The Leggett & Platt stock has been on my watchlist for a very long time. In February, I wrote an article for Seeking Alpha entitled “Leggett & Platt Is Not Necessarily A Buy Right Now”. Well, and then came the coronavirus, and it shook up the stock markets. Like many other investors, I took this opportunity and invested massively in the stock markets. At that time, I also bought shares of Leggett & Platt. And so I wrote another piece for Seeking Alpha. This time the title was: “Leggett & Platt: From A ‘Not Really Attractive’ Rating To A Very Good Buying Opportunity”. And oh boy, the Leggett & Platt stock was a great buy. But the question is whether this is still the case, which is exactly what I would like to discuss in the article.

Understanding my investment approach with Leggett & Platt

With the Leggett & Platt stock, you can easily understand the essence of most of my investment decisions. From my perspective, the company was always a company worth investing in, but it was always too expensive.

I was right here because it was the right decision to wait and invest in other companies while having Leggett & Platt only on my watchlist.

You can see this well from the performance of the stock after my two articles on Seeking Alpha. The stock is still trading below the value it had at the time of my February article. But if we look from the moment of my purchase, we see share price gains of over 55 percent.

I always say that there is no point in timing the market. Of course, I didn’t see the crash coming. But I already look at the fundamental or intrinsic value of stocks when I make my investments. And if I’m not satisfied, I don’t buy it. It is as simple as that. Often stocks come back to their average values. I wait for that moment and have a lot of patience. And when the time comes, I get greedy 🙂 .

About Leggett Platt

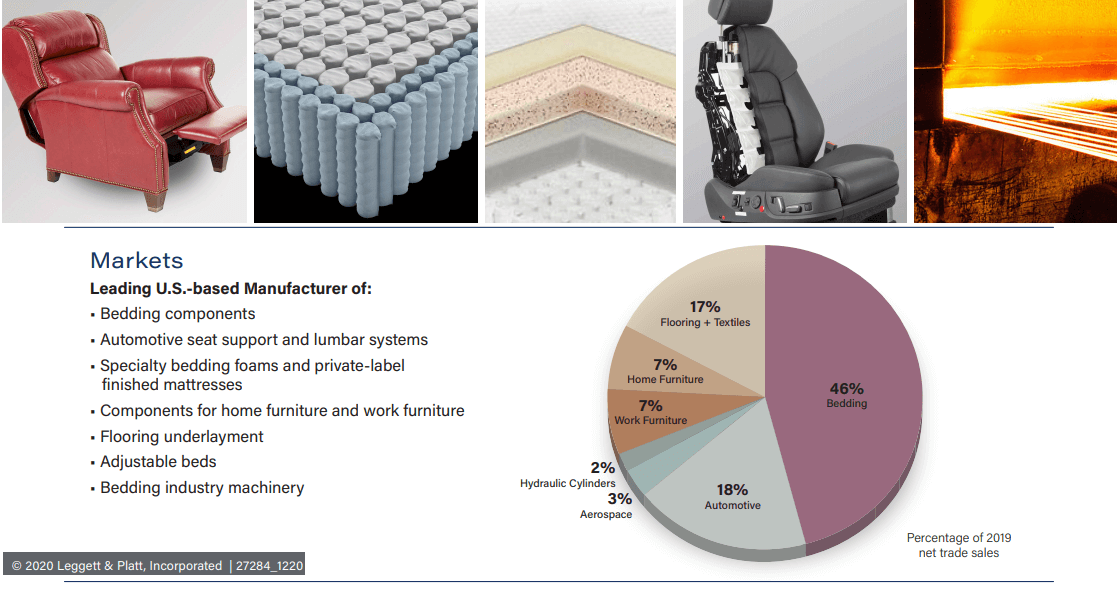

The company is a worldwide leading manufacturer of components for home and office furniture, beds, and adjustable bedsteads. It was founded in 1883 and is headquartered in Carthage, USA. Leggett & Platt is thus a leading company in a value chain for products that we humans have used for centuries and will probably continue to use for the next 100 years. These are exactly the companies I am looking for. Boring but important and well established in the industry they operate in.

Please keep in mind that Leggett & Platt is mainly active on the B2B level and therefore does not sell its products to the consumer but to other manufacturers. The following overview gives you a good idea of Leggett & Platt and its business.

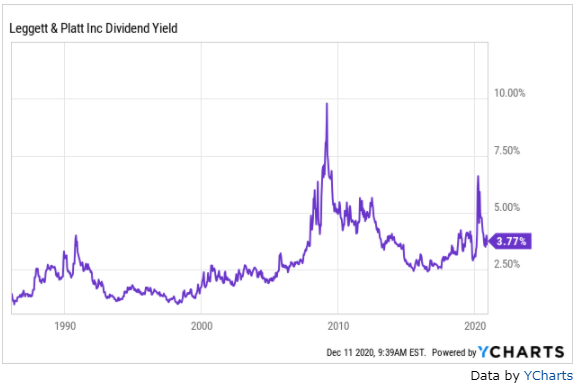

The Leggett & Platt dividend is not so attractive anymore

Unfortunately, the dividend has become less attractive with the rise in the share price. As a result, the dividend yield is no longer above average but rather within the historical average. The dividend scoreboard is also less attractive than months ago.

If you don’t want to miss any ex-dividend dates of the Leggett & Platt stock, I highly recommend my weekly ex-dividend calendar on the TEV blog.

Historical dividend yields

So you can already see that the current dividend yield is within historical limits. When the share fell, the yield was much higher, and the share was, therefore, more interesting. Nevertheless, the return is still not so bad at just under 4 percent. It is more than twice as high as the current yield of the S&P 500, which is currently around 1.6 percent.

Dividend scoreboard

A look at the Dividend Scoreboard also reveals light and shadow. The dividend scoreboard looks as follows:

- Dividend yield: 3.76 percent

- Years of dividend growth: 49 percent

- Payout ratio (profit): 61.29 percent / 91.3 percent

- Payout ratio (cash flow): 38.9 percent

- 1-year growth rate: 1.27 percent

- 3-year growth rate: 5.64 percent

- 5-year growth rate: 5.31 percent.

- 10-year yield on cost: 7.13 percent.

What I like is the continuity. The company has increased its dividend for 49 years. That is an impressive figure. Thus, Leggett & Platt is a dividend aristocrat that has increased the dividend every year for more than 25 years. Less nice is the partly quite high payout ratio.

During the COVID-19 crisis, it almost looked as if Leggett & Platt would not be able to pay the dividend. I hope that it will stabilize again and return to its old values. Then there will also be more leeway again to increase the dividend somewhat more strongly. But for now, I expect increases only in the low single-digit percentage range.

CEO Karl Glassman’s statement is encouraging. In the 3Q telephone conference, he said:

As we also reported yesterday, our Board of Directors declared a $0.40 per share fourth quarter dividend. At an annual dividend of $1.60 per share, we have increased our annual dividend for 49 consecutive years. We remain committed to our position as a Dividend Aristocrat.

So let’s hope that business development will lead to further increases.

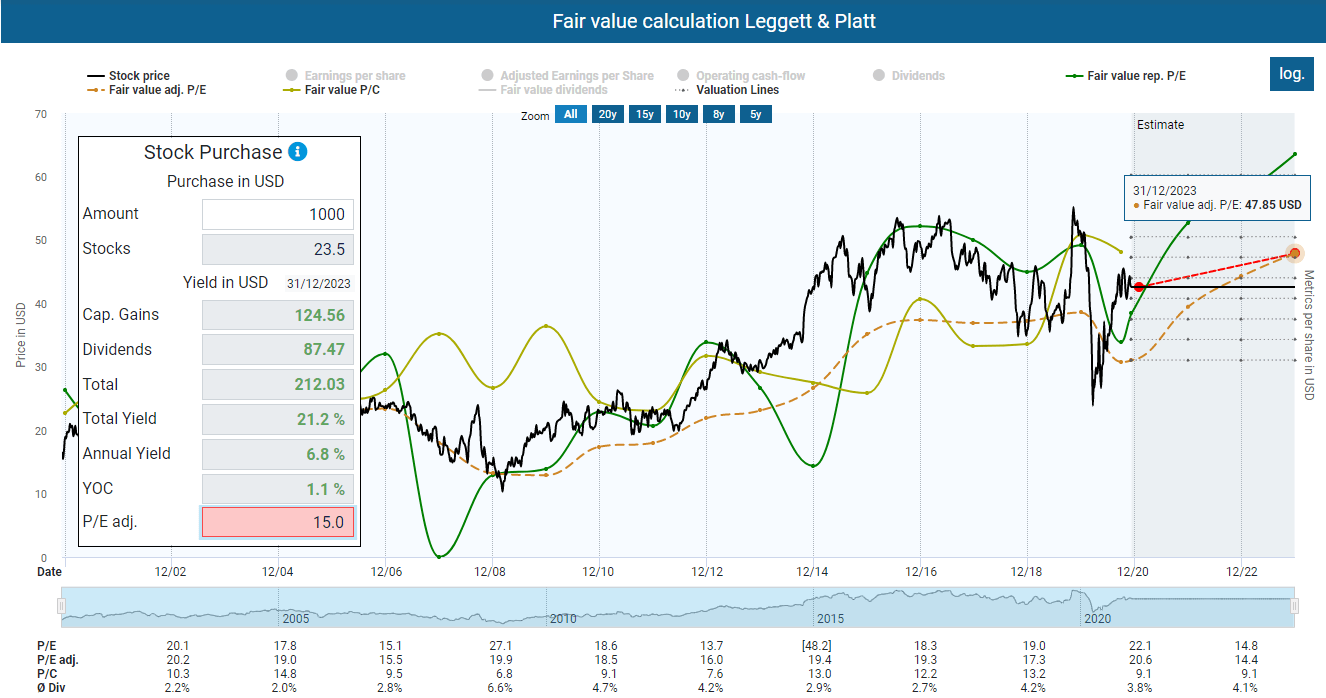

Leggett & Platt fair value

With the share price increases, the Leggett & Platt share is currently overvalued. I have based this calculation on a fair value with an adjusted P/E ratio of 15. However, in the chart below, we also see that, based on expected earnings and an adjusted P/E ratio, the share has a potential total return of at least 21 percent by 2023. The company may no longer be quite attractive, but it is not so overvalued that it seems unreasonable to hold on to it.

Conclusion

Leggett & Platt is no longer as attractive as when I bought it. This is mainly due to the share price increases, less to the fundamental outlook. I could, of course, sell my shares with a double-digit profit after only a few months.

But what would this move bring me? I want to invest my capital in companies. Thus, I would need another company to invest with a better perspective than Leggett & Platt. But I could buy this other company already with my cash reserves. I would also have to pay taxes on the profits and selling fees. So I prefer to keep the shares and enjoy my yield on cost of about 7 percent.

I have already described the reasons for selling shares in detail in an article. In the end, none of the reasons mentioned apply to Leggett & Platt. You can read the article on when to sell stocks by clicking here.

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

That said, feel free to let us know if I have overlooked an attractive stock or you know of a stock that is particularly attractive and where the ex-dividend date is coming up.

Is a stock here attractive for you? If so, let the community also know and write a comment.

You can also share this post with your favorite network: