Welcome to a new episode of my Dividend Diary on the TEV Blog. Here, I report the development of a cash flow-oriented investment approach that focuses on generating a passive income through dividends. Against this background, the goal is not to outperform the market but to put food on the table through a regular income via dividends.

With the Dividend Diary, I document how a cash-flow investment approach can be part of well-balanced wealth management. To keep things simple, I have built three pillars:

- Active income.

- Passive income.

- Conversion.

Dividends fall into the last two categories. They are passive because they provide a cash flow without me having to go to work. Additionally, they are an essential pillar for the conversion since they can be reinvested to generate even more income in the future. That is the Theory. Now let’s get down to practice.

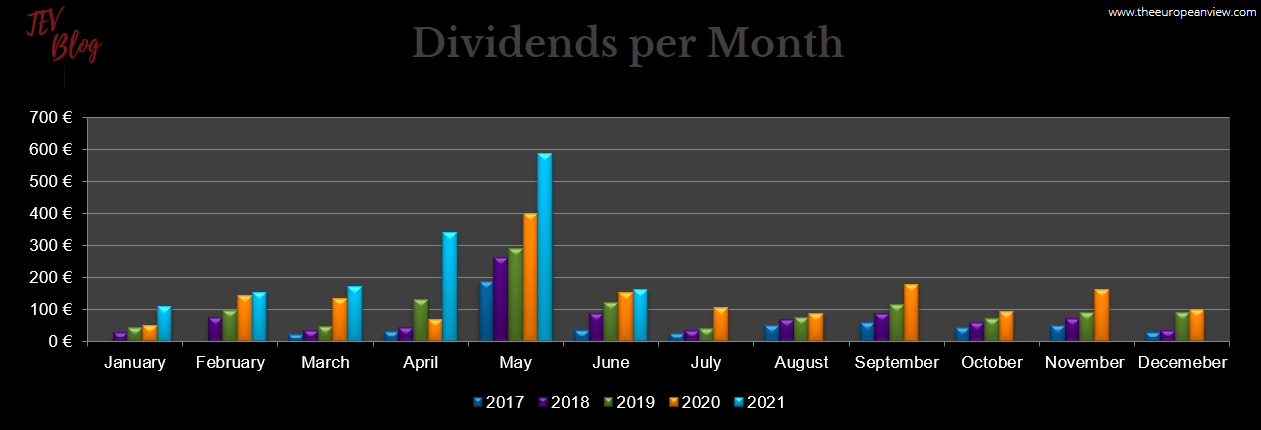

My monthly dividend income in June:

This month, my cash-flow approach generated the following income through dividends:

- Tencent (2.48 EUR)

- Johnson & Johnson (12.97 EUR)

- Archer-Daniels-Midland (7.90 EUR)

- Unilever (14.55 EUR)

- IBM (14.98 EUR)

- Snap-on (8.99 EUR)

- Reckitt Benckiser Group (24.18 EUR)

- 3M (11.71 EUR)

- Realty Income (3.01 EUR)

- Kontoor Brands (4.90 EUR)

- Royal Dutch Shell (6.69 EUR)

- V.F. Corp (13.38 EUR)

- Qualcomm (9.32 EUR)

- Broadcom (11.17 EUR)

- PepsiCo. (10.67 EUR)

- Imperial Brands (4.52 EUR)

The total dividend income in June (after taxes) was: EUR 161.42/appr. 191 USD

Dividend income check

Dividend income in June was satisfactory and a slight increase versus June 2020. But compared with April and May 2021, there was no sharp jump in income. The reason is simple. Unlike in previous years, none of my European holdings, which mostly distribute dividends once a year, paid a dividend in June 2021.

In June 2020, things were different. Back then, some companies had paid their suspended April and May dividends (Henkel and Deutsche Telekom were among them). Therefore, the June ’20 income was unnaturally high.

Additionally, the strong EUR against the USD also had a somewhat adverse impact this year. Overall, however, I expect this month to be the last in which base effects from pandemic distortions significantly impact year-to-year comparisons. They will then be less pronounced during the rest of the year.

Looking at the big picture, things are evolving pretty well.

Letting things go their way

Let’s reflect on June for a moment. Not much happened, honestly. I was on vacation and did not pay much attention to the stock markets. I did not sell any shares and executed most of the purchases in the last days of the month.

Nevertheless, I would still be extremely excited about a more substantial market correction. Stock markets are still relatively high valued and quality stocks, in particular, have a hefty price tag. Here, I am simply not willing to go along with any nonsense.

Meme stocks are robust

Just take a look at the meme stocks. More and more “meme companies” are taking advantage of the high prices to increase their equity. Usually, such a move would trigger an already hot share price to plummet since it signals that management considers its shares to be overvalued.

But not these days.

The investors around Wallstreetbets & Co. don’t care about the fundamental valuation of a share. Instead, they are soldiers of fortune, looking for a quick profit. Their criteria are an optically low price, a possible turnaround narrative, and a high short ratio to provoke short squeezes. It is a bubble from a fundamental point of view. But that’s not a bad thing, as long as I and my capital don’t get involved there.

It’s all about the narratives

Every bubble has its justifying narrative, i.e., a story that lures investors. Regarding the so-called meme stocks, investors’ strategy is to provoke short squeezes. Therefore, they look for stocks that have a high short ratio. In some cases, the battle of private investors against short sellers/hedge funds has been stylized as a battle of good versus evil.

However, it is questionable whether and for how long such narratives will last or sustain further price increases. For example, the short ratio at GameStop and AMC fell to around 20 percent without putting an end to the spook.

Investors are therefore making themselves dependent on developments that they cannot control. Moreover, compared to institutional investors, they are even at a disadvantage because information on the build-up and reduction of short positions only reaches the broad market with a delay.

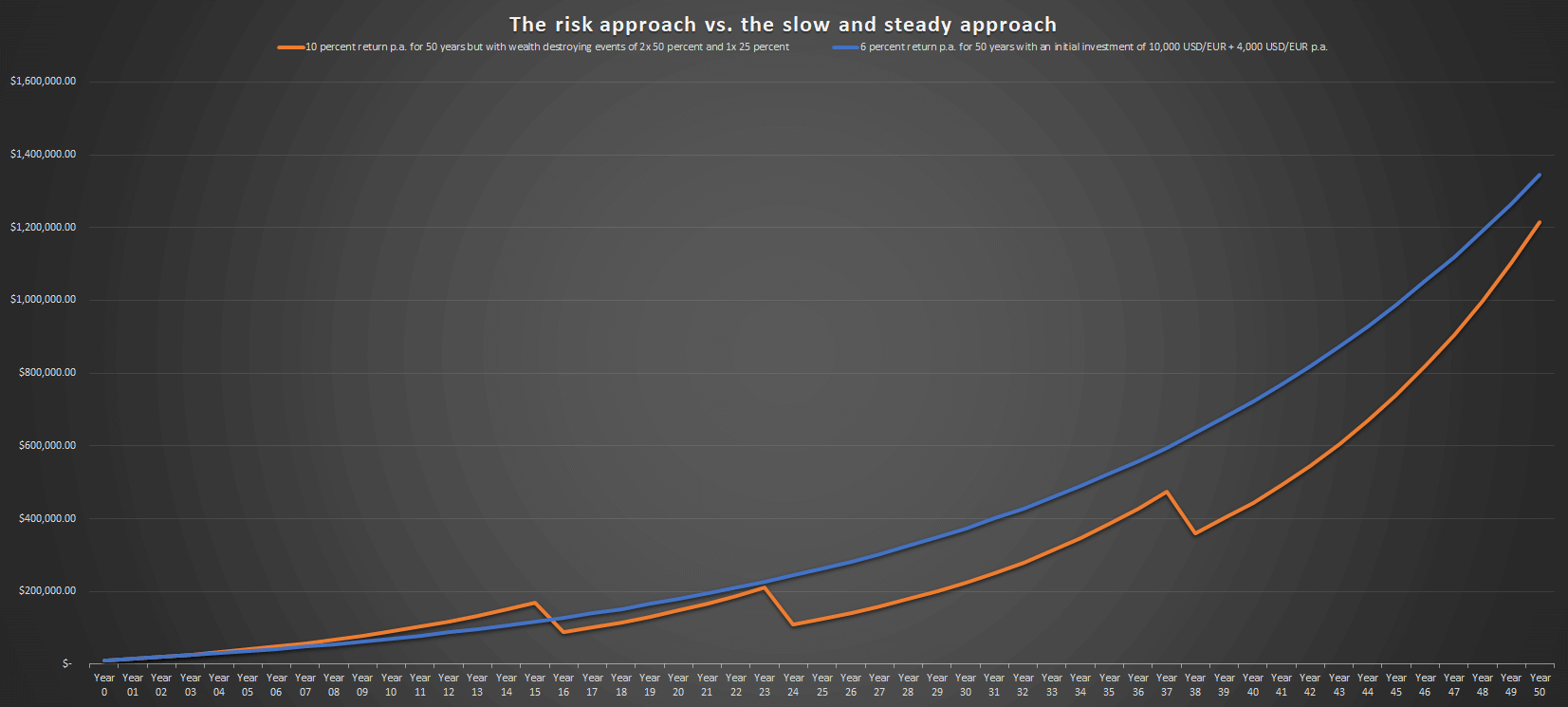

The devastating impact of final wealth-destroying events

I mean, we all want to benefit from rising profits and dividends. Nevertheless, we cannot ignore the devastating impact of final wealth-destroying events. It doesn’t matter that an approach brings an above-average annual performance of 10 percent for 47 years.

In a period of 50 years, three final wealth-destroying events with an impact of 2x -50 and 1x -25 percent will still lead to underperformance. These events, which only occur in only three out of 50 years, squeeze the overall annual performance below 6 percent.

A dull annual performance of 6 percent per year would be the better choice. I must only come through the years without these final wealth-destroying events.

I don’t care about all that noises

When I drew attention to the changing tectonic movements concerning retail investors last summer, I could only guess the current developments. But now they are here.

I have no idea how the stock markets will develop further. And I’m certainly not going to try to time the market in any way. I simply do not care.

I have the choice in which companies I invest. The share price and operating business are linked. Shares are the investor’s proof of legal ownership over a company, which means that the fate of the share is tied to the fate of the underlying business.

The more the share price is decoupled from the operating business, the higher the risk for the investor. For the long-term development of one’s assets, this risk consideration is the decisive point. Here, I am not risk-averse. I am only safety-focused, and I can decide with which risk profile I want to go on the road. Now is not the time to take high risks. Safety awareness should be at the forefront.

Putting the weight on safety rather than risk

That’s why I put the weight on safety rather than risk. I am not risk-averse, just safety-minded. This is a subtle difference in thinking.

I am not afraid of risks because opportunities always mirror risks.

However, safety results from an overall consideration of opportunity and risk in a long-term view. And investing in fundamentally overheated markets or riding bubbles is an absolute disaster for long-term safety (see the graph above). So reducing my exposure to risk is a result of a safety-focused investment approach.

Stock purchases in June

In June, I bought more shares of great companies so that the dividends will continue to rise in the future:

- Munich Re (3 shares)

- MSCI USA Financials (38 shares)

- General Mills (17 shares)

In the following, I will briefly explain why I bought these companies. Please do not expect a fundamental analysis. I will only mention some aspects per company that might be of interest to the readers. Maybe you will find inspiration for your investment. In case you disagree, feel free to write your opinion about my purchases in the comments.

Please keep in mind that this is only a non-representative sample of my overall asset management.

As I said above, I found it particularly difficult to decide on specific share purchases this month. I was thus pragmatic and increased the weight of my two ETF holdings. With these ETFs, I cover the emerging markets and the US financial sector. These sectors would otherwise be severely underrepresented in my portfolio, which is why I am increasing the shares in both ETFs bit by bit. There is little exciting to report here, which is why I will keep things short.

My last purchases were in September 2020, November 2020, December 2020, and April 2021). Generally speaking, I am happy to increase my emerging market exposure step by step. Nevertheless, measured against the invested capital, the share of my emerging markets investments (including my Ping An Insurance and Tencent holdings) is still too low at 7.5 percent. It should be at least 10 percent.

MSCI USA Financials ETF

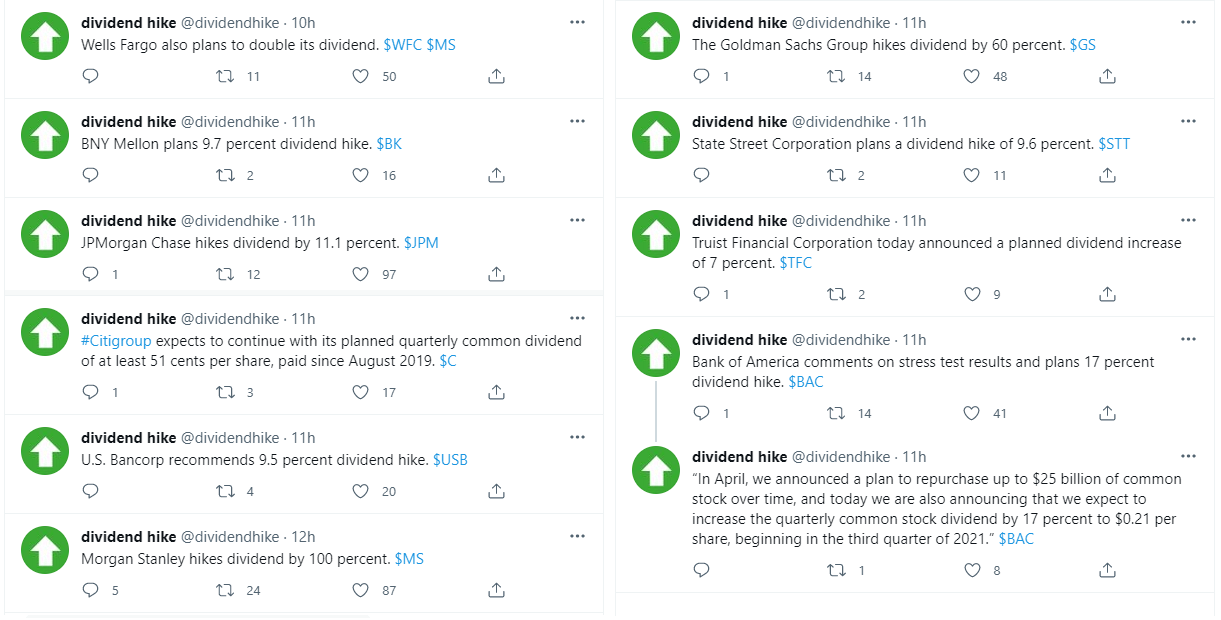

My last purchases were in May 2020 and February 2021. A key reason for the purchase this month was the prospect of banks once again having more scope to use their high cash reserves for share buybacks and dividends. And indeed. Following the Fed’s positive stress test, U.S. banks increased their capital distributions to shareholders one after the other.

Many of these companies are also represented in my ETF, in some cases with high shares. I therefore also hope for a decent increase in the distribution in the spring of 2022 (the ETF pays the dividend only once a year).

Just as pragmatically as with my ETF purchases, I have added more shares to a few existing stock holdings in a rather random manner. One of my increases was Munich Re, the biggest reinsurance company in the world. The company is also active in the insurance business via its subsidiary ERGO and asset management via its subsidiary MEAG.

Fundamental considerations were less decisive here since it is challenging to value reinsurance companies based on fundamentals. Damage events can strongly influence the results of specific years and are not predictable. Accordingly, a natural disaster or other events could bring the profits and the share price to its knees as early as tomorrow.

Thus, other aspects than fundamental considerations were decisive for the additional purchase of Munich Re shares. Right now, the share price is 16 percent below its pre-Corona high. In the last few months alone, the share price has fallen by over 10 percent. But the company isn’t any different today than it was a year or two ago – just cheaper.

On the other side, Munich Re still has excellent ratings. It is also fairly in line with the necessary Solvency II capital ratio, which requires by law a level of equity at which non-compliance with the solvency requirements can occur at most due to a shock event that only occurs statistically every 200 years.

So what we see here are rather normal price fluctuations. I like to use such volatilities to benefit from the dividend payments in the long term.

The dividend yield is over 4 percent which is roughly in line with the historical average and sweet enough for me. After the company did not increase the dividend this year, I expect another mid-single-digit increase next year. Why? Munich Re is aiming for a consolidated profit of €2.8 billion for the 2021 financial year. To remind you: profit in 2020 was only €1.2 billion. From the current perspective, management, therefore, has sufficient scope for a dividend increase next year.

In addition, Munich Re could resume its share buyback program in 2022. The company has already massively reduced the number of outstanding shares from 228 million in 2004 to the current 140.1 million. Last year, management paused the planned buyback program because of the pandemic. I think management may pick that up again in 2022.

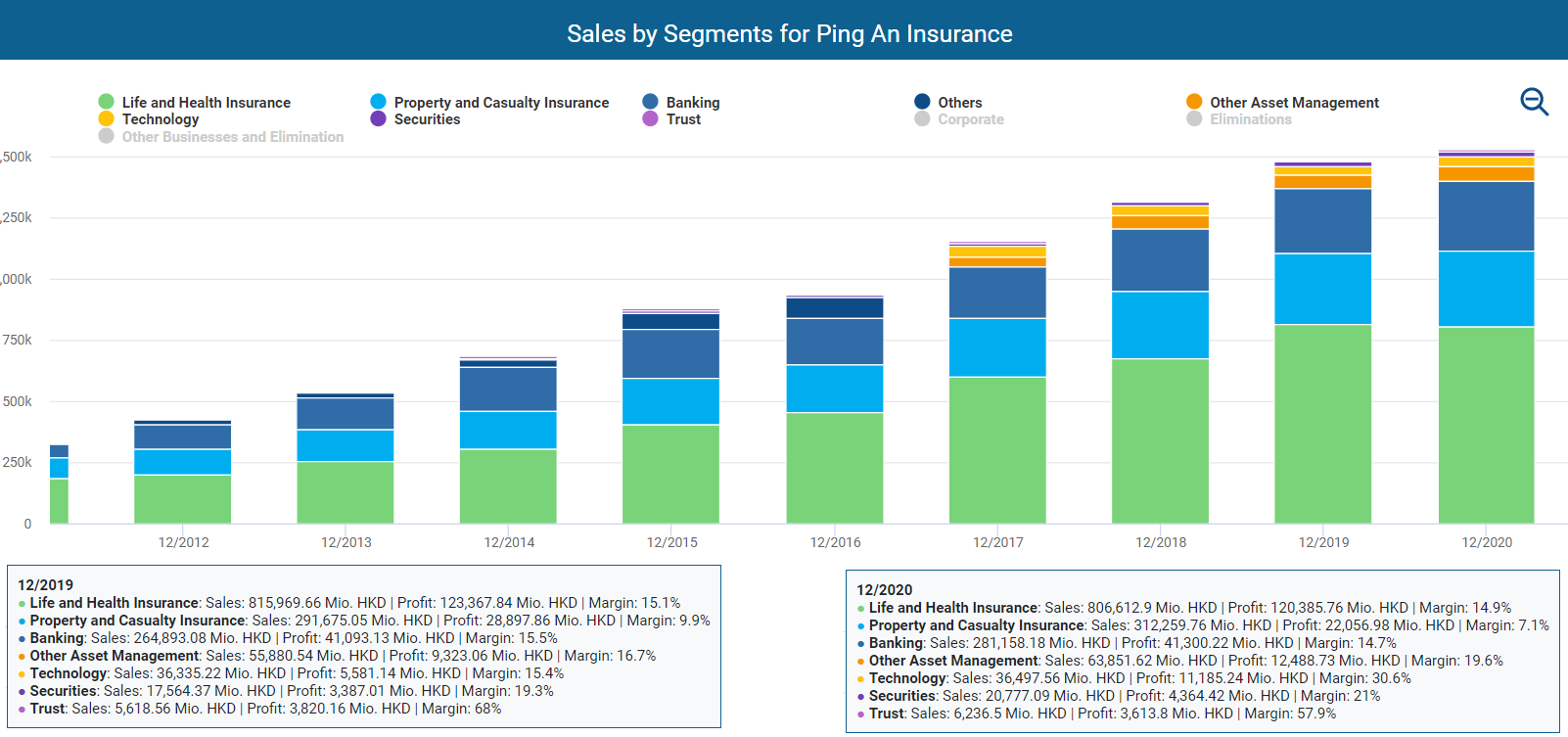

By adding 100 more shares of the Ping An Insurance stock to my portfolio, I doubled my stake in the insurance giants. My initial investment was in March 2020, hence, not so long ago. The stock price has dropped somewhat in the last few months, so I have averaged down a bit.

Operationally, things are going well for the company, which is also increasingly establishing itself in the banking, tech, and cloud sectors. While the traditional insurance business had some growth problems in 2020, the banking and technology segments performed nicely.

Overall, I like the mix of technology, platform, and insurance business. The business approach is relatively unique and offers exciting growth opportunities for the future. The following steps are global expansion. This is particularly exciting and necessary, as the Chinese market is also opening up to foreign insurance companies. So Ping An needs to expand globally as well.

If you want a better sense of the company, I recommend the following interview with one of Ping An Insurance’s Co-CEOs. Here, Jessica Tan gives some insights on how the company plans to strengthen its technology business.

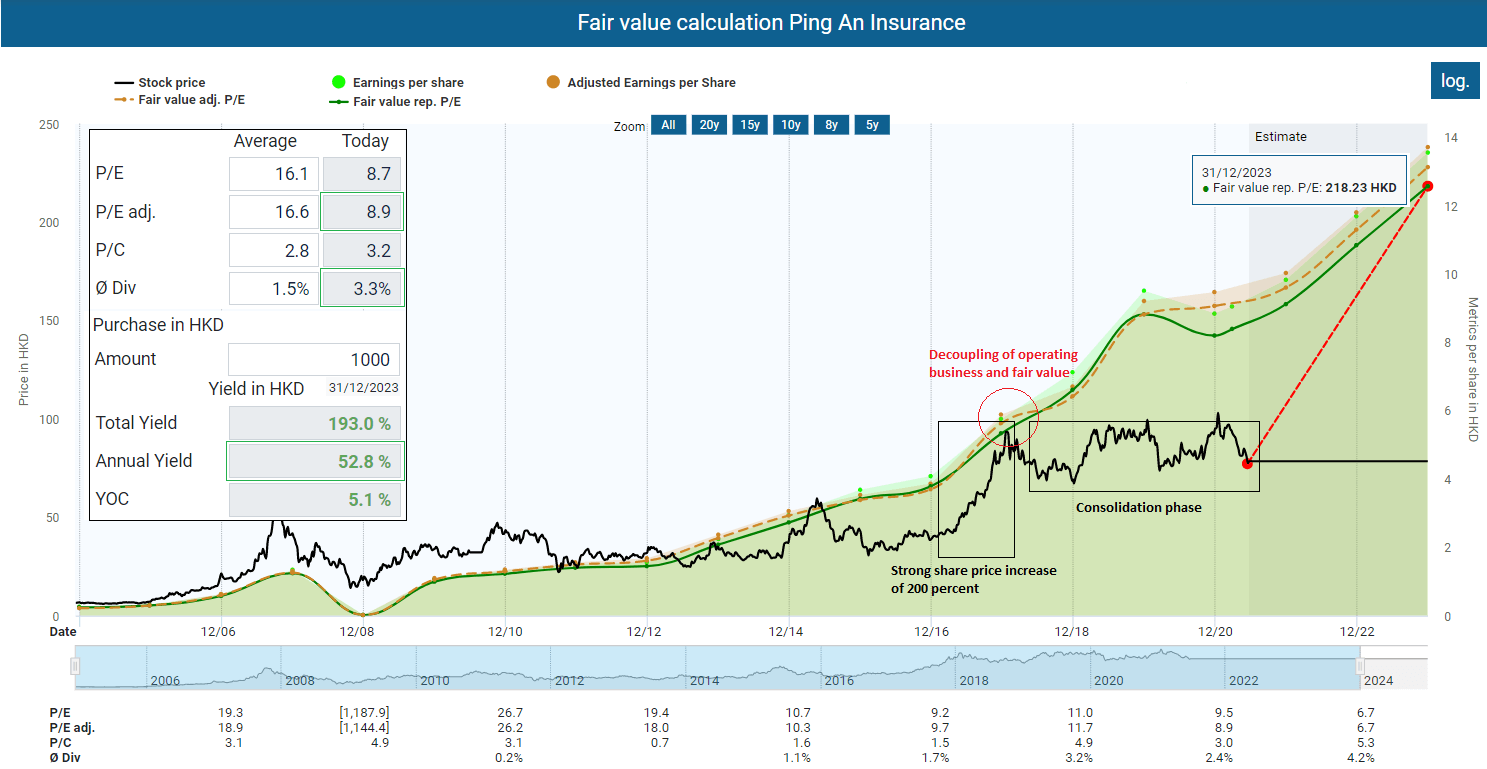

As with many Chinese companies, the share price has decoupled from operating performance. With the current adjusted P/E ratio of below 9, the stock is currently in bargain territory. The share price may fall even further. Currently, the holding is less than 2 percent of my invested capital. So I still have some room to maneuver if the price drops further.

Also, I’m more interested in the cash flow that companies offer me. The dividend yield is currently 3.3 percent which is not that much compared to European insurance companies. However, Ping An distributes less than 30 percent of its profits. Based on the expected cash flow in the next few years, the cash flow payout ratio will also be below 30 percent. In this respect, further payout increases in the range of 10 to 20 percent per year are possible for the coming years.

In addition, the annual return is almost 50 percent if we only look at the historical multiples and the expected profits for the coming two years. However, this is more of an arithmetical gimmick. For my investment decision, the dividend yield and increasing payouts were decisive.

Finally, I bought 17 shares of General Mills. The company is one of my anchor investments. Its share of my total portfolio is now slightly above 3 percent in terms of invested capital.

Yep, the share price performance was mostly flat in recent years. But General Mills is gaining momentum as management does a good job of getting the ship back on track. Firstly, management has reduced debt after the expensive $8 billion Blue Buffalo acquisition. Based on interest-bearing debt, the debt ratio fell from 41.2 percent in 2018 to 35 percent. Quite nice, considering that a major recession fell during this period.

Secondly, the company is benefiting from the strong growth of the pet food business. The pets segment revenue increased from $1.4 billion in 2019 to $1.7 billion in 2020, with profit climbing as much as $268 million to $390 million. In addition, General Mills increase its profit margin for its pets segment by five percentage points.

With an adjusted P/E ratio of 15, the share is attractively valued – at least considering the current market conditions. The dividend yield of over 3 percent is also above the long-term average. General Mills is also again regularly increasing its dividend by a mid-single-digit percentage. I expect the subsequent dividend increase within the same range as early as this fall.

Watchlist for July

There will be some additional share purchases next month. As you may know, I am relatively flexible when it comes to new investments. Either I buy new positions, or I increase my shares in existing investments.

The following companies are on my watchlist in particular:

- Microsoft (MSFT)

- Digital Turbine (APPS)

- Intel (INTC)

- Salesforce (CRM)

- Mayr-Melnhof Karton AG

- SAP (SAP)

- Bayer

- Hugo Boss

If you look at my report from last month, you will likely see that none of the companies I bought were on my watchlist. Why is that? Is the watchlist nonsense, and in the end, I only do what I want anyway? Yeah, a little bit. I don’t have a fixed system for my stock purchases, and that’s one thing I have to consider changing.

However, I have an extensive overview of many companies that I look at from time to time. The watchlist companies are primarily companies that I have currently examined particularly carefully, where substantial changes are imminent or which are in my focus for other reasons.

These companies are present to me in some form, which is why I put them on the list and perhaps monitor them a little more closely than other companies. But it often happens that I invest in different companies when it seems convenient at that moment.

Hi. In which exchange do you buy ping an?

Hi Thiago. I have the H shares, which are traded on the Hong Kong Stock Exchange.

Best!