A common question among investors is whether the price of a stock is above its intrinsic value or not. However, calculating the intrinsic value can be challenging. Besides, Warren Buffett and Charlie Munger admit that today it is more difficult to find companies with an intrinsic value higher than their share price. An original transcript of Warren Buffett’s and Charlie Munger’s speech during a Berkshire Hathaway Annual meeting helps to understand what intrinsic value is, how it can be calculated, and why it is so complicated.

Investors Key Takeaway

- The reason why investors look at a company’s intrinsic value is that its value and the price (market capitalization) can be different. Simply put, you can get less value than you pay for.

- While market capitalization follows the daily fluctuations in the stock market, the intrinsic value allows to make a stronger fundamental and long-term valuation of a company.

- In summary, intrinsic value is the value of a company or an asset class that excludes daily volatility and price fluctuations and paints a fundamental long-term picture of an asset class.

- You can calculate the intrinsic value by looking at a company’s future cash flow to its shareholders. Then, you need to compare this cash flow with other assets or asset classes.

- The problem is, however, that the future cash flow is not fixed, unlike the coupon on bonds. You must, therefore, predict the cash flow yourself, which requires that you know the company and its business model very well.

Price is what you pay, and value is what you get

When you talk about the intrinsic value of a company or a stock, you have to consider two components. One is the price of a stock, and the other is the value behind it. Since you want to invest in a business and this business has a specific price, you need to know what value you will get for that price.

Is the company a steal, or does someone want to sell you trash for gold? To answer this question, you should be guided by Warren Buffett’s wisdom who once said,

“Price is what you pay; value is what you get”.

The arbitrage due to gap between price and value is precisely the reason why investors are looking at a company’s intrinsic value. They want to know how significant the difference between the market price and the inherent value is.

What is the difference between intrinsic value and market value

The first thing you need to understand is that the value of a stock and the price of a stock can differ, which means that the market value (=market capitalization) of a company and its intrinsic value can be different.

Market capitalization of a company refers to the total market value of all outstanding shares. You can easily calculate the market cap by multiplying the total number of outstanding shares by the price of one stock. But you know yourself that the price of a share can fluctuate. Wee see it every on the stock markets which are very volatile, driven sometimes by fear and sometimes by greed.

Take the company Apple as an example. There are days when the share price drops by two percent without any obvious reason. This also reduces the market capitalization by two percent. But why should Apple be worth 2 percent less for you as an owner? Therefore, it is essential to find a valuation and a yardstick that cuts these daily fluctuations out and draws a fundamental long-term picture of the company.

To sum things up: The intrinsic value shows the inherent value of an asset class by excluding all daily fluctuations and side noises. It’s quite simple so far, isn’t it?

In the following, we will take a closer look at the method of calculating the intrinsic value. For this purpose, we will use a transcript of Berkshire Hathaway’s legendary Shareholders Meeting. There, Warren Buffett and Charlie Munger explained how they calculate intrinsic value and what might be different today than a few decades ago.

At one of Berkshire Hathaway’s legendary annual shareholder meetings (the “Woodstock for Capitalists”) in Omaha, Nebraska, a shareholder asked an interesting question.

Unfortunately, I could not verify the year of the meeting. It may have taken place in the late 1990s, perhaps in 1997 or 1998. Nevertheless, we now come to the particular question. Here is the transcript:

You write and speak a great deal about intrinsic value, and you indicate that you try to give shareholders the tools in the annual report so they can come to their own determination.

What I’d like you to do is expand upon that a little bit. First of all, what do you believe to be the important tools either in the Berkshire annual report or other annual reports that you review in determining intrinsic value?

Secondly, what rules or principles or standards do you use in applying those tools? And lastly, how does that process relate to what you have previously described as the filters you use in determining your valuation of a company?

Strictly speaking, the shareholder asked several questions. But they all revolve around the intrinsic value and Warren Buffett’s and Charlie Munger’s approach to calculate it. In the following, both did not answer the questions one after the other but held individual (from in my view legendary) monologues. Therefore, it makes sense to stick to the transcript and go through this piece by piece.

Warren Buffet’s intrinsic value calculation

Warren Buffett starts. He compares the future cash flow of a share with the coupon rate of other asset classes such as bonds.

The coupon method

Warren Buffett:

If we could see at any business its future cash inflows or outflows from the business to the owners … over the next hundred years or until the business is extinct and then could discount that back at the appropriate interest rate …, that would give us a number for intrinsic value.

In other words, it would be like looking at a bond that had a whole bunch of coupons on it …. If you could see what those coupons are, you can figure the value of that bond compared to government bonds, if you want to stick an appropriate risk trade-in.

Or you can compare one government bond with a five percent coupon to another government bond with a seven percent coupons. Each one of those bonds has a different value because they have different coupons printed on them.

Businesses have coupons that are going to develop in the future too.

At the same time, Warren Buffett draws attention to a problem. The coupon of bonds is a fixed amount determined by the issuer. In the case of companies, investors must check how high the company’s cash flow to shareholders will be in the future to be able to compare this figure with other companies or asset classes.

So to be able to determine this cash flow correctly, you need to know the company and its business model. This requirement is one reason why Warren Buffett is so reluctant to invest in tech stocks. He simply has not understood (or did not want to understand) the business model of such companies.

Warren Buffett:

The only problem is they aren’t printed on the instrument, and it’s up to the investor to try to estimate what those coupons are going to be over time.

As we have said in high-tech businesses or something like that, we don’t have the faintest idea what the coupons are going to be.

When we get into businesses where we think we can understand them reasonably well, we are trying to print the coupons out. We are trying to figure out what businesses are going to be worth in 10 or 20 years.

When we bought See’s Candies in 1972, we had to come to the judgment as to whether we could figure out the competitive forces that would operate the strengths and weaknesses of the company and how that would look over a 10 or 20 or 30 year period.

And if you attempt to assess the intrinsic value, it all relates to cash flows.

The importance of cash flow in value investing

After this illustration of intrinsic value, Warren Buffett shares general wisdom that fits in perfectly with the previous explanations.

Warren Buffett:

The only reason for putting cash into any kind of investment now is because you expect to take cash out; not by selling it to somebody else because that’s just a game of who beats who.

This sentence can hardly be surpassed in wisdom and clarity. It illustrates once again what is essential when investing and what the difference to pure speculation is.

My betting slip analogy correspondences to this groundbreaking sentence. I want to become an owner of companies and therefore want to get a substance for my money, not just a coupon that might increase in value. I want something that puts food on the table.

Otherwise, a company’s share is no longer the proof of ownership but a kind of betting slip with which one can bet that share prices will rise.

Obviously, we don’t think we know the three decimal places or two decimal places or anything like that.

But we have a high degree of confidence that we’re in the ballpark with certain kinds of businesses. The filters are designed to make sure we’re in those kinds of businesses.

We basically use long-term risk-free let’s [say] government bond type interest rates to think back in terms of what we should discount at. And you know that’s what the game of investment is all about.

Investment is putting out money to get more money back later on from the asset and not by selling it to somebody else but by what the asset itself will produce.

If you’re an investor you’re looking at what the asset is going to do, in our case [at what the] businesses [is going to do].

If you’re a speculator, you’re primarily focusing on what the price of the object is going to do independent of the business, and that’s not our game. So we figure if we’re right about the business we’re going to make a lot of money and if we’re wrong about the business we don’t have any hopes, we don’t expect to make money.

Charlie Munger’s filter of opportunity costs

Remember the shareholder’s questions? He wanted to know several things.

Firstly, he was interested in the principles Warren Buffett, and Charlie Munger applied in assessing intrinsic value. Besides, he also wanted to know which filters the two investors use for assessment.

He had a valid point here. It is indeed challenging to analyze the cash flow of hundreds or thousands of companies.

Charlie Munger:

I would argue that one filter that’s useful in investing is the simple idea of opportunity cost.

If you have one opportunity that you already have available in large quantity and you like it better than 98 of the other things you see, well, you can just screen out the other 98 percent because you already know something better.

So those people who have a lot of opportunities tend to make better investments than people that don’t have a lot of opportunities and people who have very good opportunities, and using a concept of opportunity costs they can make better decisions about what to buy.

With this attitude, you get a concentrated portfolio which we don’t mind.

This theory of opportunity costs is a significant point, which I have already mentioned in another article about multiple passive income streams.

Many investors want multiple income streams and invest their money in different asset classes. This approach is what they call diversification. But the first question is why I should invest in an asset class that gives me less return than another?

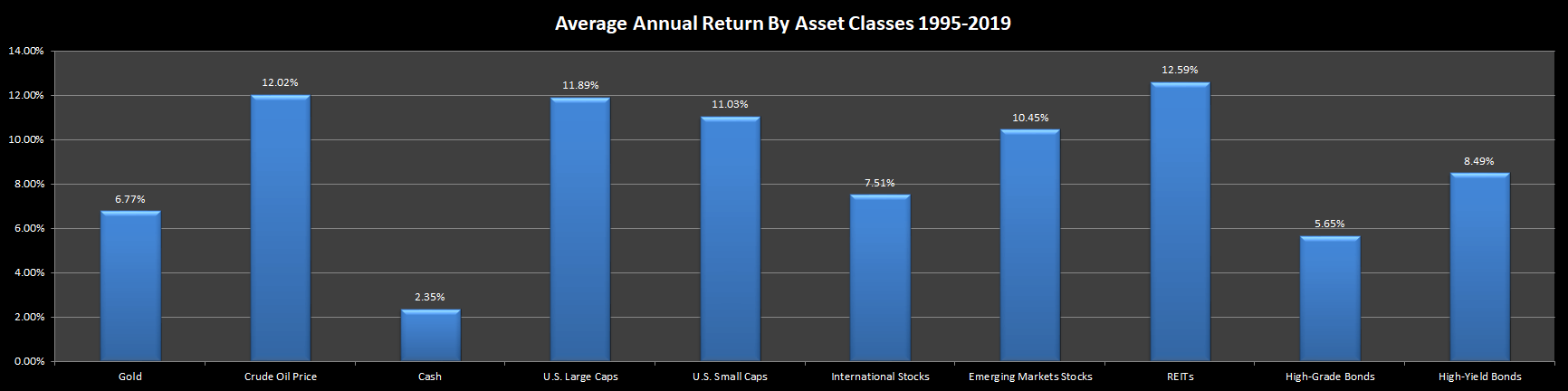

Looking at performances of different asset classes

Not all asset classes have the same historical performance. So an asset class with a lower return than another must give you a reason to invest. Gold is a good example. As you can see, gold has historically had a very poor performance

Gold bugs then quickly say: Gold is a crisis asset. Indeed, in times of recent major crises, gold has usually performed better than the average market.

In the last year of the Great Depression, for example, gold gained more than 40 percent in value. In other crises such as the bursting of the dot.com bubble or the financial crisis, gold has also outperformed equities.

Opportunity costs can be expensive

So at the end of the day, two things are essential when we are talking about opportunity costs:

- risk allocation/diversification, and

- risk correlation.

Hence, you can save your opportunity costs by excluding anything that offers either

- less return,

- no further risk diversification, and

- no better correlation coefficients.

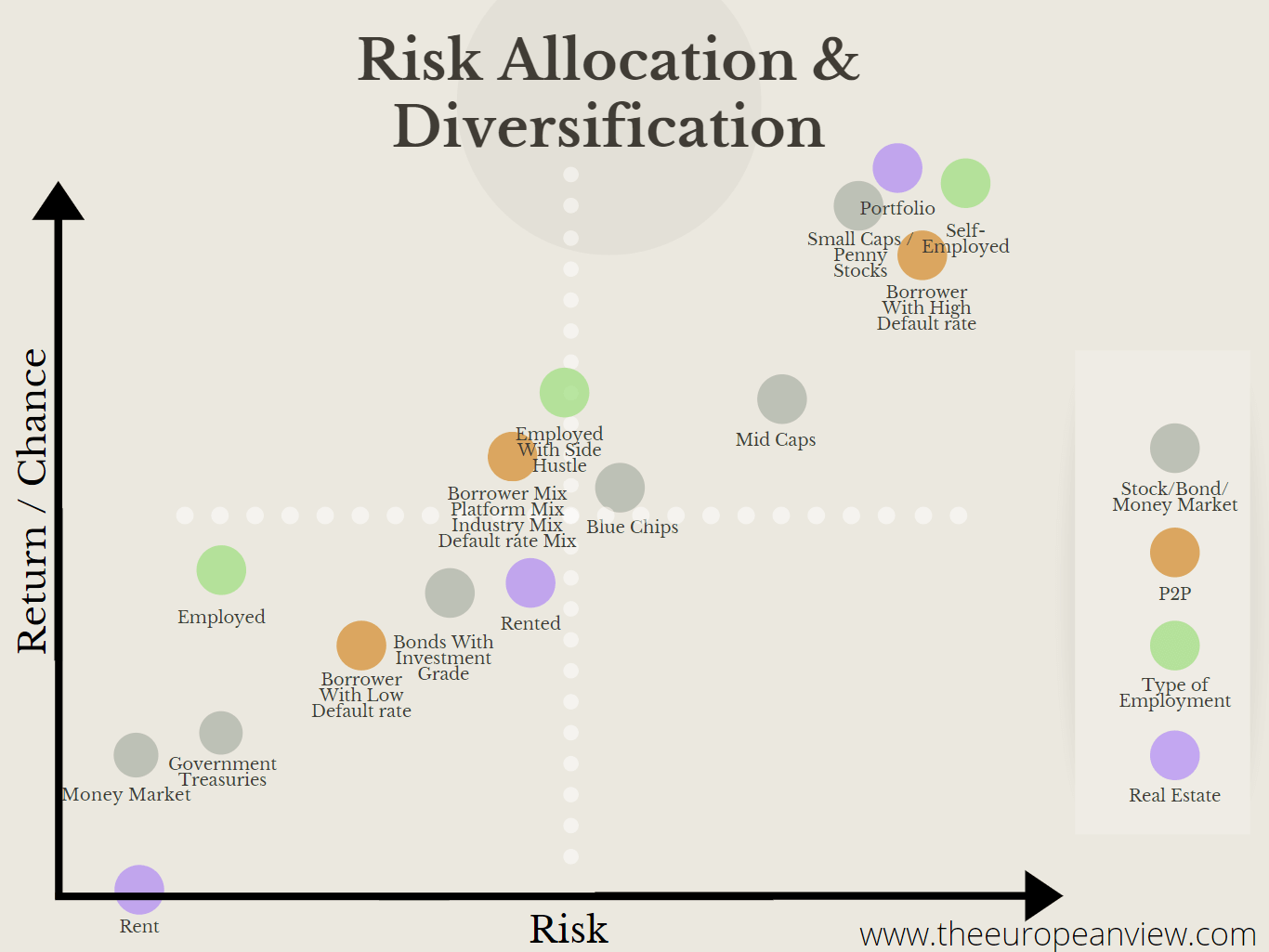

But as you can see in the following picture, most asset classes have several risk profiles. So there is little point in investing in many asset classes if they all have the same risk.

Thus here you can reduce your opportunity costs by eliminating asset classes from the outset that do not generate a better return than your existing asset classes and have a higher risk.

Conversely, however, it may make sense to invest in an asset class that may generate less return but has a lower correlation with your existing asset classes.

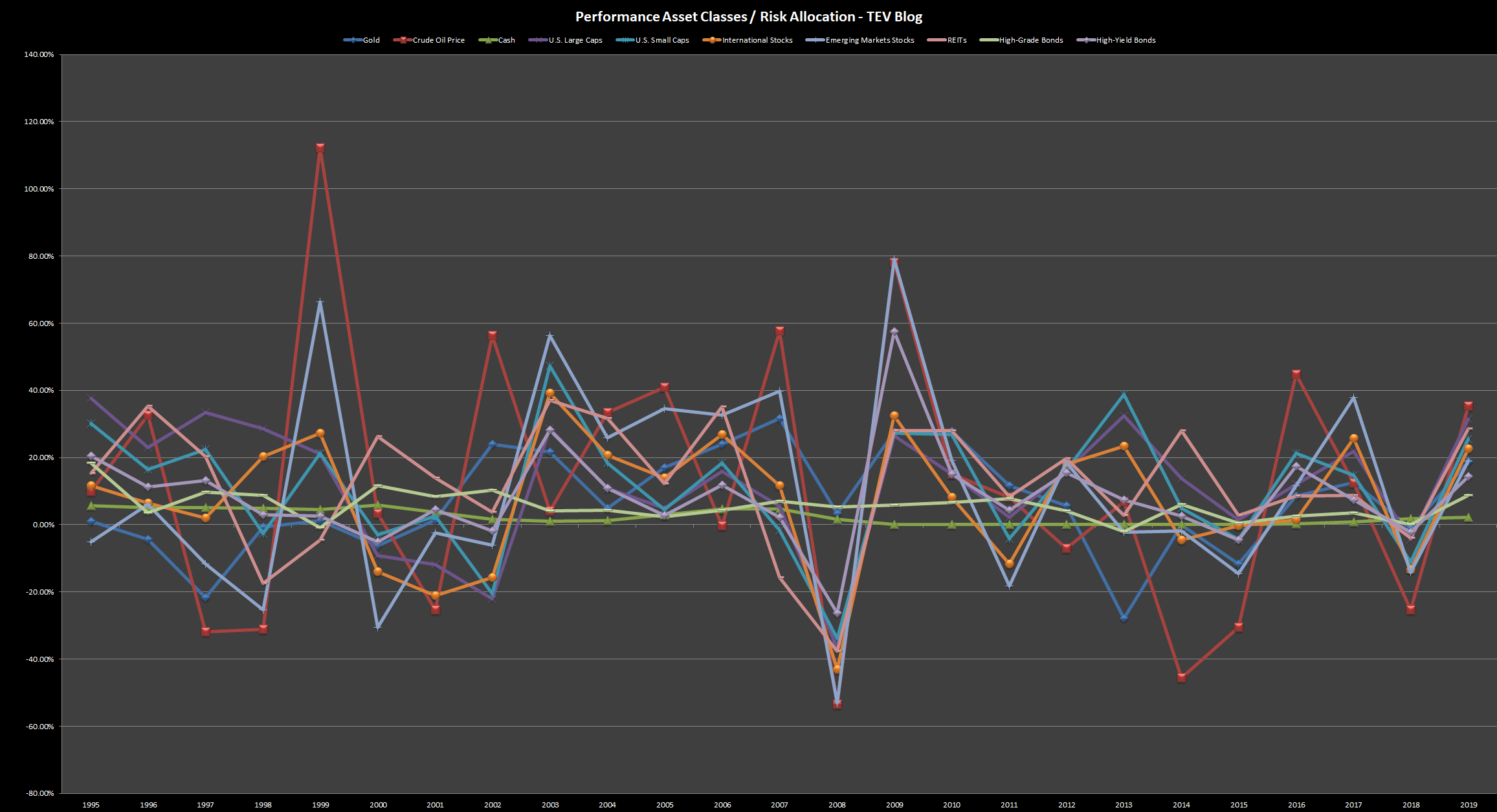

The correlation ratio tells you how strongly two companies correlate. For example, there is a strong correlation between the price of gold and gold mining stocks. If the gold price rises, the price of gold mine shares will also rise.

The same applies to the oil price and companies active in the value chain of oil products. As you can see in the chart below, many asset classes correlate. Only cash and high-grade bonds have a weak correlation to most asset classes.

On the other hand, cash and high-grade bonds have historically delivered a relatively low return. Due to the low correlation, however, it could well make sense to consider these asset classes in your asset management.

With this approach, you can reduce your opportunity costs enormously. You don’t have to deal with all kinds of income streams, but with the one, you know best.

Does the intrinsic value formula work?

So is investing that easy? One can probably say that this is the case in theory but:

Charlie Munger:

That practice of ours, which is so simple, is not widely copied. I do not know why.

Now it’s copied among the Berkshire Shareholders. I mean, all you people have learned it, but it’s not the standard in investment management, even at great universities and other intellectual institutions.

Very interesting question… if we’re right, why are so many imminent places so wrong?

Even Warren Buffett cannot quite understand why not all companies or investors think this way.

Warren Buffett:

[There are] several possible answers to that question…

The attitude, though, I mean, if somebody shows us a business, the first thing goes through our head is: would we rather own this business more than Coca-Cola? Would we rather own it more than Gillette? […]

It’s crazy not to compare it to things that you’re very certain of. There are very few businesses that we’ll find that we’re certain of the future about as companies such as that.

And therefore we want companies where the certainty gets close to that and then we’ll want to figure that we’re better off than just buying more of those.

If every management before they bought a business in some unrelated field that they might not have even heard of, you know, more than a short time before that’s being promoted to them, but they said, is this better than buying in our own stock you know is this better than even buying you know buying Coca-Cola stock or something that, there’d be a lot fewer deals done.

But they don’t. They tend not to measure against what we regard as close to perfection as we can get.

I think one problem is the different approach of many investors. Warren Buffett has already mentioned one difference: the difference between investor and speculator. Many conservative investors take an approach like Berkshire Hathaway and try to find undervalued companies.

But there are also the greedy ones who want a high return quickly. The problem is that many investors do not understand that it takes an extremely long time before an investment strategy like Warren Buffett’s pays off.

As you can see below, the wealth of Warren Buffett is the best example. Warren Buffett made most of his fortune when he was over 50 years old:

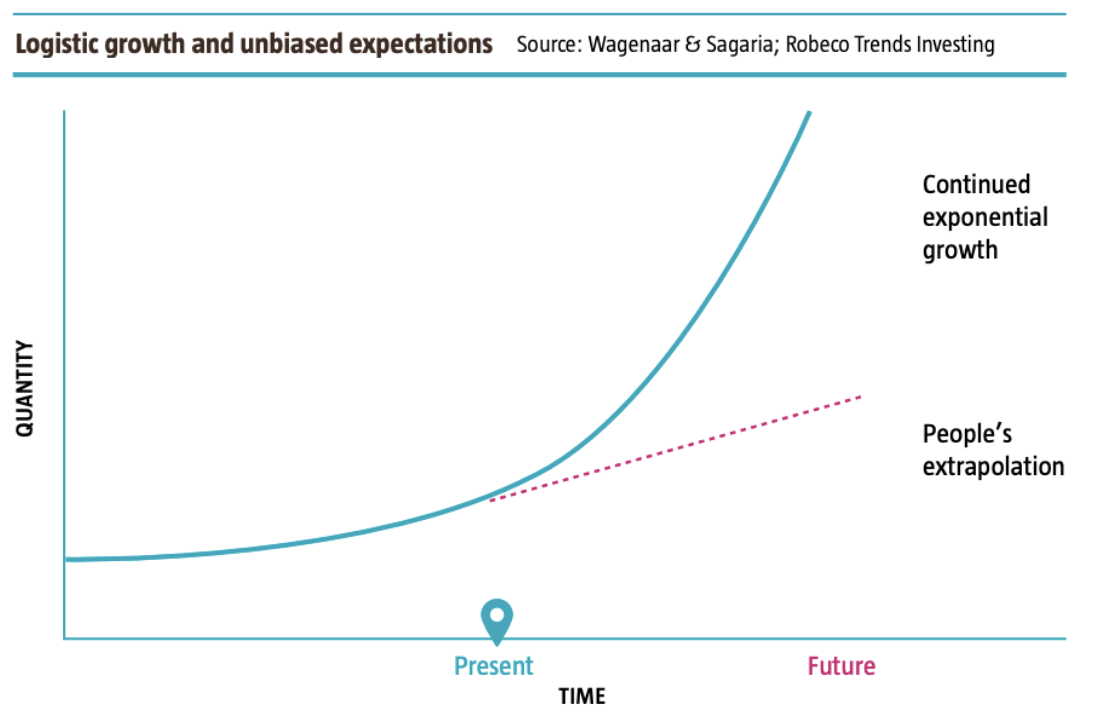

Many people lack the imagination that patience and stubborn investment can generate high returns over many decades. Dividends, which can be very low in the beginning, can grow into a veritable avalanche over the years due to the compound interest effect.

The reason why many investors lose patience too quickly is that they cannot imagine exponential growth, but can only project past growth linearly into the future.

Was it easier in the good old days?

Charlie Munger addressed another interesting aspect. In his view, it used to be much easier to find undervalued stocks.

Charlie Munger:

Well, I will say that the concept of intrinsic value used to be a lot easier because there were all kinds of stocks that were selling for 50 percent or less of the amount at which you could have easily liquidated the whole corporation if you owned it.

Indeed in the history of Berkshire Hathaway, we bought things at 20 percent of their liquidating value. And in the old days, the Ben Graham followers could run their Geiger counters over corporate America, and they could spill out a few things.

Well, no matter how bad the management, if you’re buying it for fifty percent of asset value or thirty percent or so, you have a lot going for you.

And as the world is wised up and as stocks have behaved so well for people that stocks generally have gone to higher and higher prices.

That game gets much harder: now to find something at a discount from intrinsic value. Those simple systems ordinarily don’t work. You’ve got to get into Warren’s kind of thinking, and that is a lot harder.

I think Charlie Munger had a valid point. The situation has even worsened. We have a much better information situation today. The Internet enables us to record information in real-time. It is, therefore, difficult, especially as a private investor, to have more details than the broader market. So you can assume that everything is now priced in the share price before you take a look at a company.

Another question is whether this price can still differ from the intrinsic value. Warren Buffett still thinks it’s possible. He is right when he says that in retrospect, everything always seems easier than it was.

Warren Buffett:

Charlie talks about liquidity value not talking about closing up the enterprise. He’s talking about what somebody else would pay for that stream of cash too.

I would also agree that almost at any time over the last 40 years that we’ve been up on a podium, we would have said it was much harder in the past.

Warren Buffett, on the other hand, is tormented by entirely different problems, namely the sheer size of Berkshire Hathaway.

Warren Buffett:

But it is harder now. It’s way harder…. The part of it being harder now too is the amount of capital we run. If we were running a hundred thousand dollars, our prospects for returns would be … considerably better than they are running Berkshire.

It’s just; it’s very simple. Our universe of possible ideas would expand by a huge factor.

We are looking at things today that by their nature a lot of people are looking at. And there were times in the past when we were looking at things that very few people were looking at.

But there were other times in the past when we were looking at things where the whole world was just looking at kind of crazy and that that’s a decided help.

However, this is not a problem that you have as a private investor, so you should not worry about such issues. I also believe that there will be undervalued stocks as long as there are human investors in the stock markets. As long as this is the case, the daily emotions will determine the development of the share prices.

Accordingly, there will continue to be opportunities for shareholders to stubbornly invest in excellent companies and benefit from their business development over the long term. The art is just to find these companies. This was the case in the past and still applies today.

Interesting article, thank you!

I wonder – which Berkshire Hathaway Annual meeting was this taken from – which year was this?

Many thanks for coming by ethan!

Unfortunately, I could not verify the year of the meeting. Nevertheless, it must have been in the late 1990s, perhaps in 1997 or 1998.

All the best,

TEV