New week, new fundamental stock analysis in which I will look at the Amazon stock and check whether it is a buy or a sell based on a fundamental valuation model.

The Amazon stock was a hell of an investment

Looking back, Amazon stock was one of the best investment opportunities in the last decades. And even against the coronavirus, the stock seems to be immune. While the broad market is still recovering from the corona crash, the share price is 25 percent above the pre-crisis level. Those who put the share into their portfolio in 2000 are now delighted with incredible price gains of 2600 percent. Those who entered the market 5 years later have even achieved price gains of 8000 percent thanks to the bursting of the DotCom bubble.

So the happy shareholders will hardly be bothered by the fact that Amazon is not paying a dividend. The fascinating thing about the Amazon stock is that it has never been worth buying if you take the standards of value investing as a benchmark because the share has always had a three-digit P/E ratio (price/earnings ratio). The current P/E ratio of just under 144 also literally screams for a massive overvaluation. With consistent profits, you would have to wait 144 years before Amazon’s earnings repaid the amount you invested with your initial purchase.

So has the market gone completely crazy again, or is there more behind the exorbitant price gains? And what about the constant calls for an Amazon break-up? In this analysis, we will thoroughly examine the company and show you whether Amazon stock is a promising buy or whether you should better keep your hands off the stock.

Business model

Amazon’s business model is impressive, as founder and current CEO Jeff Bezos has built a global empire from a former book distribution business. The company’s guiding principle is to be the most customer-centric company in the world (“We seek to be Earth’s most customer-centric company.”). Amazon only has three segments for its activities: “North America”, “International,” and “AWS.

The “North America” and “International” segments as the foundation for Amazon’s success

The “North America” and “International” segments include all revenues generated by Amazon as a sales platform, which includes revenues from retail sales on the Amazon Internet site’s online sales platform. Amazon either acts directly as a seller or earns commissions from other merchants who sell their products via the “Amazon Marketplace”.

Outside the Internet, Amazon also operates physical shops. To get a first foot in the market here, Amazon has acquired Whole Foods Market for $ 13.4 billion in 2017, a provider of mainly organic or sustainably grown food. Amazon also operates its physical stores under the labels “Amazon go” and “Amazon go grocery“. The unique feature of these stores is that there are no cash register payment systems. Sensors and cameras register which products customers buy and automatically charge them when customers leave the shops, which means that only consumers who have an Amazon account and activate the Amazon Go app when they enter the stores can shop in the stores.

The AWS segment (Amazon’s Cloud business)

Amazon bundles its cloud business in its AWS segment (AWS=Amazon Web Services). If you want to invest from the fast-growing market for cloud computing, Amazon definitely belongs to the best Cloud-Computing stocks.

You can think of the Cloud Computing market as a multi-layered market. On different levels, service providers like Amazon offer a diverse range of hardware and software products. Amazon is particularly active on the two levels IaaS and PaaS. In the area of IaaS (=”Infrastructure as a Service“), the company provides customers with the physical infrastructure, i.e. the hardware (especially network capacities, storage space, etc.) on which customers run their own software applications. In the PaaS (=”Platform as a Service“) area, Amazon also offers a complete platform for developers or programmers. They can access both the hardware and a software and programming environment provided by Amazon to develop their own cloud products for the end market.

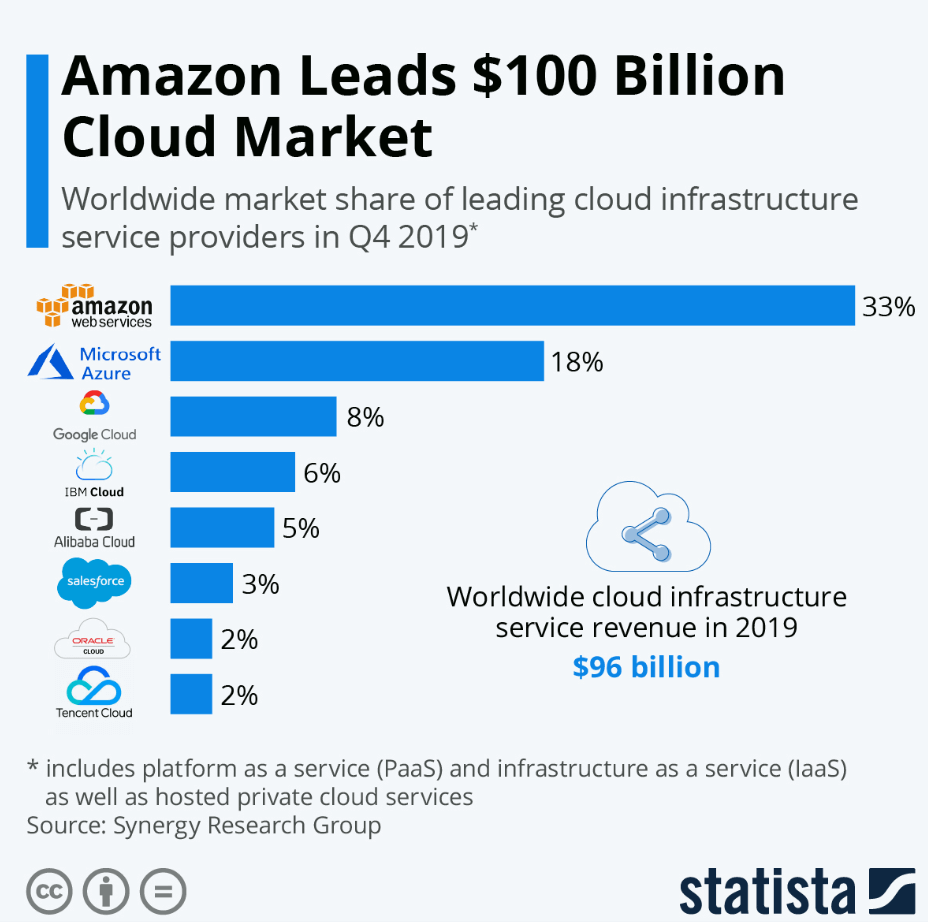

In the fourth quarter of 2019, Amazon’s market share in the IaaS and PaaS services was a strong 33 percent, which makes the company the clear market leader with a comfortable lead over the second-placed Microsoft with a market share of 18 percent.

The market value of IaaS and PaaS is expected to double within four years until 2022. And Amazon holds the pole position to benefit from future growth.

Why is Amazon so successful?

Amazon owes its success mainly to the two segments, “North America” and “International”. With these two segments and due to its customer focus, the company quickly build up a strong market position and gained high popularity among its customers.

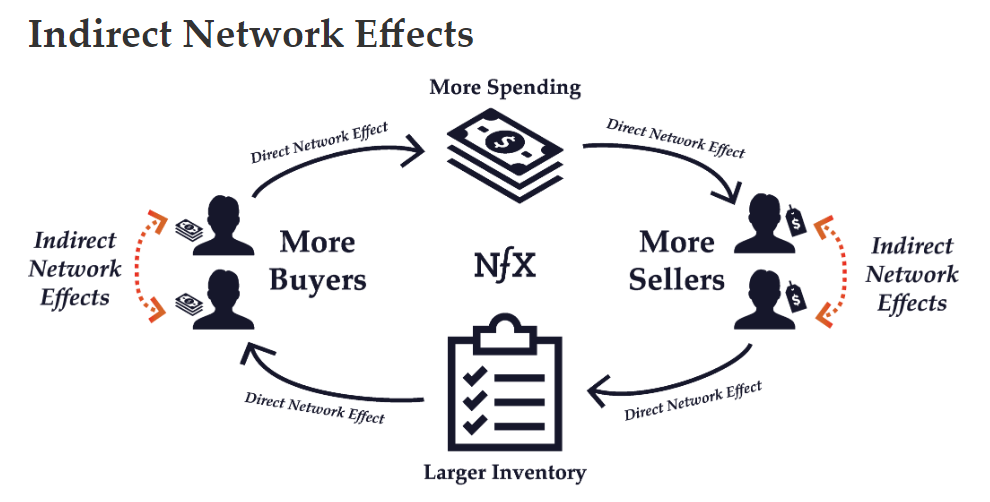

This market position was built up primarily thanks to so-called “indirect positive network effects”. Such effects are often found at platforms. They can lead to substantial increases in market share or even complete monopolies. For shareholders, such monopolies are a blessing. Firstly, they build a moat around the company. Secondly, they make it difficult for competitors to penetrate the market. At Amazon, these effects can be explained very clearly: the greater the success of the sales platform operated by Amazon, the more frequently it is used by third-party merchants, which increases the variety of products on the platform and attracts even more customers. This, in turn, increases the value of the platform for other merchants, etc.

Unlike many other companies, Jeff Bezos has never rested on this success. Instead, he used this comfortable position to facilitate new growth. To this end, Amazon has penetrated market after market through so-called vertical growth. The business now comprises several levels, on which Amazon offers various services and products.

These levels are connected so that Amazon can also benefit from synergy effects. The prime subscription, for example, not only allows free deliveries for purchases on the Amazon sales platform but also access to the company’s film and music databases, some of which Amazon produces itself. The purchased film rating portal IMDb offers meaningful ratings in addition to Amazon customer reviews. It also attracts new customers by separately advertising the productions included in the Amazon Prime subscription program.

With Alexa and the corresponding smart speaker, Amazon has also made it possible for consumers to link their homes with Amazon’s ecosystem and access Amazon’s products and services even more efficiently.

Amazon is a growth engine

With the help of this business model, Amazon has become a real growth engine. It increased its sales from $147 million in the year of its IPO to nearly $300 billion. And it seems that the end of the flag is far from being reached. Amazon is expected to break the $300 billion barrier as early as next year.

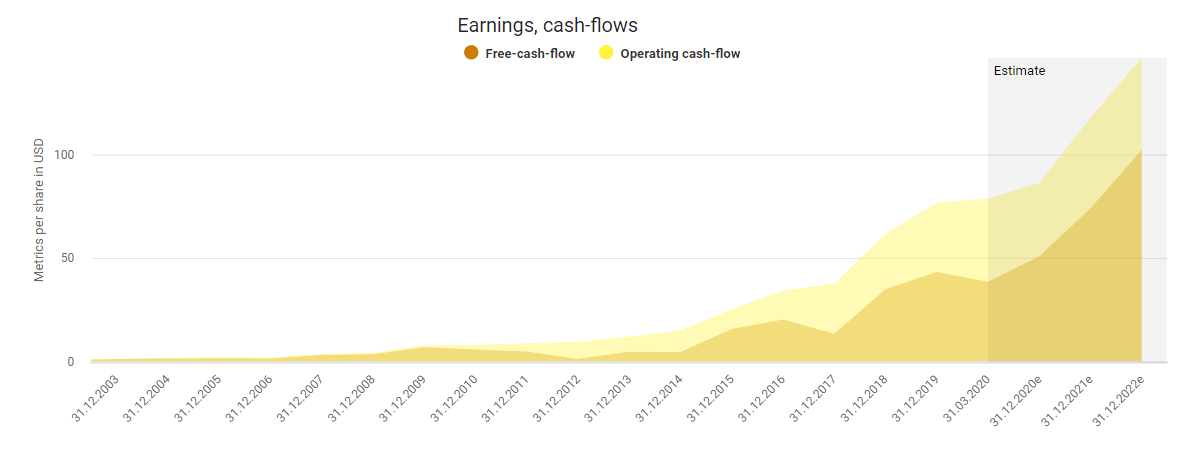

The growth of cash flow also only knows one direction in the long term. The company now generates a free cash flow of just under $40 per share, which is also expected to rise sharply in the future.

Earnings have also developed positively recently, although the coronavirus will temporarily depress earnings. Amazon has had to make massive investments in its storage capacity and its employees’ safety due to the increased demand for online purchases and the coronavirus related health risks. In the long term, however, earnings growth should continue. Next year, the company is expected to generate a profit of $37 per share.

How profitable is Amazon?

Amazon’s margins have also improved with the profit, which means that it is becoming increasingly profitable. Amazon’s extremely high-margin cloud business is responsible for this development. The gross margin has almost doubled to almost 41 percent in the last ten years. The operating margin and net margin are also expected to improve further in the coming years.

The art of calculating the fair value of the Amazon stock

As already mentioned, many investors have problems with the valuation of the Amazon stock. In particular, the high P/E ratio, which is misleading in the case of Amazon, indicates a substantial overvaluation. I will show you here why the P/E ratio is exceptionally not a suitable figure to determine the value of Amazon. Instead, it would be best if you used another metric.

Why the high P/E ratio is misleading

Jeff Bezo’s primary goal is growth by all means. And it is secondary to him if profitability suffers as a result. When Amazon received antitrust clearance to acquire Whole Foods, Jeff Bezos immediately began what he always did: cutting prices. On the very first day, Jeff Bezos arranged for far-reaching price cuts of up to 43 percent in all Whole Foods markets.

This strategy is anchored in the DNA of the company. In his first letter to shareholders in 1997, Jeff Bezos clearly stated that he did not place great value on profits and that he would always opt for cash flow when in doubt:

When forced to choose between optimizing the appearance of our GAAP accounting and maximizing the present value of future cash flows, we’ll take the cash flows.

For this reason, you can more or less forget about all of Amazon’s profit-based valuations models. However, this problem might ease up a bit in the future, as the ever-increasing share of profits from the cloud business gives a slightly better picture of the profitability of the company and thus allows a better valuation of Amazon shares based on profit.

Amazon stock analysis: Is Amazon fairly valued?

To value the Amazon share properly, however, I currently recommend that you primarily look at the cash flow. On the one hand, Jeff Bezos uses cash flow as a measure of his success. On the other hand, cash flow is difficult to manipulate and is therefore very suitable for testing a company for overvaluation. The Amazon stock seems overvalued in terms of cash flow. The difference to the fair value of about $2000 per share is almost 30 percent. As you can see in the dynamic valuation below, the Amazon stock has always corrected after phases of overvaluation to return to its fair value. In this respect, it might be worth waiting for a share price setback.

Conversely, however, it could be that the price will move sideways into the fair valuation without a significant setback. As with Microsoft, you can use the cost-average effect in such constellations. By regularly buying additional shares via a savings plan, you can put overpriced looking stocks into your portfolio at an average price. With such a method, you no longer have to worry about marketing timing but profit from the long-term rising prices of Amazon shares.

The focus is on Amazon right now

One topic that repeatedly comes up in the media is the antitrust law disputes that Amazon is facing. The company is repeatedly accused of abusing its own market position in order to harm competitors or to favor its own position. Amazon’s market power is not only the focus of attention of the US authorities FTC (Federal Trade Commission) and DOJ (Department of Justice) but is also critically examined by the European Commission and national competition authorities such as the German Federal Cartel Office.

You should not ignore such developments when valuing a company, as they can have far-reaching effects on the operating business. For example, authorities can just prohibit companies from certain activities. Besides, fines amounting to 10 percent of worldwide sales per violation are possible. Google’s parent company Alphabet has already had to transfer €10 billion to the European Commission for breaches of competition law. If no other means help, competition authorities may even resort to unbundling and break up companies.

Will we see a break-up of Amazon?

However, splitting up a company is the last option that authorities have used in very few and rare cases (for example, AT&T in 1982 and Standard Oil before that). And even in such an extreme scenario, a split-up could also have advantages, as you can see, for example, in the development of the payment service provider PayPal after it split off from eBay.

As far as the AWS segment is concerned, I think that this highly profitable and fast-growing segment would also be an excellent company. Concerning the other segments, I am more skeptical. There, the combination of the individual part generates a lot of additional value. As you have seen above, it is precisely the combination of the individual services and offerings that greatly benefit Amazon’s customers and build up the moat of the company. The network effects would fail to materialize or would even turn against the then independent segments because their reduced market presence would make them less attractive to buyers and sellers. Fewer buyers would lead to fewer sellers and vice versa.

Today, however, these are horror scenarios that I consider unlikely. Nonetheless, competition authorities can always take pinpricks. The German Federal Cartel Office, for example, ensured that Amazon has to change its General Terms and Conditions of Business vis-à-vis merchants on Amazon Marketplace worldwide. Now, Amazon is liable for intent and gross negligence vis-à-vis the merchants in the event of breaches of contract. The company also waives an unlimited right to immediate termination and the immediate blocking of the merchants’ accounts without giving reasons. As a shareholder, you should keep an eye on the development of this issue. However, panic is inappropriate.

Amazon stock analysis: There is more upside potential for the Amazon stock

The Amazon stock is the wet yield dream of every investor. The company has not only made founder Jeff Bezos one of the world’s wealthiest people. Furthermore, it has also helped many investors make excessive profits. It does not look as if Amazon will lose its growth rate in the medium term. Driven by fundamental trends such as online shopping and cloud computing, the company is rushing from one revenue record to another. Beyond strong cash flows, the highly profitable growth of the cloud segment is now generating “real profits”, although profit is still not the main focus for Jeff Bezos.

Amazon’s top priority remains growth, so don’t waste any thoughts on dividends in the years ahead. Instead, Amazon will invest every cent in expanding the existing business and opening up new markets. Measured in terms of cash flow, the Amazon stock is currently somewhat overpriced. In the past, there have certainly been more favorable valuations to buy Amazon shares. In this respect, a purchase in tranches is appropriate.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

Thank you for this very interesting article. I’m not so good in valuing growth stocks so I really learnt something again!

Thanks European DGI! It is a tricky thing with growth stocks.

Nice blog by the way… I like your 5-Bullet posts 🙂