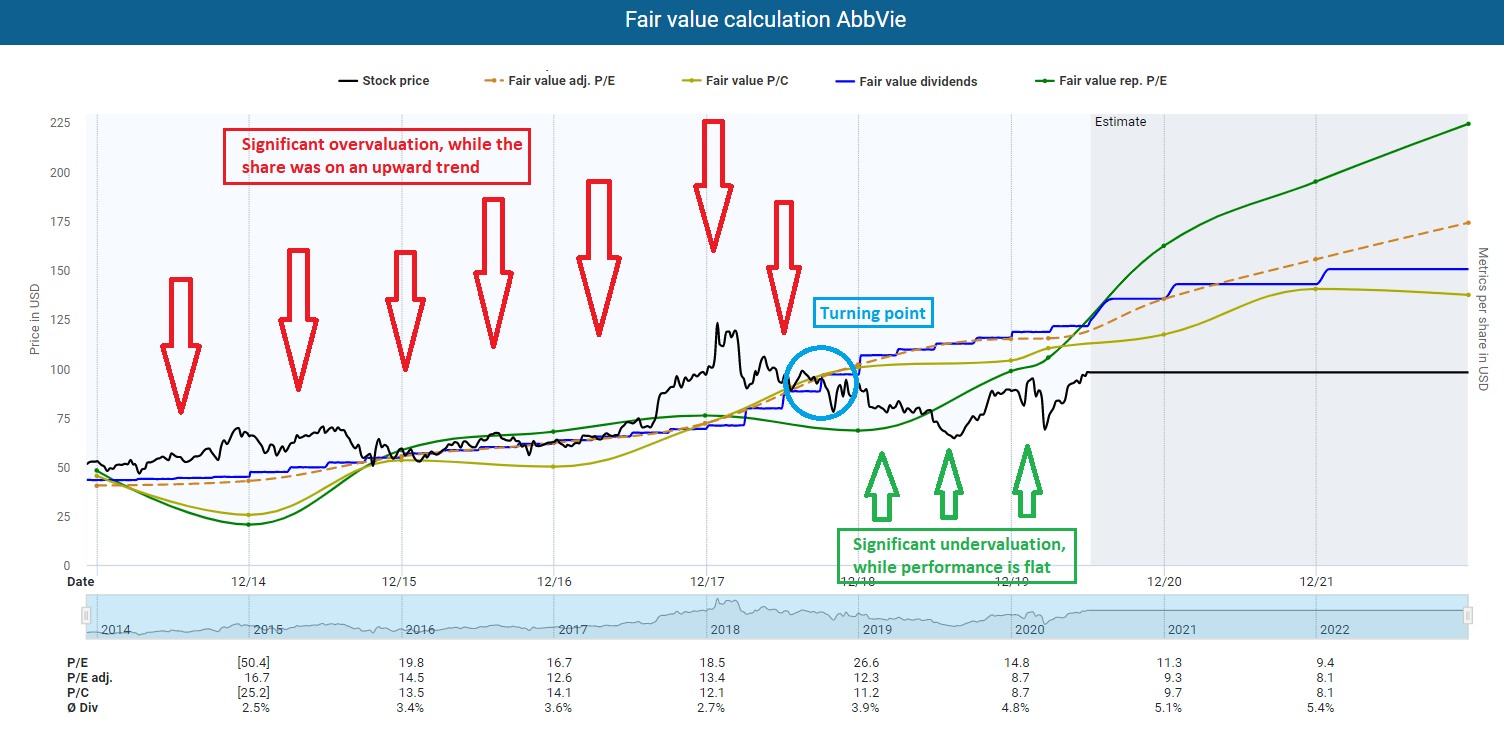

Fair value calculation AbbVie

Currently, AbbVie is hugely undervalued. The market is trading the stock at a massive discount because due to the uncertain Humira-situation and the debt pile. But there is an opportunity in every risk, and the Allergan deal could have created a mega pharmaceutical company in the long term. If the stock returns to fair value based on historical adjusted earnings, there is an upside potential of almost 40 percent. If we look at the historical cash flow, the potential is still 25 percent.

Added to this is the outstanding dividend yield of almost 5 percent. The dividend scorecard also looks good:

- Payout ratio: 45.1 percent

- Cash payout ratio: 81 percent (which is slightly too high in my eyes)

- 5 Year Growth rate: 20.86 percent (do not expect future increases of this magnitude!)

- 5 Year Yield on cost: 6.92 percent.

AbbVie is, therefore, a bet that the management will manage to exploit the bulging pipeline commercially. If the company fails, it will be in serious trouble. If it is successful, and it looks like it will be, then AbbVie could be a real gem at the moment.

Zoetis

Zoetis is a global animal health company and manufacturer of veterinary medicines and vaccines for pets and farm animals. It was initially part of the pharmaceutical company Pfizer but was spun off in 2013. The following fact sheet gives you a good overview of the companies:

The company is a profitable growth machine

The company has increased its sales from USD 4.5 billion in 2013 to over USD 6.2 billion. Over the same period, the operating margin has increased by almost 50 percent (from 18 percent to 33 percent) and the net margin by more than 100 percent (from 11 percent to 25 percent). The gross margin has also grown by almost 10 percent (from 62 percent to 67 percent). To further accelerate growth, CEO Alaix last year acquired the animal diagnostics company Abaxis for USD 2 billion.

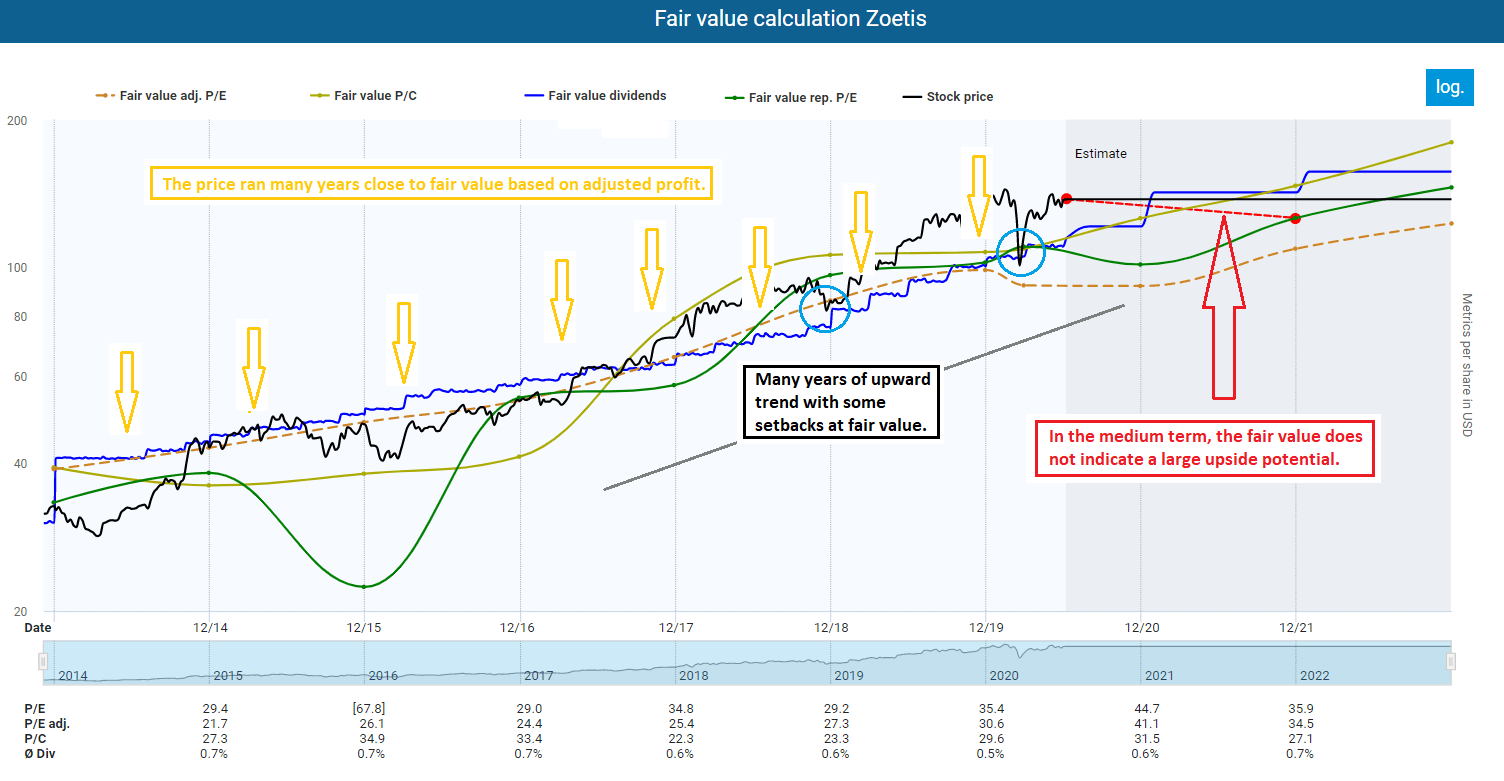

Fair value calculation Zoetis

In recent years, the market has always traded Zoetis relatively close to fair value based on historically adjusted results. From 2018 onwards, however, the share price has moved increasingly away from this and has slipped into the area of overvaluation. If you buy now, you would have to wait about a year for the company to reach its fair value.

If the stock drops 20 to 30 percent, I’d buy it immediately because dividend scorecard looks very promising:

- Payout ratio: 24 percent

- Cash payout ratio: 22 percent

- 5 Year Growth rate: 18 percent

- 5 Year Yield on cost: 1.65 percent.

Five years ago, the company had an average yield between 0.5 and 0.7 percent. The company should reach this range again to be attractive to long-term investors. At the moment, however, the company is too expensive for me; I would only invest in individual tranches at most and simply use the cost average effect.

Time to do your due diligence

Has a company caught your interest? Attractive dividend yields should not be the only reason to buy shares of a company. Instead, you must carry out careful due diligence before every purchase. The Internet offers you excellent opportunities in this respect.

My analyses here on the TEV Blog are an excellent way to start (click here). You can also contact me here or ask the community in the comments if they can help with your due diligence.

Otherwise, I use tools like those from Dividendstocks.cash and Seeking Alpha to do further research. You can also find me and my analyses on these platforms.

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

That said, feel free to let us know if a stock has been overlooked or you know of a stock that is particularly attractive and where the ex-dividend date is coming up.

Is a stock here attractive for you? If so, let the community also know and write a comment.

You can also share this post with your favorite network:

I love that you now always present a few stocks per week! cool feature

Many thanks Vic. The blog is still at the beginning, so it is very helpful to get feedback!