It could have been so pleasant for Henkel’s shareholders. Those who invested in Henkel shares during the financial crisis between November 2008 and July 2009 benefited from price gains of over 500 percent. Annual price increases averaging 25 percent drove the share to a new all-time high by mid-2017. The champagne corks at Henkel popped.

However, as the economic downturn in the core business slowed, the party hangover set in. The Corona crisis caused a further slump in the neck. In the meantime, the Henkel share price fell by more than 40 percent, and the share is still almost 30 percent away from its all-time high. Welcome to a new fundamental analysis on the TEV blog. This time we will have a look at Henkel and see if this is a bargain.

If you don’t want to miss any new articles or analysis, you can easily follow me on

or Twitter.

The business model: How Henkel generates money

Henkel is a globally active consumer goods company that has been owned by the Henkel family since its foundation by Fritz Henkel in 1876. The Henkel family currently holds 61.54 percent of the ordinary shares. Dr. Simone Bagel-Trah, the great-great-granddaughter of Henkel founder Fritz Henkel, is also Chairwoman of the Supervisory Board.

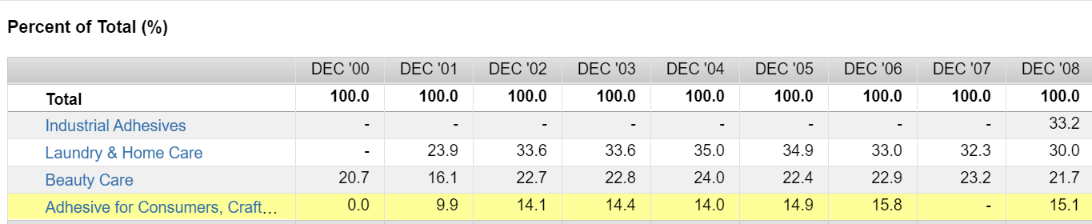

The segments – From adhesives to laundry care products

Henkel divides its business into four segments (. In the following, we have grouped together the segments “Industrial Adhesives” and “Adhesives for Consumers” as well as “Beauty Care” and “Laundry & Home Care”.

The „Adhesive“ Segment

The segment with the highest revenues is Henkel’s Adhesive business. It generates almost 40 percent of total revenues and comprises a broad portfolio of adhesives, sealants, and functional coatings. Together with the American conglomerate 3M, Henkel is the leading manufacturer in these areas.

The Pritt and Pattex brands, in particular, should be well known. However, the biggest buyers are not consumers, but smaller craftsmen and industrial companies. Henkel’s adhesives are used in industrial applications to manufacture cars, aircraft, computers, books, refrigerators, cell phones, furniture, textiles, packaging, and magazines, among other things.

Due to its industrial customers, the segment is relatively cyclical and reacts sensitively to economic downturns. For example, in recent years, Henkel has clearly felt the effects of the economic downturn in the automotive industry. This dependence on the economy contradicts the somewhat defensive nature of the other business sectors. It would, therefore, be exaggerated to regard Henkel as a company with a crisis-proof business model. Conversely, this is a luxury problem. The segment has grown organically in the past and comparatively strongly through acquisitions (for example, the adhesives business of the British chemical group ICI). For example, the adhesives business, which was still operating under a different name in 2004, accounted for just 14 percent of total revenues.

The „Beauty Care“ and „Laundry & Home Care“ segments

By contrast, the other segments, with which Henkel together generates almost 60 percent of its sales, are much more defensive and conservative. The “Beauty Care” segment generates 19 percent of revenues and includes hair, body, skin, and oral hygiene products. With its Schwarzkopf and Syoss brands, Henkel has strong and world-renowned brands in its portfolio. In the field of professional applications for the hairdressing business, the company is the clear market leader with its “Schwarzkopf Professional” products.

This leaves the”Laundry & Home Care” segment, which with the Persil and Perwoll brands, includes the company’s best-known products. In addition to detergents, Henkel also sells dishwashing detergents, surface cleaners, toilet cleaners, air fresheners, and offers electronic insect protection products.

Henkel – a dynasty

It is true that the management of a company by the founding family is no guarantee for an above-average return or a future-proof business model. Nevertheless, there is a connection between family ownership and far-sighted management. Thinking is less about quarters, but rather about years or even generations. I consider the company’s strong ties to the founding family and their will to maintain and increase success in the long term to be advantageous and am pleased to be able to benefit from this through a shareholding.

Growth problems and future plans

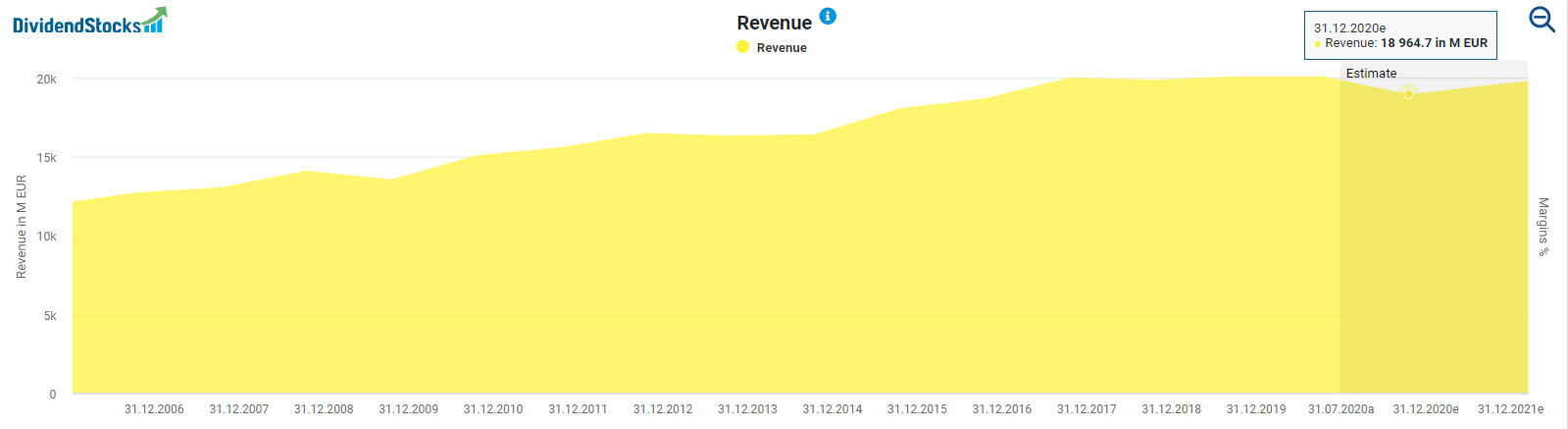

However, revenue growth has slowed down in recent years. Since 2008, revenues have risen relatively rapidly from EUR 13.5 billion to EUR 20 billion in 2017, but have stagnated since then, reaching only EUR 20.1 billion in 2019. Although Henkel has not yet published a forecast for 2020, analysts estimate that revenues will fall below EUR 19 billion.

In addition to the decline in demand for industrial adhesives, Henkel was particularly hit by the lock-down in the first half of 2020. As a result, revenues in the “Beauty Care” segment fell by an impressive 8.5 percent and by as much as 12.8 percent in the second quarter, which was primarily due to the forced closure of hairdressing salons. However, the coronavirus is not to blame for the “Beauty Care” segment’s growth problems, which have been persisting for some time. Just take the first quarter of 2019 as an example. While Procter & Gamble grew by 9 percent in its “Beauty” segment, Henkel recorded a 2.2 percent drop.

However, the company is making considerable efforts to return to growth once the corona crisis has been overcome. Like Procter & Gamble before it, it is trying to focus on particularly strong brands. Accordingly, it has identified brands and product categories in its consumer business with total revenues of more than one billion EUR, half of which it intends to sell or close. As we have seen at Procter & Gamble, it may well take longer for such a transformation process to be successful. So anyone who has missed the excellent performance of Procter & Gamble will find in Henkel a company that is trying to return to growth with the same means.

How profitable is Henkel?

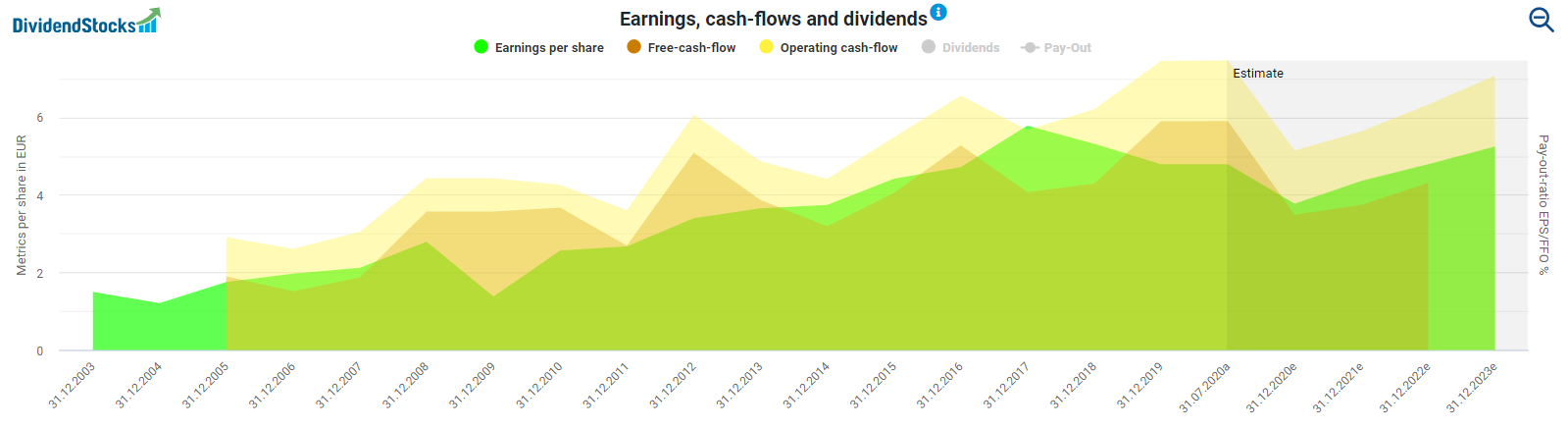

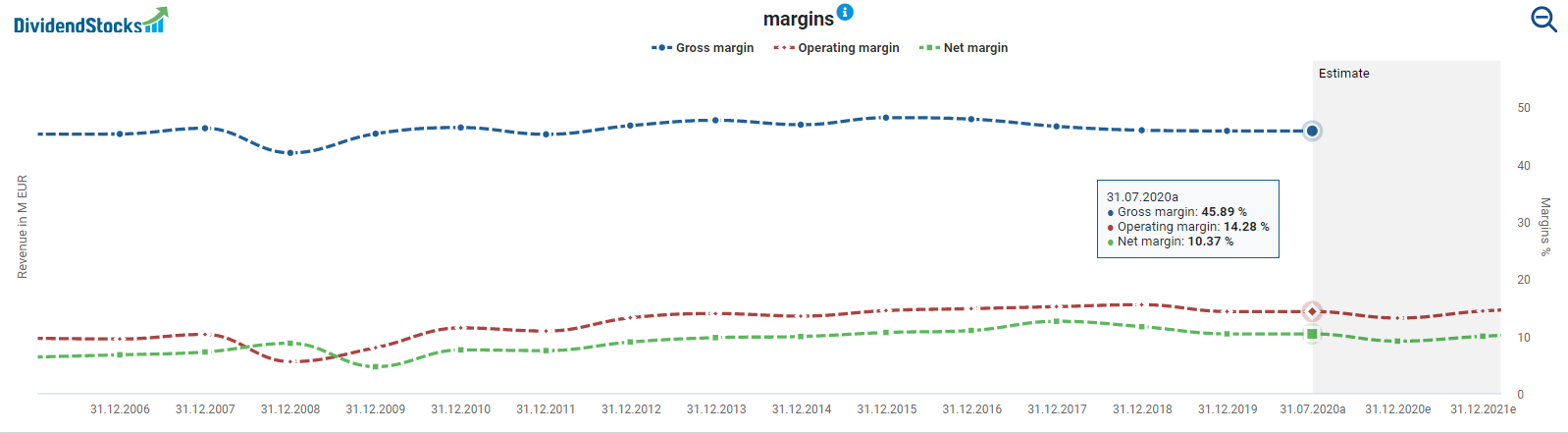

Although the recent revenue trend has been somewhat disappointing, Henkel is still profitable and generates positive cash flow. However, you should not expect any significant upswings in the medium term. The times of high growth are over for now. Increased investment costs, the ongoing restructuring of the Group, and the Corona crisis’s consequences are likely to cause a significant slump in profits and cash flow.

The slight decline in margins (net and operating) over the past two years reflects the falling stock prices. Even if the corona crisis is likely further to reinforce the trend of falling margins this year, the next financial year should see a slight upturn. Besides, the fluctuations are so small that I do not pay too much attention to them. Instead, they are linked to global economic developments and the Group’s restructuring and are entirely normal in such phases.

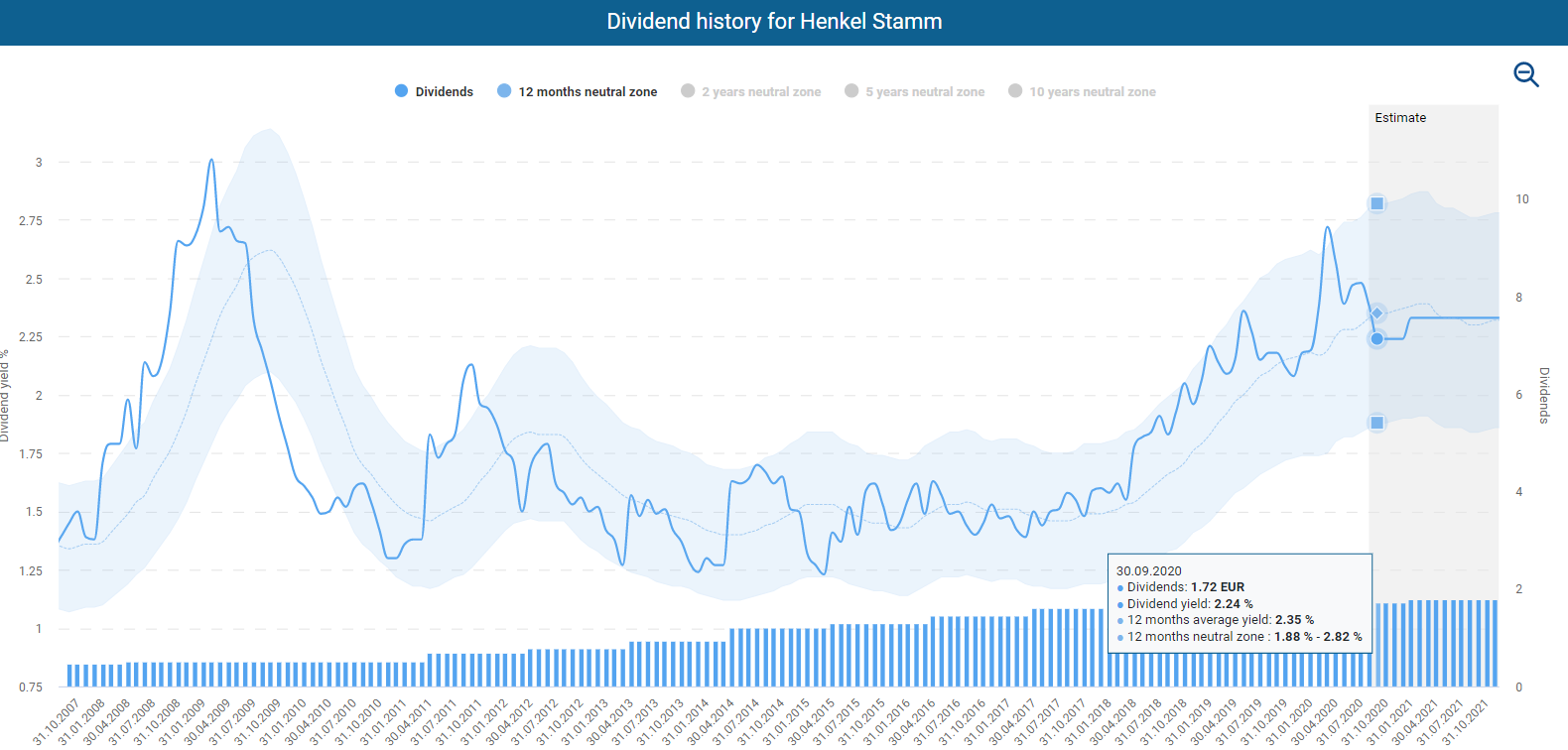

The Henkel dividend – a chapter of its own

As a dividend share, Henkel is interesting for investors who want to build up a predictable passive income. However, there are two Henkel shares. You will now find out which of the two is probably the better choice for you.

If you want to buy Henkel stocks, you have the choice between the ordinary and the preferred stocks. Even though Henkel pays a 2-cent higher dividend on the preferred stocks, this advantage is offset by the approx. 15-percent higher stock price compared to the ordinary stock, which is why the dividend yield of 2.1 percent for the preferred stock is lower than that of the ordinary stock at 2.4 percent despite the higher dividend.

If you exclusively look at the dividend yield, Henkel’s ordinary stock appears more attractive. However, compared to the preferred stock, the ordinary stock is less liquid and is not represented in any index, which means that you theoretically have to expect a wider trading margin (the so-called spread) when buying and selling the ordinary stock. I hold some Henkel ordinary stock in my portfolio. From my own experience, I can tell that I have never had problems with buying them because of poor tradeability or high spreads.

Is the Henkel dividend safe?

The Henkel dividend amounts to an exceptionally high 2.3 percent, a historic figure. The dividend yields were only higher in the wake of the financial crisis and at the height of the Corona crisis.

Unlike its competitors Procter & Gamble, 3M, or Unilever, Henkel is not a dividend aristocrat that has increased its dividend payments every year for at least 25 years. This year, for example, the management merely kept the dividend stable compared. Although Henkel does not increase the dividend every year, it does raise it regularly. Since 2005, the amount has quadrupled. For investors who invested in Henkel in 2005, the yield on cost is still over 7 percent.

Henkel’s management plans to distribute a dividend of 30 to 40 percent of profits once a year. Most recently, the payout ratio was 34 percent. Due to the expected decline in profits, the payout next year could exceed the 40 percent limit. I could imagine that management would make an exception to its distribution policy due to the extraordinary burden of the coronavirus and keep the dividend constant instead of cutting it. However, this is not guaranteed.

Is the Henkel stock fairly valued?

The graph shows that the Henkel share was overvalued from 2013 onwards. It was not until 2017, when the share price fell, including the Corona crash, that the share returned closer to its fair value. Although the Aktienfinder cannot show you the past fair values for the adjusted profit due to a change in accounting by Henkel, the comparison multiples running in a relatively narrow band show that Henkel is currently trading relatively close to its fair pre-corona value.

The adjusted P/E ratio of under 16 also signals a fair valuation. Thus, Henkel is cheaper than the struggling company 3M, which currently has an adjusted P/E ratio of 18. Procter & Gamble and Unilever also all have a higher valuation. With an adjusted P/E ratio of 18.5, Henkel’s preferred stock is slightly more expensive than the ordinary stock with a P/E ratio of 16. The more favorable valuation thus also speaks in favor of the ordinary stock.

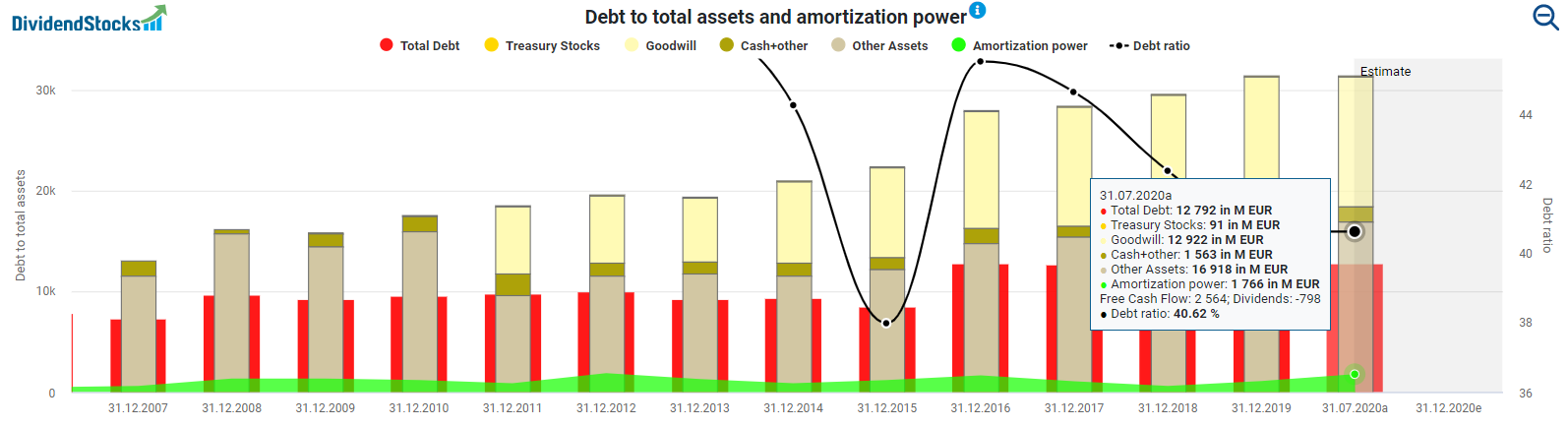

What I like about Henkel is the solid balance sheet. With a debt ratio of 40.6 percent, Henkel is above the ratio of Procter & Gamble (32.6 percent), but well below the ratio of Unilever (74 percent) and also 3M (45 percent). Besides, with an amortization power of EUR 1.7 billion, Henkel is liquid enough to address its EUR 12.8 billion debt, which means it would take 7.5 years to pay off the debt. This is significantly less than Procter & Gamble, which would need more than 11 years to pay off the debt despite its lower debt ratio due to its lower repayment power.

Conclusion: Henkel stock – Solid dividend stock with potential

The Henkel stock is still under pressure. The economic slowdown, the poorly performing “Beauty Care” segment, and the coronavirus are weighing on the stock price. Nevertheless, the management is sticking to its long-term plans and intends to return to its old-growth by means of a portfolio adjustment. The long-term approach, the business model, and the family dynasty behind the company are still convincing. However, you don’t need to expect dream returns because of the current consolidation of the business. But it is quite possible that Henkel is standing right where Procter & Gamble stood a few years ago.

At the current valuation level, Henkel is one of those companies that I keep adding to my portfolio. If you pursue a similar investment strategy and would like to hold the Henkel stock for the long term rather than trade it, I recommend that you buy the ordinary stock. Although it is less liquid, it has a more favorable valuation and higher a dividend yield.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

Thanks for the interesting article. I’ve had Hen and I’ve been following since. Quality stock but at the same price as last year September and conditions are very different. With regard to the dividend, the consensus(https://vara-services.com/henkel/) is actually to go down! Maybe there is an opportunity in the 65/67 € range.

Hi João Luz,

I am glad that you come by and share your thoughts.

“the same price as last year September and conditions are very different.”

That is not correct, I guess. In EUR (home currency), Henkel trades around 20 percent below its past September price.

Concerning the dividend. Yeah, this could be a close call.I hope, they keep it stable. We will see.

Best

TEV