Welcome to the Salesforce stock analysis. In this article, I will check whether it is a buy or a sell based on a fundamental valuation model.

If you don’t want to miss any new articles or analysis, you can easily follow me on

or Twitter.

The price of a Salesforce stock has gained nearly 4,000 percent over the last 15 years. After a slight stagnation in 2019, the share price has started it turbo again in 2020 and is now above the previous all-time high of February 2020 despite a major COVID 19 setback.

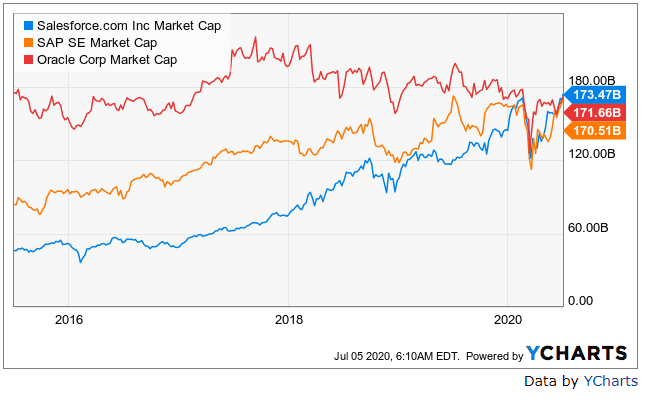

In terms of revenue, Salesforce is one of the fastest-growing companies in the world. Accordingly, the rising share price reflects the company’s success. The excessive share price gains have driven market capitalization so high that Salesforce, at $173 billion, now has a higher market capitalization than its main competitors SAP and Oracle.

What’s the secret to Salesforce’s rapid revenue growth? Will the company outperform its competitors, or has it already reached the limits of growth, making Salesforce stock hype and overvalued? No worries, we will speak about all this in this stock analysis.

Salesforce stock analysis – The business model

Salesforce is already bringing joy to nerds and fun fact junkies with its New York Stock Exchange ticker “CRM”, which is also the abbreviation for the core market in which the company operates (CRM = Customer Relationship Management). Speaking about CRM, Salesforce’s CRM business covers several market segments, as Salesforce has added more and more components, services, and products to its core competence through acquisitions. Instead of listing the individual segments, I’ll give you a better overview of the company’s business and success by showing you what exactly the company offers and then how it provides its products and services to customers.

CRM and Cloud – an undefeatable combination

As already mentioned, Salesforce is active in CRM, the so-called customer relationship management, or customer care. Why is customer care so important for companies? The answer to this question is strongly related to the acquisition of new customers and the marketing and advertising costs required for this, which are usually higher than the costs that a company has to spend on retaining existing customers. The reason for this is apparent. With existing customers, a company already has essential information, such as their name and address, and their behavior. With each additional product or service purchased, an even more detailed picture of the customer’s needs emerges, which puts the company in an increasingly better position to satisfy its customers’ needs and to tailor an offer to the specific customer’s requirements. The incentive for companies to retain existing customers is correspondingly strong.

However, the added value of customer care does not stop at existing customers. Companies can use the knowledge and data gained from their customer relationship management to acquire new customers, for example, by analyzing existing customers’ behavior and designing comparable offers for new customers. Likewise, a company can channel marketing costs more effectively if it knows which customers it needs to address. The so-called “conversion” of a potential customer interested in purchasing to an actual buying customer is much easier and cheaper. Accordingly, companies need to operate a functioning and efficient CRM. And this is precisely the secret of Salesforce’s success.

Salesforce – The secret to success

To understand Salesforce’s success, you need to take a step back in time to the early days of digitization. At the end of the last millennium, companies practiced CRM, marketing, and new customer acquisition essentially analog. Only individual software solutions brought relief and gradually shifted the CRM business to the digital world.

The problem with the software solutions that were widespread at the time, such as those offered by SAP, was their complexity: It had to be installed on a computer, could only be used there, and had to be managed there as well, for example, by adding updates. Similarly, the individual products were not very well adapted to the individual needs of customers, because small and large companies used the same program. Salesforce recognized the problem and, with CEO Marc Benioff, filled a huge gap in the market by moving to the cloud early on and, if necessary, buying the required expertise through acquisitions. Today, Salesforce offers most services and products through a single cloud, the Customer 360 Platform.

The individual services and products are primarily PaaS (Platform as a Service) and SaaS (Software as a Service) solutions based on cloud computing. As already explained in more detail in my Amazon analysis, the cloud computing market is multi-layered. In PaaS, Salesforce offers programmers and developers a complete software and programming environment alongside a hardware infrastructure. For example, Heroku, a company that Salesforce purchased in 2010 for just over $212 million, provides developers a cloud-based platform on which they can build their apps in any open source programming language.

The second significant segment in which Salesforce is active is SaaS. Here, the company sells cloud-based software solutions or apps it has developed itself directly to mainly commercial end-users (so-called B2B area=Business to Business). The nature of cloud solutions also explains why Salesforce is growing so rapidly in the CRM space.

Companies develop at different speeds, have to be different flexible, and have very different ideas about their customer care and marketing. Cloud solutions are something like the egg-laying wool-milk sow. They don’t have to be installed everywhere on every computer but are accessible from everywhere. The provider takes care of updates, further development, and (critical!) security, while the customers can concentrate fully on the growth of their business.

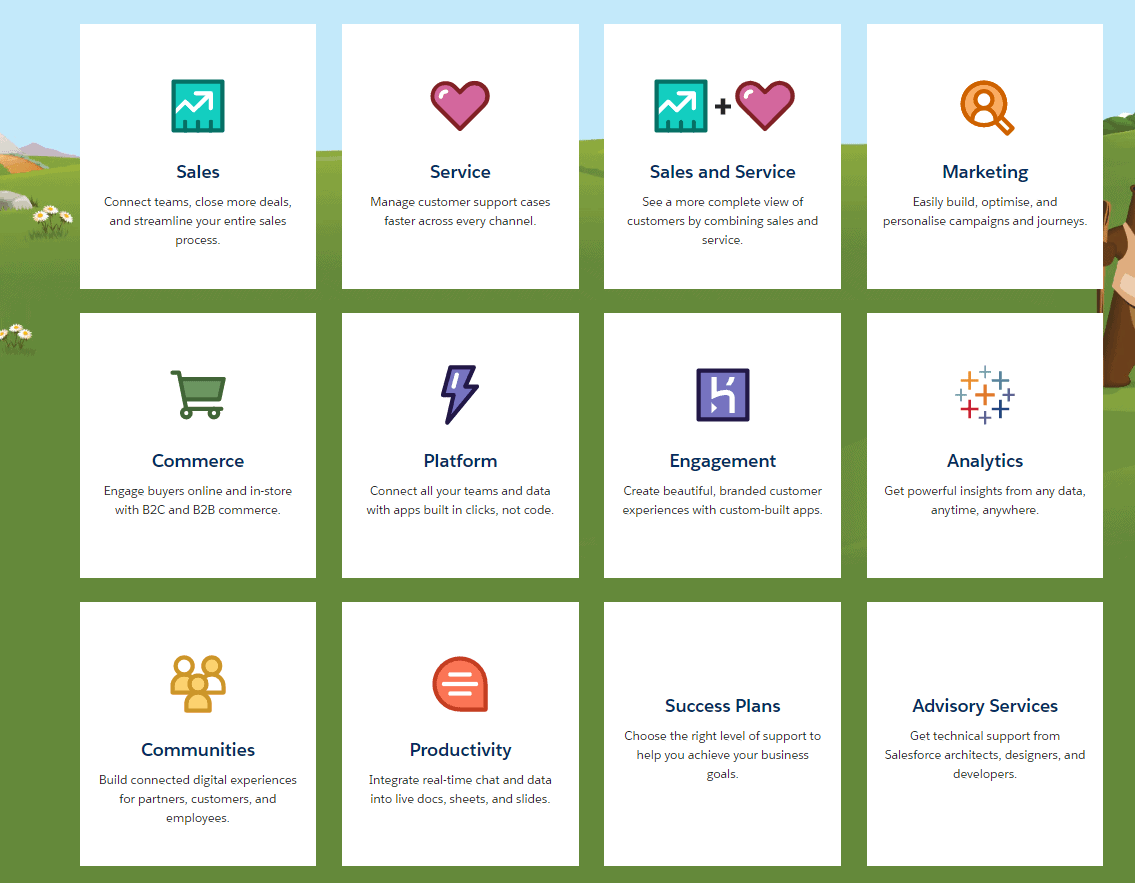

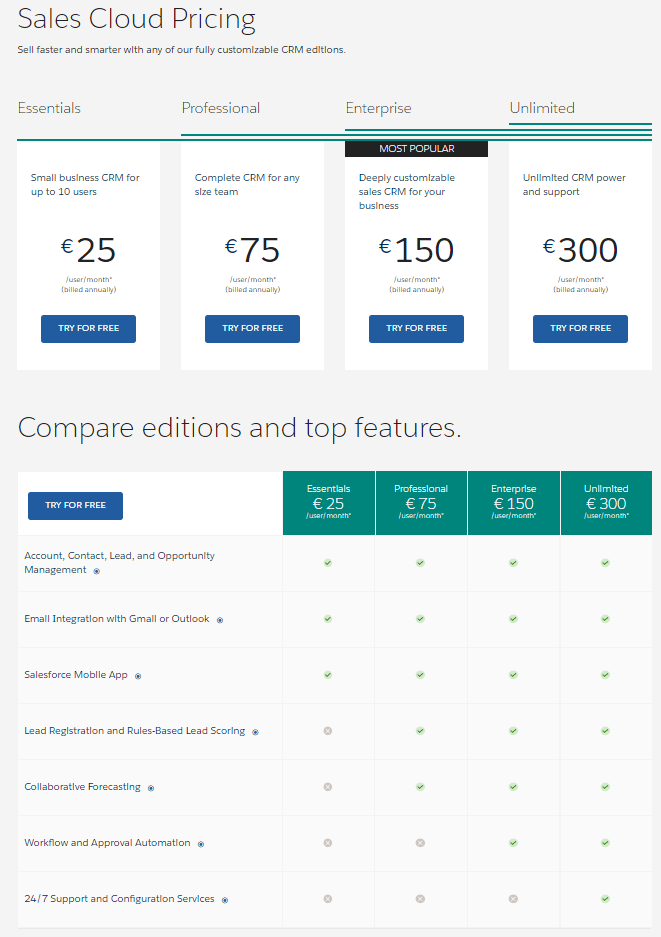

Besides, individual applications can be combined and expanded as desired. Customers can decide for themselves which product they need and to what extent. For example, Salesforce offers the modules Marketing (e-mail campaigns, SMS marketing, push notifications, evaluation functions, etc.), Customer Service (webchat, ratings, etc.) or Sales (contact management, task planner, invoicing, etc.). The pricing model of Salesforce’s Sales Cloud, which gives companies access to individual or entire customer data and orders, gives you a good picture of the different functionalities and the resulting price differences:

What the future holds

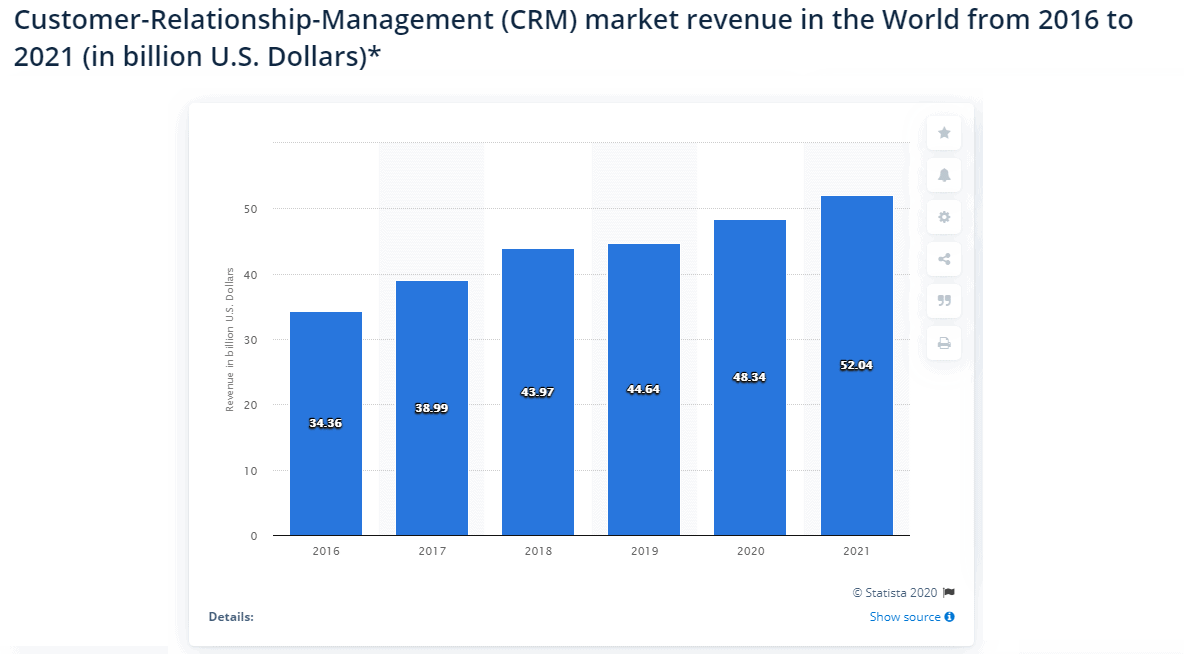

Salesforce is benefiting massively from the fact that its biggest competitor, SAP, has overslept the transition from software to cloud-based applications. As a result, Salesforce has slowly but surely become the absolute market leader. While the former market leader SAP has a market share of just 8 percent and is struggling with declining shares, Salesforce has been able to expand its share of the market for CRM products and services to over 18 percent, with a steady upward trend. Besides, the signs are good that growth will continue in the coming years. For example, the CRM market is one of the fastest-growing markets in the already enormously growing cloud computing market.

Geographically speaking, the company also still has considerable growth potential. I see the European market and Asia in particular as future growth drivers for the company. The European market volume is currently $9 billion and Salesforce’s market share of $1 billion generated in Europe is significantly smaller (approximately 11 percent) compared to the global market share of over 18 percent.

Salesforce is a revenue engine

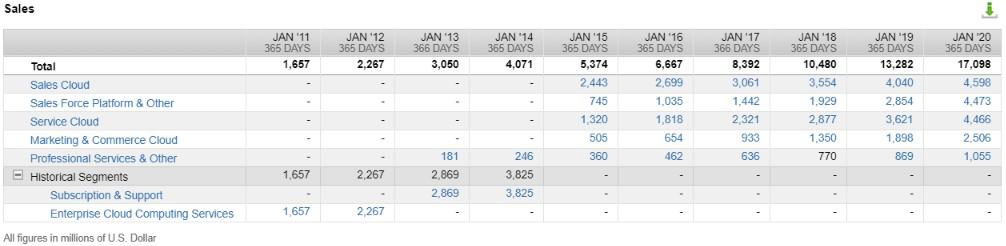

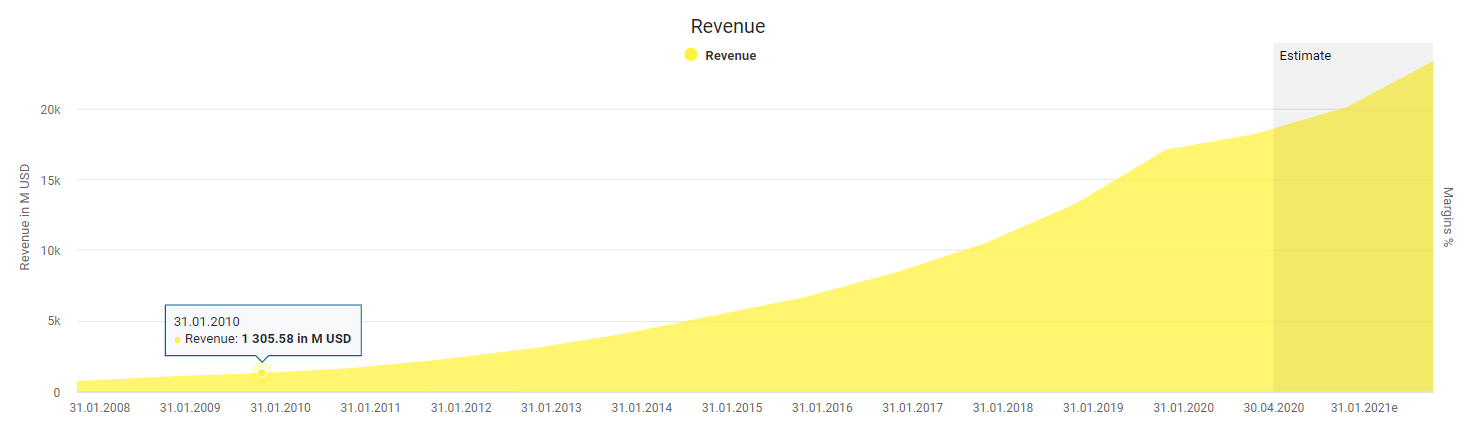

The chart below shows how Salesforce’s revenue growth is consistently around 25 percent per year. While revenue was just under $1.3 billion in 2010, it’s expected to reach nearly $21 billion in fiscal 2021. In this case, sales would have increased more than sixteen-fold within ten years.

Growth is expected to continue in the future. The fundamental development of the CRM market and its outstanding importance for companies make this assumption likely. In particular, the increasing market shares indicate that Salesforce will grow even more strongly in the future than the broader market, whose estimated growth is around 15 percent per year. In my opinion, revenue growth in the range of 20 to 25 percent in the next few years is quite plausible.

How profitable is Salesforce?

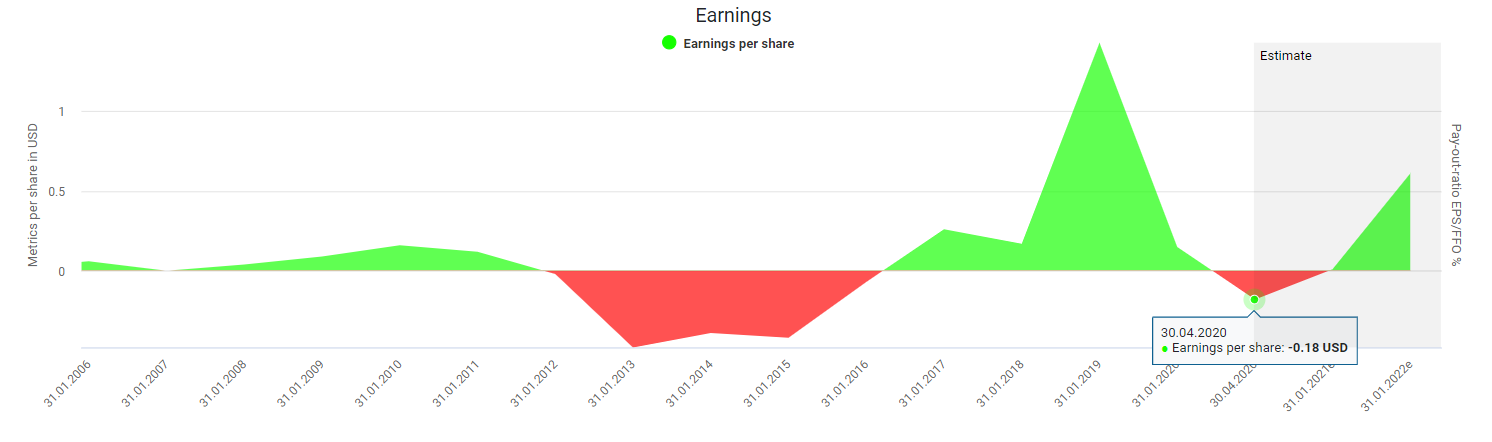

As shown in my Amazon analysis, it can be part of a rapidly growing company’s DNA to make little or no profit, which is also true for Salesforce, whose reported earnings per share are very erratic and sometimes even negative.

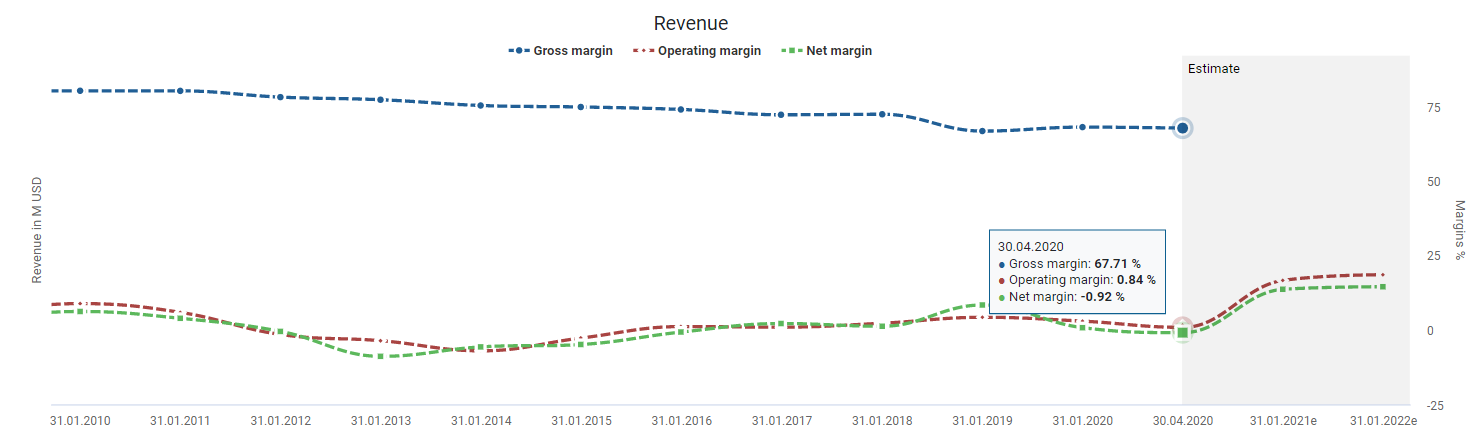

For companies that are still in their early years or a strong growth phase and therefore invest every cent in future growth, it does indeed make little sense to give high priority to profit maximization. Nevertheless, you should make sure that the business model is capable of generating profit. A castle in the air that generates revenue and cash flow but still fails to become profitable is hardly suitable as an investment. However, Salesforce’s gross margin is almost 70 percent. This strongly suggests that the company is fundamentally profitable. It only has high overhead costs, resulting in very low, sometimes negative, operating, and net margins.

Such low margins are not unusual and widespread in the cloud computing market and, for me, no reason to refrain from investing in Salesforce in general. Even the internet giant Alibaba is accepting falling profits to push its cloud business against the big top-dogs Amazon and Microsoft.

Salesforce stock analysis: Fair valuation

The stock price benefits massively from the company’s excellent position on the market and its growth prospects. It does not look as if Salesforce will leave its successful path in the medium term. So it seems clear that you won’t get Salesforce as a bargain. However, the question is whether the valuation is still appropriate or whether the stock now seems completely overpriced. As with Amazon, you should forget about using profit-based figures such as the P/E ratio. Salesforce, like Amazon, prefers to put every cent into future growth. The company doesn’t think about accumulating capital or paying a dividend to its shareholders.

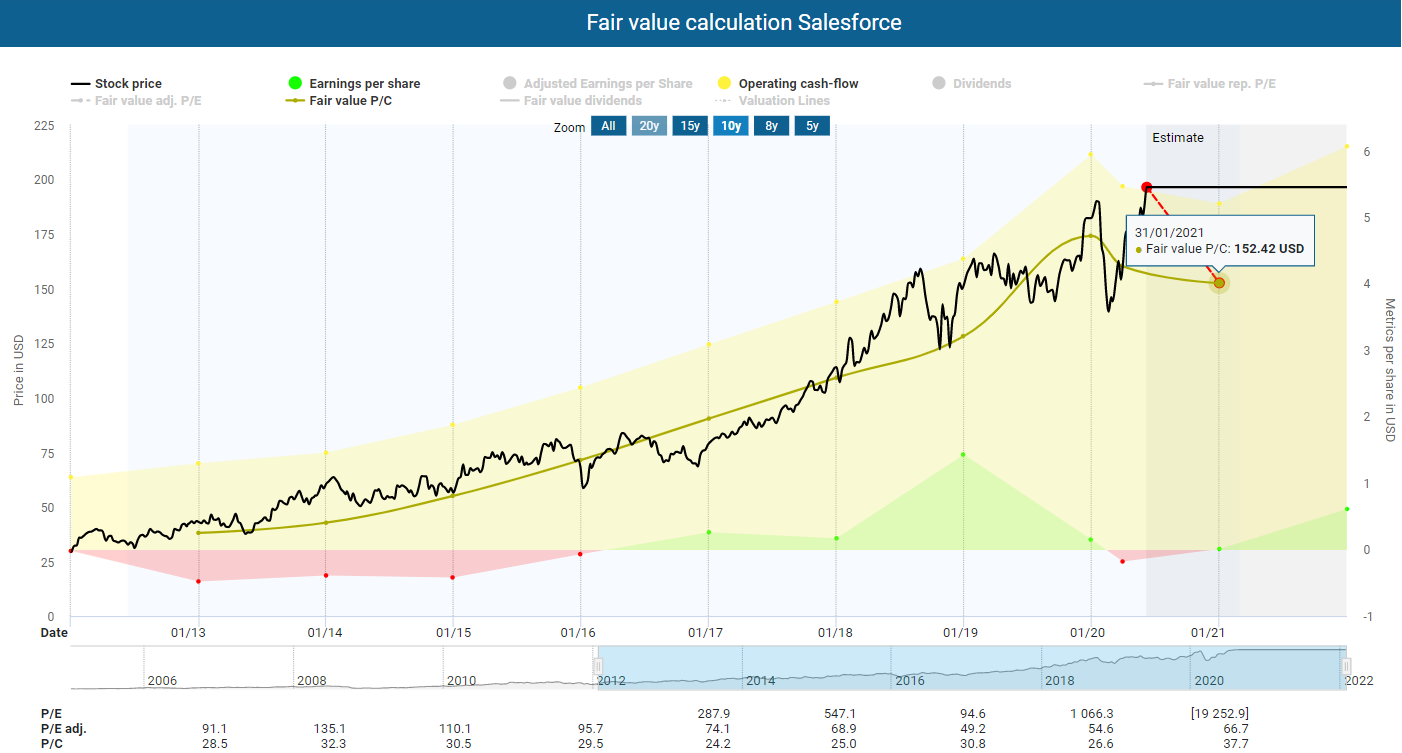

The result is a sometimes absurdly high P/E ratio, which could well be in the four-digit range. Therefore, looking at profits is not helpful. I recommend that you should look instead at the operating cash flow of such companies. As you can see in the dynamic valuation below, the Salesforce stock seems to be overvalued measured by cash flow. With a fair share price of $152 based on historical cash flow, the current price has about 20 percent downside potential.

A Price to sales ratio of over 9.2 indicates an overvaluation in the double-digit percentage range compared to the historical 3-year median of 8.3. The current overvaluation is mainly due to the recent rally after the COVID 19 crash. However, in the course of the crash and in previous years, you have found better time windows for an investment. There, the share returned to its fair value measured by the historical cash flow or even fell below it. Besides, cash flow is expected to fall slightly in the current fiscal year due to the Corona crisis. Therefore, I do not rule out that the share price will return to its historically fair value in the medium term.

Salesforce stock analysis – I would only buy after a setback!

Although the Salesforce ticker on the New York Stock Exchange suggests otherwise, the company did not create the CRM market. However, CEO Marc Benioff has turned the market upside down and taken it to a whole new level. He made this possible by focusing on the cloud early on. Furthermore, Salesforce gathered market shares by offering a broad range of easily scalable products and services. Beyond that, the Salesforce stock fundamentally fulfills all the characteristics of a growth company such as Amazon. The company pays no dividend and hardly makes any profit. Furthermore, multiples indicate a strong overvaluation.

However, you might wait for a price setback of the Salesforce shares. It wouldn’t be the first time the stock returned to its fair price. If you want to buy the stock today, you can buy it in tranches. Besides, you should keep some powder dry to buy it at a more reasonable price.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

Greed and more greed!

I am not quite sure what you mean but thanks for coming by, Marsha 🙂

Seeking Alpha brought me here, TEV! Thanks for your articles and analysis. I will come regularly now.

Thanks for coming by Jonathan. Glad you liked it! Looking forward to seeing you again 🙂