Like every week, I want to show you some stocks that will go ex-dividend in the next days. I’ll also review a few companies that are currently in the focus of investors or that have an attractive fundamental valuation. Additionally, I’ll give you some insights into my retirement portfolio and share my thoughts and experiences about individual companies with you. Today I want to take a second look at Procter & Gamble and LTC Properties.

Why yields are a simple way to screen companies

Dividends are a great thing. Even in bad stock market times, they provide a juicy cash flow per month. If you want to benefit from dividend payments as quickly as possible, you must pay attention to the ex-dividend dates. This date is the day on which shares are traded without their subsequent dividend value. Only if you owned the stocks on this day are you entitled to receive the dividend.

Usually, there are always exciting dividend companies that are worth a second look. And the dividend yield is an excellent way to get an initial overview of companies that may be worth further due diligence. To help you get started, at the end of each week, I will publish the ex-dividend dates for the coming week of individual companies here in the TEV blog.

Why I handpick and double-check the ex-dividend dates

I have recently noticed that many databases do not indicate the respective numbers and dates correctly. Spontaneous dividend cuts, in particular, are only partially taken into account, or in some cases, not at all. As a result, the value of such overviews dwindles enormously.

Therefore, I’ve decided to select individual companies by hand and check the dates and dividend yields on the company websites, which means more work for me but increases the value of this section enormously, so it is worth it 🙂

Ex-dividend dates calendar for the third week of July

Pretty few companies are going ex-dividend this week. I am curious to see if there will be a week in which no company from my broadly diversified retirement portfolio is included. But with every week that passes, it becomes less likely, because I am broadly invested in the market. Sometimes I buy new companies, and sometimes I increase existing holdings. The only thing that matters is that cash flow and investments in outstanding companies grow 🙂 So, let’s not waste any time. As always, you’ll find some handpicked exciting ex-dividend dates below.

| Company | Payment Date | Yield | In my retirement portfolio |

|---|---|---|---|

| Monday, July 20, 2020 | |||

| Pioneer High Income Trust (PHT) | July 31, 2020 | 10.6% | NO |

| Tuesday, July 21, 2020 | |||

| Apache Corp. (APA) | August 21, 2020 | 0.7% | NO |

| Lowe's Companies (LOW) | August 05, 2020 | 1.5% | NO |

| Wednesday, July 22, 2020 | |||

| Argan Inc. (AGX) | July 31, 2020 | 2.2% | NO |

| CVS Health (CVS) | August 03, 2020 | 3.1% | NO |

| LTC Properties (LTC) | July 31, 2020 | 6.2% | NO |

| Thursday, July 23, 2020 | |||

| Gladstone Capital (GLAD) | July 31, 2020 | 10.5% | NO |

| Procter & Gamble Company (PG) | August 17, 2020 | 2.5% | YES |

| Williams-Sonoma Inc.(WSM) | August 28, 2020 | 2.3% | NO |

| Friday, July 24, 2020 | |||

| Royal Bank of Canada (RY) | August 24, 2020 | 5.3% | NO |

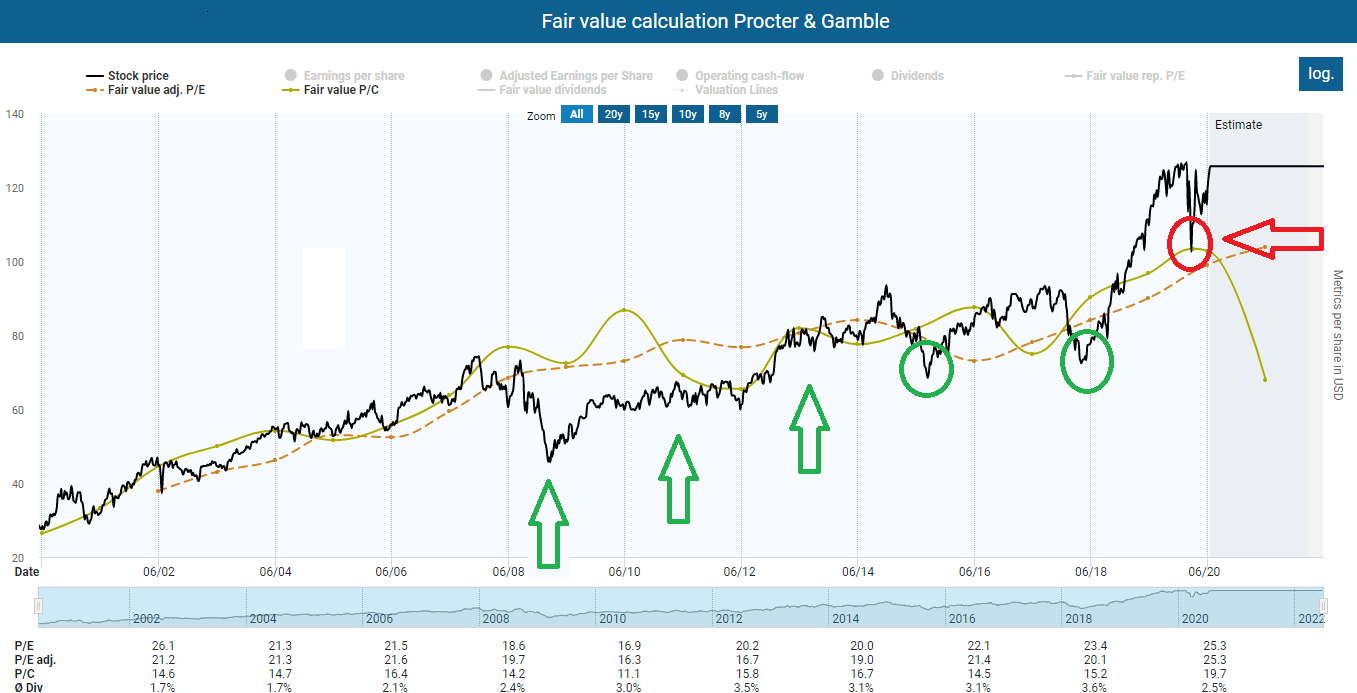

Procter & Gamble

This week, Procter & Gamble is the only company from my portfolio to go ex-dividend. The company has been dormant in my portfolio for many years. It must have been 2014 when I put the shares in the portfolio. I know for the old hands that’s not long, of course. But for me, it was one of the first stocks with which I seriously pursued an investment strategy that is oriented towards cash flow. Before that, I only invested here and there without a specific approach.

After my initial purchase, I bought the company again and again. Procter & Gamble is an excellent example of the fact that a buy & hold approach combined with regular share repurchases can be worthwhile. You can even boost your return if you are brave enough to buy when the price has just gone down. Of course, this doesn’t always work, and of course, market timing is an impossible thing to do, but with established and large companies like Procter & Gamble, such a strategy can sometimes pay off.

It is also clear that the company is currently extremely overvalued. Even in the COVID-19 crash, Procter & Gamble barely scratched at its fair valuation. Thus and as you can see below, not every dip is necessarily your friend.

Since I have always been a busy buyer when the price has fallen, my holding in P&G is already quite significant. Therefore I will not buy any more P&G shares for the time being.

LTC Properties

LTC Properties is a so-called REIT (real estate investment trust). The company invests in seniors housing and health care primarily through sale-leasebacks, mortgage financing, joint-ventures, construction financing, and structured finance solutions. It is one of the companies that pay a monthly dividend and is therefore particularly popular with investors who want to build up regular cash flow.

Business model

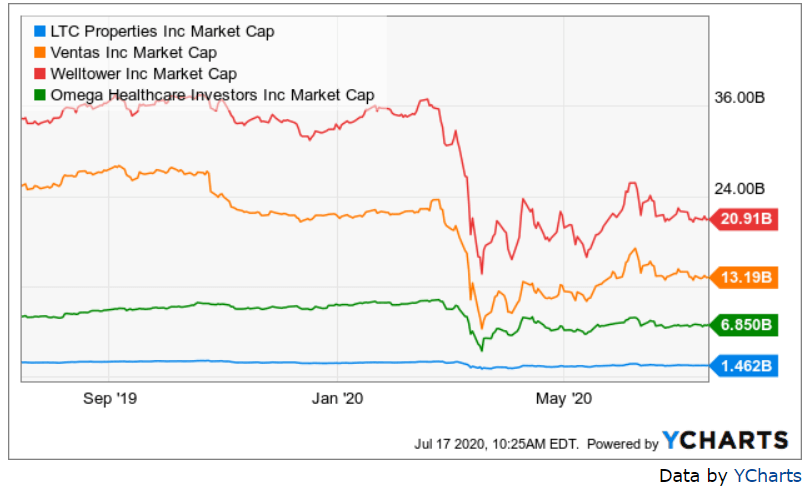

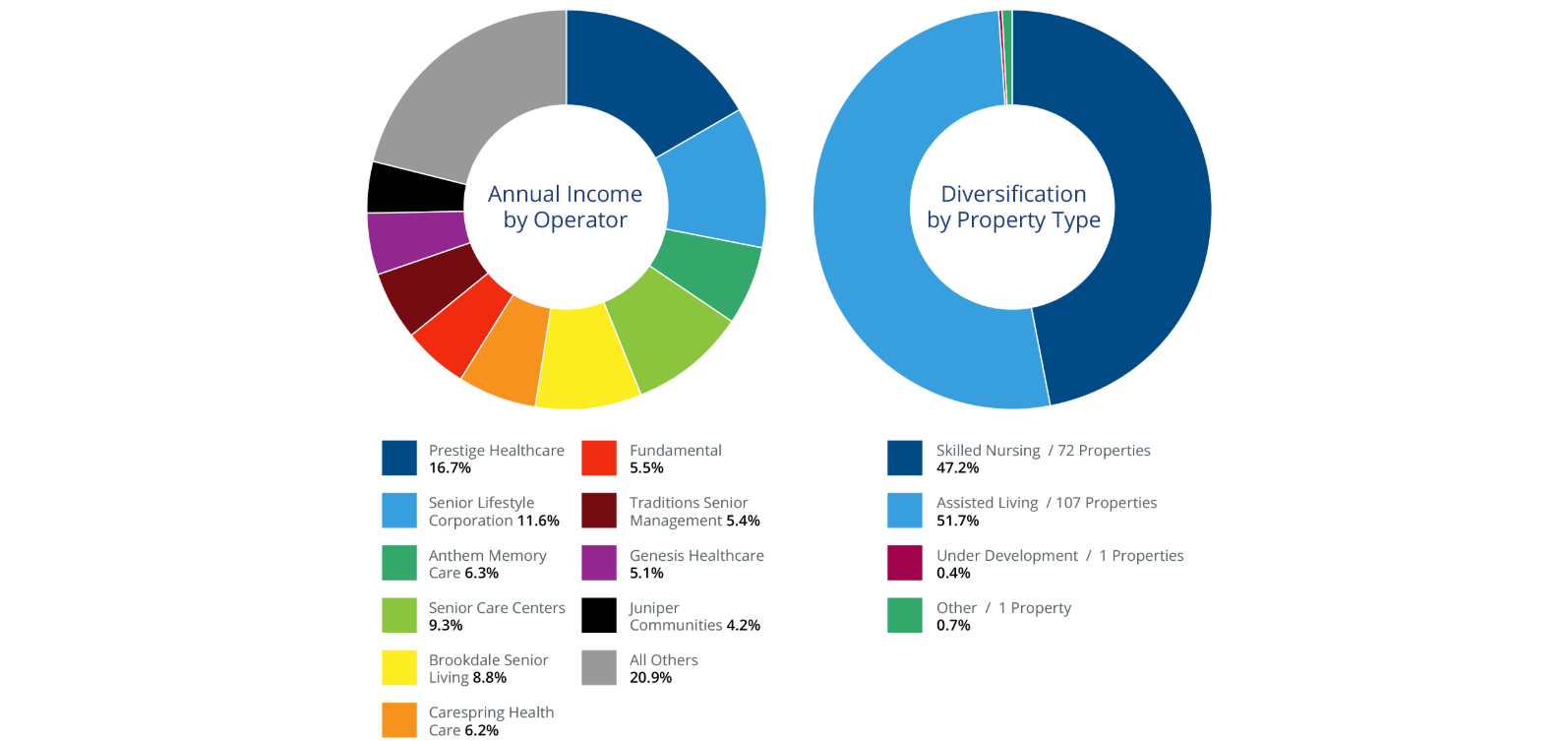

As stated above, LTC Properties focuses on senior housing and healthcare properties. The company generates income from private payments and public health programs. Although the company wants to expand its relationships with existing tenants, it also focuses on diversification and does not put all its eggs in one nest. The portfolio is comprised of approximately 50% of seniors housing and 50% skilled nursing facilities (SNF). Overall, the company is much smaller than other companies in the industry, such as Ventas, Welltower, or Omega Healthcare.

The main problem for me is the dependence on public payments since almost 70% of the SNF portfolio revenue comes from Medicaid and Medicare. I already have Omega Healthcare in my portfolio, whose revenues are also heavily dependent on public payments. Accordingly, I am already invested in this sector and not really looking to expand my holding.

Good growth and stable balance sheet

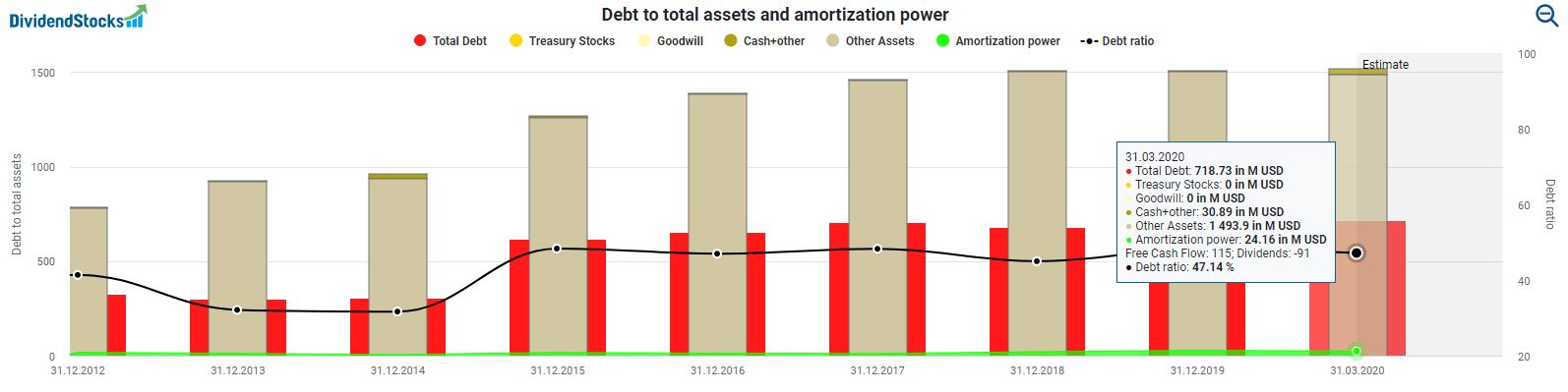

The dependence on governmental programs should not hide the fact that the company is quite successful. LTC Properties has increased its revenue from $69 million in 2008 to over $185 million in 2019. Fund from operations (FFO), the equivalent for earnings in the REIT-sector, increased from $1.91 per share to $3 per share over the same period.

Nevertheless, you have to be careful here, as the number of shares has also increased from 23 million to over 39 million over the same period. As a result, earnings/FFO were heavily diluted for shareholders. By issuing the new shares, the company was at least able to avoid building up a lot of debt, which has resulted in a relatively stable balance sheet (debt ratio is currently at 47 percent).

But is this strategy an advantage for investors? I have some doubts. This may save the company from paying interest, but in the long run, your profit as a shareholder will be diluted. Every time a company issues new shares, you have to share both the profits and the dividend with even more shareholders every year in the future.

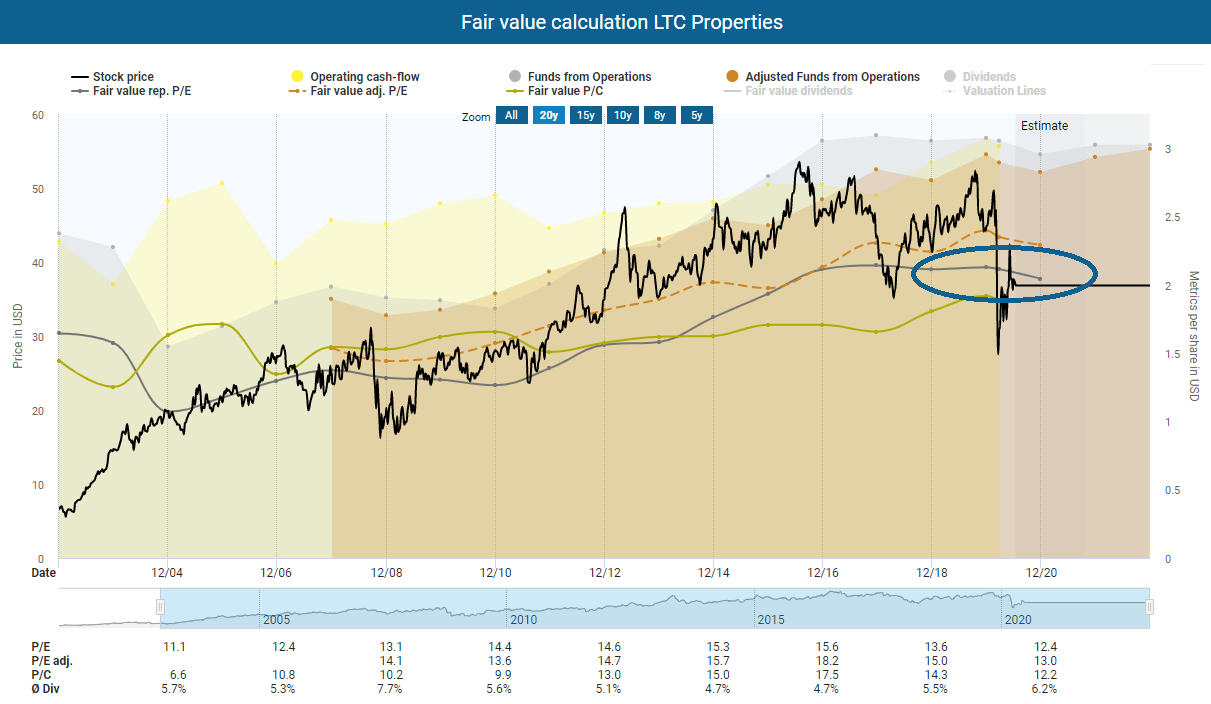

Fair value calculation LTC Properties

You can see from the following graphic why I am taking a closer look at LTC Properties this week. Due to the COVID-19 crash, you finally get the shares of the company at a fair price based on its historical cash flow and FFO. I mean, besides a short dip in 2017, 2011 was the last time the company was as undervalued as it is now.

However, the return to somewhat more reasonable valuations applies to the entire industry and can also be seen at Omega Healthcare, Ventas, and Welltower. The attractive valuation is therefore not necessarily a reason to buy at the moment.

The dividend scoreboard for LTC Properties

If we look at the dividend indicator, the results are as follows:

- Dividend Yield 6.2%

- Payout Ratio FFO: 77%

- 5 Year Growth Rate: 2.2%

- Last dividend increase: 2016

Conclusion

LTC Properties seems to be a well-managed company. It has a good balance sheet and has increased revenues and profits considerably in recent decades. It might make sense to explore a future investment and conduct thorough due diligence. In particular, I would like to know whether LTC has a competitive advantage over its major rivals or enjoys other benefits. But right now, I’m lacking the “story” to take an in-depth look at the company because I am already invested in this sector.

Who is overvalued who is undervalued?

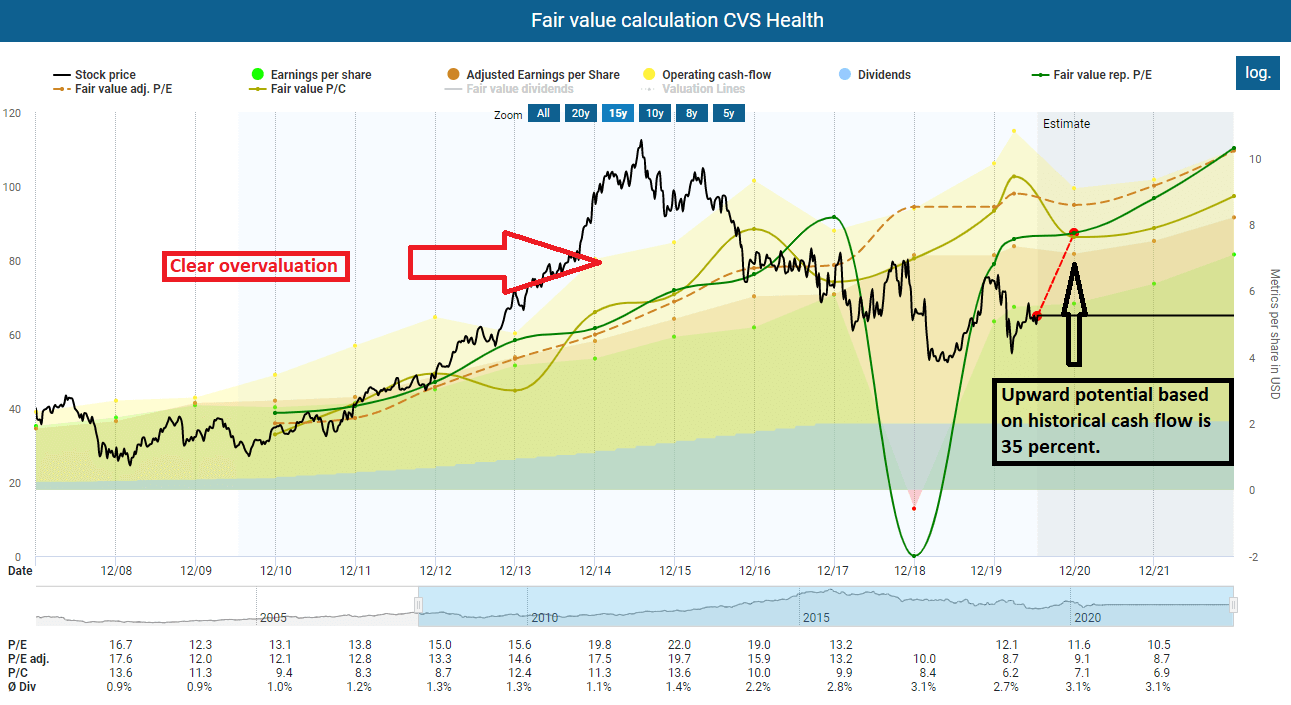

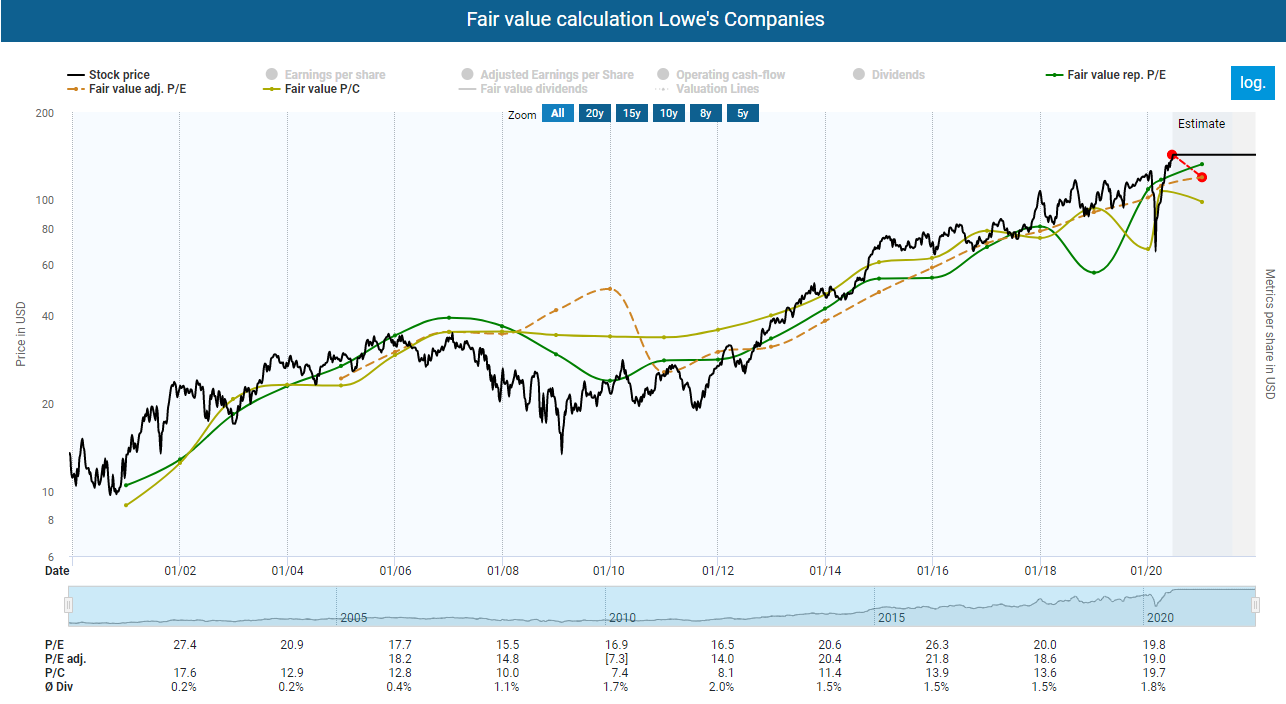

Finally, I have two more graphs for you concerning two more companies that are on my broader watchlist: One is strongly undervalued, the other overvalued (after almost doubling after the COVID-19 crash).

CVS Health ist undervalued

Lowe’s Companies is overvalued after a short crash during COVID-19

Time to do your due diligence

Has a company caught your interest? Attractive dividend yields should not be the only reason to buy shares of a company. Instead, you must carry out careful due diligence before every purchase. The Internet offers you excellent opportunities in this respect.

My analyses here on the TEV Blog are an excellent way to start (click here). You can also contact me here or ask the community in the comments if they can help with your due diligence.

Otherwise, I use tools like those from Dividendstocks.cash and Seeking Alpha to do further research. You can also find me and my analyses on these platforms. We also have a small but lovely group on Facebook that you can join. We share there only fundamental analyses of companies from various sources. So there is no spamming or anything like that.

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

That said, feel free to let us know if I have overlooked an attractive stock or you know of a stock that is particularly attractive and where the ex-dividend date is coming up.

Is a stock here attractive for you? If so, let the community also know and write a comment.

You can also share this post with your favorite network:

… [Trackback]

[…] Read More Infos here: theeuropeanview.com/procter-gamble-ltc-properties-and-more-are-going-ex-dividend-tev-blog/ […]

… [Trackback]

[…] Info to that Topic: theeuropeanview.com/procter-gamble-ltc-properties-and-more-are-going-ex-dividend-tev-blog/ […]