If you’ve owned Qualcomm stocks in the past, the last few years must have felt like watching a soap. The chaos of disputes, settlements, failed takeovers, regulatory investigations, and the speed at which all these events coincided may have left some investors with a question mark. In the meantime, some peace has returned after the eventful years. With this fundamental Qualcomm stock analysis, I want to take a closer look at Qualcomm and see whether the ups and downs of recent years do have a happy ending and whether buying Qualcomm stocks is a good idea.

As always, I would appreciate it if you could give me short feedback in the comments below or share this post if you liked it or had the opportunity to pick up some valuable thoughts.

Qualcomm stock: A roller coaster

To give you a better understanding of this analysis, I will briefly summarize the most important developments and events since 2015, as some of them have a considerable impact on Qualcomm’s business and its valuation.

Failed takeovers on several fronts

A highlight of the eventful last few years were the various takeover attempts. While Qualcomm wanted to buy the Dutch company NXP Semiconductors for 44 billion USD, it was itself the subject of aggressive takeover efforts by Broadcom at the same time. Broadcom even offered $117 billion to buy Qualcomm, although, at that time, no one knew whether the Qualcomm-NXP deal would get clearance by authorities. In the end, both takeovers failed due to regulatory hurdles in China and the USA.

Dispute and settlement with Apple

Besides, Qualcomm had a long-running dispute with Apple that both companies took to court around the world. It was all the more surprising when, as part of a major settlement package last year, both parties agreed to a one-time payment of USD 4 billion from Apple to Qualcomm. Furthermore, Qualcomm and Apple waived all legal disputes and entered into far-reaching cooperation agreements.

Qualcomm and the competition authorities

There is also a never-ending dispute between Qualcomm and various competition authorities. Qualcomm is alleged to have abused its market power in several cases to force other competitors out of the market or to gain an unfair advantage. China, South Korea, and the European Union have each imposed fines of around USD 1 billion on the company.

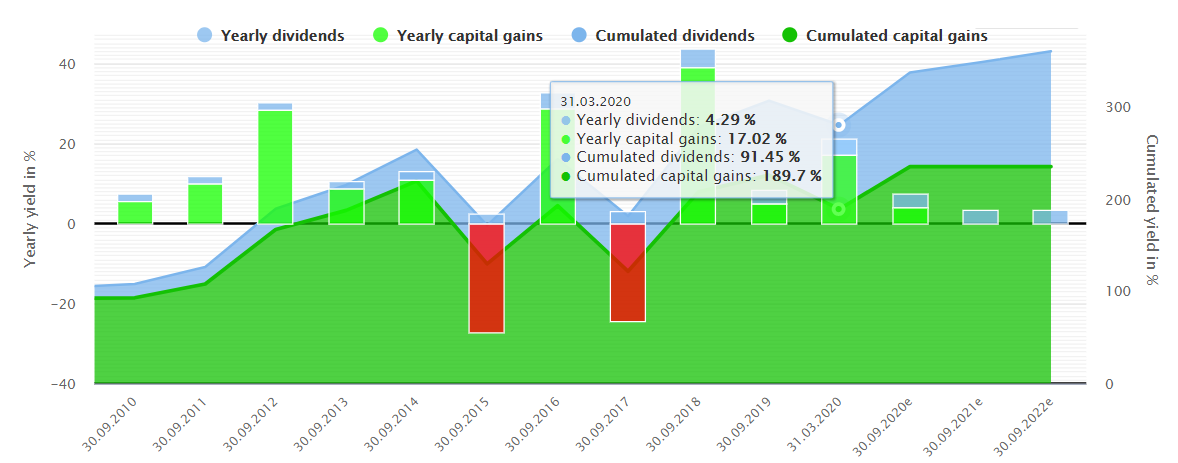

Price gains despite volatility

Although Qualcomm’s stock price fluctuated sharply as a result of the events stated above, long-term investors can look back on a successful period. For example, there were only two years with price losses of over 20 percent in the last ten years. In the remaining years, the share has steadily gained in value. Currently, the cumulative capital gains amount to a whopping 190 percent.

Business Analysis

Qualcomm is a leader in the semiconductor industry with a particularly strong position in the wireless processor market. The business consists of two larger units and one smaller unit.

QTC Segment (Qualcomm CDMA Technologies)

Until now, you could find Qualcomm’s hardware in almost every smartphone, tablet, and many laptops. The business will continue to expand massively in the future. This is due to the introduction of the new 5G wireless standard. As you know, the launch of the new standard brings far-reaching changes as it enables high-speed and accurate data transfer, opening up entirely new areas of application for data transmission. As a result, mega-markets such as the Internet of Things (IoT) or the related autonomous driving are becoming more and more a reality.

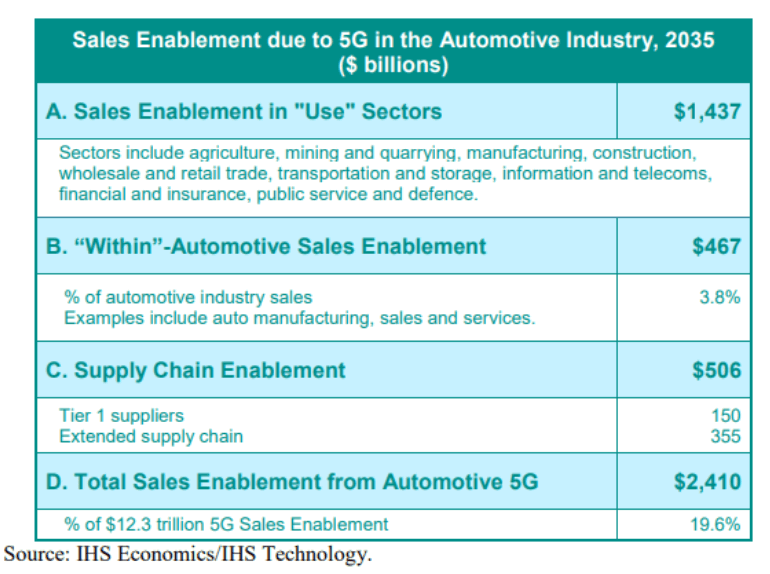

The future prospects are indeed rosy. After a ramp-up phase, the global market value of 5G is expected to reach a total of USD 12.3 trillion in the mid-1930s. USD 2.4 trillion of this is to be accounted for by the automotive sector:

In the automotive sector, a mega-market based on 5G is thus emerging with excellent growth prospects. Qualcomm is targeting both markets, 5G, and automotive. It is not without reason that the company had its eye on NXP Semiconductors and its strong market position in the automotive sector.

When the NXP deal failed, Qualcomm quickly developed its Snapdragon Ride and Automotive Cockpit platforms into complete solutions that included both hardware and cloud-based software applications. With these platforms, the company intends to offer both hardware and software to transfer and process data generated by traffic. Besides, the new offerings will enable in-car entertainment and include solutions for autonomous driving. With this move, Qualcomm is abandoning its traditional business and focusing even more on providing complete solutions to customers.

At least for the mobile sector (smartphones, tablets, laptops, etc.), you can expect that Qualcomm will have a similarly strong market position as before in 3G and 4G after Intel’s withdrawal. For example, Intel, one of the fiercest competitors, threw in the towel for the 5G mobile market very early on and admitted Qualcomm’s lead. The constitutional settlement with Apple also shows that even the proud company from Cupertino is dependent on Qualcomm because immediately after Intel’s withdrawal, Apple settled the dispute with Qualcomm and paid over 4 billion USD cash (see above). Only when Apple develops its 5G chips could Qualcomm’s supremacy theoretically crumble. So far, however, Qualcomm has always managed to maintain its lead in mobile communications standards.

If Qualcomm is as triumphant in the 5G automotive market as it is in the mobile phone sector, it is in for a golden age.

QTL Segment (Qualcomm Technology Licensing)

The QTL segment primarily includes Qualcomm’s licensing business. The business of licensing the patents held by Qualcomm to third parties is highly profitable. With an operating margin of 80 percent in 2017, 68 percent in 2018, and 64 percent in 2019, it is a significant contributor to the company’s profits. However, it generates less than one-third of total revenue.

QSI Segment (Qualcomm Strategic Initiatives)

Thirdly, there is the QSI segment, which Qualcomm uses as an investment vehicle. Qualcomm has launched several funds in this segment to invest in start-ups operating in promising markets. However, with sales of only USD 150 million in 2019, the segment is not very significant.

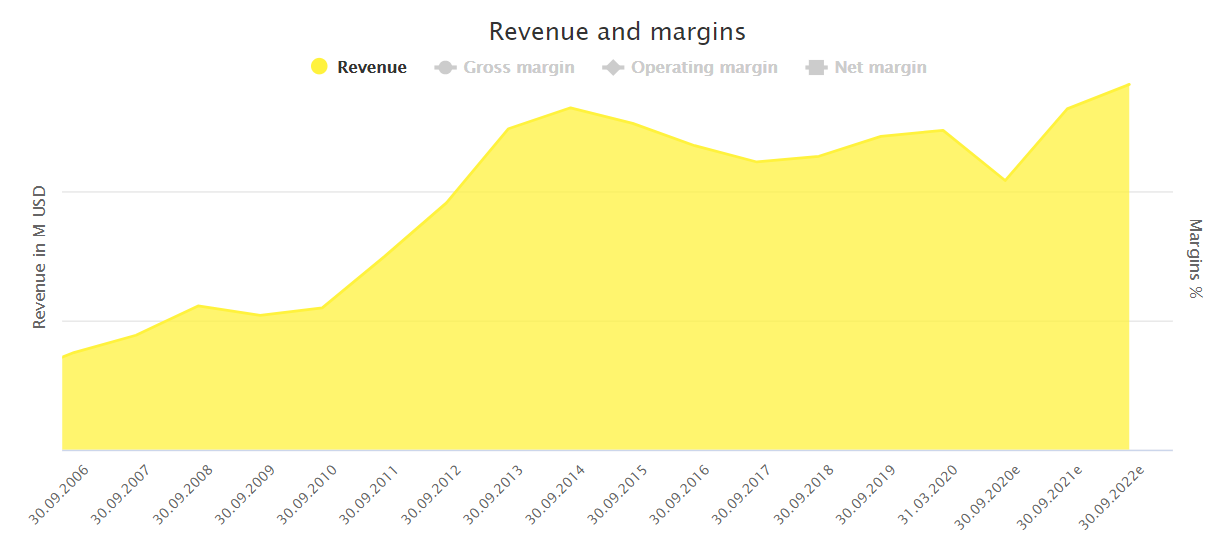

Does Qualcomm grow?

Revenue has stagnated in recent years and has even declined slightly. However, with the introduction of 5G and the expanded applications of this new technology, Qualcomm should be able to leverage its strong market position and generate further growth. In this respect, the forecast of the Dividend Screener also predicts rising revenues starting next year.

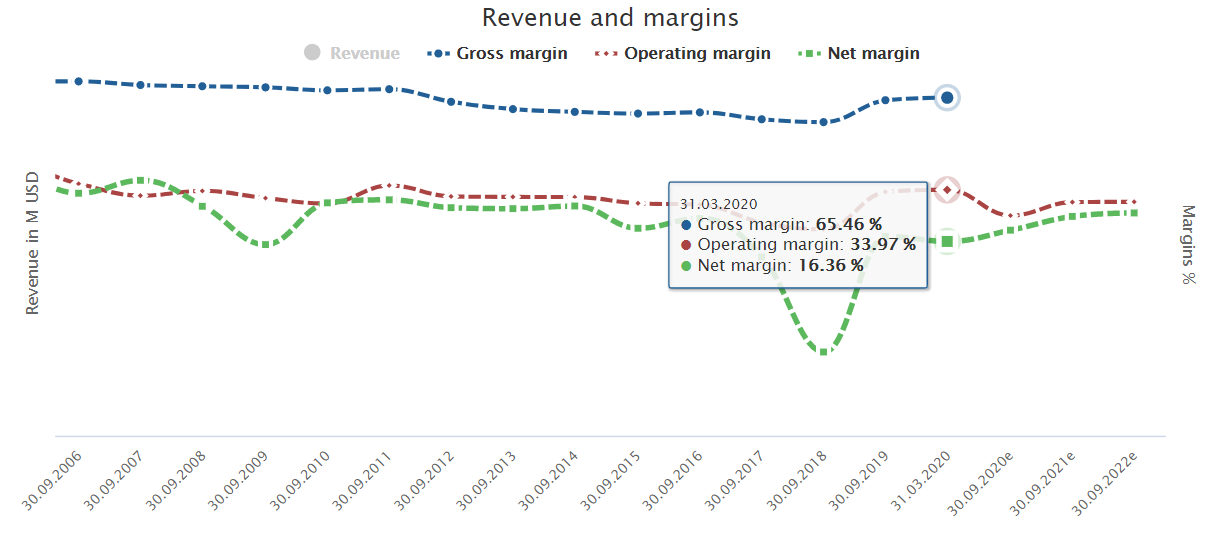

Fundamental Stock Analysis – Is Qualcomm Still profitable?

However, another question is whether Qualcomm can maintain its profitability, which is strongly based on the licensing business. As you can see, margins have been fairly stable in recent years. The brief slump in net margin was due to the disputes mentioned above over the licensing business and fines the company had to pay for competition law violations.

I could imagine that profitability will decline somewhat in the future. As you saw above, the operating margin in the QTL segment is already declining. That’s partly because Qualcomm has to be very careful not to over license. The room for maneuver that Qualcomm has been using as much as possible for a long time has probably been reduced. Competition authorities around the world are keeping an eye on the company, and competitors such as Intel continue to attack Qualcomm’s monopoly, accusing it of unfair business practices.

Fundamental Dividend Analysis for Qualcomm

Overall, Qualcomm has increased its dividend for 16 years. This makes the share attractive to dividend investors. However, the company does not belong to the noble circle of dividend aristocrats. A company is not considered a true aristocrat until it has increased its dividend every year for 25 years without interruption.

As you can see in the Dividend Screener, Qualcomm has recently delivered a fairly high dividend yield. With a current return of more than 3 percent, Qualcomm stock is actually above the 10-year average. But there have been better opportunities to get in on the stock, which could have brought you a return of almost 5 percent. This is especially true for the last five years when Qualcomm was exposed to numerous conflicts, and the share price fluctuated.

As I showed you in the last Microsoft analysis, the initial return is not the decisive criterion in the long run. What is more important are the annual increases and the compound interest effects. Qualcomm’s historical increases are indeed in an attractive range, with average dividend growth of nearly 14 percent over the last ten years, 9 percent in the previous five years, and 6.2 percent in the previous 3 years. However, the average increases have recently continued to decline. In fact, the latest increase was only 5 percent. The reason for this is probably the payout ratio on earnings of over 73 percent, which limits the scope for further increases.

The further decline in profit will also limit the leeway for higher payouts in the short-term as the payout ratio will rise to almost 100 percent. This is even a warning sign that the dividend is not sustainable and that the company could make a cut. However, an improvement is in sight in the coming years, so I do not see the dividend as a whole in danger.

Is Qualcomm overvalued?

If we only look at profit and cash flow, the company seems to be slightly undervalued based on the current figures as of March 31, 2020. However, something different results if we use the adjusted fair value (non-GAAP [adjusted earnings] compared to GAAP [reported earnings]). This method excludes items such as the U.S. tax reform and can give you a more realistic picture of the fair value of a company.

But you have to keep in mind that Qualcomm’s business performance in recent years has been particularly affected by the side disputes that have slowed profit growth. As you can see here, the market has traded Qualcomm below its fair value since 2015. Now that many uncertainties have disappeared, the market seems to value Qualcomm a little higher again.

I agree with this view, as revenue and profit should pick up again in the future, thus justifying a premium on the current P/E ratio. The adjusted P/E ratio is currently 16, which is too low for a company with excellent prospects, a monopoly in the 5G market for smartphones and tablets, and a promising strategic focus on other mega-markets such as the automotive sector.

Overall, it is fair to say that Qualcomm is no longer the cheap company it used to be. However, with a current adjusted P/E ratio of 16, it is also not overpriced and, therefore, still interesting for long-term investors from a fundamental valuation perspective.

Fundamental Qualcomm stock analysis – Conclusion

Qualcomm stock has gone through turbulent times. Now, however, calm has returned, and the company can fully concentrate on the strategic direction. If Qualcomm manages to transfer even a portion of its existing monopoly position to other markets created by the introduction of 5G, investors can look forward to golden times. In addition to the traditional wireless market, management has focused on the promising automotive sector and the IoT sector and has introduced the first products and services for these markets.

The market has already rewarded these prospects. Besides, the removal of the most significant uncertainties and has lifted the share price above fair value. Nevertheless, with an adjusted P/E ratio of 16, Qualcomm is not overpriced. For long-term investors, the stock remains a valuable opportunity to benefit from future mega markets. The dividend yield of over 3 percent and the prospect of at least minor increases in the future make the investment complete.

–> Click here for more analysis <–

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.