Please note: The analysis was compiled a few weeks ago and does not reflect the current status of events. You will find an update at the bottom of the article:

The Wirecard stock could be a story of success to this very day. Since 2005, the financial services provider has been increasing its profits year after year with one exception. Accordingly, the share price multiplied from 4 euros in 2000 to almost 200 euros by August 2018. But then the misery took its course. It all began with an inhouse presentation circulated in 2018 at Wirecard under the name “Project Tiger Summary”, which dealt with potentially questionable transactions and potentially dubious accounting at the Singapore subsidiary.

As always, I would appreciate it if you could give me short feedback in the comments below or share this post if you liked it or had the opportunity to pick up some valuable thoughts.

When a whistleblower gave the Financial Times’ internal documents, things escalated quickly. With several articles within a short period, the journal made the alleged violations public and substantiated them by publishing internal documents. After the short-selling attack by Zatarra Research in 2016, this was already the second time Wirecard had been criticized in this way. Many investors pulled the trigger and sold their shares. With the first article in the Financial Times, the Wirecard stock lost 35 percent in value within a week.

The Wirecard share price has not recovered sustainably to date (as of June 02, 2020). From the investors’ point of view, neither an audit by the external law firm Rajah & Tann in Singapore in March 2019 nor the most recent report by KPMG’s accountants were convincing enough to refute the accusations effectively. The fact that Wirecard has repeatedly asserted its innocence does not help either. The exorbitant price gains in the first half of 2018 in the run-up to the DAX listing are thus a thing of the past.

From a fundamental perspective, and this much can already be revealed, the Wirecard share looks like a bargain. On the other hand, we need to take a critical look at the risks. Therefore, now is an excellent opportunity to analyze the company with the help of the DividendStocks.Cash and to check whether the current situation offers you a good chance/risk ratio.

The business model: How Wirecard generates money

Over the years, Wirecard has become a significant provider in the field of digital payment transactions. The company owns banking licenses in many countries and can, therefore, offer its own credit cards. Besides, the company is primarily active as a payment processor, integrating other payment providers (such as Visa or MasterCard) into its payment infrastructure. For a fee, Wirecard can organize the transactions between the merchant and customer banks itself. It is also possible for Wirecard to process payments from customers who pay with Visa or MasterCard credit cards. Wirecard also charges a fee for this processing.

You may ask yourself why other payment providers or merchants should involve Wirecard in their payment processing. After all, Wirecard earns money on every transaction, which causes additional costs or lower sales for the parties concerned.

Nevertheless, the services offered by Wirecard are attractive for merchants and other payment providers. Merchants can accept payments from both Mastercard and Visa via Wirecard, which ensures higher customer satisfaction. In the case of credit card providers, Wirecard also bears the risk of payment default, and, of course, Wirecard charges a surcharge for this risk assumption. Overall, it is fair to say that you can regard Wirecard as a platform that offers merchants a complete solution for payments.

It is accordingly not surprising that the network of customers using Wirecard’s services is continually growing.

In the meantime, Wirecard is active in China as well. In addition to partnerships with Alipay and WeChat Pay (Tencent), the company has increased its footprint in the world’s most populous country by acquiring the Chinese company AllScore Payment Service. Wirecard acquired the company last year. At present, Wirecard holds 80 percent of AllScore and has the option to acquire the remaining 20 percent.

But even here, you cannot avoid a little “scandal”. The People’s Bank of China fined AllScore the equivalent of $16 million at the beginning of May. Before Wirecard acquired its stake in AllScore, a subsidiary of AllScore is said to have embezzled commissions and enabled cash transactions for illegal activities.

Fundamental Wirecard stock analysis – A growth check

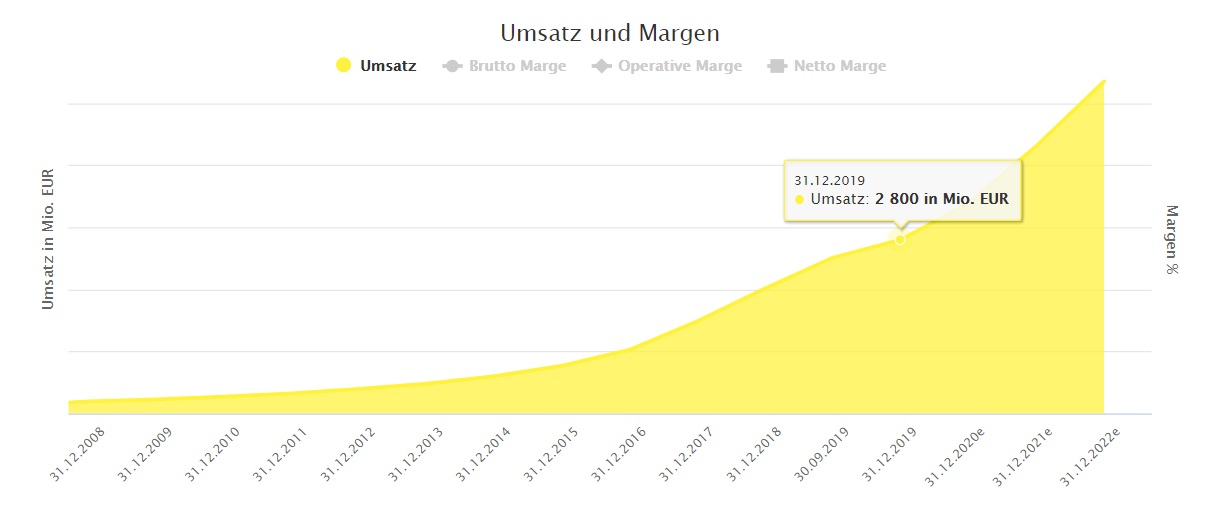

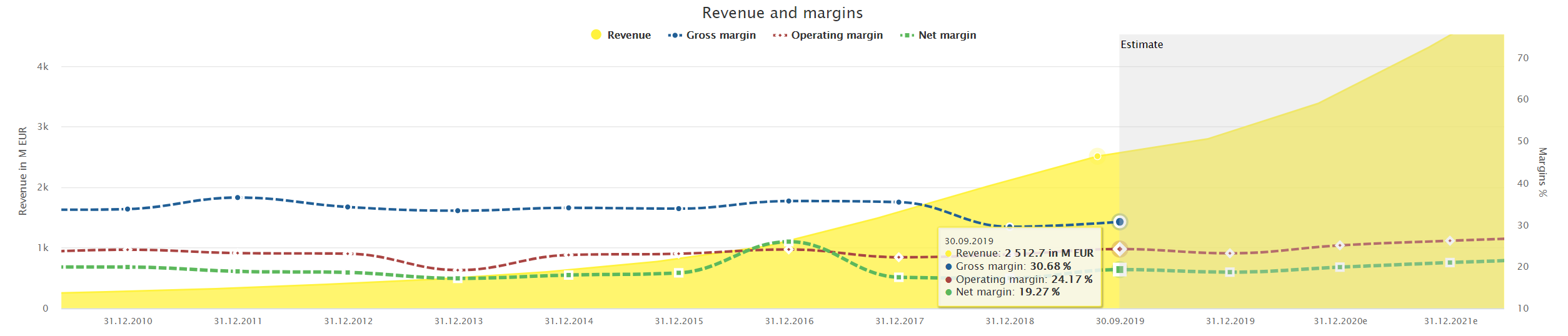

Away from all the scandals, business is flourishing for Wirecard. You can see that very well from the growth in revenue. Wirecard increased its revenue from almost €200 million in 2008 to €2.8 billion in 2019.

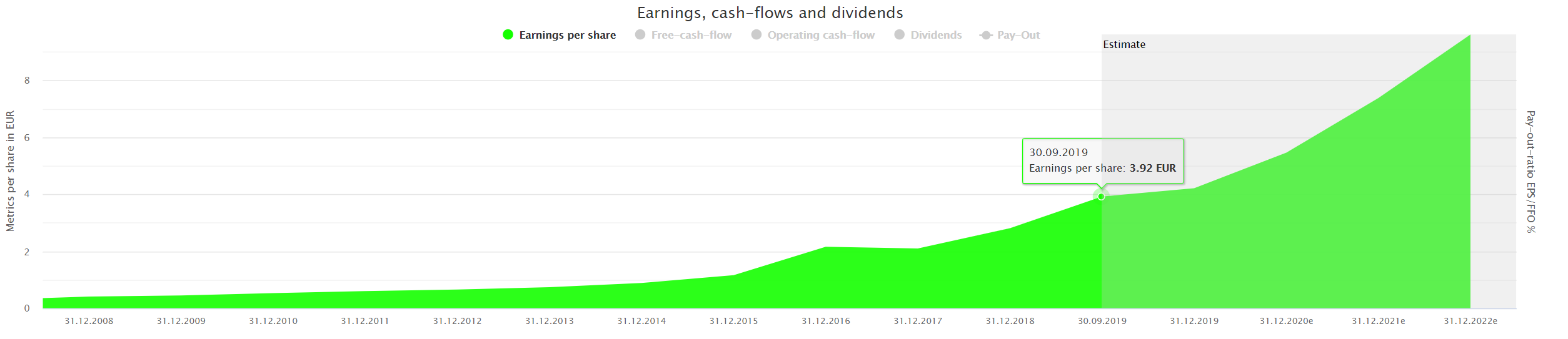

Wirecard’s earnings have also risen massively in recent years. While it still stood at €0.53 per share in 2010, it had increased to €3.93 per share by the end of 2019. In 2022, earnings are even expected to rise to €9.61 per share.

From my perspective, the trend towards cashless payments is not only likely to continue but could even accelerate due to the coronavirus. Therefore, I expect increasing profits in the future as well.

The growth in profits, which is running parallel to the increase in revenues, already points to stable profitability. DividendStocks.Cash does not show any irregularities here. The fact that the gross margin tends to be rather low can be explained by the fact that Wirecard can only charge meager fees per transaction carried out and that the profit is generated primarily via the number of transactions. Wirecard is in an excellent position compared to its competitor Adyen, which only achieves a gross margin of 18.7 percent. However, competitors such as Global Payments or First Data have margins similar to those of Wirecard.

Fundamental Wirecard stock analysis – dividend check

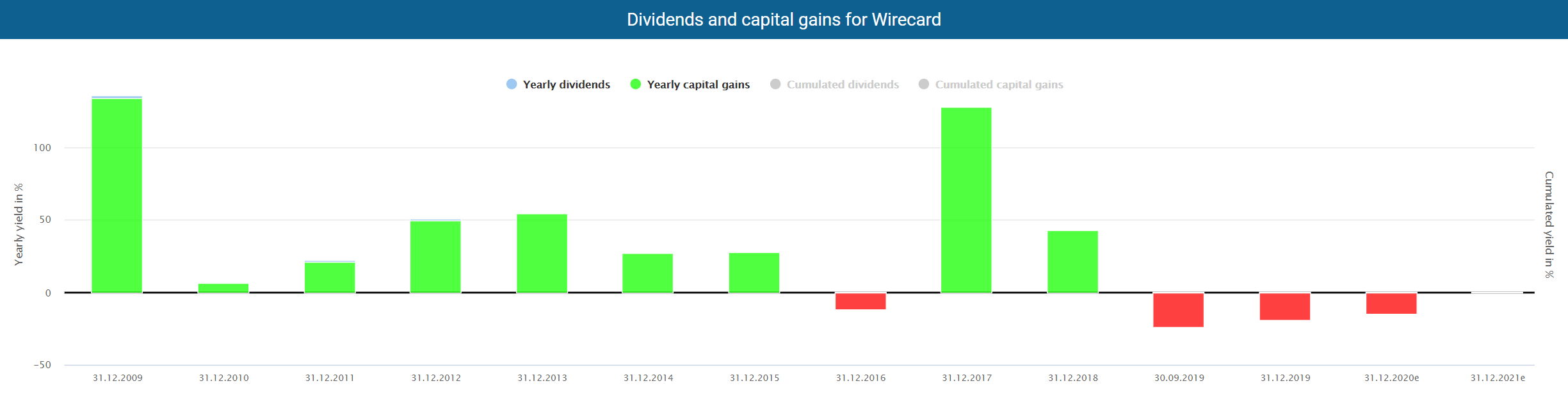

With a dividend yield of currently 0.3 percent, the Wirecard share is not targeted by income-oriented investors. But that could change. In recent years, Wirecard has always increased its distributions in the (low) double-digit range. The current payout ratio of just 5 percent offers a lot of leeway for future increases.

Fundamental Wirecard stock analysis: Bargain or trap?

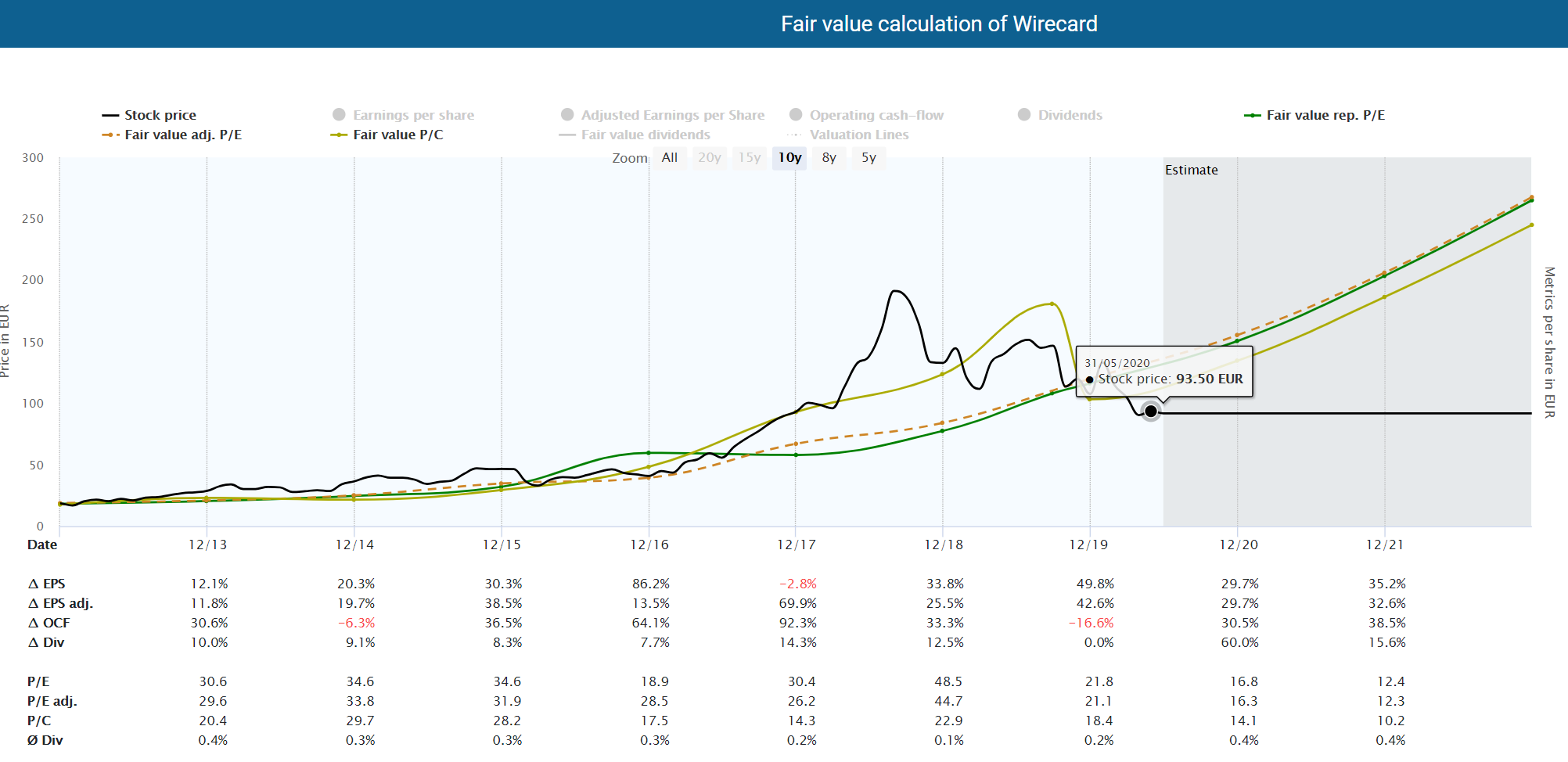

From a fundamental perspective, the market trades Wirecard stock currently at a massive discount. Based on the adjusted earnings, a fair valuation would require the stock to be around €133. At a current price of just over €90, it is far from this level. In this respect, there is a theoretical price potential of almost 50 percent. Besides, you can see that a favorable window of opportunity may have opened up, as Wirecard was overvalued from 2017 to the end of 2019.

The fundamental problem is, of course, written on the face of this purely profit-based assessment. A fundamental valuation of the stock, which does not sufficiently weight the accusations made against Wirecard, is merely impossible or negligent. That is why I would like to summarize the three essential points of the latest KPMG investigation.

Accusation 1: The third-party Acquirer business

One major accusation concerned the third-party acquirer business. The Financial Times accused Wirecard of having increased sales revenues and net profits through fictitious customer relationships. The Financial Times contacted 34 customers of the third-party partners, mainly based in Ireland and Dubai, and found several inconsistencies, especially with the “third-party acquirer” Al Alam.

The KPMG report published by Wirecard was unable to refute these accusations, contrary to management’s statements. KPMG failed to provide fully clarifying documents on the amount and existence of income from the criticized third-party business in the years 2016 to 2018, as the necessary documents were in possession of the third-party partners, and they were not prepared to cooperate. As a result, KPMG could neither “make a statement that the revenues exist and are correct in terms of amount nor make a statement that the revenues do not exist and are not correct in terms of their amount” for the investigation period 2016 to 2018.

Accusation 2: The Singapore business

Furthermore, the Financial Times accuses Wirecard of irregularities in the accounting of subsidiaries in Singapore. In addition to excessive revenues, the subsidiaries are said to have backdated contracts and transactions.

Here, too, KPGM’s report was disappointing, as it attested Wirecard blatant deficits in its accounting methods and at least questionable practices. In addition, Wirecard had concluded Software contracts “without economic substance” and booked them incorrectly. Also, KPGM was not able to examine all documents, as many are still in legal custody due to official investigation proceedings.

Accusation 3: The India business

The allegations concerning the Indian business only became public in the course of the KPGM investigations. The allegations concerned the purchase of the subsidiaries Hermes i Ticket and GI Technologies, for which Wirecard is said to have paid an excessively high purchase price using so-called “round-tripping“. A round-tripping is a series of transactions that are mainly used for money laundering in a criminal milieu. The purchase price of €340 million was paid to a fund in Mauritius acting as an intermediary, while the actual seller only received €37 million.

Again, the results of the investigation were disappointing as KPMG was unable to identify the seller. At the very least, KPMG found no evidence that members of Wirecard management were involved on the seller side.

Risk assessment of the Wirecard stock

The opportunities arising from the knocked-down stock price are offset by the risk that lax accounting and semi-fermented business activities are the rule rather than the exception at Wirecard. This situation is the reality you have to deal with as an investor. DividendStocks.Cash cannot take the qualitative due diligence off your hands. However, in the following, I would like to explain how I view this situation briefly.

Note: I have several Wirecard stocks in my broadly diversified retirement savings account. I am only giving you my private opinion as a private investor and no investing advice!

The accusations against Wirecard are quite substantial. But does it smell of falsification of the balance sheet and fraud in the tradition of the former energy company Enron?

It still cannot be ruled out, and in individual cases, it may be true that subsidiaries have been involved in false statements and other tricks. It is also apparent that communication with investors has not always been satisfactory. I take a critical view that Wirecard sees itself free of all accusations, while KPMG, as one of the most prominent accountants, identifies blatant deficits.

However, I think it is unlikely that Wirecard has been systematically and on a large scale bribing authorities and investors for years. The reason for this is that two of the largest accountants, KPMG as special accountant and EY as the regular accountant, have thoroughly examined Wirecard and received a great deal of public attention. Even if the KPGM report does not compliment their EY’s colleagues, investors can probably assume that Wirecard has built its business not on a house of cards, but that most of the transactions and business activities correspond to reality. I do not rule out that Wirecard has not always been able to keep pace with the growth of its business in terms of its operational organization and has brought on board one or two black sheep through its third-party partner programs.

The management has to learn that a company listed on the Dax has to apply completely different standards in terms of compliance and transparency than a small provider of payment services that mainly has porn or gambling sites as customers. The company is contributing here with a transparency offensive. The long-standing and controversial major shareholder and CEO, Dr. Markus Braun, will probably have to hand over further responsibilities to the Supervisory Board.

Conclusion: The Wirecard stock as a bargain for hard-boiled investors

It will still take a while before things settle down for Wirecard. So far, the serious allegations have not been cleared up, and the loss of confidence of investors is rightly enormous. However, you can see from the fundamental valuation that the market is already trading Wirecard at a discount to the fair value, right after the stock was overvalued for years. With a current P/E ratio of 22, the company looks fundamentally like a bargain given the speed of growth and the excellent prospects for digital payments. The stock is, therefore, worth considering as a more risky addition to your portfolio. If Wirecard manages to regain confidence from investors in the coming quarters, the price rocket could ignite, and we could see the old highs again.

Update on the denied testimony on 18.06.2020 – by Torsten Tiedt

The annual financial statements should be published on 18 June. Instead, Ernst & Young refused to issue an auditor’s certificate on the planned date of publication. The reason: the balance confirmation of two important accounts, into which Wirecard subsidiaries have paid a total of 1.9 billion euros, is incorrect. Worse still: it does not appear to be a technical error, but rather a deliberate deception. The intention to defraud is therefore obvious. Accordingly, Wirecard has filed a complaint against unknown persons.

The two accounts are accounts in which securities are deposited for merchants in the event of payment defaults, because “in addition to the core services … Wirecard also provides the financing of loans. As a rule, the borrowers are external third parties, i.e. private consumers or companies, … . The risk of default is minimized by means of loan collateral”. (Source: Annual financial statement 2018, p. 38).

As the collateral is provided by Wirecard, the money is managed in trust accounts and not directly by Wirecard. The trustee was only appointed last year in 2019 and the trust accounts are managed by Asian banks.

What is at stake are “not only” the 1.9 billion euros actually paid in by Wirecard subsidiaries, but also loans amounting to 2 billion euros, which could be terminated as early as June 19 in the event of a lack of an audit certificate. In this case, the insolvency of the company would not be ruled out.

In principle, I consider it unlikely that one or more banks would pull the plug on a Dax group overnight. But with Wirecard, nothing can be ruled out anymore.

In the wake of this scandal, Wirecard has destroyed further trust. Even a resignation of CEO Markus Braun, which has been demanded for quite some time, is unlikely to restore confidence in Wirecard in the foreseeable future.

–> Click here for more analysis <–

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.