With a current dividend yield of over 5 percent, the Allianz stock is one of Germany’s standard stocks for dividend-focused investors. Since the financial crisis, the stock price gained more than 400 percent. Even those who invested a bit later, for example in 2011 have experienced a tripling of their initial investment. In between, profits were even higher. However, with the Corona crisis, the stock lost some of its mojo and is now trading at a discount of 20 percent to the pre-Corona high.

In this fundamental Allianz stock analysis, we will discuss whether or not the Allianz stock is a bargain after the price reset. We also show you which pitfalls you should be aware of with insurance companies. Due to their business and regulatory requirements, there are several peculiarities to be considered in insurance companies’ fundamental analysis.

The business model: How Allianz generates its money

Allianz is one of the world’s biggest insurance and financial companies, with more than 83 million customers and operations in over 70 countries. Allianz structures its business into three segments. For the following explanations, we summarize the two insurance segments.

Property and casualty insurance and life and health insurance

The segment property and casualty insurance include personal property insurance, such as your house – your car – your boat, and the coverage of personal liability. The segment is responsible for 45 percent of total sales and about 25 percent of net profit.

Allianz offers health, life, and disability insurance and a range of health and protection services to individuals, families, organizations, and partners in the life and health insurance segment, which accounts for almost half of net profit and revenue. The Allianz portfolio also includes corporate insurance and risk consulting for companies.

Unlike Munich Re, Allianz is essentially a pure primary insurer that takes premiums from policyholders and covers their risks by committing to pay benefits (usually payment) in the event of a claim. Only within the Group does Allianz, through its subsidiary Allianz RE, act as a reinsurer for other subsidiaries.

Asset Management

In addition to the insurance business, Allianz is one of the world’s largest investors and asset managers, with more than 92 million private and corporate customers. The company manages around EUR 592 billion on behalf of its insurance customers and more than EUR 1.658 trillion in third-party assets via its asset managers PIMCO and Allianz Global Investors.

Here the Allianz invests in bonds, shares, mixed funds, and alternative asset classes. Up-to-date, Allianz has invested 80 percent of its assets in bonds. For a long time, the segment was the company’s problem child and fought with high cash outflows. In the meantime, however, the asset management segment has succeeded in achieving a turnaround. In the first six months, operating income rose by 5.2 percent in nominal terms. Only in the second quarter, i.e., at the height of the corona crisis, did Allianz have to make concessions in the Asset Management segment. Operating profit fell by 7.2 percent. Nevertheless, it still accounts for 25 percent of the net income.

The business model is cyclical

The Allianz business model is cyclical, which was evident during the financial crisis and is also the case in the current corona crisis. For example, revenues in the second quarter of 2020 fell by 6.8 percent. Allianz continues to expect adverse effects on its travel insurance business (Allianz Partners), credit insurance (Euler Hermes), and increased insurance payments in the entertainment sector due to canceled events and business interruption. The company also fears that the situation could worsen if the economic recovery stutters and government support measures expire.

However, insurers have an effective means of countering increased risks. If the likelihood of an insured event occurring, for example, due to a pandemic, Allianz enforces higher premiums, which gives the insurance industry certain stability despite the cyclical nature of the market.

A growth strategy that pays off

The current CEO Oliver Bäte leads the Allianz with a clear growth strategy: “Simplicity wins“. The CEO aims to reduce complexity, streamline its portfolio of complicated products, and place a stronger focus on digitization and customer satisfaction. For a heavyweight like Allianz, this digital transformation focus cannot come soon enough, as small and agile start-ups with lean structures could otherwise become a threat. “Move with the times or move with the times,” is Oliver Bäte’s motto. With this strategy, Allianz was able to continue its past revenue growth seamlessly. Since Oliver Bäte joined the company, it has increased its sales from EUR 125 billion in 2015 to over EUR 140 billion.

In the medium term, the effects of the corona crisis will probably continue to weigh on business. In the long term, however, Allianz should return to its old growth. China could gain in importance in this context. Allianz is the first foreign insurance company ever to be granted a license for the Chinese market, which gives it a competitive advantage over other insurance companies and time to gain a foothold in the Chinese market. Allianz will not only benefit from the growing middle class in China. Compared to other Western countries, China is a growth market with insurance premiums rising sharply every year. So there is still a lot of potential slumbering! However, Allianz will have to face domestic competitors in the Chinese market, who are once again a size bigger than the German insurance giant.

How profitable is Allianz?

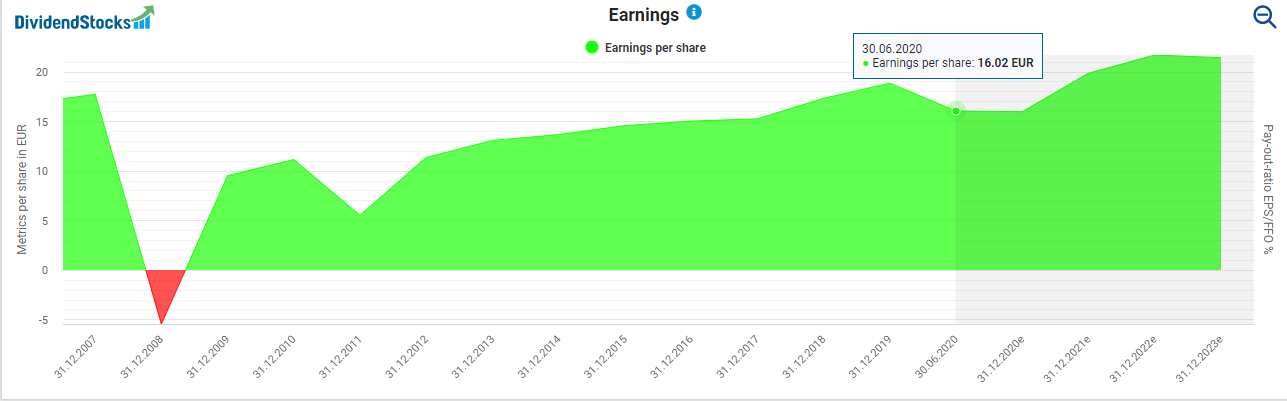

Allianz regularly generates substantial profits. However, the profit analysis confirms that Allianz is susceptible to economic cycles. But the last year of losses was more than ten years ago when Allianz slipped into the red during the financial crisis in fiscal 2008 with EUR 2.44 billion, which was the highest annual loss in the Group’s history. It was caused by the sale of the former subsidiary Dresdner Bank to Commerzbank, which led to write-downs totaling EUR 6.4 billion at Allianz. After that, though, Allianz quickly returned to the profit zone. Currently, the Corona crisis is affecting Allianz. Earnings per share fell by almost 30 percent in the first half of the year. The operating result decreased by 20.5 percent.

How to analyze the profitability of insurance companies

If you analyze insurance companies for their profitability, you should know the following three ratios:

- the loss ratio

- the expense ratio

- the combined ratio.

These ratios reflect the proportion of premiums that remain with the insurer after dedicating all material costs. The loss ratio corresponds to the ratio of an insurance company’s claims expenditure to the insurance premiums paid. In contrast, the expense ratio reflects the ratio of operating acquisition and administrative costs to the premiums earned. Accordingly, the combined ratio should be below 100.

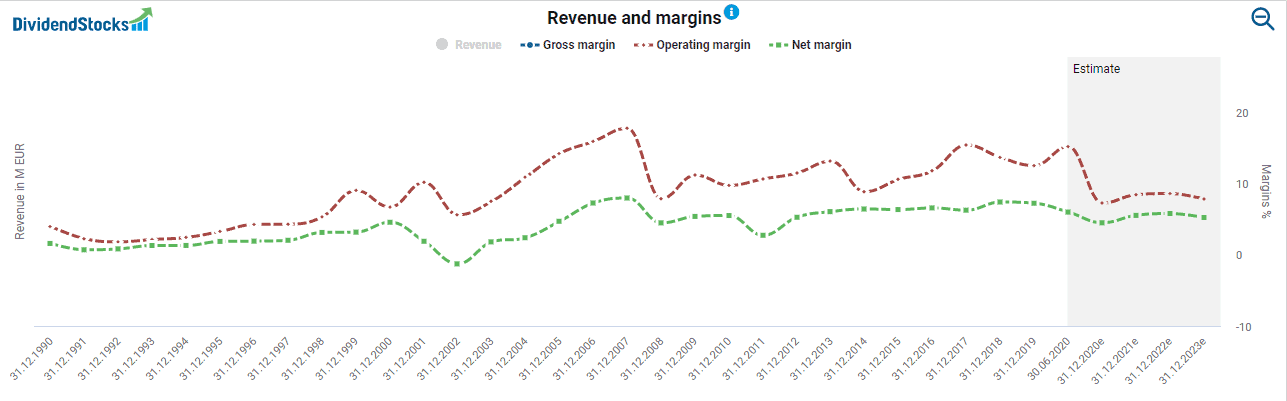

In the first half of the year, the loss ratio rose by 3.7 percentage points from 66.4 percent to 70.1 percent. The expense ratio fell slightly from 27.6 percent to 26.5 percent. Overall, the combined ratio of 96.7 percent was in the positive range but deteriorated by 2.7 percentage points compared to the previous year. This is still better than Munich Re’s ratio, which most recently stood at 97.3 percent.

The overall margin of Allianz

The corona crisis will have an overall negative impact on Allianz’s margins before they should stabilize again next year. The net margin in the share finder comes closest to the development of the combined loss ratio.

Is the Allianz dividend safe?

The Allianz stock is popular with dividend investors thanks to the generous distributions.

Historically high dividend yield

Currently, the dividend yield of just under 5.3 percent, which is historically very high and above the historical. Even higher dividends were only paid during the aftermath of the financial crisis and a short time window in 2016.

However, the Allianz stock is not a dividend aristocrat with 25 years of dividend increases in a row. Unlike Munich Re, who had no dividend cuts since 1970, Allianz cut its dividend by 36 percent from EUR 5.5 per share to EUR 3.5 during the financial crisis. Here, the fiasco surrounding Dresdner Bank was a decisive factor. Nevertheless, in 2015, Allianz had topped the pre-financial crisis dividend with a distribution of EUR 6.85 per share. Since then, Allianz increased the dividend to EUR 9.6. Even in the corona chaos, Allianz pleased shareholders with an increase of 6.7 percent.

Reasonable dividend policy

Overall, Allianz pursues a conservative dividend policy. Although the management intends to limit the annual payout to 50 percent of the net profit for the year. At the same time, however, dividends should at least correspond to the previous year’s figure. For the sake of sustainability, Allianz is willing to accept years with a higher payout ratio than 50 percent. Currently, the payout ratio is just under 60 percent, which is good news for shareholders who value reliability. Incidentally, when analyzing the dividend security of insurance stocks, you should exceptionally not use cash flow as a basis, since cash flow is made up of the contributions of policyholders and is reserved as debt capital for the settlement of insurance claims.

Is the Allianz stock fairly valued?

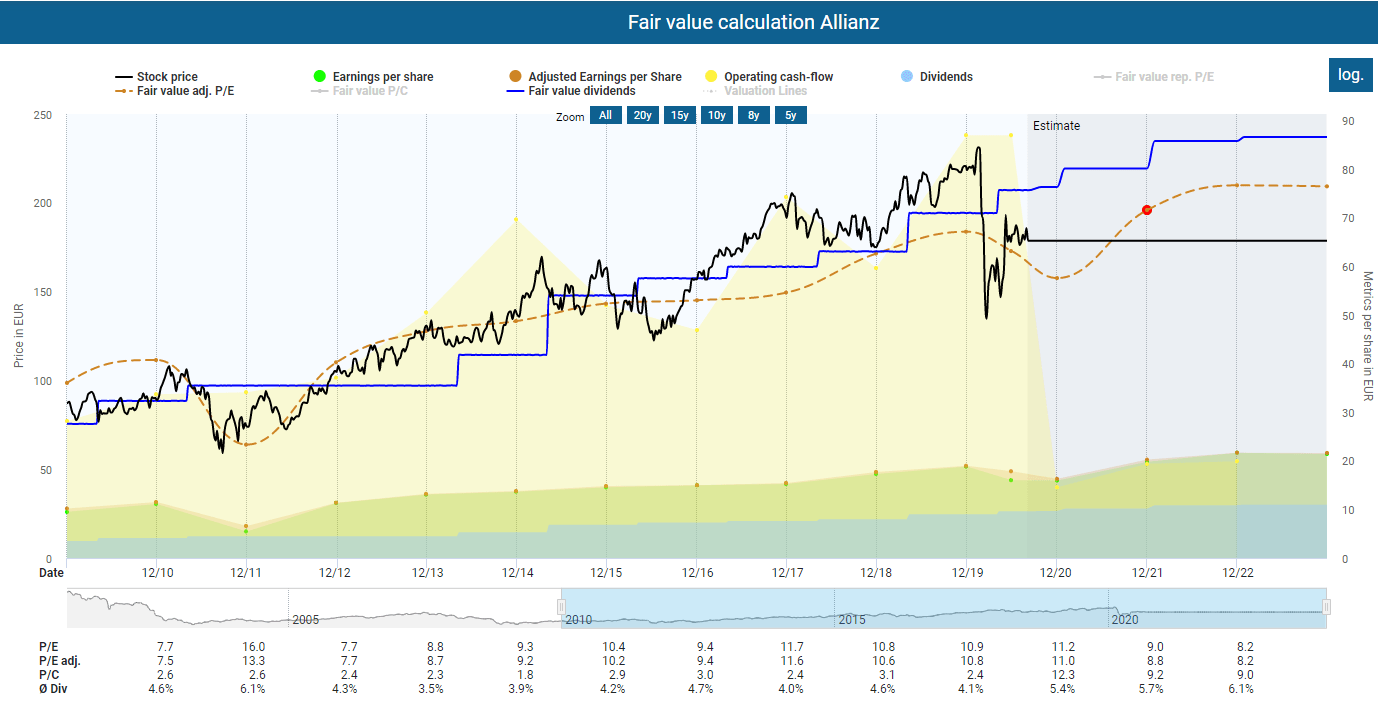

The graph below shows that the Allianz stock is undervalued on the basis of the last 20 years and has a short-term upside potential of 13 percent to its fair value due to the share price losses during the Corona period.

The single-digit P/E ratio of 9 for the forecast fiscal year 2021 (based on the current share price) is not untypical for an insurance company but compared to the previous year’s figures. It also signals that Allianz is currently not overpriced.

Stable balance sheet

When analyzing Allianz, do not be irritated by the high debt ratio. Although DividendStocks.Cash shows that the debts are almost as high as the total assets on the balance sheet, the company does not have a debt problem. The high ratio is explained by the fact that the policyholders’ contributions are considered liabilities.

Solvency II capital ratio

Allianz easily meets the 100 percent capital ratio required by law (the so-called Solvency II capital ratio). The Solvency II capital ratio requires a level of equity capital at which, in the next twelve months, non-compliance with the solvency requirements can occur at most as a result of a shock event that occurs statistically every 200 years. In the second quarter of 2020, the Solvency II capital ratio was a stable 187 percent, and within Allianz’s target corridor. Previously, Allianz regularly had ratios above 200 percent. Adverse market developments due to the COVID 19 pandemic mainly drove the decline.

Do changes in interest rates affect the profitability of insurance companies?

A decisive factor for future profit development is the interest rate level. Low-interest rates and strict legal requirements make it challenging to invest the capital managed by Allianz in a profitable way. Unfortunately, the tectonics of the international interest rate world seem to continue to change to investors’ disadvantage. The US Federal Reserve Bank, for example, has indicated that it will accept years of high inflation without raising interest rates. Higher inflation could mean that the premium payments from old contracts could no longer cover inflation-induced higher loss amounts. Admittedly, we are still a long way from such a scenario affecting the entire industry. However, shareholders should keep an eye on this scenario.

Conclusion fundamental Allianz stock analysis: Attractive dividend with risks

Allianz brings a high and relatively safe dividend, which it has increased every year since the financial crisis. Besides, the company scores with its size, the growth strategy of CEO Oliver Bäte, and promising prospects in the Chinese market. However, the Allianz stock is not immune to risks typical for the industry, such as an accumulation of extreme events or the unforeseeable consequences of global financial policy. Those who want to invest in the sector find an opportunity to buy an industry leader at a fair price.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

Hi, I am a long time reader, but this is my first comment. I really like your analyses, they are really detailed and on point! One question, what do you think about the European Real Estate stocks at the moment?

Hi Marco,

many thanks for coming by and commenting with such nice words.

Concerning your question: Well, I am not the real estate/REIT guy. I am holding two European companies operating within that sector. One company performs excellently (German Vonovia), the other one performs due to the Corona virus poorly (French Unibail Rodamco). I will keep both and may add a little bit in the future. Unibail looks indeed very cheap. But I’ll wait a bit longer and see how the situation develops (the same goes for my US based Simon Property and Tanger holdings). I would rather miss some profits than throw my money into a black hole.

However, from my perspective, there are other good real estate companies in Europe (Deutsche Wohnen for example). Overall, it is how you would expect it: Real estate companies in the retail sector suffer and might offer a good value opportunity, while housing companies perform very well but are somewhat overvalued.

All the best,

TEV

Another good article, thanks.

Excellent company especially for the great dividend but I think it should not grow much in the coming years and the debt may increase, in addition to the huge costs of digitization. But yes China and Brazil can make a difference.

It has been sidelining practically since June but I hope that there will be a good opportunity to enter one of these days. I also like Talanx at 26-28 €.

Could the Marco’s question be related to the fact that ALV has great exposure to the real estate sector? (https://www.allianz-realestate.com/)

I recently bought URW (ams) at 41.25 because I thought it was too cheap and after all it still dropped another 6%, but I think they can handle the impact without issuing new shares.

It’s like you say, wait a bit longer and see how the situation develops.

Thanks João Luz!

Totally – and good point! However, it is not a pure real estate company. Allianz could change its focus at any time without changing the character of the company. In other words: I wouldn’t buy Allianz solely because I want to profit from the development in the real estate sector. There are other companies (e.g. Vonovia).

Best

TEV