I welcome you to a new episode of my Dividend Diary on the TEV Blog. Is there anything better in the financial world than a dividend income? Well, I guess not. And so, in January, I was again pleased to see a substantial increase in my dividends. I also used this month to add more shares and stocks to my portfolio. As always, in my monthly reports, I will give an update on my purchases. I document my monthly dividend income and the changes in my broadly diversified retirement portfolio. Here, I show you which companies have generated juicy cash flow for me each month and which stocks went into my basket. Besides, I analyze how the month has performed compared to the previous year. In the best case, my dividend income has increased.

As you know, I take care of my wealth management. To keep things simple, I have built three pillars:

- Active income.

- Passive income.

- Conversion.

Dividends fall into the last two categories. They are passive because I no longer have to work to receive the payments. Furthermore, they also contribute to the conversion because I reinvest the dividends and thus increase my passive income through dividends for the future.

My monthly dividend income in January:

This month I have received payments from the following companies:

- Automatic Data Processing (5.77 EUR)

- Kimberly-Clark (9.36 EUR)

- Iron Mountain (14.05 EUR)

- PepsiCo (11.29 EUR)

- Altria (18.92 EUR)

- GlaxoSmithKline (18.17 EUR)

- Realty Income (3.41 EUR)

- Leggett & Platt (10.81 EUR)

- Cisco (10.35 EUR)

- Simon Property (5.43 EUR).

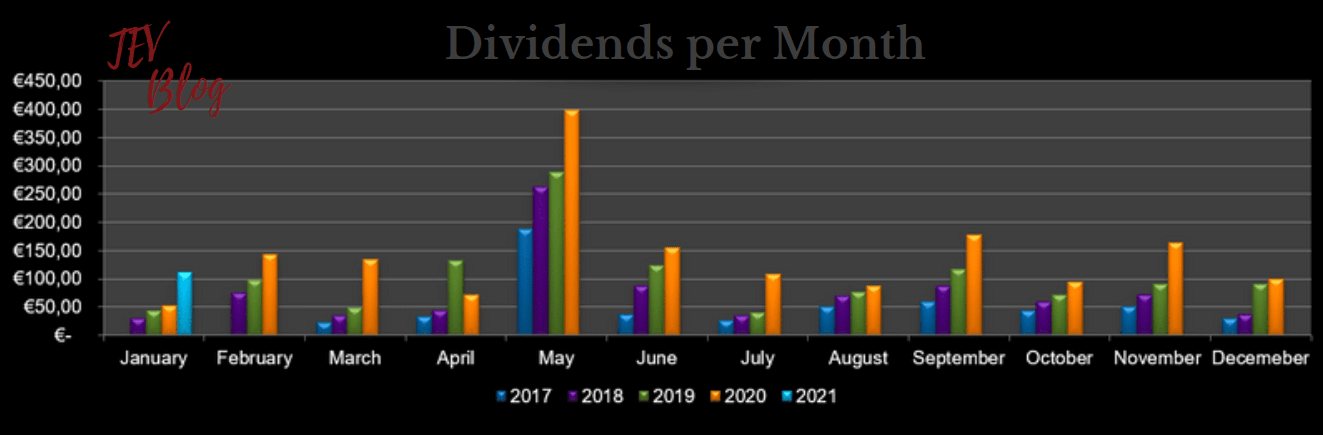

The total dividend income in January (after taxes) was: EUR 111.19 /appr. 135 USD

Dividend income check

Now let’s see how the performance was compared to the previous year. Last year, I received only EUR 52 in dividends in January, representing an increase of more than 100 percent.

Overall, this is how the year has started, and I look forward to the upcoming months. Will I set a new record with my “keep it slow and steady” investment approach? Well, probably. The overall development of my dividend income throughout the years is as follows:

Stock purchases for more dividend income

In December, I bought more shares of great companies so that the dividends will continue to rise in the future:

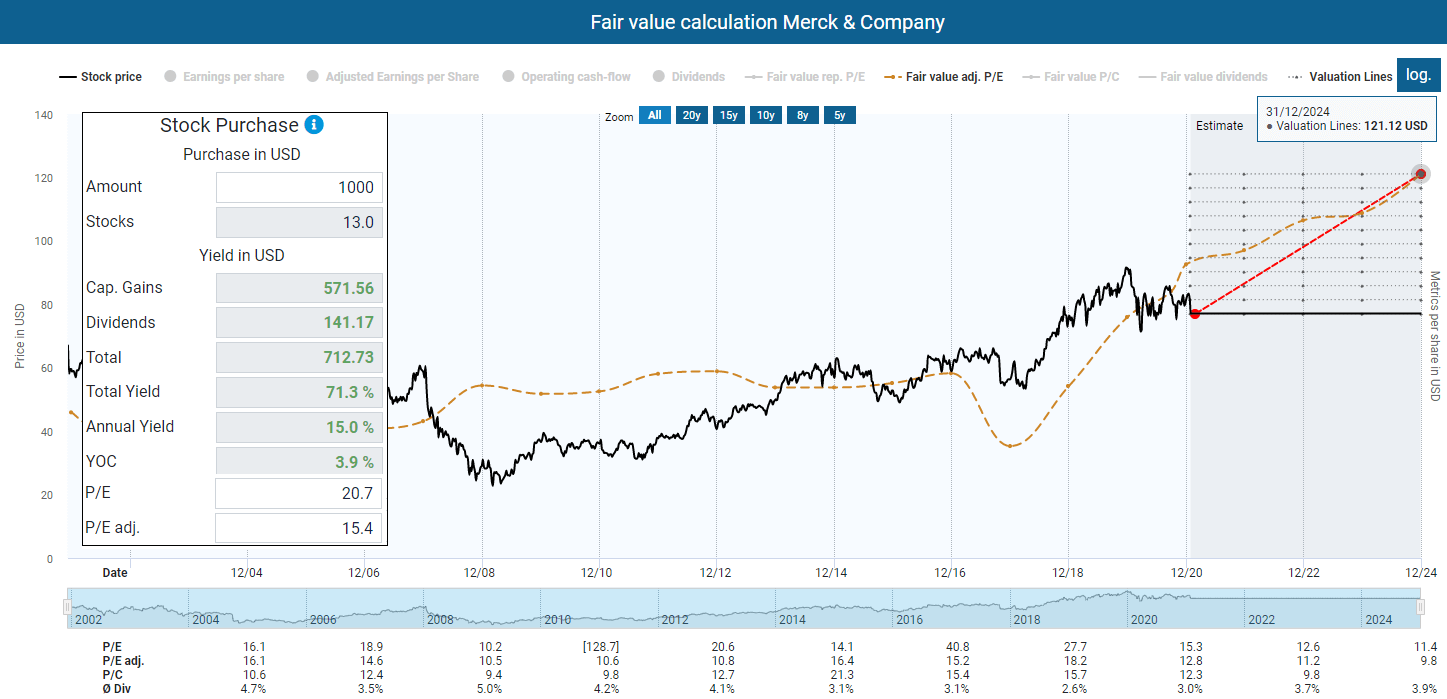

- Merck & Co. (20 shares)

- China Mobile (180 shares)

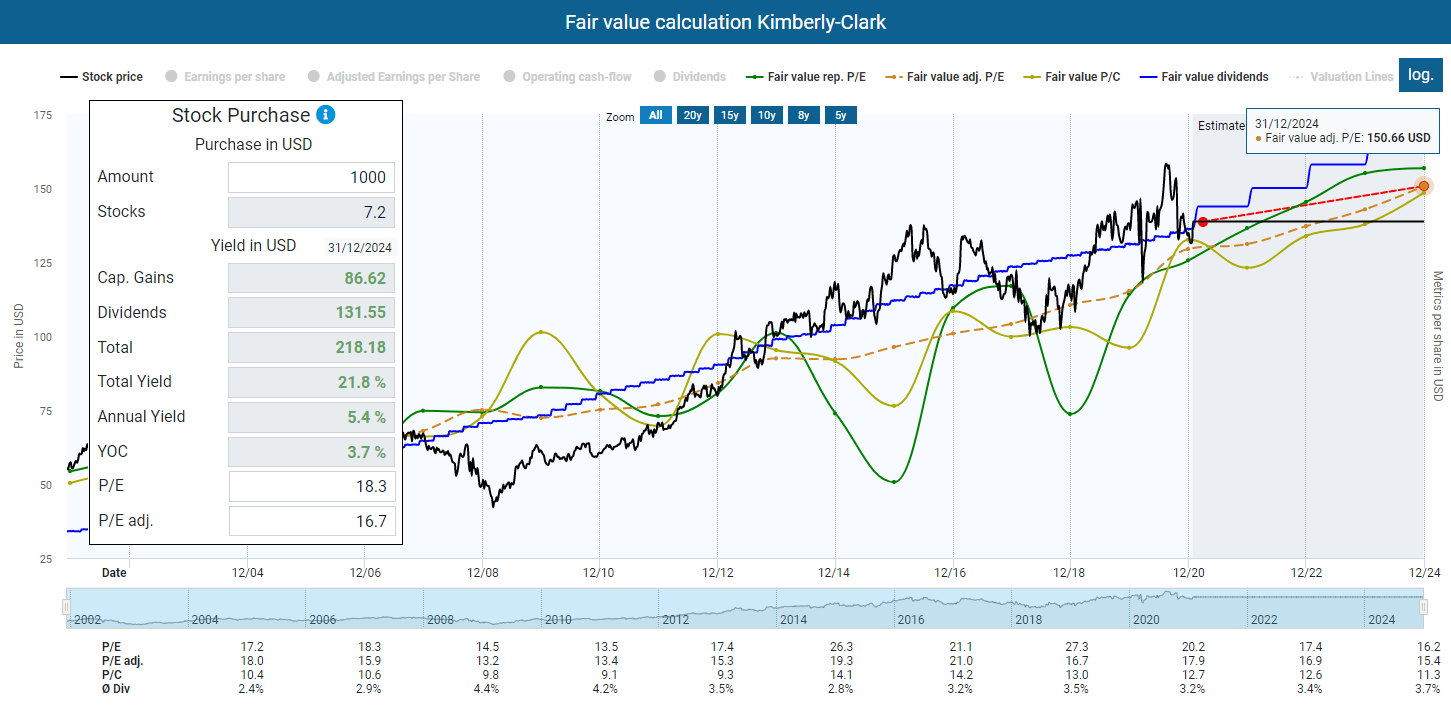

- Kimberly-Clark (7 shares)

- Swiss Re (19 shares).

In the following, I will briefly explain why I bought these companies. Please do not expect a fundamental analysis. I will only mention some aspects per company that might be of interest to the readers. Maybe you will find inspiration for your investment. In case you disagree, feel free to write your opinion about my purchases in the comments.

General thoughts – the market goes crazy!

The year 2021 has already written some very crazy stories about stocks. We have seen some extremely brutal short squeezes. It is a drama of epic proportions. Many small investors coordinating over the Internet are bringing institutional investors who were short on certain companies to their knees. It’s crazy, and I haven’t formed a final opinion about it yet. What is clear is that it is a circus, and I have no intention of participating in it.

Do I sympathize with all the soldiers of fortune? To be honest, a little bit. Short sellers are an essential element in the stock markets. They dig deep and, at best, ferret out corruption and failure. The same risk hedging rules I always preach must also apply to short sellers. It’s simple. But short-sellers often exaggerate and are driven by greed. GameStop is a great example. More than 100 percent of the shares were shorted.

The naked short seller

How does something like that work? An investor borrows shares from person A and promises that he will give the shares back after one month. In the meantime, he sells the shares to person X. He thinks the price will go down so he can repurchase the stock cheaply in a month to give the shares back to A. At the same time, however, our little greed investor borrows more shares from C (sells them to Y) and even from D (sells them to Z) and so on. But in the end, he has to return all the shares to person A, person B, and person C. And, naked as he is because he sold all the shares, he has to get those shares on the open market. It’s a potentially bottomless pit. Anyone who is that greedy is taking an enormous risk.

A revolution eats its children

However, Robinhood had stopped the madness and severely restricted trading (or better, buying) individual companies, which comes with a very bitter taste. Robinhood has thus single-handedly shifted the market rules in favor of the short-sellers, which I view very, very critically. The company has left its role and, in my view, taken sides. Robinhood has thus violated its ideals.

However, there are apparently regulatory reasons for this move. In a blog post, Robinhood said:

“As a brokerage firm, we have many financial requirements, including SEC net capital obligations and clearinghouse deposits […]. Some of these requirements fluctuate based on volatility in the markets and can be substantial in the current environment. These requirements exist to protect investors and the markets and we take our responsibilities to comply with them seriously, including through the measures we have taken today.”

Right now, Robinhood is looking to raise fresh capital to meet its obligations to the authorities to allow investors to trade stocks such as GameStop again. So the mania is likely to continue.

What’s next?

Stories like this always make me think of Nassim Taleb, author of the book “The Black Swan”. When violent events hit complex systems, the consequences can be nasty and possibly unforeseeable for many (what happens when all the big banks have financed short-sellers or have initiated extreme short positions themselves?).

So the question is, what will remain after this story ends? Well, obviously frustrated private investors and maybe a reinforced image of those (big banks, “smart” money, big money) up there and us (poor money, dumb money, retail investors) down here, which is not healthy for a society. The private investors have used their leverage, just as the short-sellers used their leverage with all the capital and the publications of studies and market reports.

What’s next? This should be extremely uncertain. We see regulatory intervention. Will they be enough to stop this madness? It depends on how entrenched groups/phenomena like “r/WallStreetBets” are. If it is a grassroots movement, then I can imagine that we are only at the beginning. The internet offers outstanding coordination opportunities, and even if small investors as individuals have little capital, their mass is enormous.

Anyway, I’m sticking with my approach, and so far, I’m doing quite well with it (I’m not a millionaire yet, though). I invest stubbornly and steadily, and I don’t get rattled by volatility. However, if my Tanger shares increase tenfold or twentyfold, then I’ll think about selling 😉

What did I buy?

So back to business as usual. This week I bought shares in four companies.

I have added 20 Merck & Co. shares to my broadly diversified retirement portfolio. The company has been on my watchlist for a long time. It is one of the largest pharmaceutical companies in the world. In my view, the pharmaceutical sector is one of the few sectors that is still reasonably valued or even undervalued. You can also see that with Merck & Co. With an adjusted P/E ratio of around 15, the expected earnings in 2024 offer a potential upside of 15 percent per year. The reason for this is an expected increase in profits over the next few years.

Besides that, I like the balance sheet of the company. Merck & Co. has a comfortable debt ratio of 40 percent and sits on a mountain of treasury stock worth almost USD 57 billion. The dividend yield is more than three percent, and the payout ratio is below 50 percent. No further questions 🙂

Uhhwee, I gambled now after all? Maybe a little, a tiny bit. I bought my first China Mobile shares. The shares have taken an extreme hit due to the US sanctions, but they are an absolute bargain with a dividend yield of over 8 percent and an adjusted P/E ratio of far below 10. I have absolutely taken my risk compliance into account here and only invested a minimal amount. Unlike with the other companies, I am not planning any subsequent purchases. Otherwise, I invest in the Asian market/emerging markets through an ETF. The consideration with China Mobile was the following: The sanctions have no impact on China Mobile’s business. It is the same as it was a few years ago, only much cheaper. So the China Mobile purchase was a one-shot opportunity, and it is open to me how I will deal with the shares in the future. If the stock rises significantly in the next few months, I would also consider selling.

Also new in my portfolio are 19 shares of Swiss Re. Swiss Re is the world’s second-largest reinsurer behind Germany’s Munich Re. The dividend yield is relatively high at just under 8 percent. The company has not fully recovered from the COVID-19 crash because the coronavirus has weighed enormously on the company. Some fear a dividend cut, but cash flow covers the payout for now. Even if the dividend is cut, there should still be an attractive yield.

Furthermore, I expect the situation to improve again in the next few years. Swiss Re is, therefore, another long-term building block in my retirement portfolio. That’s where the shares should stay and do their work.

Also, I increased my existing stake in Kimberly-Clark with the purchase of 7 shares. The company exceeded expectations with its latest quarterly results, raised its dividend by 6.5 percent, and announced a further share buyback program. The shares are currently not too overpriced, with an adjusted P/E ratio of 18 and a dividend yield above 3 percent. The business is defensive, and management knows what it is doing. According to the company, 25 percent of all people in the world use a company product (such as Huggies, Kleenex, and Scott) at least once a day.

Watchlist for January

Next month, there will be some additional purchases of shares. I am relatively flexible here. Either I buy new positions, or I increase my shares in existing investments.

The following companies are on my watchlist in particular:

- Microsoft (MSFT)

- Digital Turbine (APPS)

- Intel (INTC)

- Salesforce (CRM)

- Mayr-Melnhof Karton AG

- Bayer

- Hugo Boss

- Sysco (SYY)

- AT&T (T)

If you look at my report from last month, you will see that none of the companies I bought were on my watchlist. Why is that? Is the watchlist nonsense, and in the end, I only do what I want anyway? Yeah, a little bit. I don’t have a fixed system for my stock purchases, and that’s one thing I have to consider changing.

However, I have an extensive overview of many companies that I look at from time to time. The watchlist companies are mostly companies that I have currently examined particularly carefully, where substantial changes are imminent or which are in my focus for other reasons.

They are present to me in some form, which is why I put them on the list and perhaps monitor them a little more closely than other companies. But it often happens that I invest in different companies, after all. And so it happens that I buy other companies because it seems convenient at that moment.

Have you received dividends this month? What’s on your watchlist? Let me know and write it in the comments.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

Thank you for the wealth of information you are sharing. Actually I am 44 and starting with 10K euros with small monthly saving capacity. I was thinking about ‘swing trading stocks’ for some time to benefit from volatility and increase my capital. I am curious to know your opinion about trading.

Second, I would like to know more why you prefer dividend stocks. Any article link on your thoughts on both subjects would be very helpful.

Thanks a lot

Hi Bassem,

many thanks for coming by and leaving such nice words!

So first off, congratulations on wanting to manage your own wealth! 10k is a great amount that provides a comfortable basis to start the journey. It’s funny, I think everyone starts out with the wild stuff like “swing trading” etc. The motive “to increase my capital” sounds logical. But if it were so simple, why doesn’t everyone do it? I did the same back then (shorts on gold and gold mines for example). It ended up being a zero-sum game. It is paradoxical. We want the really complicated things right away before we have tried the simple.

And from my point of view (and this is just my opinion), here lies the key: in the simplicity of things. And that’s why I like dividends so much. With shares in companies, you become the (co)owner of a company. You could also start a company yourself. You could also build up a farm. In all these ventures, the purpose is for you to earn a living. With dividends, it’s very simple: you get something for your investment immediately. You don’t have to wait for the price to go up, you don’t have to find a fool who will buy the shares for more than you paid. The money comes and you don’t have to do anything.

Well, that doesn’t mean dividends don’t come with downsides (taxes, for example). It’s an old dispute about which is better. I also have growth stocks such as Apple, Facebook, Logitech, and Teamviewer in my portfolio. I’m sure there will be more to come. So it’s not black and white, and it always depends on the strategy you’re pursuing. I want cash flow without selling my company shares, so I invest heavily in those companies that give me cash flow via dividends. The overall performance may be poorer than if I invest in an ETF (statistically, hardly anyone manages to outperform the market). However, I sleep well with my approach. Wealth management is not a race or competition.

I like Bill Ackmann (I prefer to learn from people who have made it, rather than some gurus trying to sell me some trading courses). There are some great videos from Bill Ackmann on youtube about investing (here, for example). Videos/interviews with Warren Buffett and Charlie Munger are also legendary when it comes to value investing.

So I hope, this helps a little bit. All the best,

TEV

Hi TEV,

Thank you so much for this lengthy answer, much appreciated.

It took me a year now to build some culture and make the first steps 5 months ago. I watched Buffet, Munger, Dalio, Ackman, Lynch and found they have something in common but diverge in some aspects of their investment. I have also been listening to some famous traders like David Paul, Burton and others.

The whole domain is fascinating by its complexity and it is really difficult to draw a clear line between investment and gambling.

I have been following many ressources out there and found that I can rely on your stock recommendations with confidence, not disappointed yet. This blog became my main source of information, given especially the hard time I have with fundementals.

Stay assured your work is very useful and helping many.

I had been reflecting about the usefulness of swing trading for a while, I watched my portfolio P/L ‘swinging’ up and down and found that there is an opportunity. Off course it is impossible to time the market but I thought why not swing trade a pool of selected stocks with good fundementals or paying dividende.

Worst case is that my capital won’t be locked in shares with weak fundementals.

I guess it comes down also to the personal situation and risk tolerance.

In my case, I hold PhD in engineering, worked non stop simetimes double work, and 10K is the half of my wealth (the market penalizes my ID documents). With 44y, I feel like I am already broke. So I am very much open to risk as it couldn’t go much worse.

I neeed to stay a good family man though, so I guess I will swing trade from a diversified pool of stocks (degiro custody account, no short selling, no leverage). I will pick some stock from your recommendations and retirement portfolio.

Thanks again for your answer and for your precious work.

Bassem