Many investors try to trick the market with elaborate techniques and instruments like swing trading and stop-loss orders. Data and studies show that such techniques have indeed enabled outperformance in the past. Swing trading and stop-loss orders are worth considering, in my opinion. They invite investors to think fundamentally about the art, purpose, and principles of investing. This is exactly how my readers should understand this article – as a small intellectual reflection.

Two techniques that seem to be promising

Swing trading and using stop-loss orders are two techniques I have used a few times myself. Their popularity comes mainly from the fact that they are quite simple to understand in theory. In particular, they provide comprehensible reasons for outperformance.

Especially beginners in the stock markets hope for quick first successes in order to let their capital grow fast. Afterward, they want to put the (accumulated) capital in defensive buy & hold stocks for the long term.

Swing Trading

Swing trading is a type of trading that focuses on realizing small profits in a relatively short period of time. Every investor knows the swings of stock prices (also known as volatility). The basic idea of swing trading is to take advantage of those volatile movements.

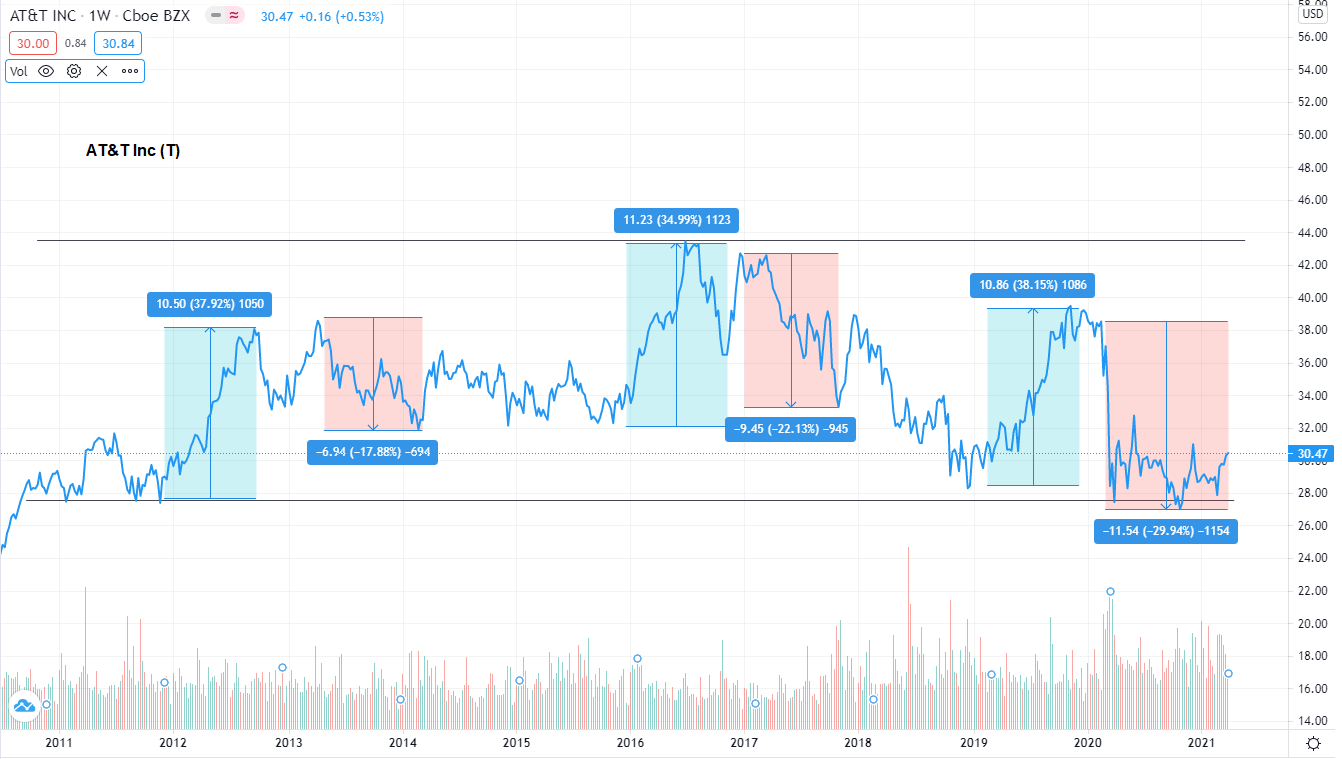

Why should you be invested in a stock for years if it is more or less always stuck in the same price range? AT&T is an excellent example. If we exclude dividends, the stock barely returned anything from 2011 to 2021. However, with the help of swing trading, investors were able to make excellent use of the price movements for quick profits.

Of course, it is impossible to predict the exact highs and bottoms of every move precisely. Thus, the key is to capture the price movements between these bottoms and peaks. Swing traders use technical signals such as moving averages of share prices or the break or test of certain barriers or supports. In the AT&T example above, you can see massive support of around USD 28. When the share price tested this support and bounced off it was the beginning of massive rallies in 2012 and 2019.

Swing traders wait for such signals, they analyze stocks and stock price developments and wait for the right moment to enter. If they think that a trend (price increase or price decrease) is stable enough, they buy shares or even leverage their investment capital. If the share price reaches a predefined price target, then they sell and realize the profits or they set a stop-loss which brings us to the second instrument.

Stop-loss order

Traders or investors who care about short-term price movements cannot wait months or years for a stock price to move in the direction they want. Accordingly, many investors set so-called stop-loss orders, which, for example, trigger a sell order if a share price falls too far. In this way, investors limit their loss of capital and liquidity in order to be able to invest in other promising opportunities.

A trailing stop loss is also a way of protecting profits. With a trailing stop loss, the stop price is linked to the share price at a fixed interval (trailing value). This means that the stop-loss price increases with the share price.

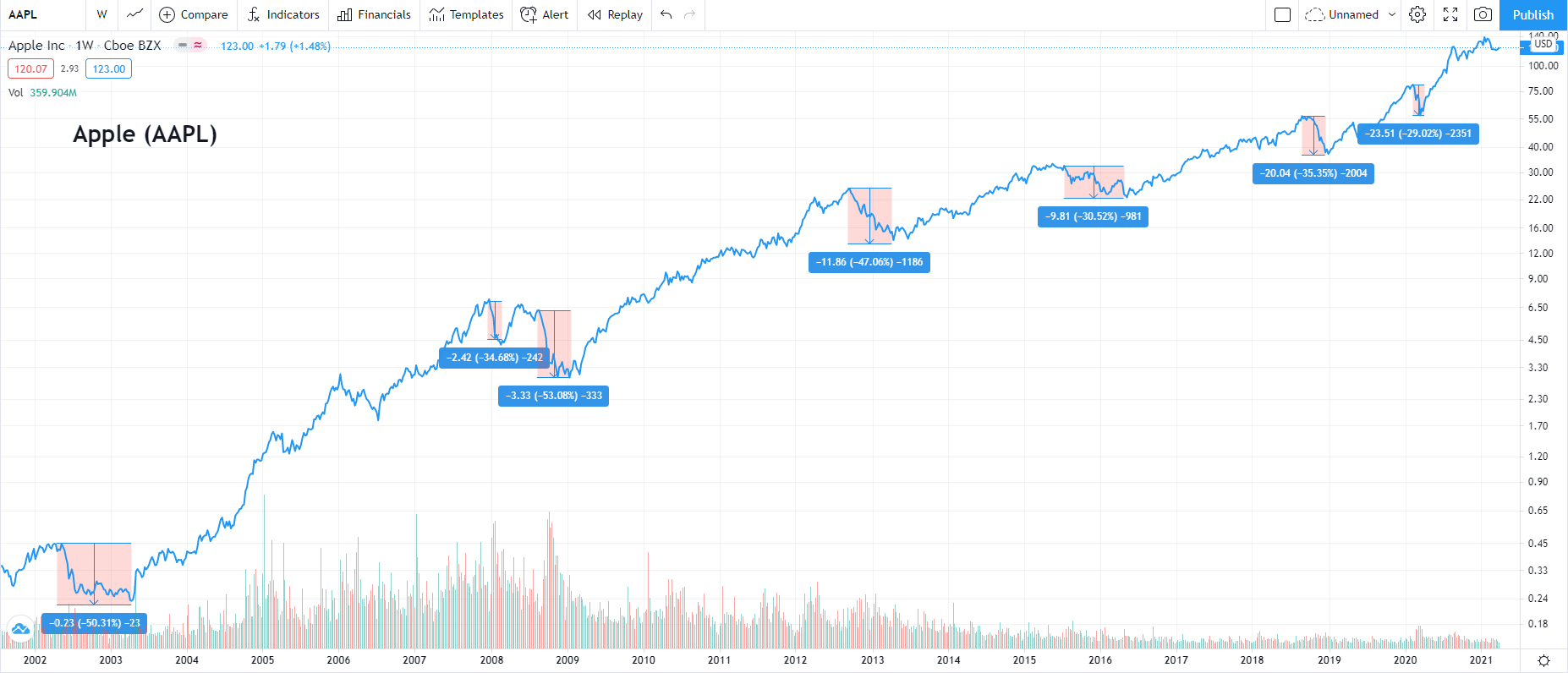

Let’s take Apple’s share price to visualize how powerful such instruments could be. The Apple share shows the typical course of an excellent long-term investment. In the long term, it went up and up. But if we zoom in a little more closely, we see multiple corrections and veritable crashes of more than 50 percent in some cases.

Imagine that you had already sold the shares at minus 10 or minus 20 percent due to the stop-loss order during the corrections, some of which were over 50 percent, and then bought them back when the trend reversed (see swing trading above).

Stop-loss orders – Taking empirical research papers into account

A reader brought an interesting article to my attention. The colleagues from Quant Investing analyzed in a blog article three research papers which focused on stop-loss orders:

- When Do Stop-Loss Rules Stop Losses? (study)

- Performance Of Stop-Loss Rules vs. Buy-And-Hold Strategy (study)

- Taming Momentum Crashes: A Simple Stop-Loss Strategy (study)

Quant Investing summarizes the results as follows:

- When applied to a 54 year period a simple stop-loss strategy provided higher returns while at the same time lowering losses substantially

- A trailing stop loss is better than a traditional (loss from purchase price) stop-loss strategy

- The best trailing stop-loss percentage to use is either 15% or 20%

- If you use a pure momentum strategy a stop loss strategy can help you to completely avoid market crashes, and even earn you a small profit while the market loses 50%

- Stop-loss strategies lowers wild down movements in the value of your portfolio, substantially increasing your risk adjusted returns

The results are quite impressive and thought-provoking. Nevertheless, some aspects are already evident by logic. Among them is the result that a trailing stop-loss strategy is superior to a simple stop-loss strategy. It should also be clear that a momentum strategy with a (trailing) stop-loss will ensure that you avoid crash phases.

Nevertheless, the advantages of a stop-loss strategy become clear here. For those who are close to retirement or have a certain loss aversion, stop-loss orders are excellent ways to let stock gains run and protect them at the same time.

A few reflections

I had already announced it in the introduction to the article. That’s why I want to reflect a bit here and think fundamentally about investing. The following considerations are, therefore, somewhat subjective. I welcome comments, objections, and counterarguments 🙂

Methodical problems – Taleb’s “triplet of opacity”

From my perspective, models that prove the superiority of a strategy often have problematic methodical issues.

Past data explain past events, but they say little about what the future holds. We also tend to perceive past events as more predictable than they actually were (so-called hindsight bias). This puts us very close to Nassim Nicholas Taleb’s “Triplet of Opacity”, taken from its book “The Black Swan”:

The illusion of understanding, or how everyone thinks he knows what is going on in a world that is more complicated (or random) than they realize.

The retrospective distortion, or how we can assess matters only after the fact, as if they were in a rearview mirror (history seems clearer and more organized in history books than in empirical reality).

The overvaluation of factual information and the handicap of authoritative and learned people, particularly when they create categories— when they “Platonify.”

Accordingly, we must be careful about deciding our investment strategy just by looking in the rearview mirror. For example, it is not at all clear whether the results of the above-mentioned research papers are purely coincidental. Furthermore, they do not even capture unknown extreme events. I am thinking of fat tails that can easily destroy the “normal distribution” of all those past data.

The flash crash / the fat tail event that no one saw coming

In addition, such models quickly lull investors into a sense of security where there is none. They may work out 99 times out of 100. But what happens if that one exception has unpleasant consequences for me as an investor? Flash crashes can quickly trigger sell orders.

Here’s the scenario I’m thinking of: imagine a flash crash triggers a sudden 40 percent drop in the stock markets. The sell order triggered by stop-loss sells only at 30 or even 35 percent price loss instead of 20 percent (a common risk with stop loss). Shortly afterward, prices recover and return to their initial level. Imagine that all this happens within a few hours. Then you’ve burned about 30 or 35 percent of your portfolio.

I know all of this is unlikely and has never happened on this scale before (the flash crash of 2010 had a scale of “only” 9 percent and lasted 40 minutes). But that’s what it’s all about. Just because something like this hasn’t happened in the past doesn’t mean it can’t happen. Black swans are so destructive precisely because no one thought they were possible.

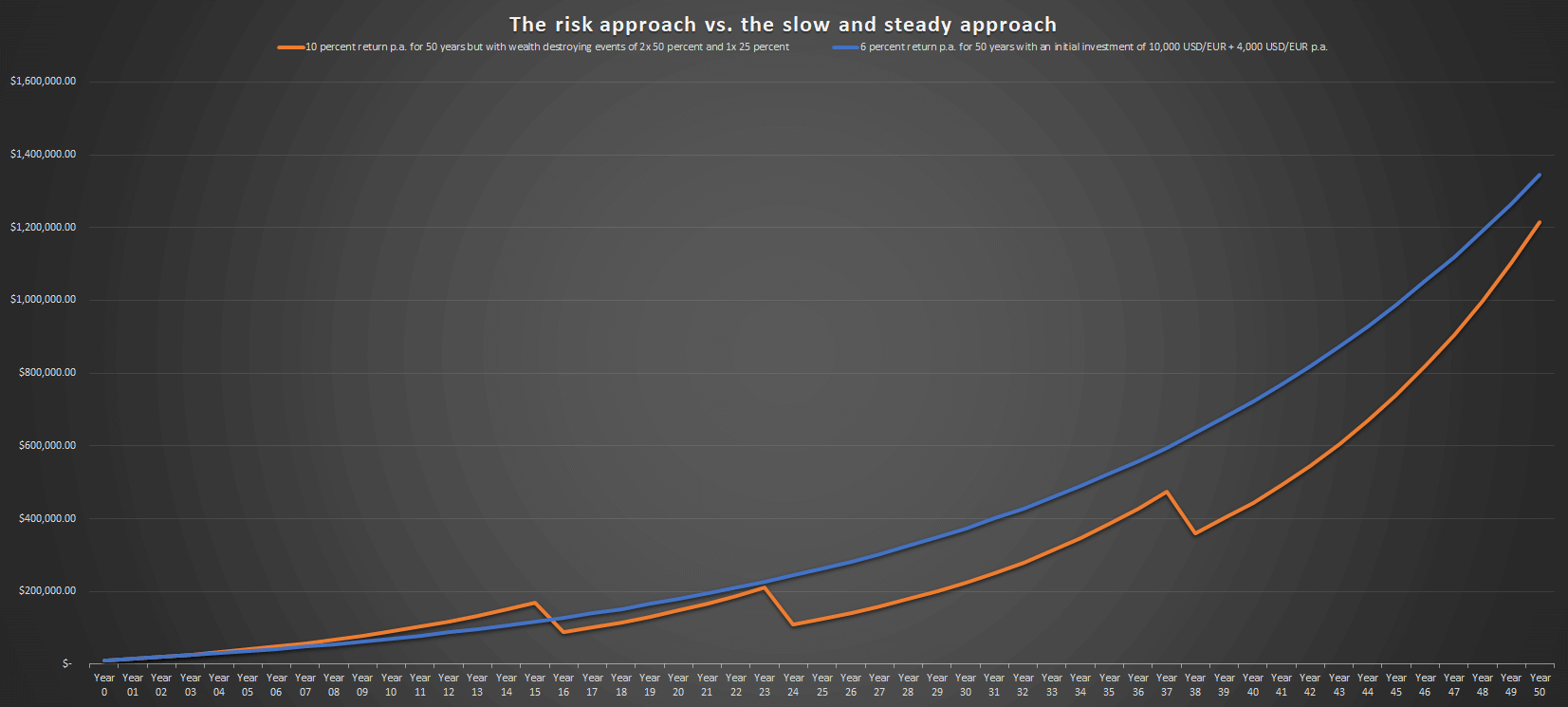

The impact of wealth-destroying events on our overall performance

I try to minimize my vulnerability to such scenarios as much as possible because their impact on my overall return can be devastating. In another article on the TEV Blog, I provided the following example that also fits in here:

Even for an investor who has a higher return because of his risky strategy, such events significantly impact the overall performance. Not in a good way. We assume that the high-risk investor achieves an annual return of 10 percent. As in the example above, the initial capital was 10,000 USD/EUR, and the yearly investment 4,000 USD/EUR. With three extreme events of losing 50 percent of the assets twice and 25 percent once, this investor did worse after 50 years than the investor with an annual return of only 6 percent.

Here you can see well why I want to avoid any final wealth-destroying events. Given that the sale of my assets at an inopportune time, triggered by a stop-loss, is such a scenario, I try to avoid this from the outset.

Buying for fundamental reasons and selling for other reasons doesn’t work

Every investor who manages his own assets should follow a long-term strategy and stick to it. I, and the majority of my readers, buy companies that they want to own from a commercial point of view.

They look at how expensive the share in the company is. They also check whether the price of this piece of the pie is appropriate and reasonable. I like this approach and proceed in the same way.

A stop-loss stands in the way of this strategy. Why should I sell my piece of the pie because the price has dropped? Then another investor gets the same piece for less than I got. Even a trailing stop-loss does not change this. If I buy a stock for fundamental reasons, then only fundamental reasons should justify a sale, right?

We see here that it always comes down to strategy. For value investors, there are fewer reasons to sell shares than one might think.

We should treat big money the same as small money

In conversations with colleagues, friends, and readers, I often hear that they first want to make money with certain strategies. Afterward, they also want to switch to the buy-and-hold camp. Of course, this sounds tempting. First, we accumulate capital. Then we invest it for the long term.

However, I don’t see any reason why we should treat big money differently than small money. Many people tend to take a riskier approach with less money. But even if you only have small amounts of money, I think we should take the same risk approach should as with high net worth. As we have seen above, wealth-destroying events can be an extreme brake on wealth creation.

Besides that, I also think the following. Doesn’t it make sense to take a cue from what the particularly wealthy people do? Do you think Bill Gates sold all of his Microsoft stock when the stock corrected 20 percent once? Do you think he used a stop-loss order when the stock exploded during the tech bubble?

So instead of putting our existing wealth at greater risk, I suggest increasing the income side.

You have discussed the pros and cons of the swing trading. People will understand it very well. Images and the descriptive way of trading method makes it user friendly and readers good will.