Hello, my dears, welcome to a new overview of upcoming ex-dividend dates and dividend ideas here on the TEV Blog. Like every week, I want to show you some stocks that will go ex-dividend in the next days. I’ll also review a few companies that are currently in the focus of investors or that have an attractive fundamental valuation. Additionally, I’ll give you some insights into my retirement portfolio and/or share my thoughts and experiences about individual companies with you.

Why yields are a simple way to screen companies

Dividends are a great thing. Even in bad stock market times, they provide a juicy cash flow per month. If you want to benefit from dividend payments as quickly as possible, you must pay attention to the ex-dividend dates. This date is the day on which shares are traded without their subsequent dividend value. Only if you owned the stocks on this day are you entitled to receive the dividend.

Usually, there are always exciting dividend companies that are worth a second look. And the dividend yield is an excellent way to get an initial overview of companies that may be worth further due diligence. To help you get started, at the end of each week, I will publish the ex-dividend dates for the coming week of individual companies here in the TEV blog.

Why I handpick and double-check the upcoming ex-dividend dates next week

I have recently noticed that many databases do not indicate the respective numbers and dates correctly. Spontaneous dividend cuts, in particular, are only partially taken into account, or in some cases, not at all. As a result, the value of such overviews dwindles enormously.

Therefore, I’ve decided to select individual companies by hand and check the dates and dividend yields on the companies’ websites, which means more work for me but increases this section’s value enormously, so it is worth it 🙂

Because I’ve been asked about it by some of the readers: I don’t decide my investments based on whether a company goes ex-dividend or not. This overview is simply a way to screen companies regularly. By double-checking the current dividend yields, I scan companies’ business development more or less once a quarter and see if anything significant has changed. In the end, however, comprehensive due diligence always decides whether I invest or not.

Ex-Dividend Calendar

As always, you’ll find some handpicked exciting ex-dividend dates below.

| Company | Payment Date | Yield | In my retirement portfolio |

|---|---|---|---|

| Monday, October 12, 2020 | |||

| - | |||

| Tuesday, October 13, 2020 | |||

| Comtech Telecommunications Corp. (CMTL) | October 27, 2020 | 2.60% | NO |

| InterDigital Inc. (ITDD) | October 28, 2020 | 2.40% | NO |

| HarborOne Bancorp Inc. (HONE) | October 28, 2020 | 1.36% | NO |

| Wednesday, October 14, 2020 | |||

| AbbVie Inc. (ABBV) | November 11, 2020 | 5.42% | YES |

| Abbott Laboratories (ABT) | November 16, 2020 | 1.3% | NO |

| Arcosa Inc. | October 30, 2020 | 0.43% | NO |

| Bel Fuse Inc. | October 30, 2020 | 2.58% | NO |

| China Petroleum & Chemical Corp. (SNP) | November 13, 2020 | 13.11% | NO |

| HB Fuller (FUL) | October 29, 2020 | 1.30% | NO |

| Sabine Royalty Trust (SBR) | October 29, 2020 | 7,80% | NO |

| Trinity Industries Inc. (TRN) | October 30, 2020 | 3.72% | NO |

| The Buckle Inc. (BKE) | October 29, 2020 | 4.2% | NO |

| Watsco Inc. (WSO) | October 30, 2020 | 3.00% | NO |

| Thursday, October 15, 2020 | |||

| Emcor Group (EME) | October 30, 2020 | 0.45% | NO |

| Eog Resources (EOG) | October 30, 2020 | 4.00% | NO |

| First United Corp. (FUNC) | November 02, 2020 | 4.10% | NO |

| Foot Locker Inc. (FL) | October 30, 2020 | 2.43% | NO |

| Global Water Ressources (GWRS) | Otober 30, 2020 | 2.62% | NO |

| Morningstar (MORN) | October 30, 2020 | 0.66% | NO |

| Quaker Chemical Corp. (KWR) | October 30, 2020 | 0.81% | NO |

| Oxford Industries Inc. (OXM) | October 30, 2020 | 2.46% | NO |

| Patterson Cos. Inc. (PDCO) | October 30, 2020 | 4.01% | NO |

| Saul Centers Inc. (BFS) | October 30, 2020 | 7.6% | NO |

| Friday, October 16, 2020 | |||

| Hormel Foods Corp. (HRL) | November 16, 2020 | 1.9% | NO |

What’s on the list this week?

As always, I will report something about the week. This time I will start with some general thoughts before I turn my attention to three companies.

General thoughts

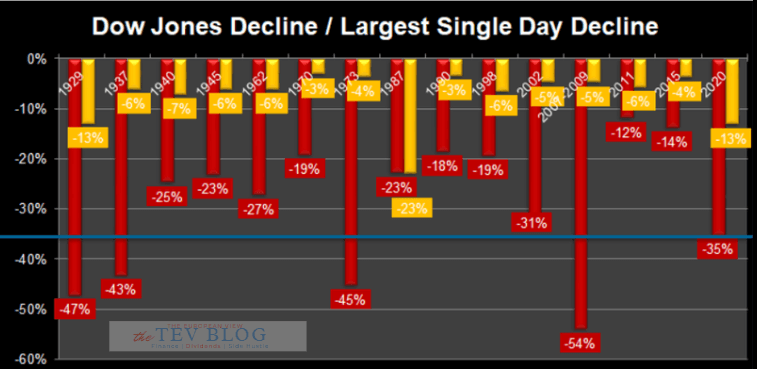

A few days ago, I thought about the beginning of the Corona pandemic. Almost exactly seven months ago, the big crash began, which caused stock markets to collapse worldwide.

Once again, it has been confirmed that it is possible to buy excellent companies at a reasonable price in a recession or crisis. Thus, investors can build wealth in times of crisis or lay the foundation for wealth during these times.

In the meantime, however, the shares are again close to their record levels, which applies to the US American indices as well as to the European and, to some extent, Asian indices. But if we look at what caused the crash in March, we see that the facts have not changed compared to today. By this, I mean, of course, the development of the corona pandemic, the number of people infected, and the increasing fear that existing capacities in intensive care units are not sufficient.

In my view, there is still an extreme downside risk that every investor must be aware of. The many young and inexperienced investors must keep in mind that they will end up owning companies with shares. So their capital will suffer just as much as the business of these companies.

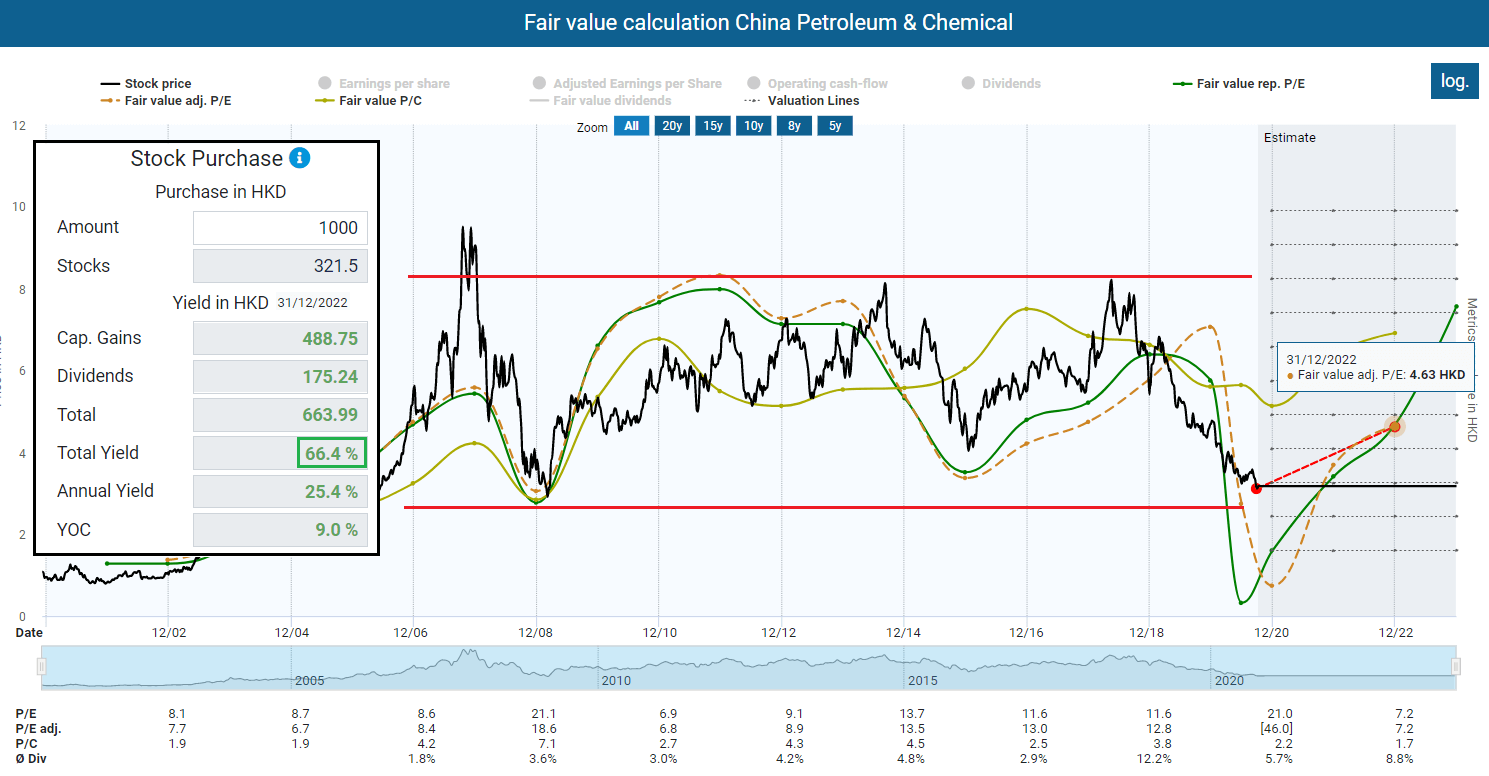

China Petroleum & Chemical Corp. (Sinopec)

China Petroleum & Chemical Corp. (also called Sinopec) is a Chinese natural gas and petroleum company based in Beijing. Sinopec is one of the three largest petroleum companies in China and was at the top of China’s top 500 companies list from 2006 to 2010. The company is active in the exploration and production of oil and natural gas, the construction of pipelines with the corresponding marketing, oil refinery and production, storage and transport of petrochemicals, chemical fibers, chemical fertilizers, and other chemical products, as well as the import and export of crude oil and natural gas.

If you look at the fundamental valuation, the stock is at the bottom end of a wide range. Like other oil companies, the low oil price has left deep scars and made the stock relatively cheap. Based on historical multiples, we have an upside potential of 66 percent.

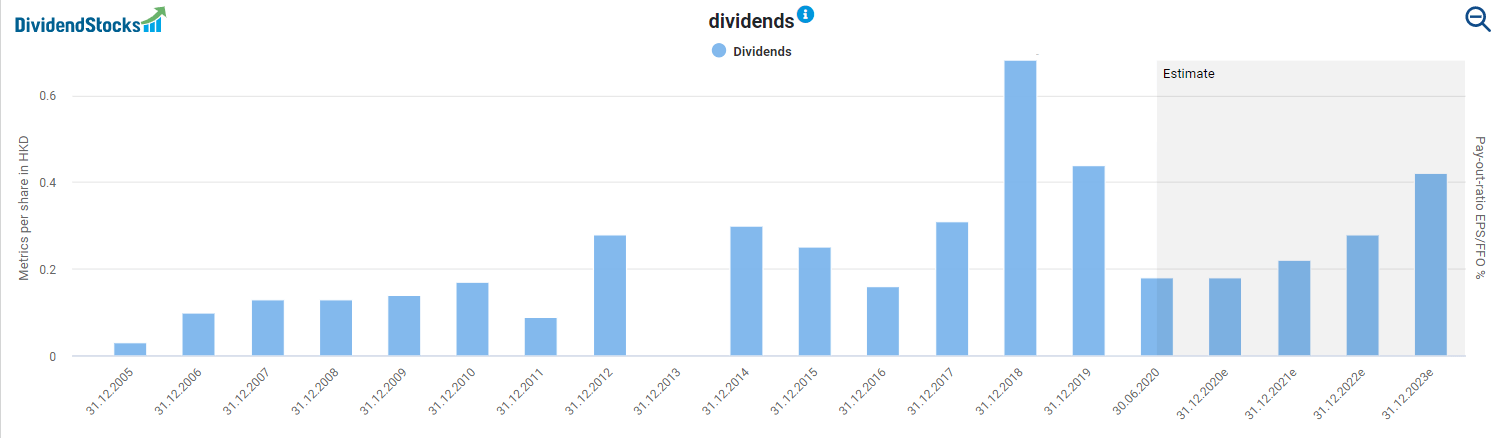

But from my point of view, there are several problems. Such as Royal Dutch Shell or Kinder Morgan (two companies I hold), the company is active in industries that are facing difficult times. The company is also a very irregular dividend payer and anything but a growth stock. Therefore this is not an exciting investment option for me. Even the high dividend yield of 13 percent does not change this.

For example, the company has a good A1 rating from Moody’s with a stable outlook. The reasons for the rating were as follows:

- Credit profiles (liability to asset ratio of 54.4 percent in 1H 2020) will remain resilient amid slower economic growth in China (A1 stable) and the low oil price environment.

- The large integrated downstream businesses, which help mitigate the impact of low crude prices, a robust financial profile, and the expected very high level of support from the Chinese government, would support the business in the future.

You can find more financial information and presentations for the company here.

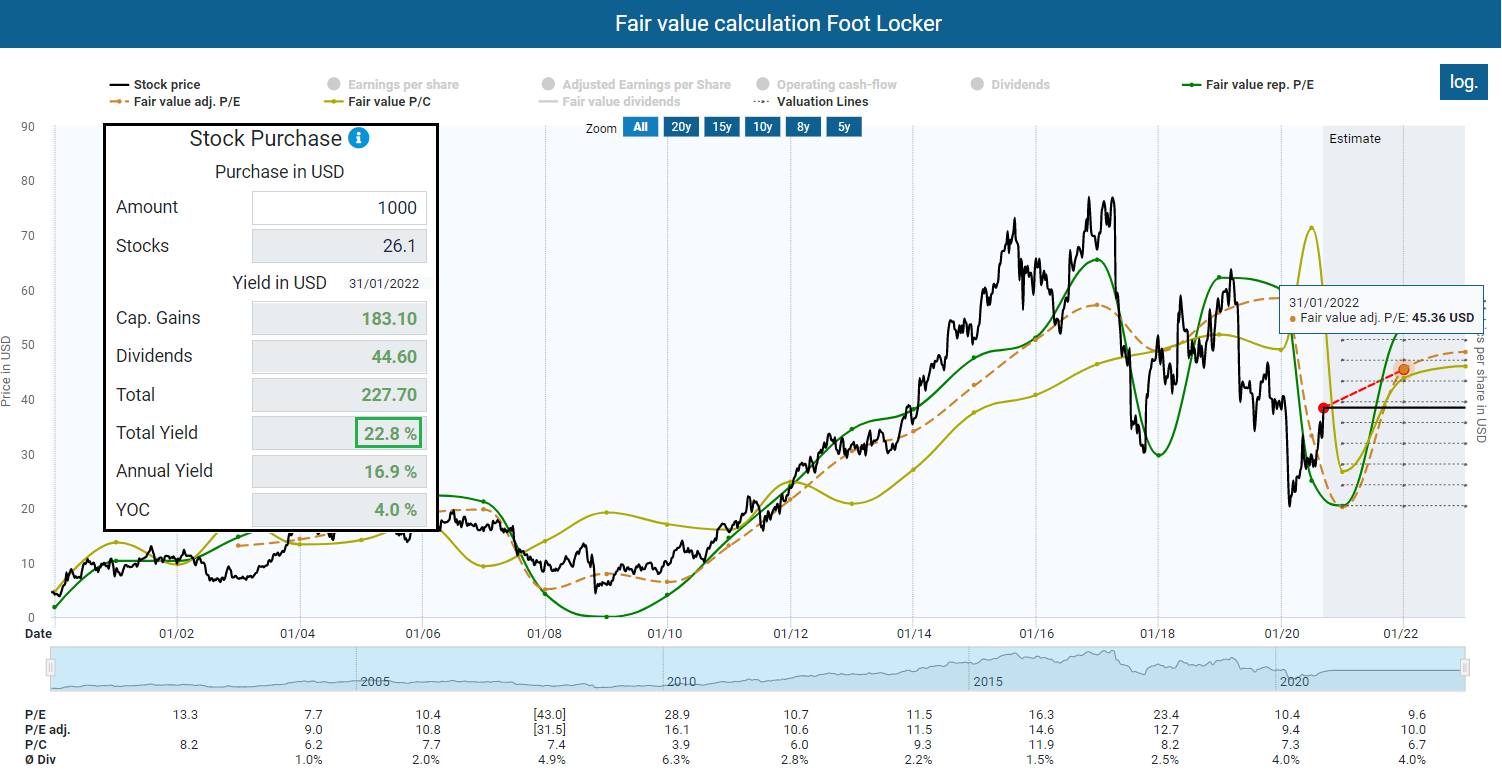

Foot Locker Inc.

Another investment idea could be Foot Locker. The company sells shoes and apparel through different channels, e.g., its 3,100 retail stores in 27 countries, websites, and mobile apps. Based on the expected profit for the end of 2022, the fair value is 22 percent over the current price. Also, the P/E ratio of just 10 indicates a relatively favorable valuation.

The company has been paying a dividend (USD 0.03) since 2003 and has increased this to USD 1.25 per share. However, Foot Locker paused the dividend in the second quarter. In August, Foot Locker then announced that it would again pay a quarterly dividend. Nevertheless, the company reduced the payout by 66 percent to USD 0.15 per share. It has also stopped its share buyback program. If Foot Locker returns to the old payouts, this would mean a yield of 4 percent, which wouldn’t be that bad.

Out of context: IBM

This week, we have a kind of special guest today, namely IBM. Although the company is not going ex-dividend this week, the news was quite impressive, so I use the TEV blog to talk a bit about IBM.

What happened?

IBM’s share price has risen by up to 12 percent after the company announced that it intends to spin off its IT infrastructure business. Until now, IBM operated through five business segments:

- Cognitive Solutions

- Global Business Services

- Technology Services & Cloud Platforms

- Systems

- Global Financing

The spin-off will result in a listed company that does not yet have a name and is initially called “Newco”. The company will incorporate the existing maintenance business for IT infrastructures such as networks, mainframes, data storage, PCs, or data centers.

According to IBM, the new company (to be named at a subsequent date) will immediately be the world’s leading managed infrastructure services provider. For NewCo, IBM sees a USD 500 billion market where NewCo can help companies in all industries build and modernize infrastructures. NewCo will then have around 4,600 customers in over 100 countries, 90,000 employees, and generate revenues of approximately USD 19 billion. The separation will be tax-free for IBM shareholders who receive shares of NewCo and is expected to be completed by the end of 2021.

This is what CEO Arvind Krishna said in a press release about this step:

IBM is laser-focused on the $1 trillion hybrid cloud opportunity. Client buying needs for application and infrastructure services are diverging, while adoption of our hybrid cloud platform is accelerating. Now is the right time to create twomarket-leading companies focused on what they do best. IBM will focus on its open hybrid cloud platform and AI capabilities. NewCo will have greater agility to design, run and modernize the infrastructure of the world’s most important organizations. Both companies will be on an improved growth trajectory with greater ability to partner and capture new opportunities – creating value for clients and shareholders.

If you want, you can find more info here:

- IBM strategic partnership (slides)

- IBM strategic partnership (press release).

Will there be another spin-off?

After that transformation, “Global Business Services” is a difficult fit for the new IBM company. In this segment, IBM houses its consulting business, i.e., strategic consulting services for external customers. IBM would not be alone with a spin-off. As early as 2016, HP Enterprise sold its IT consulting division four years after the purchase. Before that, HP Enterprise had to write off 50 percent ($8.5 billion) of the 2012 purchase price. The business is not very attractive and suffered during the Corona period. In the second quarter, for example, revenue was down 7 percent.

My opinion

For shareholders, this step means that they will receive shares of NewCo in their securities account, which means that the existing proportion of IBM shares will decrease. The new IBM has better growth prospects than NewCo since IBM will be active in the more vital growing segment. With the spin-off, IBM basically dumps a low-margin and shrinking business. Additionally, this business may be in the long-term cannibalized by the cloud business. Therefore, I can well understand investors who sell their shares in NewCo and prefer to invest in the new IBM. In this respect, I assume that the share price of NewCo could even come under heavy pressure at the beginning, but this is something we will have to see.

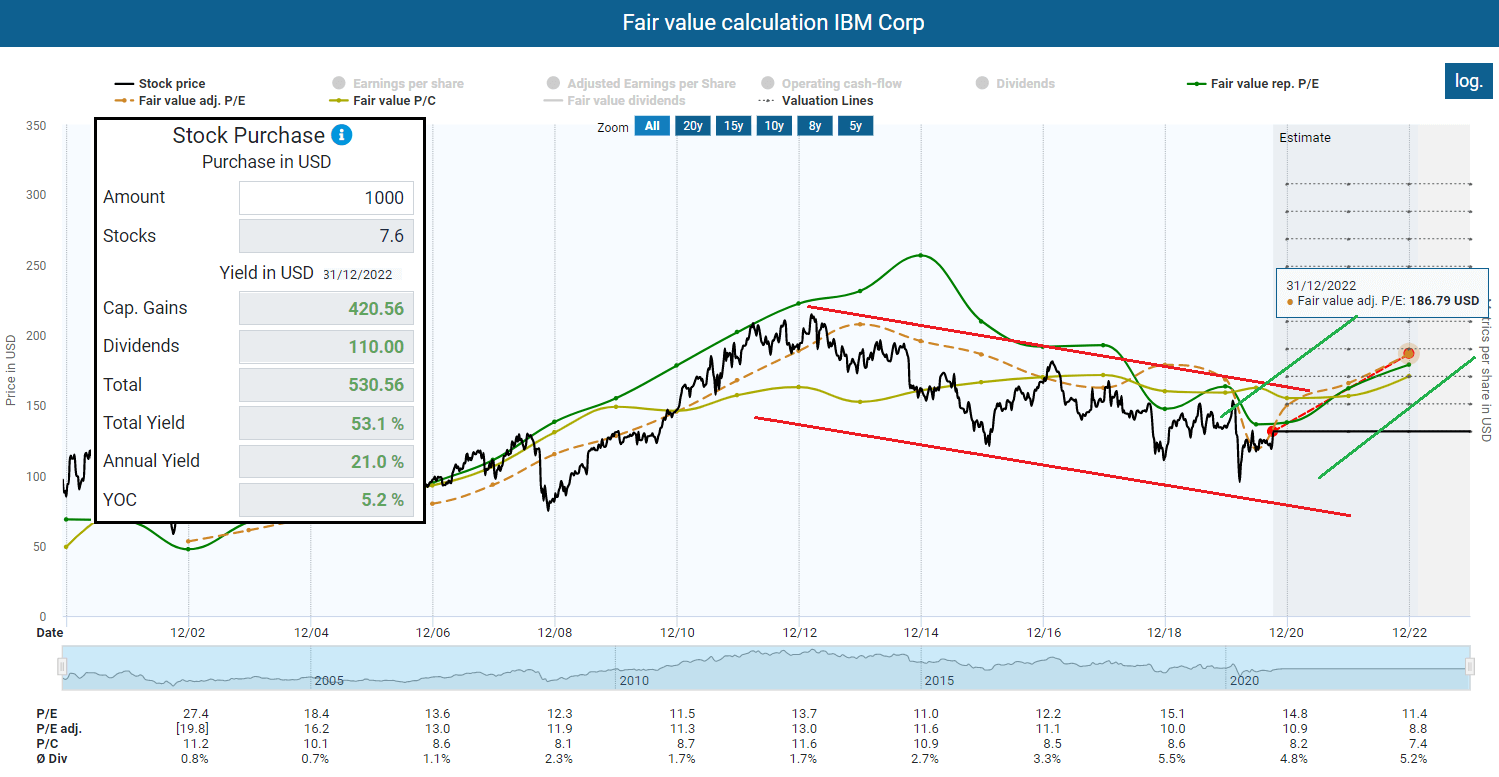

In my opinion, the shares of the new IBM have enormous potential. The cloud segment has a profit margin of over 70 percent and operates in a rapidly growing market. IBM shares are also extremely cheaply valued. Based on historic multiples such as the adjusted fair value P/E ratio, we have an upside potential of roundabout 55 percent.

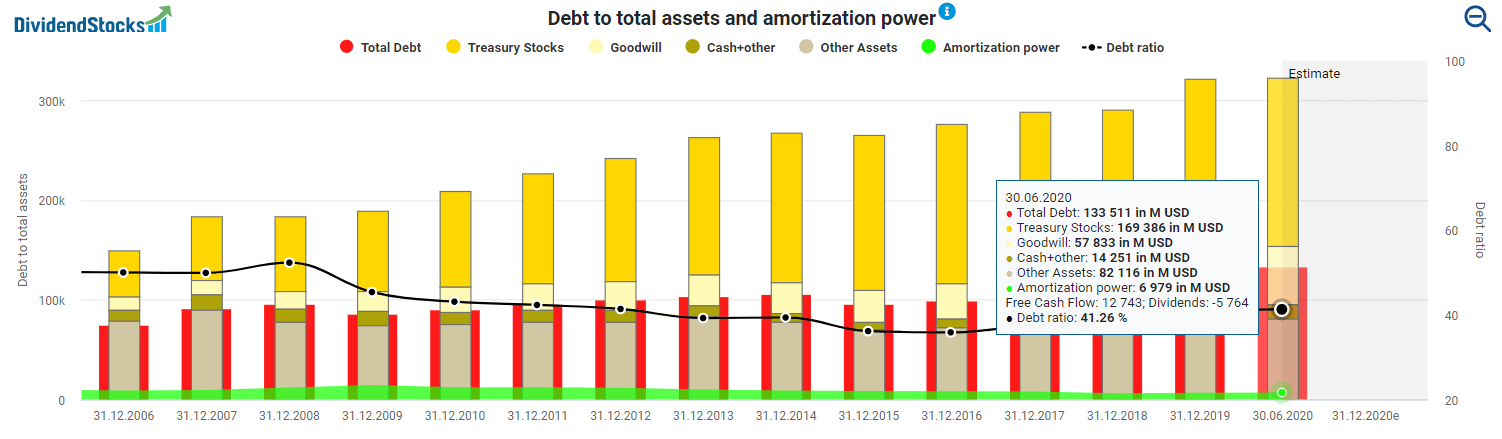

Furthermore, the company is on an excellent financial footing. Just look at the pile of IBM’s treasury stocks. The company is sitting on 170 billion US dollars worth of its own shares.

IBM expects that the companies together will pay a combined quarterly dividend no less than the IBM dividend per share prior to the spin-off. Against this background, IBM remains attractive to dividend investors. However, this does not necessarily mean that the ratio of dividends will be the same as the spin-off of NewCo from IBM. Investors should therefore be somewhat suspicious here.

Dividend scoreboard:

- Dividend Yield:4.9%

- Years of Dividend Growth: 21 years

- Payout ratio based on earnings: 73 percent

- Cash Payout ratio: 47 percent

- 5 Year Dividend Growth Rate: 8.63 percent

- 1 Year Dividend Growth Rate: 1.88 percent.

Conclusion

The new IBM could be extraordinarily successful and bring the Red Hat acquisition synergies to full bloom. I am somewhat less convinced of the NewCo. Investors could speculate that IBM shares will rise now. Whoever buys now could profit from this development and sell the shares of NewCo after the spin-off. There is then, of course, the risk that the prices of NewCo shares will come under pressure.

Time to do your due diligence

Has a company caught your interest? Attractive dividend yields should not be the only reason to buy shares of a company. Instead, you must carry out careful due diligence before every purchase. The Internet offers you excellent opportunities in this respect.

My analyses here on the TEV Blog are an excellent way to start (click here). You can also contact me here or ask the community in the comments if they can help with your due diligence.

Otherwise, I use tools like those from Dividendstocks.cash and Seeking Alpha to do further research. You can also find me and my analyses on these platforms. We also have a small but lovely group on Facebook that you can join. We share there only fundamental analyses of companies from various sources. So there is no spamming or anything like that.

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

That said, feel free to let us know if I have overlooked an attractive stock or you know of a stock that is particularly attractive and where the ex-dividend date is coming up.

Is a stock here attractive for you? If so, let the community also know and write a comment.

You can also share this post with your favorite network:

ABB is not Abbott but ABB Ltd.

Abbott is ABT and yields 1.31%

You are absolutely right, thank you very much. I used the wrong ticker regarding the yield.

Now everything is right!