The Intel stock has performed disappointingly this year. While AMD has gained about 75 percent and Nvidia even about 120 percent year to date, Intel shareholders will probably close the year with stock price losses despite a relatively high dividend yield of almost 3 percent. After a strong start into 2020 at an all-time high, Intel´s stock price fell by over 30 percent. Now, however, multiples strongly indicate that Intel is a bargain. In this Intel stock analysis, we show you whether the Intel stock’s high price losses are exaggerated. Besides, we point out some pitfalls in stock valuation. We will show how supposedly shareholder-friendly management can have a long-term negative impact on the company’s success and, ultimately, on the stock price.

Intel’s business model: How the chip giant generates money

Intel is one of the largest semiconductor manufacturers in the world. Intel has a market capitalization of USD 210 billion. That makes the company still almost worth twice as much as AMD with a market capitalization of USD 113 billion. Only Nvidia passed Intel in the middle of the year. Thanks to rising share prices, Nvidia capitalized over USD 341 billion. All three companies compete in crucial future markets such as CPUs (Intel and AMD) and autonomous driving (Intel and Nvidia).

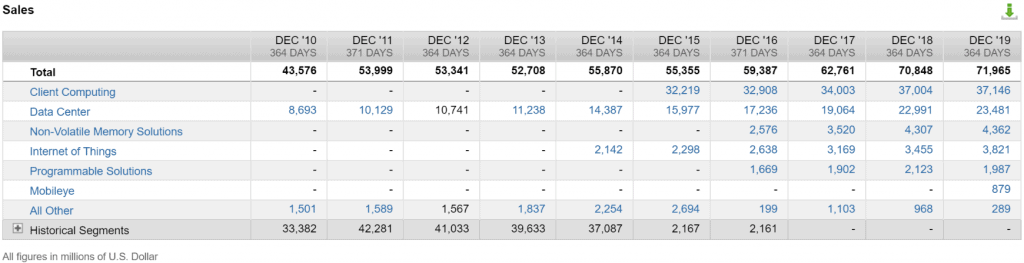

Intel divides its business areas into the six segments: “Data Center Group (DCG)”, “Internet of Things (IOTG)”, “Mobileye”, “Non-volatile Memory Solutions Group (NSG)”, “Programmable Solutions Group (PGS)” and “Client Computing Group (CCG)”.

The “Client Computing Group (CCG)” segment

By far, the largest segment with a 54 percent share of revenues is the CCG segment. This segment includes the PC processors that have made Intel widely known over the past decades. Intel sells CPUs for desktops and notebooks. However, the growth of the last few years has been modest. For example, in the previous quarter, growth was only one percent because, from today’s perspective, Intel has mostly lost its technology lead over its eternal competitor AMD. We will go into this separately later.

The “Data Center Group (DCG)” segment

In the DCG segment, Intel designs and produces chip solutions for computing, storage, and networking functions that are sold to cloud service providers, enterprises, government agencies, or communications service providers. The segment accounts for 32 percent of total sales. After average double-digit growth in recent years, the segment’s growth in 2019 was relatively meager at two percent. In the last quarter, however, revenue picked up again by 7 percent.

The small segments “IOTG”, “Mobileye”, “NSG” and “PGS

The four segments “IOTG“, “Mobileye“, “NSG“, and “PGS” each account for only fractions of total revenues. The largest segment is the segment for storage solutions NSG, with 6 percent of total revenues.

The “Mobileye” segment is particularly exciting among those smaller segments. Here, Intel is addressing the mega-market of “autonomous driving”. The company gained a foot in this market in the USD 15.3 billion takeover of the Israeli company Mobileye. Intel’s market position is robust, thanks to Mobileye. At level 2 of autonomous driving, currently “state of the art”, 70 percent of all systems are based on Mobileye solutions. However, their share of Intel’s total revenue is still minor at just one percent. After strong growth from 2017 to 2019, the segment also grew by only weak 2 percent in the last quarter. Therefore, it will be some time before the segment becomes a viable pillar of business, especially as competition is very strong. Tesla, Nvidia, and more recently, Qualcomm are among the biggest rivals.

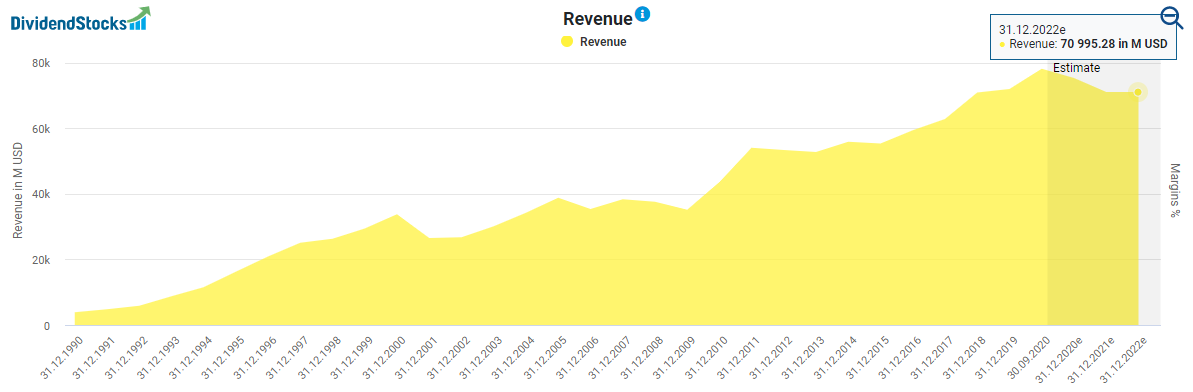

Intel, where has your growth gone?

The segment description already showed that Intel currently lacks a growth catalyst in its product portfolio. The consequence is declining sales for this fiscal year and probably also for the next fiscal year. Not until 2022 is revenue expected to increase slightly again.

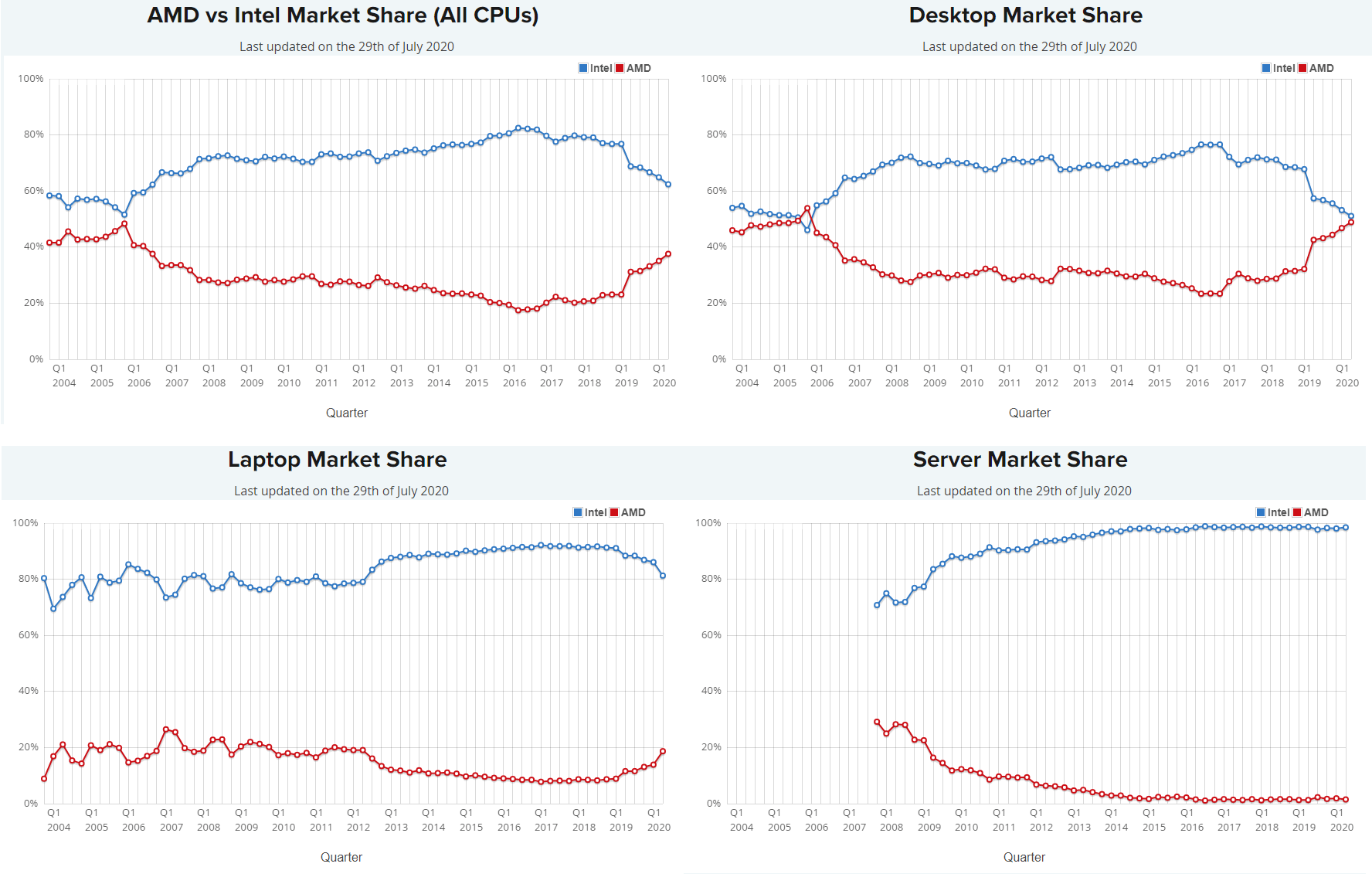

Intel produces most chips in its factories, which makes its success dependent on competitive manufacturing technologies in house. On the other hand, AMD uses the large contract manufacturers Samsung and Taiwan Semiconductor. Thus, AMD has access to the world’s only producers who already master the 7nm (nm=nanometer) production standard.

In contrast, Intel has significant problems with the introduction of 7nm production and has already had to postpone its market launch several times. Intel’s 10nm disaster of the past, which even led to a delayed market launch by several years, threatens to repeat itself. Intel’s first shipments of 10nm-based desktop CPUs are scheduled for the second half of 2021.

As a result of the manufacturing problems, margins in chip production are falling, and Intel is increasingly losing market share to its competitors. Hence, AMD has reduced Intel’s market share in three of four important sub-markets. Intel’s weak phase, which has lasted for quarters, increasingly gives the impression of a longer-term trend, which could lead to Intel losing its dominance in the CPU sector in the worst case.

Intel had to cope with another setback in the production of 5G modems for the cell phone market. The management had repeatedly announced 5G modems with big words without ever delivering a single product to a customer. In 2019 Intel had to admit its defeat to Qualcomm and withdrew from the future market.

In my opinion, Intel’s management has focused too much on maintaining the stock price in recent years by investing massive amounts of money in share buybacks. Since 2007, the number of outstanding shares has fallen from almost 6 billion to the current 4.2 billion. Although the share buybacks increased earnings and dividends per share in the short term, they would have been better off with research and development in the long term.

AMD shows that it can be done better. The number of outstanding shares of AMD has risen from 835 million to currently over 1.21 billion since 2016. Nevertheless, Intel’s competitor’s stock price also increased by more than 640 percent within the same period. Intel shows that supposedly shareholder-friendly management does not necessarily lead to a superior investment. Here you see, that operational problem cannot be concealed in the long run by share buybacks.

How profitable is Intel?

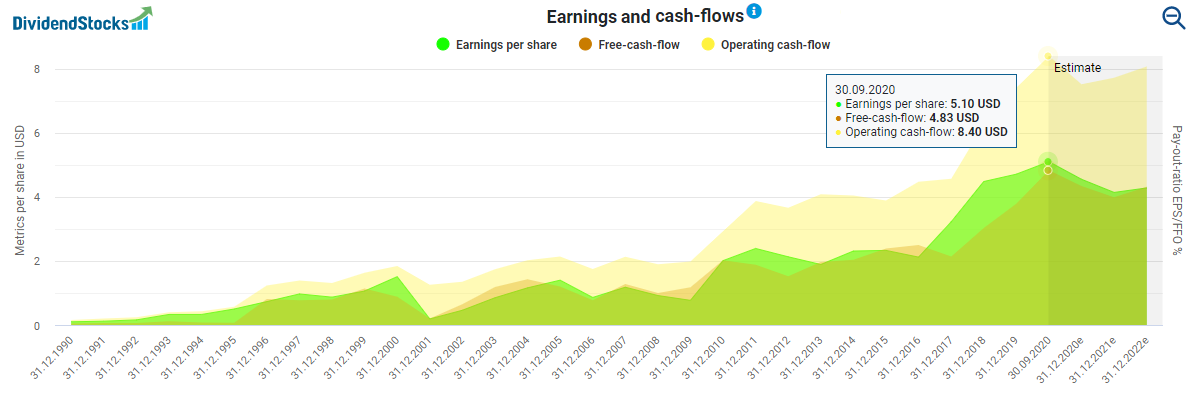

The current problems are impacting Intel’s earnings and cash flows. Like revenues, earnings, and cash flow will decline over the next few years. After that, however, they could slowly start to rise again from 2022 onwards based on analyst forecasts. However, it will probably take several years before the old highs are reached.

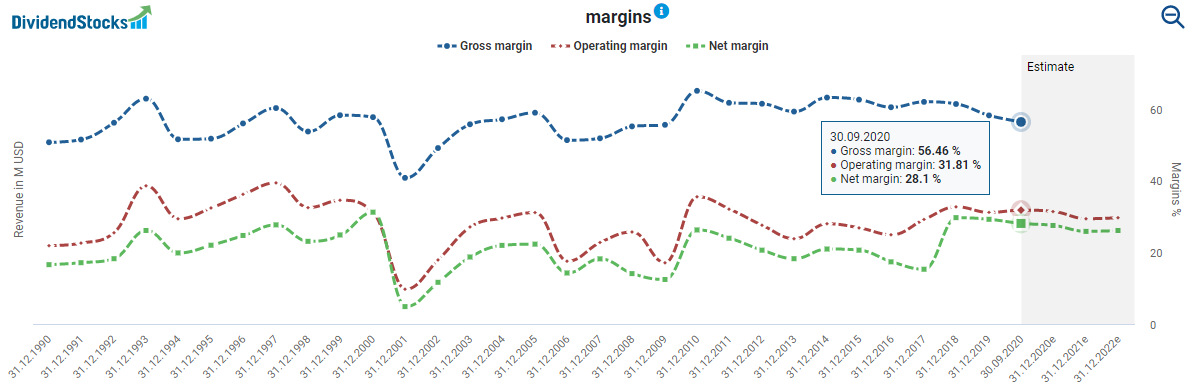

Margins also developed negatively. The gross margin fell from 62 percent in 2017 to currently 56 percent. The operating and net margins are also expected to fall by one to two percentage points in the next two years.

ARM might be a threat to Intel and AMD’s CPU business

Investors interested in Intel should continue to monitor the acquisition of ARM Limited by Nvidia. ARM is a British chip designer for which Nvidia is willing to pay USD 40 billion. If the antitrust authorities give their go, Nvidia’s existing products and ARM portfolio will create a new giant in the market. This giant will have a major position in the markets for AI, autonomous driving, and high-performance computing.

ARM develops CPUs based on the so-called RISC architecture. With this architecture, it competes with the x86 architecture on which the CPUs from Intel and AMD are based. ARM licenses the design to other companies such as Qualcomm, Samsung, or Apple for their new M1 chip. Especially in the mobile sector, you can find the power-saving ARM design almost everywhere. For Intel (and AMD), there is a threat that ARM design will push the x86 architecture used for desktop CPUs further back due to the convergence of mobile and stationary application areas.

How safe is the Intel dividend?

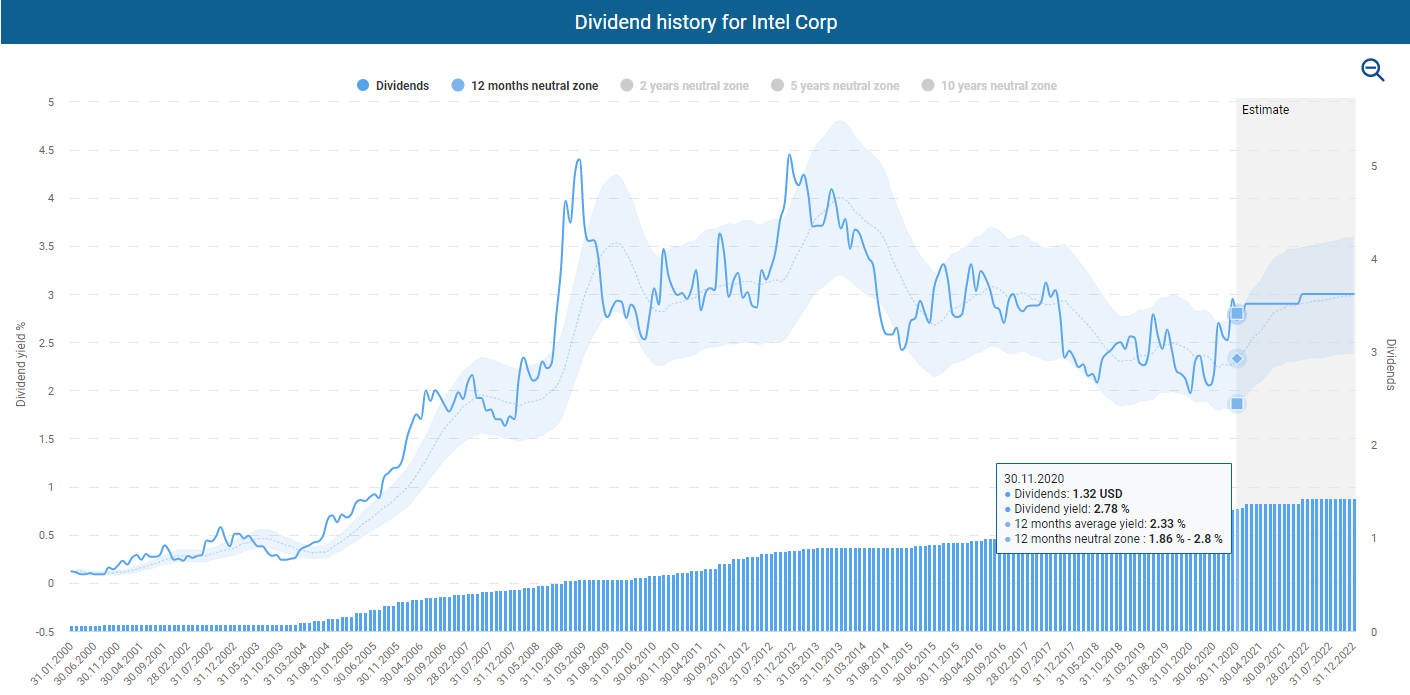

More pleasing than the operating business is the development of Intel’s dividend. Intel has increased its dividend every year for the last six years but has been paying its shareholders a dividend every quarter since 1992. Since 2000, Intel has increased its dividend from USD 0.06 to USD 0.33. In the last three years, the dividend has increased by 6.6 percent, and in the previous ten years, by an average of 8.45 percent. Following the recent increase from USD 0.315 to USD 0.33, shareholders receive USD 1.32 per year. At the current stock price of USD 45, this represents a dividend yield of 2.91 percent.

Due to the stock price losses in recent months, the dividend yield is approaching the upper end of the short-term corridor of one year and is on average over the last ten years period. A significantly higher dividend yield occurred only in the years 2009 and 2012 to 2013.

However, the low payout ratio of 32.9 percent based on free cash flow and 25.4 percent based on reported earnings leaves sufficient leeway for further dividend increases. Despite all current problems, Intel has by far the most attractive dividend profile compared to its competitors. In comparison, Qualcomm’s current dividend yield has melted to 1.74 percent due to recent price increases, while Nvidia’s current yield is only 0.13 percent. AMD, in turn, does not pay a dividend at all.

Is the Intel stock fairly valued?

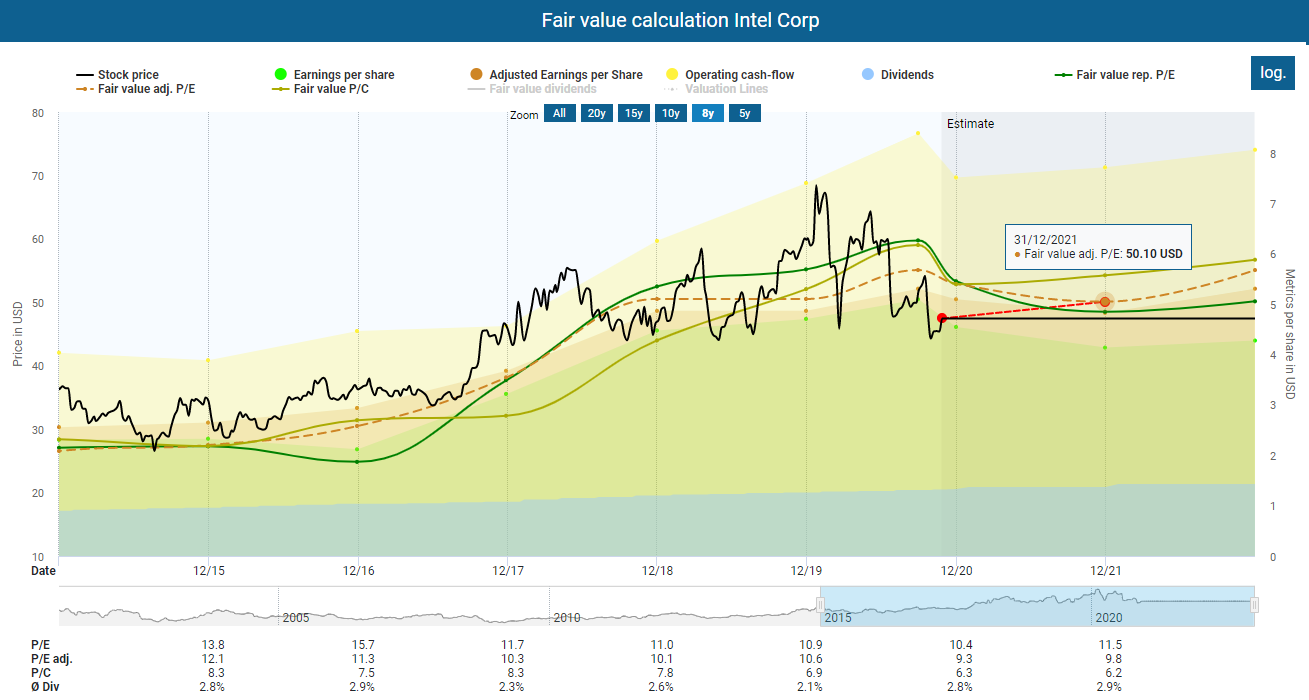

The stock price losses of recent months have pushed the Intel stock deep into undervaluation. In purely arithmetical terms, based on fair adjusted earnings, this results in an upside potential of 17.1 percent up to the end of 2021. A similar upside potential results if we look at the projected earnings development in the following year 2022. The stock is a significant 31.6 percent off of its fair value.

Despite all the problems, I am surprised that the market is trading the Intel stock with a single-digit adjusted P/E ratio. The price-cash flow ratio of less than six also points to a significant undervaluation. In comparison, AMD’s price-cash flow ratio is more than ten times higher. Intel’s current poor performance seems to be exaggerated by the market in my opinion.

Conversely, however, there is little to suggest that the operating business will improve quickly. Intel will probably continue to lag behind AMD’s successes in the coming years and will probably continue to lose market share. However, when you look at Intel’s sales and profit development, you can see that the operational business is dependent on the success of individual chip generations. Phases of growth alternate with years of stagnation. Currently, AMD is the clear leader in the CPU market. However, in the mid-2000s the Primus itself was already deeply in the red, which shows that no market share holds for eternity. In my AMD analysis, I wrote:

Poor management that makes the wrong decisions usually leads to worse distortions in the highly competitive technology sector than in other more conservative industries. But this doesn’t just affect AMD, it affects the entire industry and is a risk you have to bear with all investments in this industry. Personally, however, I think the current valuation is too high given such a risk.

The example of Intel shows how lousy management has an impact in the chip industry. Long-term oriented investors, however, may see an opportunity in this situation. Already in the next cycle or the cycle after, Intel can be among the winners again. Until then, high and further increasing dividends will compensate for the weak stock price development, while the already low valuation will ensure a limited downside risk.

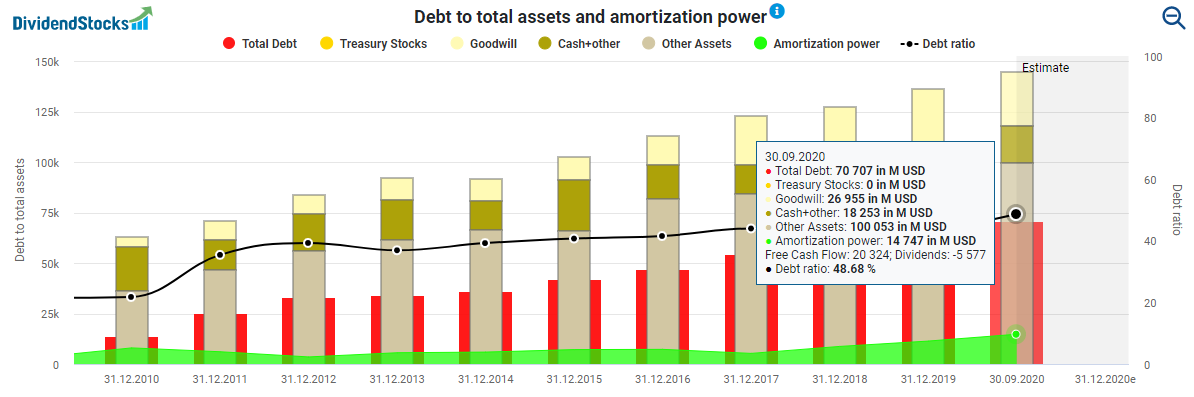

Aglance at the balance sheet also shows that Intel’s situation is not threatening its existence. USD 70.7 billion of debt is offset by significantly higher assets, resulting in a moderate debt ratio of only 48 percent, which is only slightly higher than AMD’s debt ratio of 44.2 percent (which is decreasing from quarter to quarter) and significantly lower than Qualcomm’s debt ratio of 82 percent. Only Nvidia has an even stronger balance sheet with a debt ratio of 30 percent.

Conclusion: Intel stock – battered, but far from knocked out

There is a reason for the decline in the Intel stock price. Severe disappointments in the 5G and 7nm production seem like the tip of an iceberg of current problems, leading to a weakness in competitiveness and consequently to a slowdown in growth. Fierce competition with Nvidia and the ARM portfolio also weigh on the future business. And yet, long-term investors continue to see Intel as a tech giant that may be staggering but still stands on strong feet. Should he regain his old form, Intel’s current price will be a bargain in retrospect.

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts. You can also share this post with your favorite network: