The Colgate-Palmolive stock is a classic dividend stock. It fits into the list of supposedly boring consumer goods stocks like Procter & Gamble or Unilever. In fact, Colgate-Palmolive has not skyrocketed in the last twenty years. However, with a total return of almost 260 percent over the last 20 years, investors have been well compensated for their boredom, especially since almost a third of the return has been paid out in the form of rising dividends. But all in all, the lion’s share of the returns was still generated in the form of price gains.

Today, the stock price is at an all-time high and investors are wondering whether significant returns are still to expect when buying Colgate-Palmolive stocks. In this Colgate-Palmolive stock analysis, we examine the company’s business model and determine whether a buy still seems worthwhile or if there are more promising consumer goods stocks.

The business model: How Colgate-Palmolive generates money

Colgate-Palmolive is one of the giants in the consumer goods industry, selling its well-known products worldwide. Founded in 1806 by William Colgate as a soap factory, the company divides its business into two segments: “Oral, Personal and Home Care” and “Pet Nutrition”:

To explain the business model in more detail, we will divide the large segment Oral, Personal & Home Care into further sub-segments.

Oral care products from the “Oral, Personal and Home Care” segment

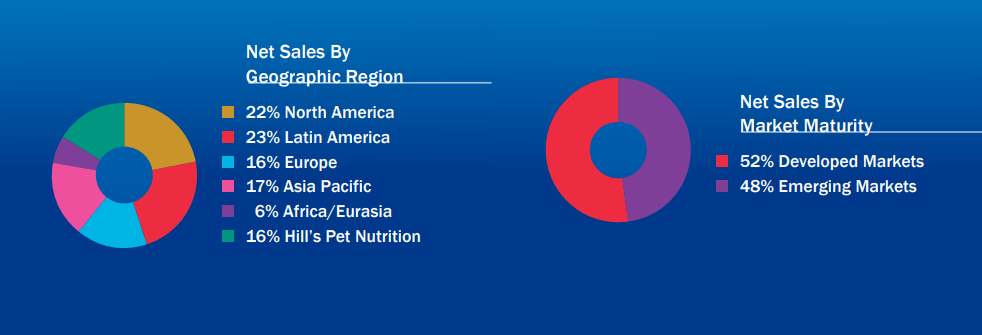

At 46 percent, oral care products such as toothbrushes, toothpaste, and mouthwashes from Colgate-Palmolive account for the largest share of sales, which includes well-known brands such as Colgate, Meridol, or Elmex. In the market for manual toothbrushes and toothpaste, the company is the global market leader with an impressive 39.9 percent market share. The market share for manual toothbrushes was also an impressive 31.1 percent in the last quarter.

Personal care products from the “Oral, Personal and Home Care” segment

Colgate-Palmolive has a strong position in the personal care market and is even the market leader for liquid hand soap. The most well-known brands are Softsoap, Palmolive, and Protex. The portfolio also includes deodorants, antiperspirants, shampoos, and conditioners. Personal care products account for 20 percent of total sales, making them the second-largest product group.

Household products from the “Oral, Personal and Home Care” segment

Colgate-Palmolive is also known for its Palmolive and Ajax dishwashing detergents. Besides, the company is the market leader with softeners and operates here under the brands Suavitel in Latin America, Soupline in Europe, and Cuddly in the South Pacific. Colgate-Palmolive generates 18 percent of its sales with household products.

„Pet Nutrition“ Segment

Colgate-Palmolive also holds a strong position as a leading supplier of specialty foods for dogs and cats in the pet food market, where it generates 16 percent of sales. Under the brand “Hill’s Pet Nutrition”, Colgate-Palmolive sells two product lines: “Hill’s Science Plan” and “Hill’s Prescription Diet”. These products provide dog and cat owners with a balanced diet with coordinated ingredients and special nutritional products against diseases.

Strengths of the business model

As a Colgate-Palmolive shareholder, you will benefit from the business model’s resilience. This resilience consists primarily of selling everyday products that are omnipresent in most of our households. The demand for these products is independent of economic cycles, so the company is immune to an economic downturn, making Colgate-Palmolive particularly attractive to risk-averse shareholders.

Another of the company’s strengths is its size and the distribution of sales across many product groups. The resulting risk diversification is reflected in the geographical distribution of revenues. The company generates just under half of its sales in the developing markets, with Latin America as the biggest region contributing only 23 percent of total sales.

There is also no particular dependency on specific significant customers. Walmart is the only company responsible for more than 10 percent of revenues. Besides, Colgate-Palmolive can sell poorly performing brands and sharpen its portfolio by adding more profitable or margin-strong brands. One example is the purchase of the Filorga brand in 2019 for USD 1.7 billion, which will strengthen Colgate-Palmolive’s position in the higher-priced skincare cream market.

Vulnerabilities of the business model

Conversely, the business model suffers from the weaknesses typical of the industry. In addition to the risk that the charisma of individual brands such as Elmex or customer loyalty may be diminished, shareholders are primarily concerned that smaller and more agile competitors could take market share from the big giants. So far, however, this concern has been unfounded. Procter & Gamble, which generates four times more revenue than Colgate-Palmolive, has recently shown that organic growth is possible from its strength. However, the fundamental problem of defensive business models is that “only” moderate growth remains. For example, Procter & Gamble has already sent shareholders into euphoria with a 6 percent increase in revenues. Accordingly, annual growth rates in the mid to high single digits are the most for this industry.

Colgate-Palmolive’s revenue development

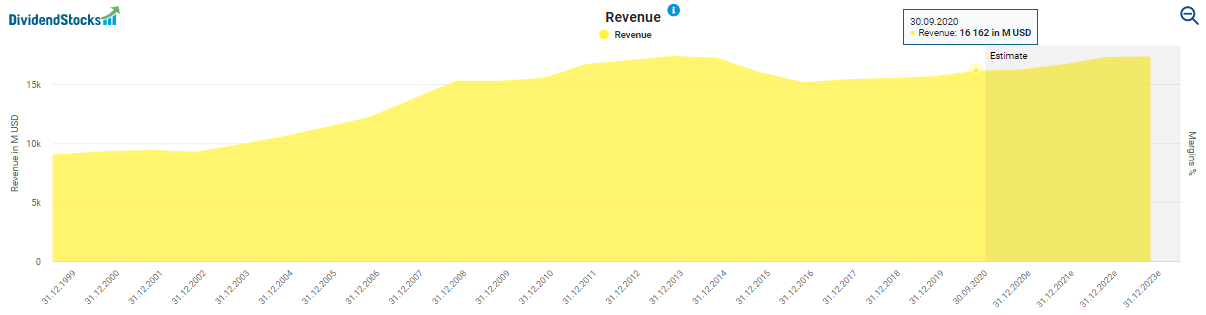

Appropriately, the strengths and weaknesses of the business model are reflected in the revenue development. For example, Colgate-Palmolive’s revenues increased to USD 15.7 billion, from USD 5.7 billion in 1990. While this is not close to growth rockets like Amazon & Co, it is a testament to a stable and growing business. Recently, there has again been good news. For example, the company recorded organic sales growth of 7.5 percent in the third quarter of 2020.

The fear that individual shareholders had at the Corona pandemic’s peak due to the revised forecast also proved to be unfounded. In 2020, both net sales and organic sales are expected to grow in the mid-percent range.

How profitable is Colgate-Palmolive?

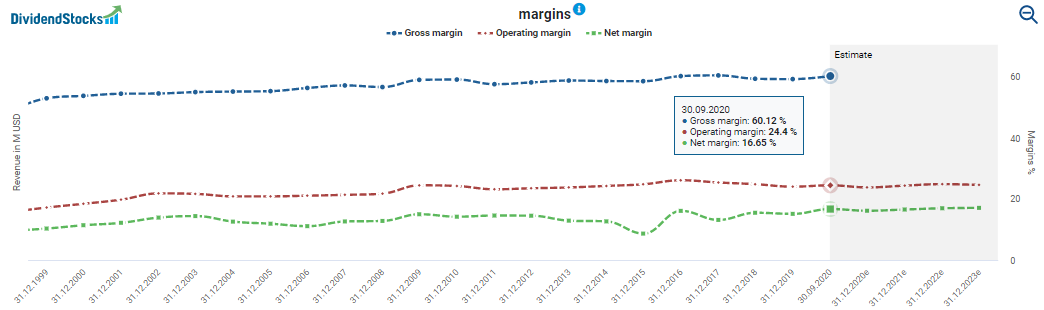

In the development of earnings, there are also no surprises. The company showed a regular increase in earnings. The only major slump occurred in 2014 due to high restructuring costs and the sharp devaluation of the Venezuelan currency Bolivar. Accordingly, these were only one-off effects that had no impact on the long-term earnings trend.

In recent years, shareholders have criticized the development of margins slightly. Since 2016, the operating margin has fallen somewhat by almost two percentage points from 26.06 percent to 24.4 percent. However, the operating margin has recently recovered slightly and stood at 24.5 percent in the third quarter (compared to 21.8 percent in 2019). The gross margin also improved slightly, rising from 59 percent to 61.2 percent, which is quite impressive, given the rampant corona pandemic worldwide.

How safe is the Colgate-Palmolive dividend?

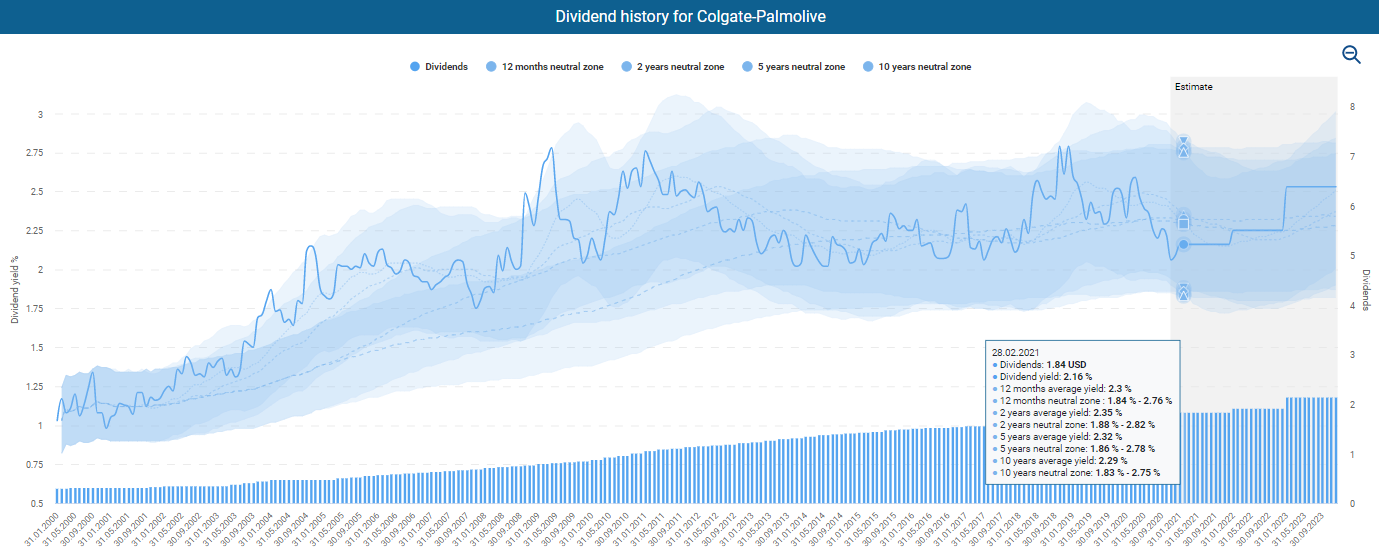

Colgate-Palmolive distributes its dividend on a quarterly basis. Following the recent increase from USD 0.43 to USD 0.44, shareholders now receive USD 1.76 per year. At the current stock price of USD 83.35, this represents a dividend yield of 2.1 percent. The dividend has increased by 3.3 percent over the last three years and by 7.1 percent over the previous ten years.

Are higher dividend increases in the pipeline?

Besides, Colgate-Palmolive has been paying dividends on an annual basis since 1895. It has even increased the payouts annually over the past 57 years. Therefore, the stock belongs to the illustrious circle of the over 120 dividend aristocrats. Next year, I also anticipate a significant increase in payouts. The last increase was quite low. Furthermore, it was mainly due to the corona crisis’s uncertainties as well as the lowered forecast for the current fiscal year.

Currently, however, management is expecting an increase in profits of almost 7 percent for 2020. The payout ratio is also below 60 percent again, so I consider an increase of 4 or even 5 percent to be probable. I, therefore, see no danger of a dividend cut in the short and medium-term.

Low dividend yield

However, fans of high dividend yields are likely to be disappointed with a current dividend yield of 2.2 percent. However, other popular dividend stocks such as Procter & Gamble only reach 2.2 percent. Church & Dwight even distributes a dividend yield of only 1 percent due to the lower payout ratio of 34 percent. Unilever, on the other hand, pays a slightly higher dividend of just under 3 percent. In short: Colgate-Palmolive’s dividend is somewhere in the golden mean, which also applies to the comparison between current and historical dividend yields.

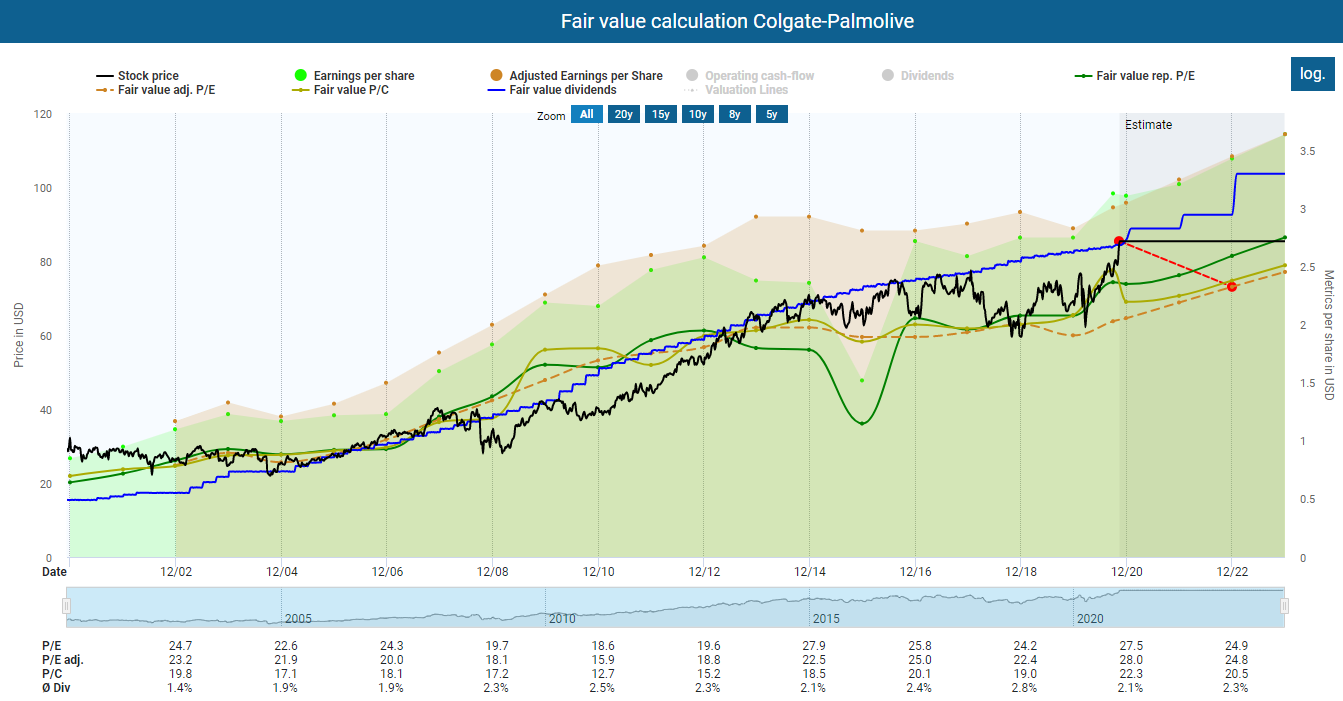

Is the Colgate-Palmolive stock fairly valued?

Like many consumer products stocks, Colgate-Palmolive is currently overvalued based on historical trends in adjusted earnings and operating cash flow. The relatively high adjusted P/E of 24 also suggests an overvaluation given the relatively moderate profit development. Only concerning the average dividend yield, we see a minimal overvaluation.

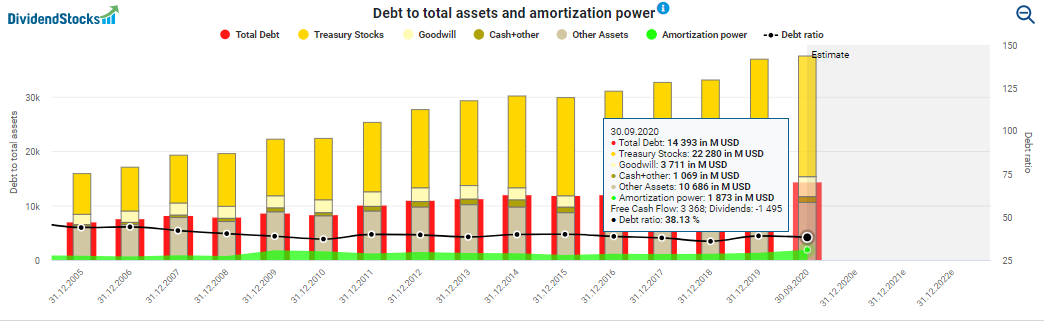

Explanations for the chronic overvaluation

Several explanations for the everlasting overvaluation of Colgate-Palmolive stock have persisted with brief interruptions since 2014. In addition to the defensive business model and the impressive dividend stability, the stable balance sheet with a low debt ratio of 38 percent (it should be noted that treasury stock is counted as an asset). The company has also reduced the number of outstanding shares from 1.3 billion to 861.8 million since 1997. Currently, the value of shares repurchased is more than USD 22 billion. Colgate-Palmolive could – at least arithmetically – offset its USD 14.3 billion of debt and liabilities in one fell swoop by selling its treasury shares and even use the remaining USD 8 billion of treasury shares to make acquisitions.

Procter & Gamble has a similarly good balance sheet, and there, too, the adjusted P/E ratio is somewhat high with 25 so you can see a correlation here. If you are looking for a somewhat cheaper investment in terms of multiples, you may take a look at Unilever. Unilever comes with an adjusted P/E ratio of just under 21, but the balance sheet is less solid, with a debt ratio of 74 percent.

Conclusion of our Colgate-Palmolive stock analysis: A low-risk investment with low return potential

For risk-averse investors, Colgate-Palmolive is a good anchor investment. Year after year, the growing and crisis-proof business generates a stable cash flow, which the company passes on to shareholders in dividends and share buybacks. However, the current valuation at a historically high level limits the short- and medium-term potential for further price gains. If you would like to put Colgate-Palmolive stock into your portfolio despite the high valuation, I recommend a stock savings plan. In the case of a reset, you can profit from the lower share prices.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.