With reliable dividends in the mid to high single-digit percentage range, the Royal Dutch Shell stock was a no-brainer for dividend seekers for a long time. However, the dividend has now been reduced to one third. Shell is facing the biggest challenges of the last decades with the world´s shift towards renewable energies. Many shareholders have lost faith in Royal Dutch Shell and have sent the stock price southward by more than 50 percent year to date.

But perhaps the time has come for shareholders with guts to buy Royal Dutch Shell stocks at a decent discount. In this analysis, we clarify whether the remaining dividend is safe and whether the stock is undervalued after the price drop.

The business model: How Royal Dutch Shell (still?) makes money

Royal Dutch Shell divides its activities into three business areas: Integrated Gas, Upstream and Downstream.

A characteristic of the company is the vertical integration along the complete value chain of oil and gas. In the so-called downstream, Royal Dutch Shell searches for and produces the energy sources. Midstream is where they are transported and stored. At the end of the value chain is the so-called downstream, where the raw materials are refined and then sold.

The „Integrated Gas“ segment

The “Integrated Gas” segment deals with liquid gas and natural gas conversion into marketable products, such as fuels. Shell explores and produces natural gas and liquid gases and maintains the complete infrastructure to sell the final and intermediate products on the market. Royal Dutch Shell trades in natural gas, liquid gas, electricity, and carbon dioxide emission rights.

New energies are also included in this segment. Here, Royal Dutch Shell is researching renewable energy sources. The company invests in organic growth and acquisitions intending to shape the energy transition actively. However, the “Integrated Gas” segment accounted for only 12 percent of total sales in 2019. The low share of renewable energy in the group’s turnover shows that Royal Dutch Shell is still dependent on traditional energy sources. A dependence of which Royal Dutch Shell must break free to survive in the long term:

We know the energy transition is unfolding, and we must be part of it if we are to survive…

Ben van Beurden – Chief Executive Officer (Source: Annual report 2019, p. 19)

The „Upstream“ segment

In the “Upstream” segment, Royal Dutch Shell explores, produces, and markets oil, natural gas, and natural gas liquids. The company constructs and operates the infrastructure for transporting oil and gas. Shell is also involved in processing mined oil sands into asphalt (bitumen) and its conversion into crude oil. At 2.9 percent, the “Upstream” segment is the smallest in terms of sales.

The „Downstream“ segment

The “Downstream” segment includes Royal Dutch Shell’s activities with oil products and chemicals and was responsible for 85 percent of sales in 2019. This is where the company produces and sells so-called petrochemicals for industrial use. It also markets fuel oil, aviation fuels, marine fuels, biofuels, lubricants, bitumen, and sulfur.

Challenges of the next 100 years

The oil price, which has been falling for years, has had a significantly negative impact on Royal Dutch Shell as an oil-producing company since production costs remain the same on the one hand. Still, revenues from oil sales are falling on the other. However, it is advantageous for Royal Dutch Shell that the demand for fossil fuels will continue to rise for the time being – apart from special effects such as the collapse in demand due to the Corona crisis.

The demand for oil in 2019, for example, increased by as much as 1 percent. The global gas market even rose by 2.5 percent. However, the problem is that the rising demand did not increase oil and gas prices in the end. The reason for the drop in prices was overcapacity due to the booming fracking industry in the USA. Besides, the end of the rising demand is foreseeable. Even Royal Dutch Shell assumes that oil and gas will lose importance as an energy source in the long term.

Although lower raw material prices will lead to higher margins in the processing of oil and gas into other products, this will not be enough for Royal Dutch Shell to compensate for the lower revenues from the downstream business, as Royal Dutch Shell only generates 2.9 percent of its total revenues in this area. Also, Shell has to struggle with dwindling oil reserves.

The deposits of Royal Dutch Shell secure production for only 8 years. Accordingly, the pressure and associated costs to develop new oil deposits are correspondingly high in the near future, which will further increase the debt burden. Indeed, the slightly increased demand for oil and gas should give some planning security for the coming years. But I do not believe that the core business will ever blossom again.

Opportunities for the next 100 years

The long-term opportunities, therefore, lie elsewhere. Royal Dutch Shell plans to become a significant player in the electricity market. The management wants to generate electricity and be climate-neutral by 2050 and offer solutions for charging electric vehicles and trading electricity. Royal Dutch Shell is also investing in renewable energy sources such as biofuels and hydrogen. The company assumes that renewable energy consumption will increase massively in the coming decades and significantly exceed all fossil fuels’ total consumption by the end of the century.

Royal Dutch Shell invests between 1 and 2 billion USD annually in renewable energy, which is the only opportunity for a successful future. We have to see and wait that the management will position itself in this market as successfully as in the oil and gas business. After all, last year, Royal Dutch Shell overtook its competitor Total in its transformation to a producer of renewable energies. However, it will be some time before Royal Dutch Shell achieves significant revenues from renewable energies.

Shrinking revenues at Royal Dutch Shell

The falling oil price has left its mark on revenue development. Despite the acquisition of competitor BG Group in 2015 for EUR 64 billion, revenues fell from USD 476 billion in 2012 to an estimated USD 231 billion in 2020. Although revenues are expected to pick up again in the next few years, it is uncertain whether Royal Dutch Shell will reach the record revenues of 2010 to 2013 in the foreseeable future.

How profitable is Royal Dutch Shell?

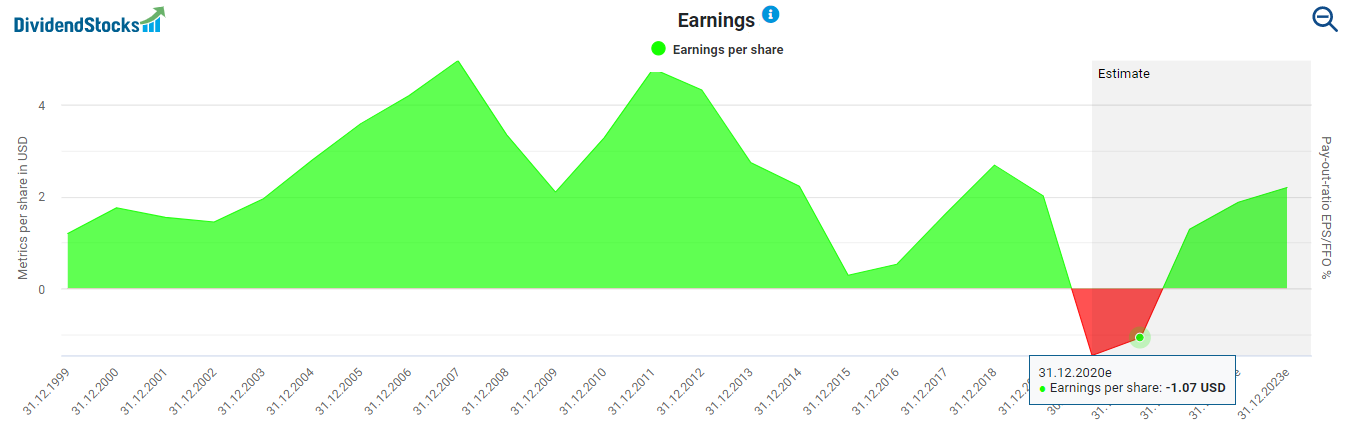

The low price of oil is nibbling at profitability. In the second quarter of 2020, Royal Dutch Shell, for example, had to make a sharp write-down due to the sharp drop in prices and the collapse in demand as a result of the Corona crisis, which ultimately resulted in a loss of USD 18.1 billion (EUR 15.4 billion) for the company. Even adjusted for this exceptional event, net income collapsed to USD 638 million. However, the company paid USD 1.2 billion in dividends in the same quarter. While you can see that profits have fluctuated in the past, the negative trend is evident and is now turning into a loss-making year.

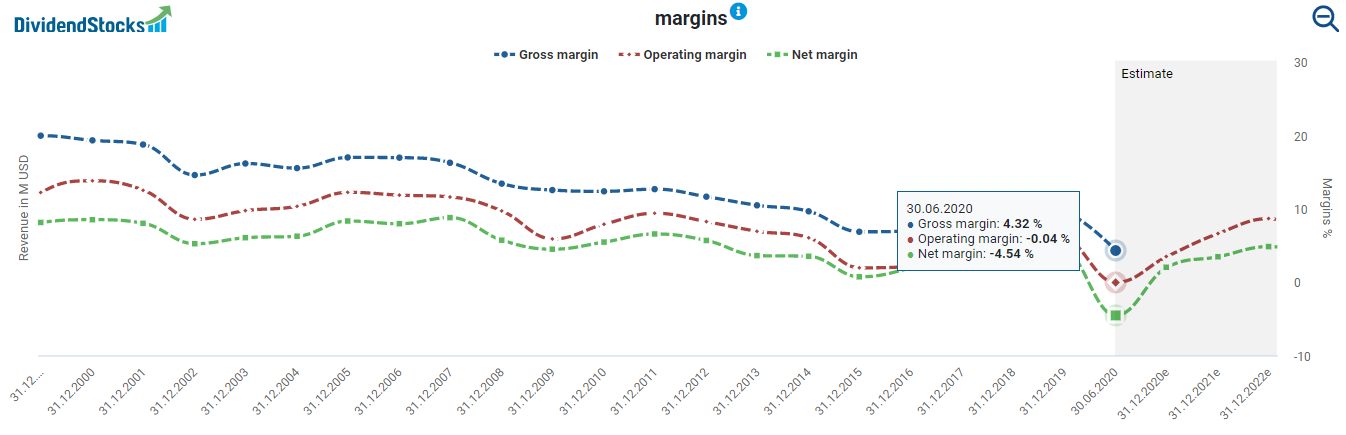

In parallel with profits, margins have also fallen sharply in recent years. In the Corona crisis, the gross margin fell from once 20 percent at the turn of the millennium to less than 5 percent today, while the operating margin is already slightly in the red.

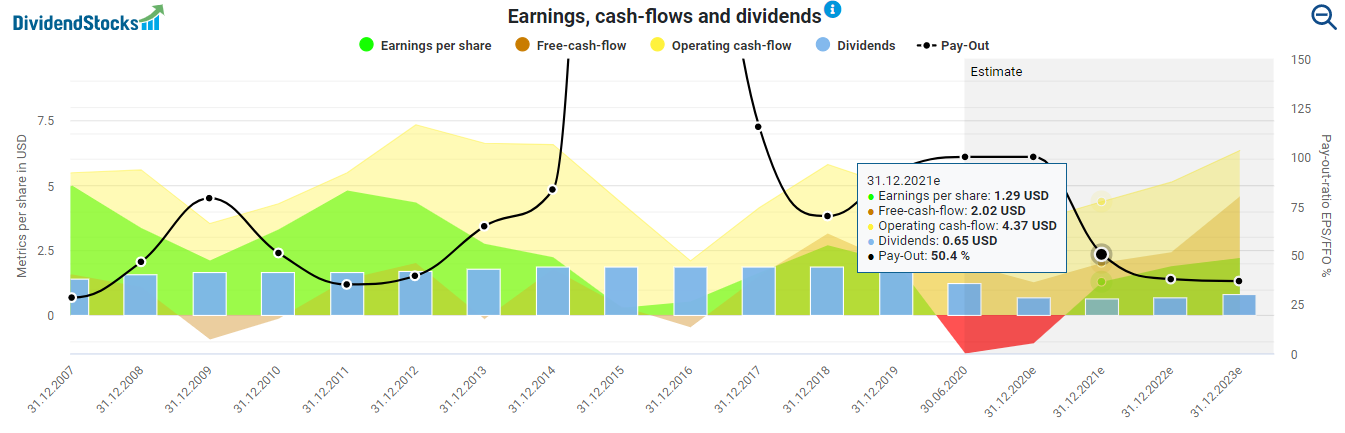

Is the Shell dividend safe after the cut?

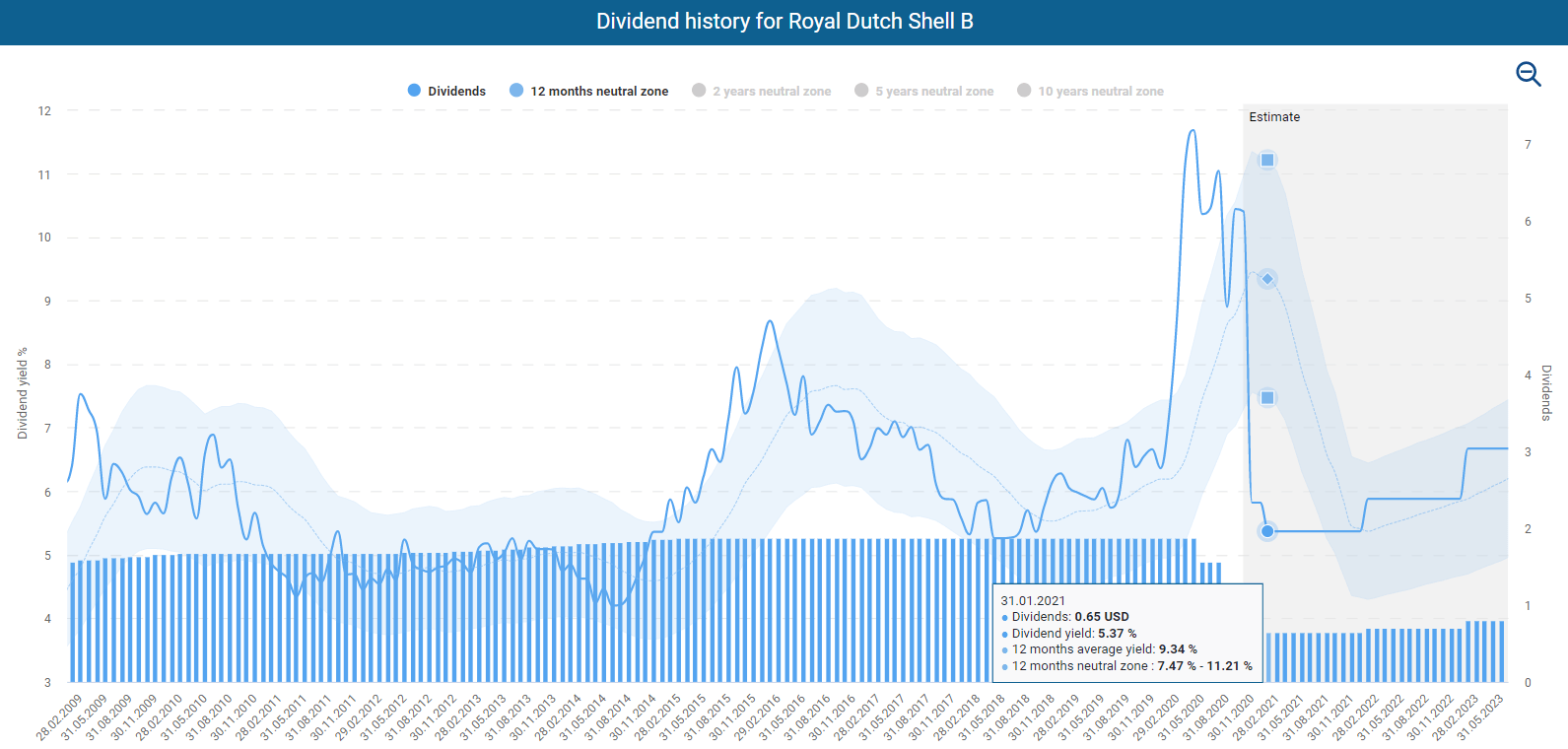

Shell pays dividends quarterly. In recent years, it has paid a dividend of USD 0.47 per quarter. However, with the recent dividend cut, Shell is paying only 0.16 USD now, which corresponds to a cut of 66 percent! Dividend growth stagnated with the financial crisis 2008/2009. Nevertheless, the Shell stock was still considered a solid dividend stock because there had been no dividend cuts since 1945. Accordingly, the dividend cut was unexpected by most investors.

The dividend history shows that the reduced dividend yield of 5.5 percent is below the historical average despite the lower share price. Therefore, I wouldn’t consider Royal Dutch Shell to be a dividend bargain:

It would be best to consider that earnings and free cash flow will probably not cover the dividend until the end of 2021. Whether Royal Dutch Shell will automatically increase the dividend to the previous level in the following years is questionable. Management may focus even more intensely on the transformation process in the future and prioritize debt reduction (see below).

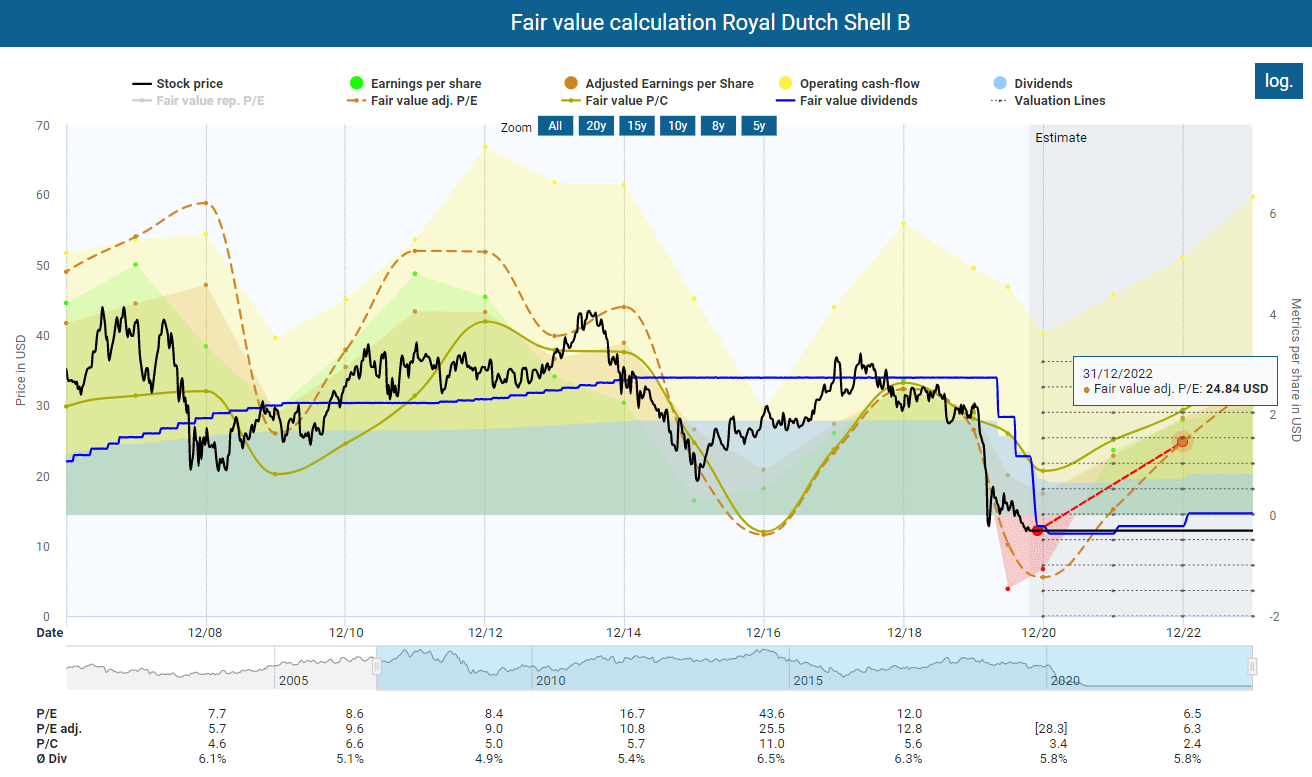

The fair value of Royal Dutch Shell

Despite the last price drop, the current multiples indicate a slight overvaluation. However, since the Corona crisis has had an exceptionally strong impact on the global economy and thus on demand for oil and the business of Royal Dutch Shell, these circumstances have a distorting effect on the current fair value. Based on the adjusted historical profits and assuming a normalization of business, the Shell share’s fair value should be close to USD 25 at the end of 2022. With a share price at an all-time low of USD 12.50, this would correspond to a price potential of 100 percent (see red dotted line)! However, if one takes the dividend into account when determining the fair value, the Shell share appears to be only fairly valued.

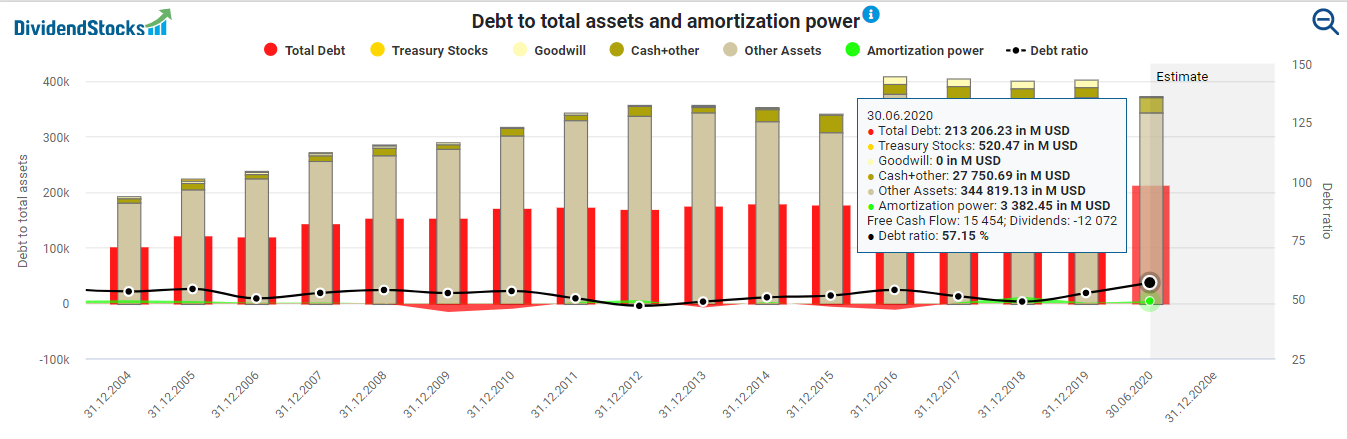

However, we cannot rule out that the markets will make a significant risk discount. The reduction in the dividend has destroyed a lot of confidence. As an additional burden in the near future, Royal Dutch Shell will face high investment costs for the development of new oil wells and the expansion of renewable energies. These burdens can also lead to a further discount. Although Royal Dutch Shell’s debt ratio of 57 percent is still in the green zone, the proportion of repayment power of USD 3.4 billion to debt of USD 213 billion is somewhat unfavorable.

Conclusion: The Royal Dutch Shell stock is a risky turn-around bet

For a long time, the Shell share was a reliable high yield dividend stock. With the recent dividend cut, the company has lost this nimbus. Besides, I do not expect to see an increase in the dividend in the next few years because management is struggling with the looming energy turnaround, dwindling oil reserves, and the currently low margins. There is still much to be done in the field of renewable energies. Whether the current dividend yield of just over 5 percent is appropriate given the risks is a question that each shareholder must answer for himself. For me, the Shell share is a risky turnaround candidate for investors with nerves of steel and a lot of patience.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.