Stryker has become a respectable yield generator in the medical technology sector. Anyone who invested in Stryker, founded in 1941, twenty years ago, can celebrate a cumulative total return of more than 850 percent, which corresponds to an average annual return of more than 12 percent. The performance goes hand in hand with a 40-year growth period. The question is how well Stryker has coped with the epidemic year 2020 and what growth can be expected in the future. This analysis will reveal the reasons for the long success story and whether Stryker is still a worthwhile investment.

The business model: How Stryker generates money

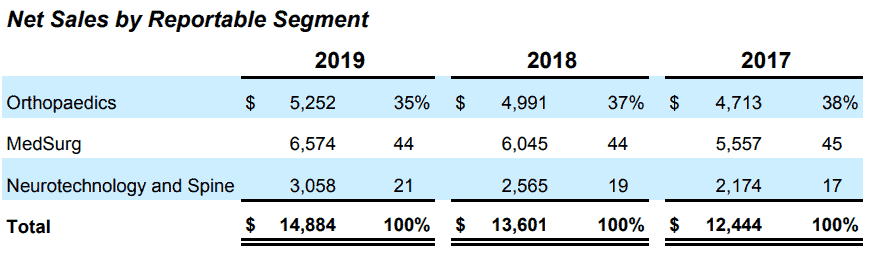

Stryker is active in the field of medical technology. In other words, it’s not about drugs or vaccines but prostheses, devices, and other “hardware” in the healthcare sector, as well as related services. Stryker earns its money with the three segments “Orthopaedics”, “MedSurg,” and “Neurotechnology and Spine”. The respective segments are subdivided into further divisions, which I will discuss separately below.

Orthopaedics

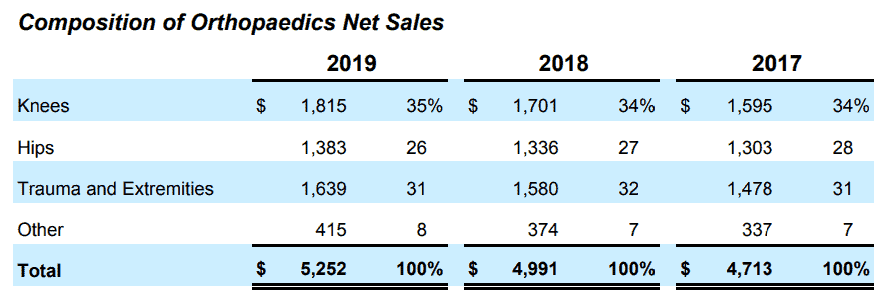

The Orthopaedics segment accounts for 35 percent of sales. It includes implants to replace knee and hip joints and devices and technologies for operations in trauma surgery and other surgical operations in extremities. One example is the Mako robotic arm, which enables a new surgical technique. The system uses previously prepared computer simulations to provide the surgeon with a precise plan and monitor the slightest deviation. Overall, revenues in this segment are evenly distributed among the three subgroups of knee, hip, trauma, and extremities.

MedSurg

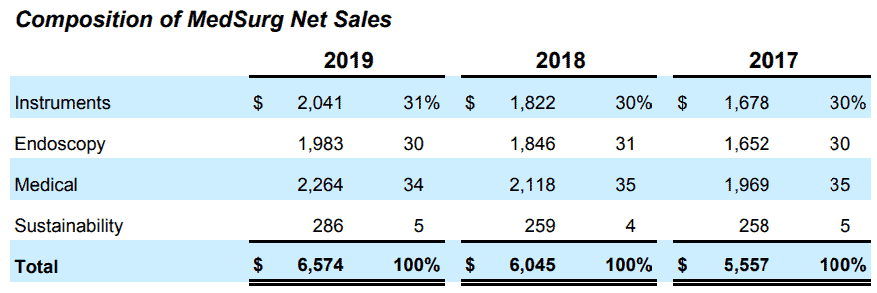

In the “MedSurg” segment, Stryker bundles various products into further sub-segments. For example, surgical equipment and navigation systems fall under the sub-segment “Instruments”, endoscopy and communication systems under “Endoscopy”, patient handling, emergency medical equipment, and disposable critical care products under “Medical” and remanufactured medical equipment under “Sustainability”.

MedSurg is the largest segment, accounting for 44 percent of total sales. The product range is versatile. In addition to disinfection solutions, bed frames, and transport solutions, Stryker offers illuminated instruments, suction instruments, protective clothing, waste disposal utensils, and much more. I recommend the excellent and illustrated presentation on Stryker’s website (here).

Neurotechnology and Spine

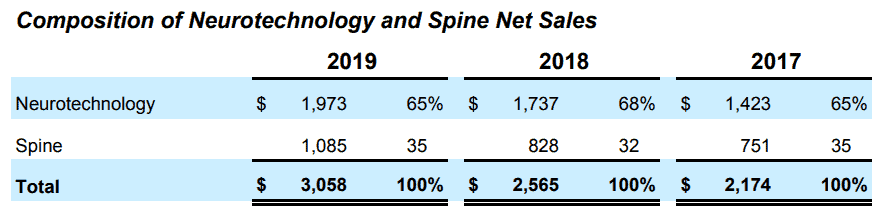

In the “Neurotechnology and Spine” segment, Stryker bundles neurosurgical, neurovascular (i.e., affecting the nerves and blood vessels) products, and spinal implants. It is in all areas one of the five largest producers. Within this segment, Stryker generates the majority of its revenues in the “Neurotechnology” segment. The product range includes products for minimum invasive and traditional surgical procedures. The implants manufactured by Stryker are used for spinal injuries, deformities, and degenerative diseases.

Stryker’s revenue development: Will the 40-year winning streak last?

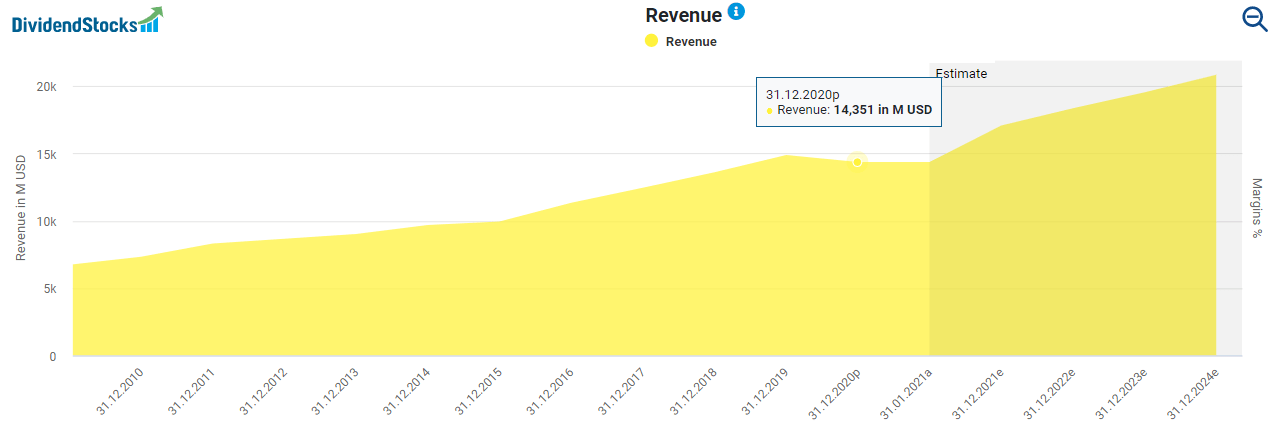

As you can see from the segment description above, all segments and sub-segments contribute to Stryker’s growth and, therefore, to its past stock price gains. Through 2019, the company has enjoyed 40 consecutive years of revenue growth. Unfortunately, this impressive streak came to an end in the epidemic year of 2020. As a result, revenue dropped from USD 14.8 billion in 2019 to USD 14.4 billion in 2020.

Like other companies in the healthcare sector, Stryker suffered from governments’ measures to slow the spread of the coronavirus. These had the effect of postponing surgeries and other non-essential procedures, reducing demand for Stryker’s products. However, management announced in January 2021 that it plans to return to 8-10 percent growth this year compared to 2019. Whether that forecast is too optimistic remains to be seen. The vaccination campaign against Corona, which has been launched worldwide, gives hope that a return to normality is not too far off.

Don’t overestimate the revenue drop

I do not want to overestimate the slight drop in revenue. What is decisive is the long-term outlook, and here the signs for Stryker are still pointing to growth. By 2024, revenues are expected to rise to an impressive USD 20.8 billion, which corresponds to an increase of more than 44 percent from 2020. Stryker is benefiting, in particular, from an increasingly aging population. The aging of the people and the daily office routine are causing severe wear and tear on the joints. The associated loss of life quality makes surgery seem inevitable in many cases (but sometimes too hastily).

However, Stryker’s profit growth is not purely organic

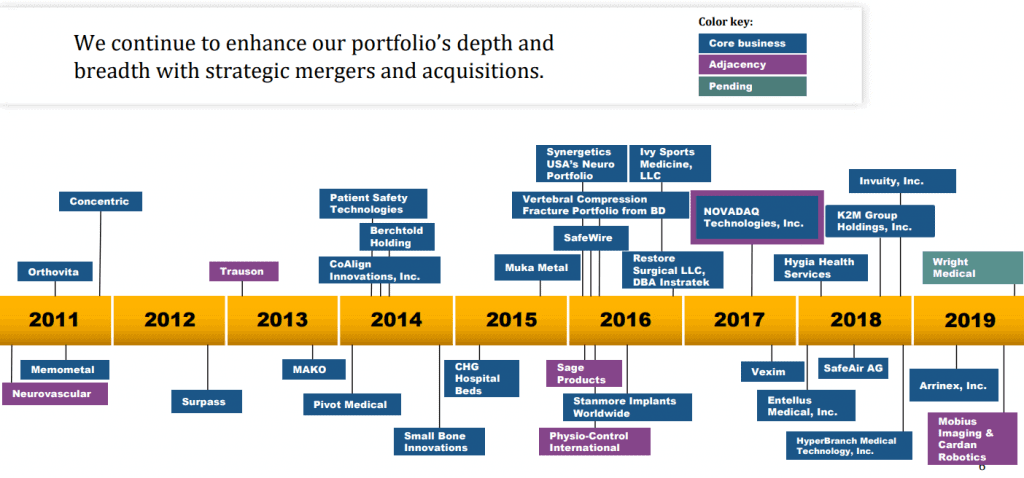

But beware – Stryker’s profit growth is not purely organic. A significant part of this has been the more than 30 acquisitions since 2011. Most recently, Stryker acquired Wright Medical for $5.4 billion, including all debt, with which Stryker intends to strengthen its business in the extremities area and the company OrthoSensor for an undisclosed amount.

From my perspective, it is okay to generate external growth through acquisitions as long as the companies are well integrated and contribute to profitable growth. Although this has worked well for Stryker in the past, future acquisition failures cannot be ruled out. The increased risk of a write-off in the case of acquisitions is the downside of such a strategy. The goodwill accumulated over the years shows the potential dangers here.

Another disadvantage is the risk of high debt. Stryker’s debt ratio of just under 62 percent is still acceptable, but it is at the limit for my taste. In the chart below, you can see how the acquisitions have caused the debt mountain to rise.

How profitable is Stryker?

The chart below shows that the development of profit is not as straightforward as that of revenues. Here, special items and write-offs of the acquired companies have an impact. However, the long-term development is also decisive for profit, and here, the direction looks good. While earnings per share were USD 3.19 in 2010, they are expected to rise to USD 10.85 per share over the next few years. Operating cash flow also follows this long-term trend and is expected to rise from the most recent USD 8.62 to USD 12.60 per share in 2020. For a mainly manufacturing business, such high cash flow is a sign of strength.

A look at the net margin shows that Stryker’s profitability also fluctuates due to special items. Besides, the continuous decline in gross margin and operating margin throughout the last few years fundamentally suggests that the business’s profitability is on the decline. Such developments may harm the future profit trend and the ability to increase dividends continuously in the long term. However, analysts expect the operating margin to rise again in the next few years.

Is the Stryker dividend safe?

Stryker pays quarterly dividends and has increased them every year for the past 11 years. After the most recent quarterly dividend increase from USD 0.57 to USD 0.63, shareholders will receive USD 2.52 per share annually, which translates to a dividend yield of 1.08 percent at the current stock price of around USD 240.

High dividend increases in the past

Over the last ten years, Stryker has increased its dividend by a decent 14 percent annually. If we look only at the previous five years, the annual average growth was a respectable 10.5 percent. The last increase in December 2020 was even higher than the 5-year average at 12 percent. Such rates of increase have a considerable compound interest effect, which becomes apparent when looking at the so-called “yield on cost,” i.e., the dividend yield in relation to the personal cost price.

Anyone who bought Stryker stocks ten years ago, for example, is having a dividend yield of 4 percent today. And with a payout ratio of 53 percent based on earnings and 31 percent based on free cash flow, there is also room for further dividend increases. Analysts expect the annual dividend to increase to USD 2.78 per share in 2021, an increase of 10.3 percent and in line with previous increases. I also think an increase of this size is realistic, given the projected earnings and cash flow development.

Low dividend yield

However, due to the stock price gains in recent years, the dividend yield is only in the lower third of the last ten years’ long-term corridor, despite impressive dividend increases. Shareholders who put the Stryker stock in their portfolio today must thus count on the continuation of the company’s high dividend increases in the coming years and decades.

The fair value of the Stryker stock

As you can see below, the Stryker stock price has developed in parallel with adjusted earnings and operating cash flow over the long term. Nevertheless, there have always been phases in which the stock was significantly undervalued or overvalued. Currently, Stryker stocks appear overvalued in terms of both cash flow and adjusted earnings. However, thanks to further increasing profits and cash flows in the future, the fair values are rapidly approaching the current stock price.

Fundamental Stryker Stock Analysis Conclusion: Stryker stock – not a must for me

Stryker impresses with long-term revenue growth and continuously rising dividends. However, investors should take into account that acquisitions have strongly influenced growth. In addition to the rising mountain of debt, the Damocles sword of write-offs hovers over the company. Fundamentally, Stryker seems overvalued to me. Due to the high stock price, the current dividend yield is also relatively low with respect to the past. When buying the stock as of today, shareholders will have to be patient until the yield on cost reaches an attractive level, and the fair value of the stock has grown into the purchase price. Because of the ambitious valuation, Stryker stock is not a buy for me at this time.

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts. You can also share this post with your favorite network: