The AT&T stock offers dividend investors a great deal thanks to the high dividend yield of currently 7 percent. However, in the last ten years, the dividend was the only thing that brought you a return at AT&T. Unfortunately, you missed out on any price gains during that time. Instead, the price for AT&T shares has fluctuated within a range of $26 to $40 over the last ten years. Currently, AT&T has once again reached the lower end of this range.

If you don’t want to miss any new articles or analysis, you can easily follow me on

or Twitter.

While the dividend is really attractive, such a dream yield usually has some shady sides. And if you look more closely, several alarm lights flash at you. AT&T has accumulated debt and liabilities of an incredible $350 billion. Millions of customers are running away, and we have the uncertain consequences of the COVID crisis on top. All this is enough to send a cold shiver down the spine of AT&T shareholders. Whether the situation is that gloomy or the high dividend might be an excellent buying opportunity, after all, we will shed light on this free stock analysis for you.

How AT&T generates money

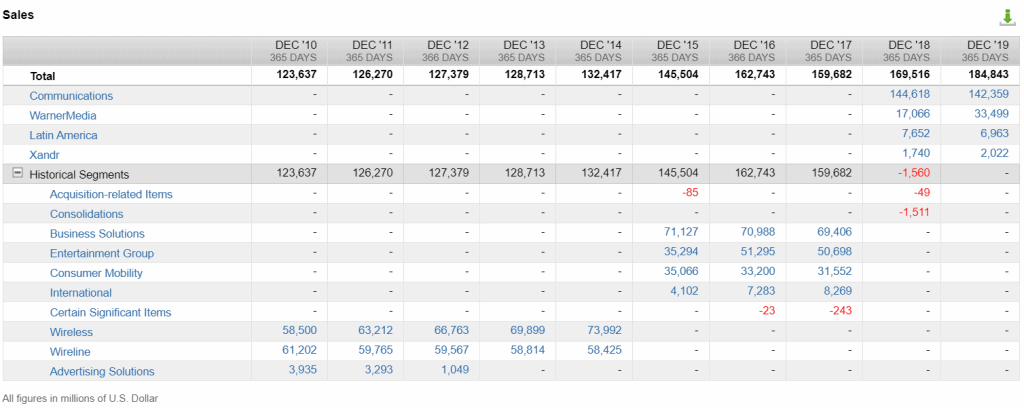

AT&T, whose roots go back to 1877, has weathered many storms and successfully adapted to changing circumstances. However, two recent takeovers have ensured that the telecommunications giant has transformed itself into a media company. In 2015 AT&T took over the world’s largest television satellite operator and program provider DIRECTV for $50 billion. And just one year later, AT&T announced its next coup with the acquisition of Warner Media, which was closed two years later for an impressive $108 billion. Management then restructured the new AT&T into four main segments: “Communications”; “Warner Media”; “Latin America”, and “Xandr”. A further adjustment was made in the second quarter of 2020 by integrating the “Xandr” segment into “Warner Media”. To better understand AT&, we nevertheless present the two segments separately.

The “Communications” segment

The Communications segment mainly comprises the traditional telecommunications business and accounted for 77 percent of revenue in the last financial year 2019. Here AT&T provides wireless and wireline telecommunications, video, and broadband services to consumers and businesses in the US. AT&T is investing heavily in the expansion of its mobile infrastructure, including the rollout of the new 5G wireless standard. 5G could become a customer magnet. The new standard opens up entirely new areas of application and business, for example, in the areas of autonomous driving and the Internet of Things (IoT).

With the subsegment “Entertainment Group”, the “Communications” segment also includes the video and TV services of AT&T (DIRECTV, U-Verse, AT&T TV, as well as AT&T TV Now). However, AT&T is currently struggling with high customer loss. Every quarter, almost 900,000 customers are lost in the premium TV segment. A large part of the customer loss can be explained by price increases and the expiry of unprofitable discount and advertising campaigns. Recently, however, gains at AT&T TV have been able to slow down the decline in customer numbers for other video and TV services.

The „Warner Media“ segment

The second-largest segment, “Warner Media”, accounts for 18 percent of total revenues and is thus much smaller than the main segment “Communications”. “Warner Media” includes the Warner services that were added to AT&T through the Warner Media acquisition, as well as a comprehensive portfolio of well-known brands and popular content, including numerous films, series, games, or channels such as CNN. Just how popular and valuable this content is can be seen in the already quite aged series “Friends”. Netflix paid nearly $100 million to continue streaming all seasons of the series in 2019.

AT&T plans to bundle all of these valuable assets into its streaming service HBO Max to compete with Netflix, Amazon, and Disney. However, AT&T is not really on track. Launched at the end of May after enormous investments, only 4 million US-customers have subscribed to HBO Max. In comparison, rival Disney+ has gained 10 million customers in the first 24 hours alone after it started in the USA, Netherlands, and Canada. AT&T management nevertheless hopes to achieve 50 million HBO Max and HBO customers by 2025.

The „Latin America“ segment

The “Latin America” segment includes wireless and wireline telecommunications, video, and broadband services for consumers and businesses outside the United States. It is the second smallest segment and accounts for just 4 percent of total revenues.

The advertisement segment “Xandr”

An exciting and new segment created in the course of the Warner Media takeover is “Xandr”, which resulted from the acquisition of AppNexus. AppNexus is a cloud-based company that offers a platform on which both advertising companies (so-called demand-side) and advertising space owners (so-called supply-side) come together in auctions. Xandr currently reaches more than 76 percent of all households and more than 200 million viewers in the U.S. and is of interest to both the demand and supply sides. Even Disney, the powerful streaming competitor, handles the advertising inventory of its entire national TV inventory through Xandr.

Even though the other segments also generate advertising revenues, AT&T intends to bundle its advertising business in this segment. The segment is still tiny and contributed only one percent of total revenues in 2019. AT&T is strengthening its position with inconspicuous but very smart takeovers. In 2019, for example, AT&T took over the clypd platform, which enables targeted advertising in the TV sector and provides advertising space on open and private marketplaces as well as analysis tools. The segment is promising due to high margins. At 2.21 percent, the Xandr segment’s share of profit in the 2019 financial year was twice as high as sales and above-average profitability compared to the other divisions.

Where does AT&T grow and where does the giant shrink?

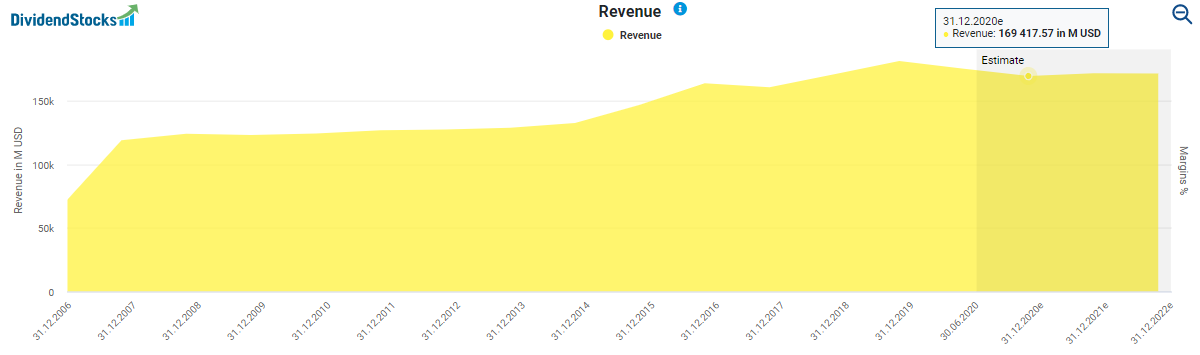

AT&T is growing slowly but steadily – at least if you take the last 10 to 15 years as a basis. Revenue rose from $118 billion in 2007 to $181 billion in 2019, but AT&T has recently suffered from a decline in revenue, which is mainly due to Corona. Revenue suffered from lower sales in cinemas, production delays, and declining advertising revenues, especially in the sports sector. From almost $9 billion in the second quarter of 2019, the revenue fell to only $6.8 billion in 2020. Revenue is expected to stagnate further in the coming years. On the one hand, Corona is proving to be a damper on revenue, and, on the other hand, it will be some time before gems such as Xandr or new technologies such as 5G bring a further boost to revenue.

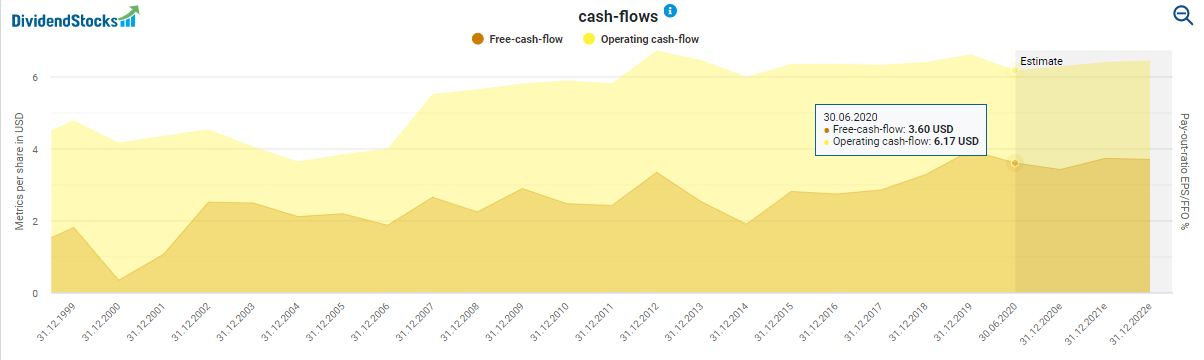

Nevertheless, AT&T generates massive and regular cash flow. However, growth is not expected here, either for the time being. Instead, both free cash flow and operating cash flow are expected to decline slightly and then more or less stagnate.

How profitable is AT&T?

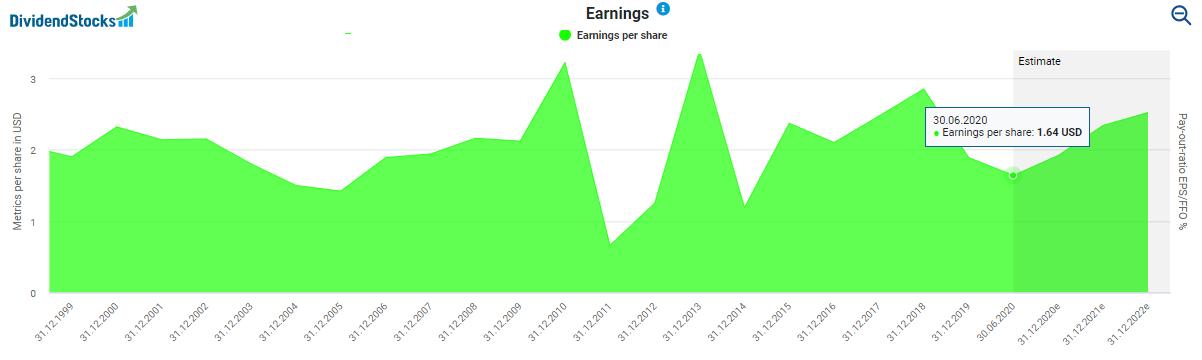

As you can see on DividendStocks.Cash, AT&T’s reported earnings fluctuate strongly. After all, AT&T makes a profit every year and is, therefore, reliably profitable. Next year, earnings per share are even expected to increase slightly, even though they will probably not reach the level of 2018.

The relatively stable margins ensure steady earnings. Although the gross margin has fallen slightly in recent years, AT&T manages overall to keep margins stable.

How safe is AT&T’s dividend?

For many dividend investors, the AT&T stock is the mother of all dividend stocks. With 36 years of dividend increases in a row, AT&T is one of the dividend aristocrats. Still, in terms of the number of years of dividend increases, it cannot quite keep up with “superstars” like Procter & Gamble (64 years), Johnson & Johnson, or Colgate-Palmolive (both 57 years). Furthermore, you should not expect high dividend increases for the AT&T share. The average growth in dividends in recent years has been a mere 2 percent per year, a neck-and-neck race with the inflation rate. By the way, the low dividend growth seems to be industry-related because even at the big competitor Verizon the dividend hardly increases. Shareholders seeking dynamic dividend growth should give AT&T a wide berth. Nevertheless, the current yield of 7 percent is tempting. Rarely has the dividend been at such a high level as it is now.

The comparison between AT&T and Mastercard illustrates the conflict between high dividend yield and high dividend growth. Mastercard’s current dividend yield of 0.5 percent is significantly lower than that of AT&T. However, the average dividend increases per year at Mastercard were more than ten times higher than at AT&T. Whoever bought Mastercard shares ten years ago with a modest dividend yield of 0.5 percent even then, has a yield on cost of 7 percent today and is thus on a par with AT&T, including high price gains. Nevertheless, there are good reasons for income-oriented shareholders to buy shares with historically high dividend yield, such as AT&T.

However, the premise for buying AT&T stock is that the dividend is safe. In particular, the strongly fluctuating profits cause continuously changing payout ratios and a high degree of uncertainty among shareholders. It is not unusual for AT&T to pay out 150 percent or more than twice the reported profit to shareholders in a few years. At first glance, the dividend does not appear to be safe. But it is worth taking a closer look!

For capital-intensive telecommunications companies that invest a lot in the expansion of infrastructure, it can be challenging to generate stable earnings regularly, which is not dramatic for dividend investors, because AT&T pays the dividend not from the reported earnings, but from the massive cash flow. These cash flows are mostly predictable because they are largely based on subscriptions. Currently, AT&T is paying out “only” 57 percent of its free cash flow as a dividend, which is significantly less than in the past. Even in the second quarter, which was strongly affected by the COVID crisis, the payout ratio based on cash flow was only 49 percent. For the full year, the company expects a payout ratio of just over 60 percent – a solid ratio for such difficult times.

Is the AT&T stock fairly valued?

Looking at the relevant multiples, the AT&T stock appears to be undervalued by more than 20 percent. For this conclusion, I focus mainly on the adjusted earnings and the operating cash flow from the last ten years due to the extremely fluctuating reported earnings.

But before you now add this undervaluation and the dividend yield and calculate an excellent total return for the coming years, you should be careful. In addition to poor revenue performance, high customer fluctuation, and a disappointing start of the streaming service, AT&T is sitting on debts and liabilities of more than $350 billion. If we only look at its 152 billion debt pile, AT&T is one of the most heavily indebted companies in the world. However, there is no sense in taking an absolute view of such figures. It makes more sense to compare debt with liquid assets and the cash flow generated. Thus, a company with little cash reserves and cash flow can go bankrupt on just a few million USD in debt. At AT&T, however, the high level of debt is offset by liquid assets of $16 billion and annual repayment capacity of almost $11 billion. Accordingly, AT&T is in a position to shoulder the interest burden and also to repay its debts. The debt ratio of just over 60 percent is also in a range that may seem high but is far from worrying.

Conclusion: The AT&T stock is interesting for fans of high dividends

Streaming, 5G, advertising, and mass content are enough to make shareholders dream. Indeed, in my opinion, AT&T has the right ingredients for a very excellent yield cocktail of dividends and price gains. However, dreams have not yet materialized in the operating business, and some promising business areas are still in their infancy. Added to this are high investments and the coronavirus, which weigh on business and the share price. Should the corona crisis lead to a worsening economic crisis, these burdens could increase further. However, the cheap money from banks and the US government’s aid programs should cushion some of the acute problems, so I am cautiously optimistic that AT&T will not be a dividend aristocrat that faltered during the corona crisis. In my view, the AT&T share is certainly worth considering for income-oriented shareholders, especially since the current dividend yield is historically high, and the dividend is secure in my view.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.