I welcome you to a new episode of my Dividend Diary on the TEV Blog. Is there anything better in the financial world than a dividend income? Well, I guess not. And so, in February, I was again pleased to see a substantial increase in my dividends. I also used this month to add more shares and stocks to my portfolio. As always, in my monthly reports, I will give an update on my purchases. I document my monthly dividend income and the changes in my broadly diversified retirement portfolio. Here, I show you which companies have generated juicy cash flow for me each month and which stocks went into my basket. Besides, I analyze how the month has performed compared to the previous year. In the best case, my dividend income has increased.

As you know, I take care of my wealth management. To keep things simple, I have built three pillars:

- Active income.

- Passive income.

- Conversion.

Dividends fall into the last two categories. They are passive because I no longer have to work to receive the payments. Furthermore, they also contribute to the conversion because I reinvest the dividends and thus increase my passive income through dividends for the future.

My monthly dividend income in February:

This month I have received payments from the following companies:

- AT&T (20.75 EUR)

- CVS Health (6.31 EUR)

- General Mills (12.15 EUR)

- General Dynamics (6.19 EUR)

- Siemens (28.00 EUR)

- Apple (8.04 EUR)

- Tanger Factory Outlets (5.08 EUR)

- Realty Income (3.43 EUR)

- AbbVie (23.60 EUR)

- Kinder Morgan (12.28 EUR)

- Omega Healthcare (10.29 EUR)

- Procter & Gamble (12.15 EUR)

- Caterpillar (5.95 EUR).

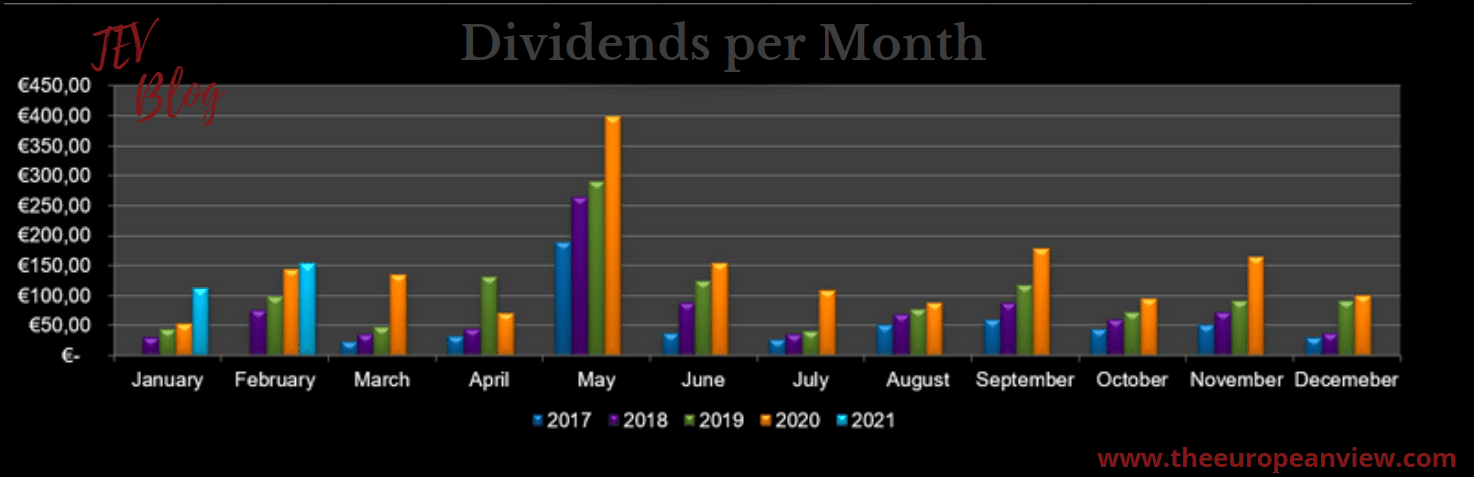

The total dividend income in February (after taxes) was: EUR 154.22/appr. 186 USD

Dividend income check

Now let’s see how the performance was compared to the previous year. Last year, I received only EUR 143.10 in dividends in February, representing only a slight single-digit increase. There are two reasons for this. First, the EUR has gained massively since last year. Secondly, only a few new stock purchases from last year were companies that pay a dividend in February, e.g., Caterpillar, General Dynamics, and CVS Health.

Now two months have already passed in 2021. I am pleased to have seen a slight increase in cash flow despite those unfavorable currency effects.

That is the reason why we follow this approach: We invest to generate cash flow streams and to build a long-term and stable cash flow. So yes, it was a good start, and I look forward to the upcoming months. Will I set a new record with my “keep it slow and steady” investment approach? Well, probably. The development of my dividend income throughout the years is as follows:

Stock purchases for more dividend income

So back to business as usual. Last month, I bought shares in four companies and additional shares of one of my existing EFT holdings:

- Teamviewer (24 shares)

- Danone (23 shares)

- Unilever (16 shares)

- Fresenius Medical Care (20 shares)

- Xtrackers MSCI USA Financials UE 1D (30 shares).

In the following, I will briefly explain why I bought these companies/ETFs. Please do not expect a fundamental analysis. I will only mention some aspects per company that might be of interest to the readers. Maybe you will find inspiration for your investment. In case you disagree, feel free to write your opinion about my purchases in the comments.

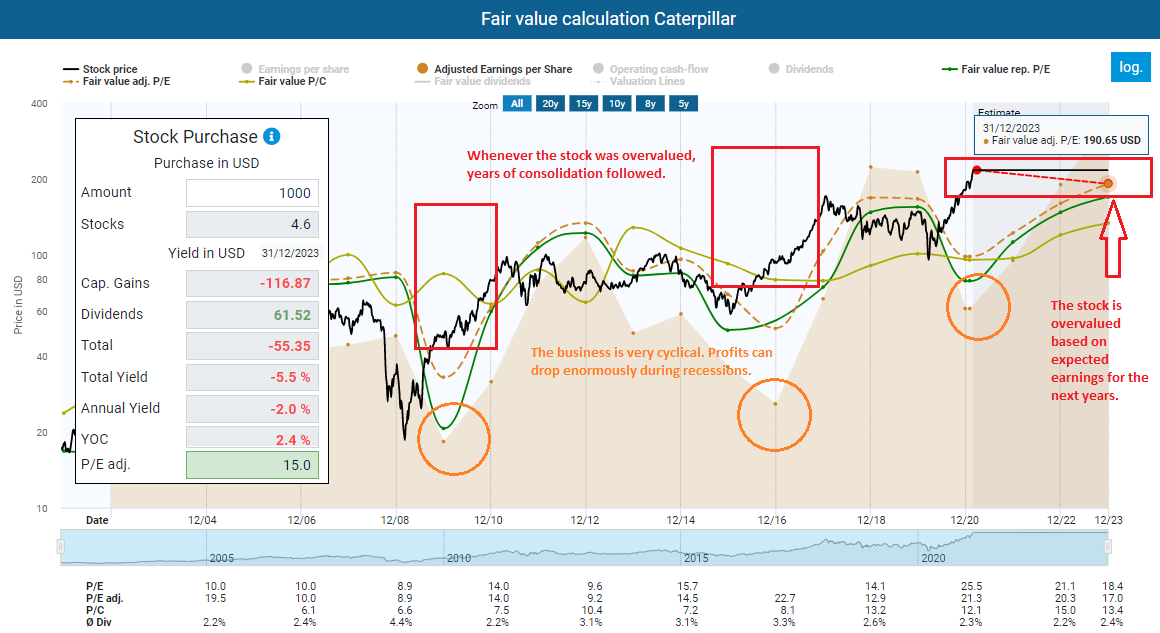

Probably the most notable thing last month was my sale of all my Caterpillar shares, which means that I have not even held the shares for a year. I only added Caterpillar to my portfolio back in June 2020. My purchase of Caterpillar shares represented only a small part of my portfolio (below 1 percent). It was, therefore, not a core investment but a kind of satellite investment. With such investments, I take shares that offer a favorable opportunity. My investment in China Mobile, for example, was also led by such an approach.

Did I try to time the market?

By selling the shares, I was not in line with my long-term investment approach, which is to hold companies for the long term to benefit from rising shares and dividends. What happened? Well, I guess you can say I timed the market, even if that’s not the whole truth. I did not sell Caterpillar because I expect the share price to fall. That would be nonsense because no one can predict such developments.

Caterpillar is an excellent company

Caterpillar is and will continue to be a great company. Thus, I have not sold my shares because I believe that the company is facing challenging times, which is also a point that I cannot predict.

Many investors even assume that commodities are about to enter a bull market, which could ensure that many companies invest in their machinery and equipment, from which Caterpillar will naturally benefit.

Other considerations led to my decision to sell.

Caterpillar is heavily overvalued and a cyclical company

Caterpillar’s share price has grown significantly in recent months and brought me juicy book profits. Within only eight months, my capital, including dividends, has grown by almost 50. That is a solid performance, and I would be happy if any of my investments had resulted in such performance.

I usually just let profits run their course because I don’t want to end up making the mistake of many investors who sell their best-running stocks and hold on to the losers. However, Caterpillar is a classically cyclical company whose profits can fall sharply during recessions. The share price also generally reacts to such phases and then performs less well. Besides, at Caterpillar, the share price always consolidated strongly after phases of overvaluation.

What we are seeing now is that Caterpillar has never been so overvalued. Even based on expected earnings for 2023, the stock is overvalued on the current level.

We want to achieve a good return on investment and to build up cash flow streams

There I was. I had book profits of almost 50 percent. The capital tied up in the overvalued Caterpillar stock generated a historically low dividend yield of just 2 percent. My yield on cost was higher, of course, but this refers only to the initial capital and not to the total capital, including book profits.

But the approach of my readers and me is to generate cash flow. We are not betting that the stock price will go up. Accordingly, I have decided to sell the shares and reallocate the freed-up capital to other companies with better valuations and higher dividends. Well, my choice fell on Danone and you can find the reasons below 🙂

So I may repurchase Caterpillar when the valuation is a little more reasonable. If the price keeps going up, so be it. There are so many good companies and my future cash flow will not depend on whether I sold Caterpillar too early. It might not be the best decision then, but not a wrong one either, to redeploy tied-up capital into an investment with better return potential.

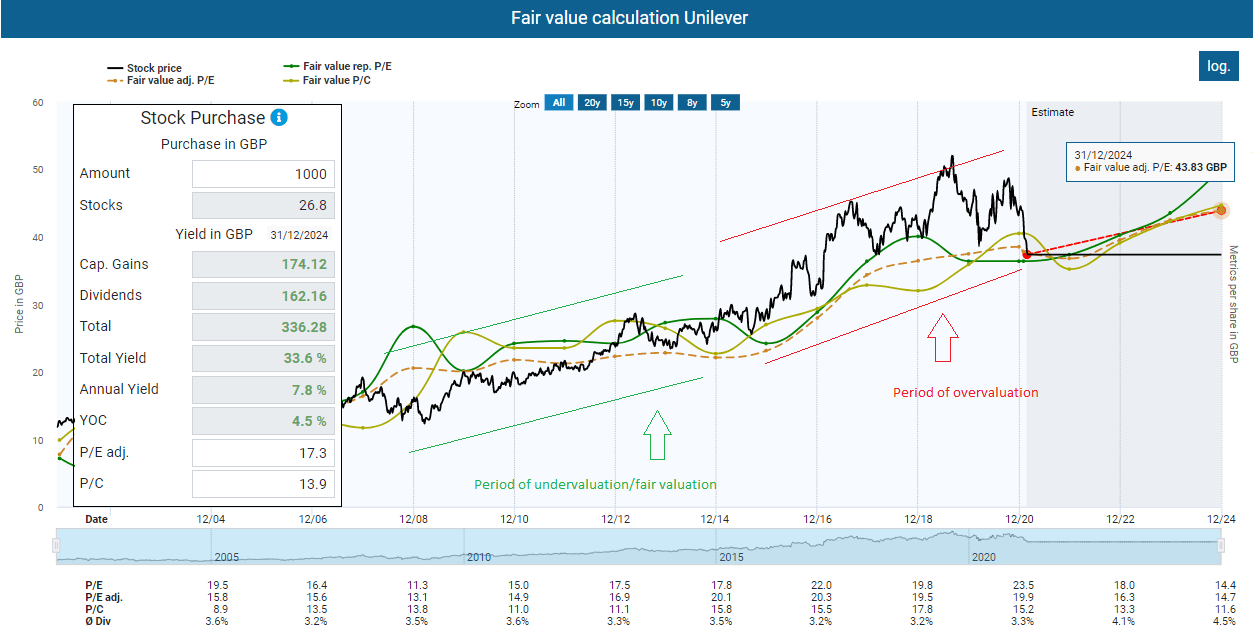

Unilever is also a company that I added to my portfolio last year. Unlike Caterpillar, I want to establish Unilever as a core investment in my portfolio. The share price recently fell by 10 percent. The reason was somewhat weaker growth in COVID-19 year (wow!). I don’t want to beat around the bush here. Unilever has strong brands, a suitable footprint in the emerging markets is restructuring (one headquarters and legal structure instead of two as before). It has increased its dividend by 4 percent (yielding almost 4 percent right now). Also, based on historical multiples, it is finally fairly valued once again.

Essentially, I shifted all of the capital from Caterpillar into Danone. Danone has been on my extended watch list for a long time. However, a real opportunity has not arisen for me. In January 2020, I wrote the following about Danone in a stock analysis:

Overall, Danone is a great company that offers products for nutrition and health-conscious people and has a strong position in the market. It also invests heavily in the Asian market. It is in principle suitable for a broadly diversified retirement portfolio. However, Danone is not a must-buy, and certainly not a jewel that you absolutely have to buy now. There are the reasons for my grading:

- There is a lot of light and shadow.

- High debt / free cash flow ratio.

- Dividend not increased several times in the last decade, thus low dividend growth during this long bull market.

- Low margins

Since then, the share has fallen by a further 15 percent (in USD) (in EUR even more than 20 percent). With this performance, the share price has now reached an area where I consider the medium- to long-term risk/reward ratio reasonable. In the short term, however, it may remain volatile.

Danone’s business model

Danone SA is a global manufacturer of food products. The company was founded in 1899 and is headquartered in Paris, France. The business units are “Fresh Dairy Products”, “Waters”, “Early Life Nutrition”, and “Medical Nutrition”. The “Fresh Dairy Products” segment includes yogurts, fresh dairy products, and other fresh dairy products. The segment “Waters” comprises the natural waters and aqua drinks business. The “Early Life Nutrition” segment includes specialty foods for infants and young children. In “Medical Nutrition”, Danone’s main focus is on people undergoing medical treatment, babies with certain illnesses, and frail elderly people.

My expectations: A company for the long-term prospects

Danone is the same company as in my analysis last year. Nothing has changed since then, except that I can get them for 20 percent cheaper once again. What I like about Danone is the product portfolio and the focus on sustainable and healthy products. I see enormous potential here in the long term, as consumer needs move in precisely this direction.

Currently, however, Danone’s water business suffered due to the closed restaurants. Furthermore, the company had problems with its “Early Life Nutrition”, which is the most profitable business. These development have put pressure on the company, forcing the management to cut the dividend by 8 percent.

Right now, Danone is in the process of focusing on the most profitable brands and regions, which reminds me of Procter & Gamble or Nestlé. Both companies underwent a comparable development. Currently, Danone is undervalued and still has a dividend yield of over 3 percent. Its total upside potential for the next few years amounts to a straight 8 percent annually. Overall, a good deal in my eyes.

Fresenius Medical Care is a leading global provider of dialysis products and dialysis care/services for chronic kidney failure patients. The company develops and produces various health care products, including dialysis and non-dialysis products. Fresenius Medical Care was founded on August 5, 1996, and is headquartered in Bad Homburg, Germany. The biggest shareholder is its former mother company Fresenius SE, which I bought in November 2020.

Like Fresenius SE, Fresenius Medical Care is currently struggling with COVID-19. In the fourth quarter of 2020, FMC generated revenue of EUR 4.40 billion, slightly below the estimate of EUR 4.49 billion and down 4 percent compared to last year. EPS of EUR 0.61 were also significantly below the forecast of EUR 1.23. Despite the challenging previous quarter and the expected negative impact of the Corona pandemic in 2021, Fresenius Medical Care intends to increase the dividend from EUR 1.20 to EUR 1.34. The yield is thus slightly below 2 percent.

With a payout ratio of 30 percent, the dividend is also sufficiently covered. One big reason for my purchase was also the poor share price performance after the last quarterly figures’ announcement. The share has thus slipped back into undervaluation.

Fresenius Medical Care will not become a core investment of my portfolio. I am already indirectly invested in the company via Fresenius SE. I simply see upside potential in the medium term and want to take advantage of it. The disappointing results of the last quarter were mainly due to the pandemic. I expect the operating performance to improve again once the vaccinations in the USA (the most important market for Fresenius Medical Care) start to show results. Furthermore, the demand for dialysis services will increase in the long term. As one of the largest providers, Fresenius Medical Care can use economies of scale and thus has an advantage over its competitors. So yes, I am very optimistic that the company will grow successfully in the long term.

I have already said everything about TeamViewer. For me, the company is one of the great opportunities in the field of Industry 4.0. It is still perceived as a simple remote and conference system company, which is misleading. The areas of application are much broader and pretty promising. With TeamViewer’s solutions, companies can access and control devices from virtually anywhere in the world or instruct other people to operate them. But I repeat myself 🙂 My last purchases of the stock were in November and August. Currently, I have 3 percent of my capital invested in TeamViewer, and I am willing to go up to 5 percent.

The last thing I did was to increase my investments in the finance sector. My problem is simply that I have never dealt with the industry with detailed due diligence and have no real knowledge of it. In such cases, stock-picking is similar to a lottery. To solve this problem, I invest in an ETF to cover the sector. For this purpose, I have chosen an ETF whose benchmark is the MSCI USA Financials Index. The current dividend yield is roughly 3 percent. All securities in the index are classified in the Financials sector as per the Global Industry Classification Standard, which enables me to cover several complex industries with little knowledge.

Watchlist for March

Next month, there will be some additional purchases of shares. I am relatively flexible here. Either I buy new positions, or I increase my shares in existing investments.

The following companies are on my watchlist in particular:

- Microsoft (MSFT)

- Digital Turbine (APPS)

- Intel (INTC)

- Salesforce (CRM)

- Mayr-Melnhof Karton AG

- SAP (SAP)

- Bayer

- Hugo Boss

- Sysco (SYY)

- AT&T (T)

If you look at my report from last month, you will see that none of the companies I bought were on my watchlist. Why is that? Is the watchlist nonsense, and in the end, I only do what I want anyway? Yeah, a little bit. I don’t have a fixed system for my stock purchases, and that’s one thing I have to consider changing.

However, I have an extensive overview of many companies that I look at from time to time. The watchlist companies are mostly companies that I have currently examined particularly carefully, where substantial changes are imminent or which are in my focus for other reasons.

They are present to me in some form, which is why I put them on the list and perhaps monitor them a little more closely than other companies. But it often happens that I invest in different companies, after all. And so it happens that I buy other companies because it seems convenient at that moment.

Have you received dividends this month? What’s on your watchlist? Let me know and write it in the comments.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

Thanks for the update TEV!

Interesting that you sold your Caterpillar shares. I see the aristocrat as a buy and hold forever.

But I see your point. Unlucky, however, that Danone has cut the dividend. That wouldn’t have happened to you with Caterpillar 😉

Kind regards

Vic

Hi Vic,

happy to see you coming by 🙂

Yep, I missed a few gains on Caterpillar, indeed. However, catching the exact endpoint of the rally was never my intention, not to mention within the realm of the expected.

Nonetheless, the share has thus slipped even further into overvaluation in fundamental terms. I have realized my profits and reinvested them in Danone. Danone’s share has also risen considerably since I bought it. The difference, however, is that Danone currently has far more potential than Caterpillar from a fundamental perspective.

All the best!