The Facebook stock is closely linked to the company’s founder, Mark Zuckerberg. Someone who teaches himself coding as an adolescent, who is a billionaire at 23, who is one of the five wealthiest people in the world in his mid-thirties, and who has been awarded an honorary doctorate from Harvard University despite leaving university without a degree, has done many things right. Facebook’s shareholders also have reason to be happy. Since the IPO in May 2012, the Facebook stock has risen by 530 percent and recently reached a new high. However, the CEO of Facebook does not intend to retire yet. Instead, we can assume that the self-made billionaire will continue to hold the reins of Facebook in his hands.

With this introduction, I would like to welcome you to my latest stock analysis. In this analysis, we will discuss if the Facebook stock is still a buy. Furthermore, we will bring light to the persistent rumor that Facebook is one of the few tech stocks that are still undervalued.

If you don’t want to miss any new articles or analysis, you can easily follow me on

or Twitter.

If you’re considering buying Facebook shares and looking at the fundamental figures, you may notice the somewhat strange name “Facebook Inc-A”. The reason for this is quickly explained. Like Berkshire Hathaway or the Google mother alphabet, Facebook shares are divided into different classes (A, B, and C). The difference between the classes has to do with differences in voting rights. Like other companies, Facebook uses different classes of shares to limit the voting weight of its shareholders.

Besides, Mark Zuckerberg allegedly wants to sell and donate 99 percent of his shares, but still wants to keep control of his baby as long as possible. As a result, Facebook’s A-shares carry only a single voting right, while the B-shares carry tenfold voting rights and are mainly held by employees, for example, co-founders Eduardo Saverin, Dustin Moskovitz, and Christopher Hughes. However, a few years later, non-voting C-shares were added, which diluted the value of the existing shares accordingly. C-Shares make it easier for Mark Zuckerberg to keep his promise and donate C-Class shares to Facebook without losing voting rights.

How Facebook generates money

Facebook started its success story with the social network of the same name, on which friends, colleagues and like-minded people can connect and exchange information. However, Mark Zuckerberg is steadily expanding his company’s portfolio by buying up companies, including competitors.

Facebook, WhatsApp, Instagram, and 19 billion USD for revenue of 1 million

In 2012, Facebook acquired the Instagram platform for almost one billion USD, where users can share photos and videos and follow each other. In 2014, Zuckerberg also bought the growing messenger competitor WhatsApp for an unimaginable $19 billion. At that time, the sum was incredible because WhatsApp had revenues of nearly $1 million, which consisted of the purchase price for the app download and an annual fee in some countries. This meager income source dried up completely when Facebook made the app available to users completely free of charge.

Why has Facebook put nearly $20 billion on the table for WhatsApp? One aspect was undoubtedly the growing importance of WhatsApp as a messenger, which Facebook could not match with its in-house messenger. But just as valuable was the data treasure that WhatsApp holds for Facebook. Although communication on WhatsApp is encrypted, Facebook gained access to contact lists, name, birthday, status, profile pictures, and other data that users voluntarily shared. The additional users and their data are fueling Facebook’s growth engine. Therefore, we will take a closer look under the hood of this engine, how it works, and why it was worth paying $19 billion “just” for data.

Advertisement as a growth engine

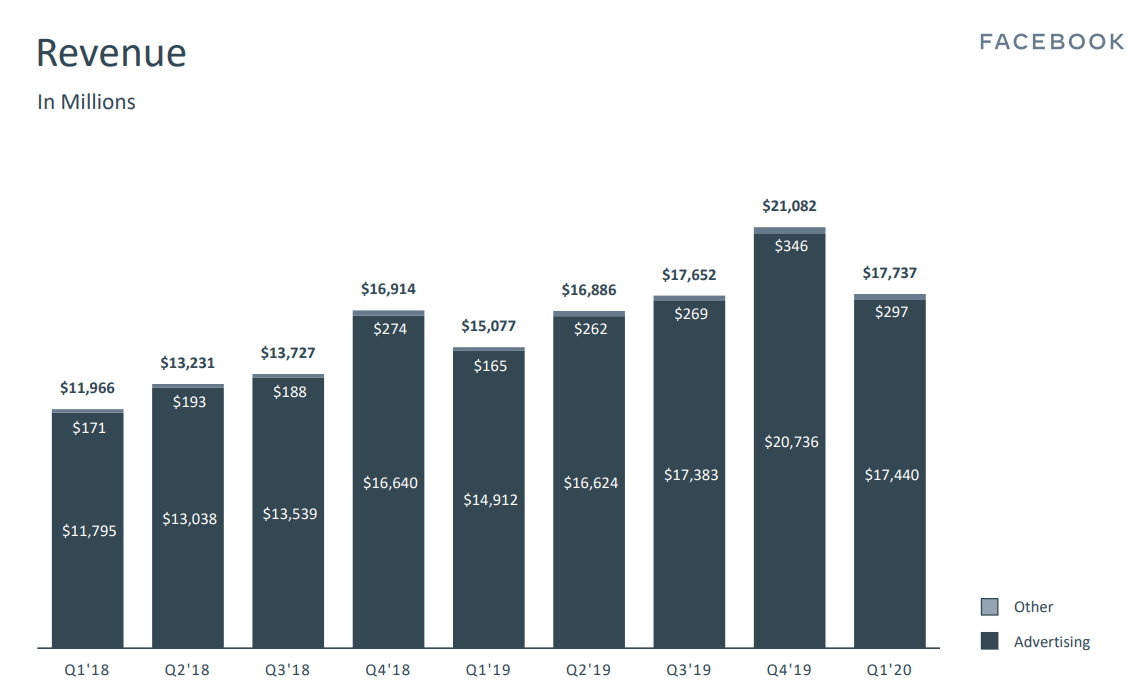

The business model of Facebook is advertising. Facebook makes its platforms available to users free of charge, but not out of pure charity. It is not the platform that is the product, but the users for whom other companies pay to place targeted advertisements on the platform to market their products. Although Facebook has repeatedly tried to diversify its business, advertising revenue remains the most important source of income. The weight of the other revenue sources is negligible and was less than $300 million last quarter. Compared to total revenues of $17 billion in the first quarter of 2020, this is just 1.6 percent.

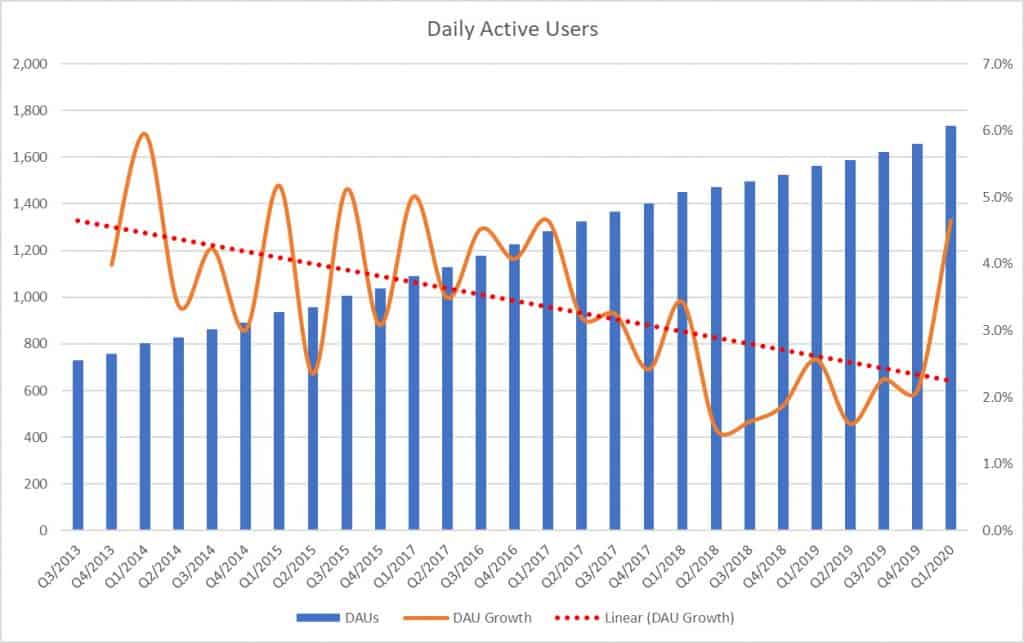

Conversely, Facebook cannot be blamed for monetizing its active users as its most valuable assets to the limit. And the number of daily active users is still growing in all parts of the world. Even the long-serving core product Facebook has still not reached it peak but continues to record growing user numbers every quarter. However, the speed of growth has been declining for years. Due to the corona pandemic, the number of users increased in the first quarter of this year, but this special effect will fizzle out as the initial restrictions are eased worldwide. The moving average in the form of the red dotted line shows the long-term declining growth of daily users.

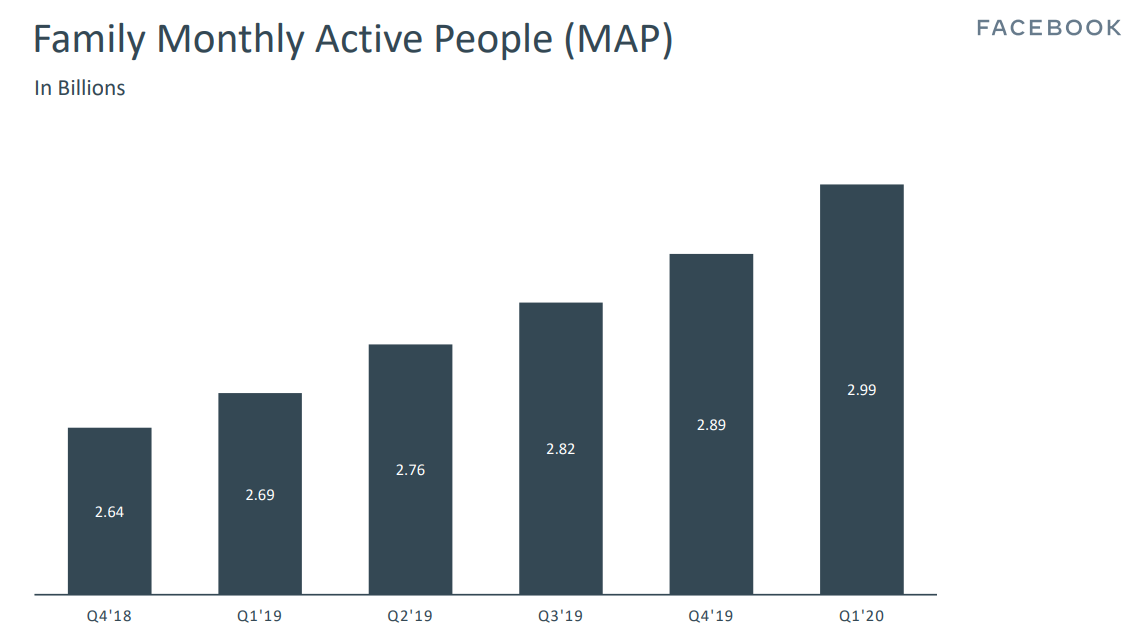

While the number of daily users above only includes the use of the Facebook platform, the following figures show cross-platform growth including WhatsApp and Instagram. In the first quarter of 2020, nearly 3 billion people will use Facebook services at least once a month. A truly impressive number.

Currently, about 4.5 billion people in the world have access to the Internet. A proud two-thirds of them use one of the Facebook platforms at least once a month and provide the company with valuable data and information through their use. Facebook can, in turn, use this data to place targeted advertisements for other companies’ products and services. Such personalized advertising is very valuable for companies because it promises a higher conversion rate (=successful conversion of potential customers to actual buyers) than conventional forms of advertising with immense wastage.

Facebook also benefits from so-called negative network effects, which we already discussed in our Amazon stock analysis. If all users use Facebook services, hardly anyone will bother with another messenger that only a fraction of their friends and acquaintances use. Facebook benefits from this moat. Likewise, with every new service, new users are added, who, in turn, provide Facebook with more data, which increases the advertising value of the Facebook platforms, so that even more money is spent on targeted advertising.

Further acquisitions

Like Alphabet, Facebook has been trying to put its revenues on a broader basis to make it less dependent on the advertising business. To get closer to its goal, Facebook has acquired companies here and there or bought shares in other companies. Particularly early examples are the takeover of the virtual reality hardware manufacturer Oculus VR in 2014 and of the game developer Beat Games, also active in the field of virtual reality, last year. The so-called Virtual Reality creates a virtual environment using computer technology, into which users can immerse themselves, for example, through glasses or a mask.

Facebook has already made two more purchases in the current year 2020. Once Facebook acquired a 10 percent stake in Jio Platforms, a subsidiary of the Indian Reliance Industries. In addition to India’s largest telecommunications company with almost 400 million users, it hosts several other apps, such as the Jio Money app, which offers digital payment options. In addition to Facebook, Intel, Google, the private equity firm KKK, as well as Qualcomm and the Saudi Arabian sovereign wealth fund have invested in Jio Platforms. Facebook hopes that this investment will give it a better foothold in the Indian market and provide insights into user data and usage behavior.

Besides, Facebook acquired the GIF database “Giphy” in spring 2020 to integrate it into its platforms. A GIF (“Graphics Interchange Format”) is a small short video that hardly takes up any storage space, usually transports a specific message, and allows users to express themselves in chats.

What the future holds for Facebook

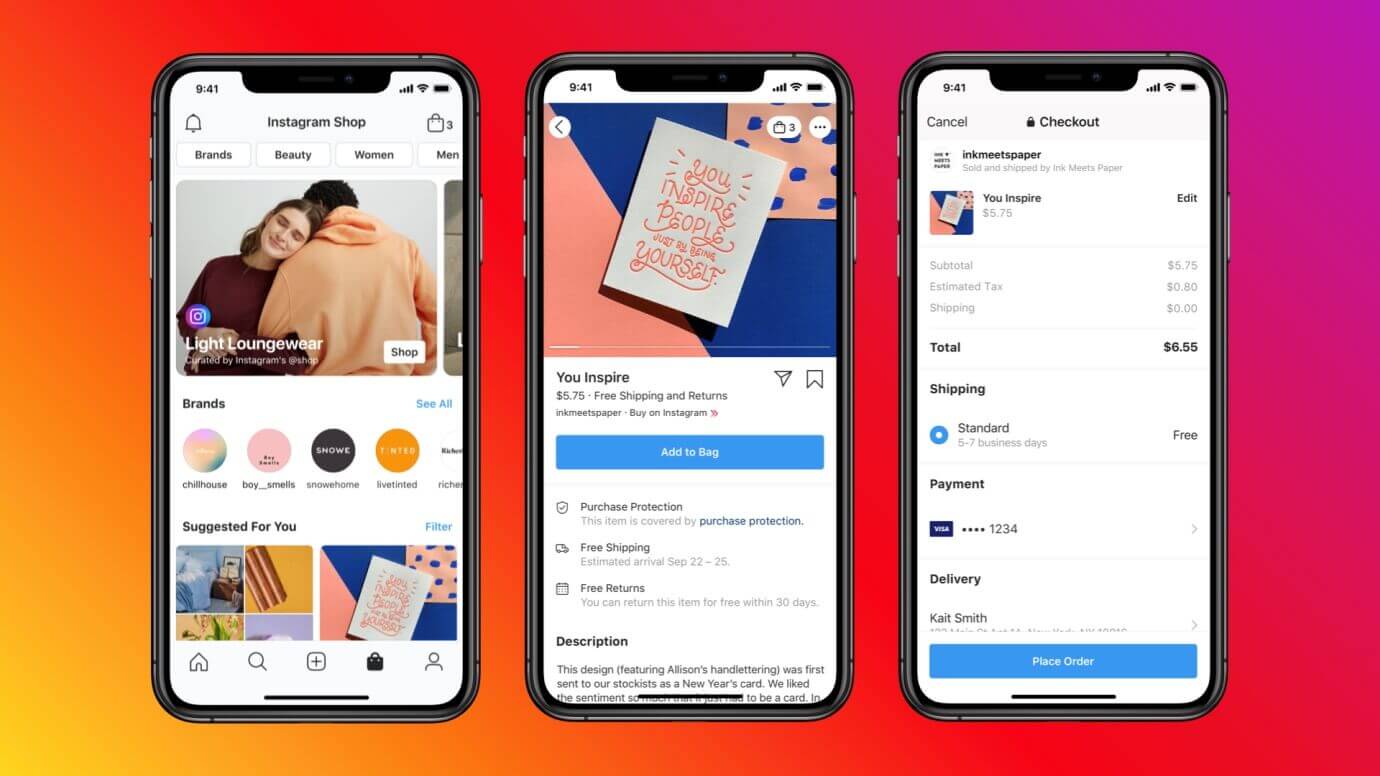

I think that Facebook will find other ways to monetize its data treasure in the future. The management is very experimental. The possibilities of using Facebook as a sales platform are particularly exciting. With Facebook Marketplace, a first possibility has been created to allow private users and smaller businesses to sell mainly local products. Furthermore, Facebook and Instagram Shops were introduced in May 2020, enabling sellers to post their online shops directly on Facebook platforms. You can imagine that Facebook provides shop windows on its services where companies can post and even sell their products. The redirection to the company’s website, which must also have implemented an online shopping system, is now a thing of the past.

The internet currency Libra, which was co-designed by Facebook, shows Mark Zuckerberg’s desire to expand the company. Facebook wants to offer a wallet application, a kind of digital wallet, through its subsidiary Novi (former Calibra), which will allow users of Facebook, WhatsApp, and Instagram to make online purchases conveniently. WhatsApp Pay, which is attempting to launch in Brazil with considerable regulatory problems, is also aiming in this direction.

I suspect that Facebook is increasingly developing its ecosystem in the direction of a digital “mall” or digital “shopping center” where people meet for social reasons and, at the same time, buy products alone or together. The advantages over Amazon and the Amazon Marketplace are apparent. At Amazon, customers have to navigate to Amazon; at Facebook, customers are already there in the form of active users and only need to be picked up by the company present there. And who picks up the customers? Facebook, of course, using personalized advertising.

Growth and profitability

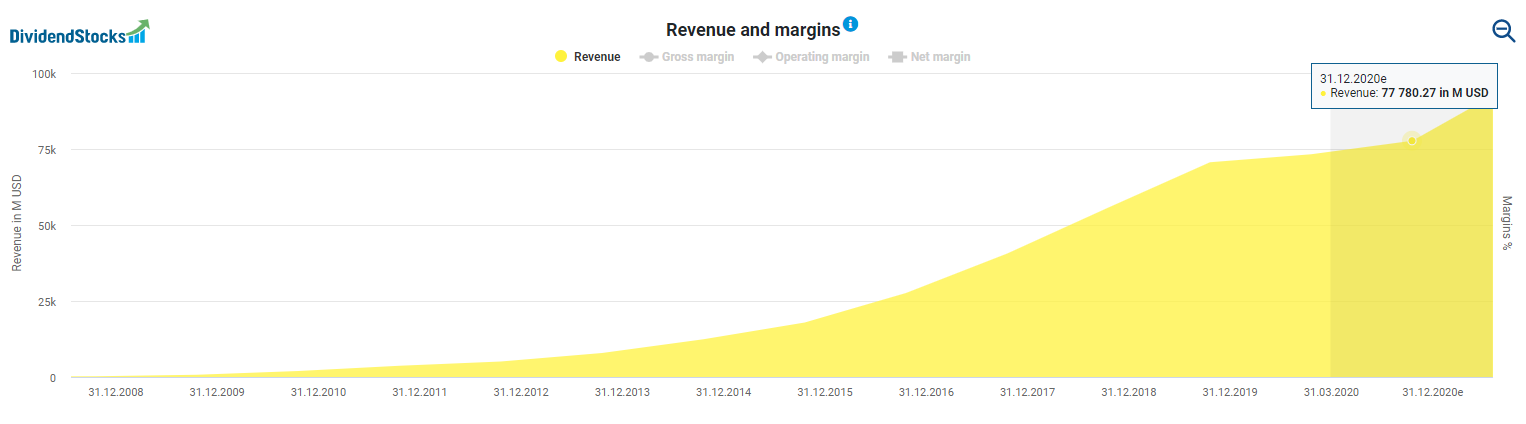

Facebook is one of the tech companies that became profitable relatively quickly and has continuously increased revenues and profits. While the revenue in 2009 was only $777 million, the turnover in 2020 will probably be $77 billion. Facebook has thus increased its revenues a hundredfold in just under 11 years. Although the current corona pandemic is driving increased Facebook platforms’ usage, revenues are declining as many companies have seen their advertising budgets shrink in the wake of the crisis.

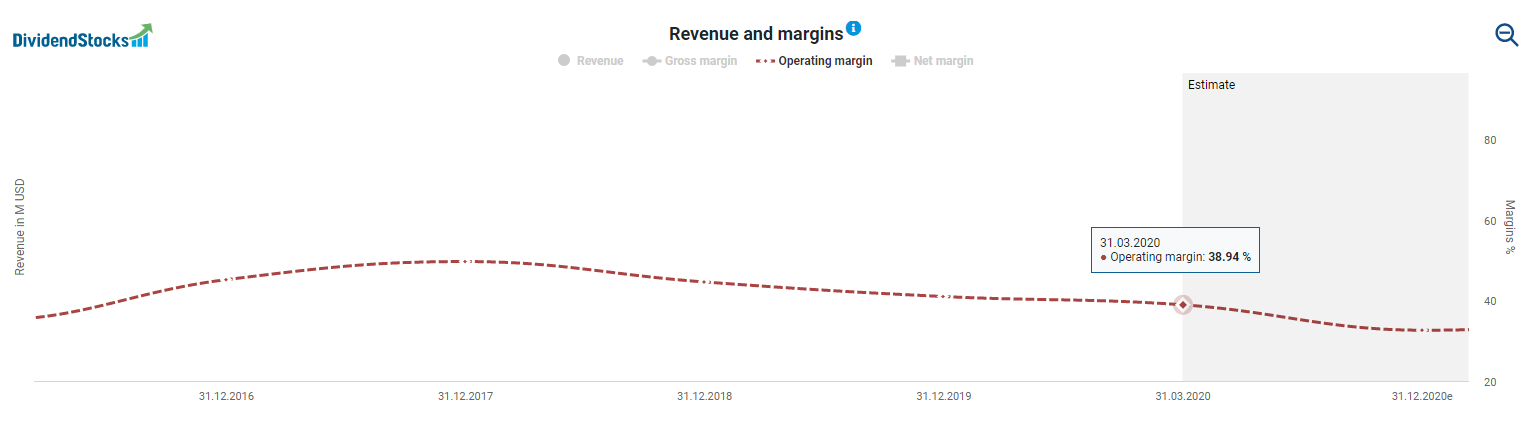

Profitability has fallen significantly in recent years. Data scandals such as Cambridge Analytica or abuse of the Facebook platforms to agitate or spread alleged “fake news” cost Facebook a lot of money. To avoid further scandals, Facebook is investing massively in data security, data transparency, and data control and new employees, at the expense of operating margins. These fell from just under 50 percent to a predicted 33 percent for the current fiscal year.

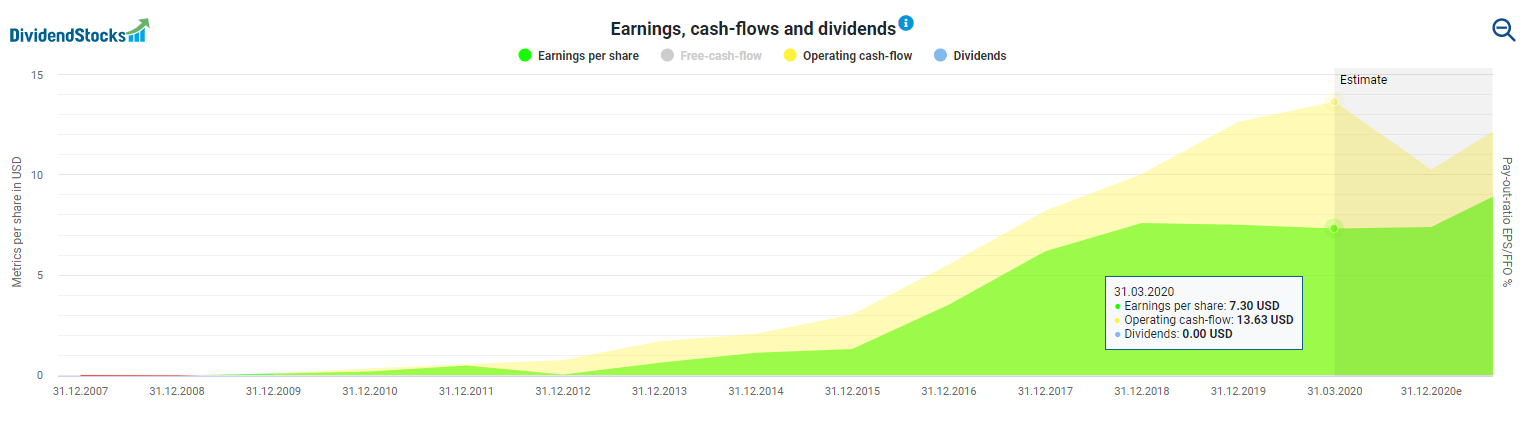

The declining margins explain why earnings are only moving sideways despite rising revenues since 2019. Improvement is only in sight for the financial year 2021, and only then should earnings pick up again with even more substantial growth in revenues. It is nevertheless impressive how quickly Mark Zuckerberg succeeded in making the company profitable. In 2015, cash flow and earnings exploded before stagnation sets in due to falling margins. Once margins have settled at the lower level, further sales growth will bear fruit again, and profits and cash flows should rise again.

Facebook stock analysis: Fundamental valuation

As you can see in the dynamic valuation below, historical cash flow and reported earnings of the last four quarters indicate a slight overvaluation. This overvaluation increases when we look at the forecasts for the current fiscal year, which assumes a decreasing cash flow with stagnating earnings. I have used the period from the fiscal year 2017 to calculate the valuation because Facebook was previously valued significantly higher. At that time, margins were still rising and peaked at just under 50 percent, before margins and multiples such as the P/E ratio went south. The situation is not expected to improve until the next financial year, in which case the share would be roughly fairly valued at today’s price level, only to be undervalued in the fiscal year after that finally.

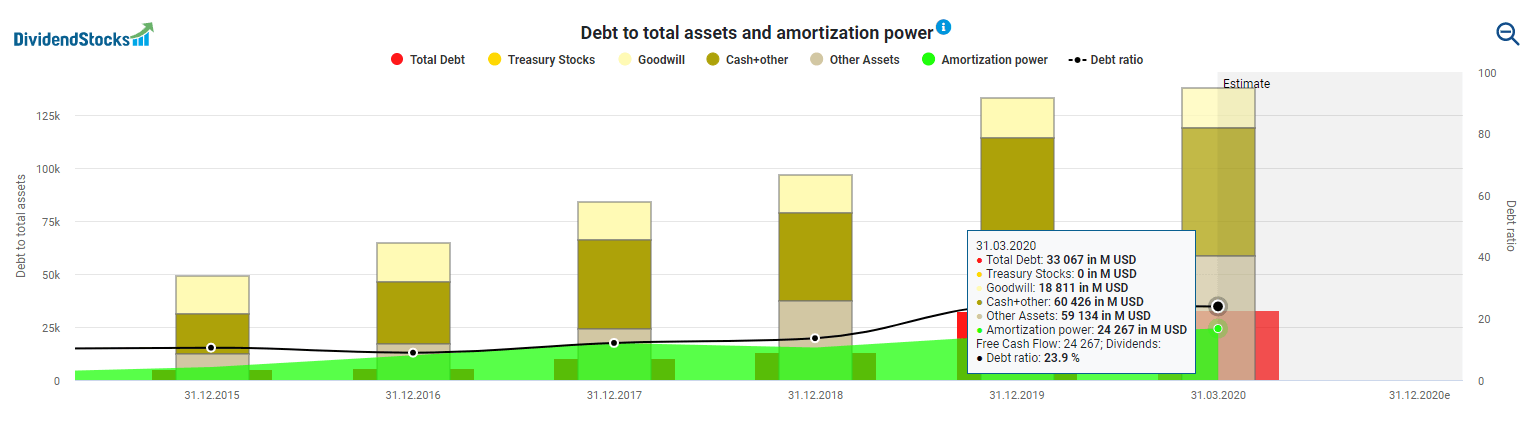

A definite plus point for Facebook, however, is its solid balance sheet. Facebook has a debt ratio of just 24 percent. The company sits on a cash mountain of over $60 billion that reaches into the clouds. In one fell swoop, it could pay off all its debts, including liabilities, and it would still have $30 billion in its hands to use it for investments, acquisitions, share buybacks, or even dividend payments. I think Facebook could easily manage a second lockdown in the wake of the COVID 19 pandemic, even if companies cut their advertising budgets due to economic difficulties.

Further risks of the Facebook stock

To find a company from the group of FAANG stocks (Facebook, Apple, Amazon, Netflix, Google) with a solid balance sheet and a moderate valuation seems unusual in the current market phase. The above mentioned lower margins are a significant reason for the comparatively low valuation of Facebook. Two other reasons for the moderate valuation are the potential risks that you are taking with the Facebook share in your portfolio.

High dependence on advertising

Facebook is still struggling with its strong dependence on advertising. The advertising business is vulnerable from two sides. On the one hand, the popularity of Facebook services could decline, and users could migrate. On the other hand, companies could reduce their advertising spending for economic, social, or political reasons or boycott Facebook as an advertising platform altogether.

The possible break-up of Facebook

As with Amazon, another threat lies in the market power of Facebook. Competition authorities around the world are looking at Facebook with a critical eye, competitors and politics are demanding, for example, that WhatsApp should be spun off from Facebook. However, such spin-offs, or unbundling, are very rare. However, the German Federal Cartel Office has already prohibited Facebook from combining user data from different platforms. As a consequence, this decision leads to an internal unbundling of the company. Although the Düsseldorf Higher Regional Court overturned the decision, the Federal Supreme Court recently ruled in favor of the Federal Cartel Office. Accordingly, I would not ignore such developments in the valuation of the Facebook share.

Facebook stock analysis conclusion – supposedly low valuation tempts to buy

With the Facebook stock, you get a tech company with enormous market power. Furthermore, you put a lot of growth potential in your portfolio. But be careful: the stock is not as cheap as it seems at first glance. Since 2017, the market has rightly been giving Facebook a sharp discount. The declining margins are, and Facebook’s dependence on advertising revenues are the main reasons for this. Political discussions and antitrust demands for unbundling are also weighing on the share price.

Conversely, however, the advertising business is still going strong. I may open up new revenue channels such as Facebook Shops and Instagram Shops. Besides, Facebook has a bursting war chest, so that it can simply buy up up emerging competitors if necessary. We will see whether Facebook will be able to improve the margin and to generate new revenue streams with advertising alongside the bread-and-butter business. If so, today would be a similarly favorable entry opportunity as at Microsoft when Steve Ballmer was still in charge.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.