Even though the stock markets are currently continuing to rise, the public bailouts of many companies once again illustrate the extent of the COVID-19 crisis. These bailouts took on historic proportions and eclipsed everything that had gone before. With such measures, states want to protect jobs and companies from insolvency. On the other hand, such developments may eliminate the functioning of competition and turn stock markets into casinos. However, apart from gamblers, you can also find serious investors who take advantage of the moment.

Investors Key Takeaway

- In the COVID-19 crisis, governments worldwide are putting together financial aid packages. Such bailouts have always been measures to support ailing companies or even states.

- In the G7 countries, the bailout packages were almost as high as all previous bailouts combined.

- However, bailouts also have adverse effects, as they distort competition. Besides, states spend taxpayers’ money to finance possible inefficient companies. But even these companies offer jobs that are important to secure in an economic crisis.

- Both gamblers and defensive investors use the uncertainties and volatility to go bargain hunting. Just take the German entrepreneur and billionaire Heinz Hermann Thiele as an example. In the wake of the COVID-19 crisis, he invested massively in the faltering aviation giant Lufthansa. Now, he is the largest shareholder of the company. The company gets a bailout of €9 billion and is expected to survive the crisis in the long term.

- I also took the opportunity and bought massive amounts of shares in the crash.

Why governments bailout companies?

Bailouts are a widespread means of rescuing companies that have fallen into troublesome waters. The reasons for this can be many and varied.

Bank bailout of 2008

During the financial crisis of 2008 and 2009, the main concern was to keep the financial system stable and not to cause it to collapse. The stability of the system was of paramount importance for governments to keep the economy afloat. Otherwise, companies would have had difficulty getting credit, which would only have exacerbated the problems of the companies and probably led to an even deeper recession, causing extreme suffering and social decline among the people. To avoid this and to help the financial industry, the US Congress passed The Emergency Economic Stabilization Act. In the end, the American government spent nearly $700 billion to bail out ailing companies and boost the economy.

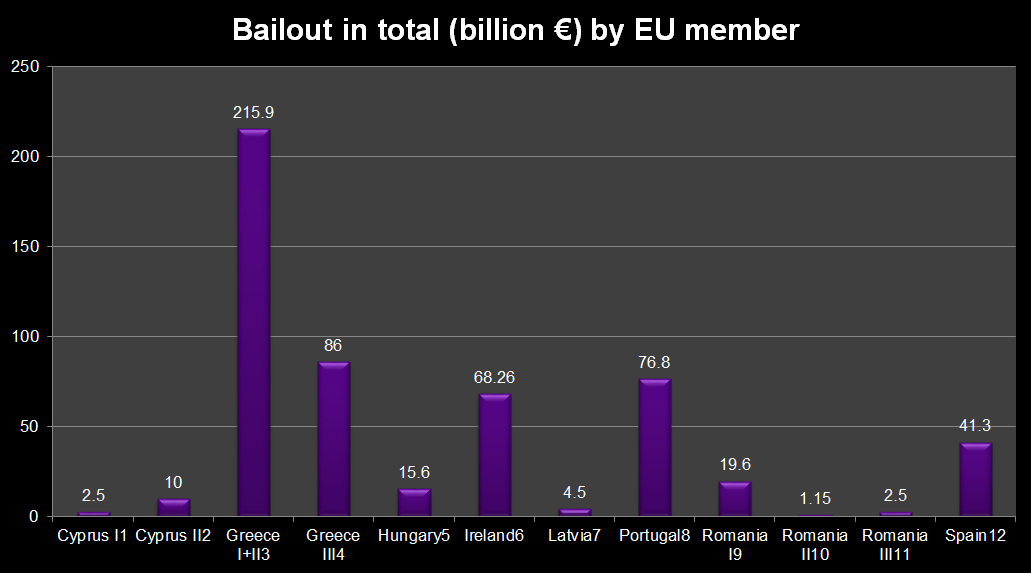

Bailouts in the European debt crisis

In the European debt crisis, the European Union tied up massive bailout packages as well. In total, €544 billion were paid to EU member states in need of financial help, such as Greece, Cyprus, Ireland, and Spain.

COVID-19 calls for a new era of bailouts

During the COVID 19 crisis, states have so far been concerned with saving jobs and companies from insolvencies and hostile takeovers. Just take a look at the €10 billion-bailout of the Lufthansa Group, the second-largest airline in Europe. Because of COVID-19, tens of thousands of the company’s jobs are at risk. The company is barely liquid. At the height of the crisis, it had around 800 million euros a month in cash drain. Many customers are demanding compensation for canceled flights, and it is not foreseeable when air traffic will normalize again. The situation for the company is correspondingly difficult. Other companies were less fortunate and have already had to file for bankruptcy:

Retailers, who were already suffering from the change in consumer shopping behavior, were particularly affected. REITs such as Tanger Outlet Factory Centers and Simon Property Group, popular among dividend hunters, suffered extreme losses of up to 70 percent.

Depending on how long such crises last, companies can no longer afford to pay dividends. They simply no longer have any cash. The high dividend yield thus becomes a warning signal. Public bailouts will not save the dividends either. There are often conditions that forbid companies to pay dividends as long as they have not repaid loans or other aid measures.

Bailouts became bigger and bigger

In the COVID-19 crisis, the bailouts have reached historic proportions. In the G7 countries, the bailout packages were almost as high as all previous larger bailouts combined. Accordingly, the total debt also rose sharply. The debt is now nearly three times the Gross Domestic Product (GDP).

Bailouts May Have Adverse Effects

Bailouts also have adverse effects. They are an intervention in healthy competition. Companies that have managed well and reasonable and that, therefore, do not need help are disadvantaged compared to companies that have poorly managed for years. In the worst case, the market is full of zombie companies. Zombie companies are companies that are older than ten years and have an interest coverage of less than 1 for more than three consecutive years. With bailouts or other aid measures, states keep inefficient companies alive artificially, even though they could not exist if the competition were effective.

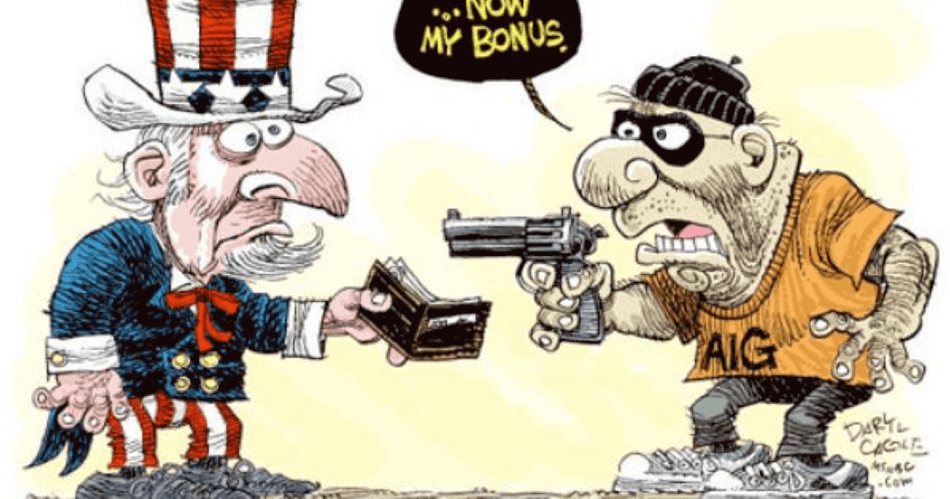

In the end, it is the taxpayer who pays public bailouts. Many people are frustrated when they see that this money is used to bail out poorly managed companies instead of putting the money into schools and infrastructure. When AIG wanted to pay bonuses to managers in 2009, even though the company had lost more than $60 billion and had to be rescued with taxpayers’ money, the public was rightly furious. The US aid package for the Group amounted to 180 billion dollars. In return for the rescue, the state received 79.9 percent of the shares in the insurer. But then, in the middle of the Great Recession, more than 400 managers were to receive fat bonus checks and referred to their contracts of 2008.

Bailout Of Companies Attracts Gamblers And Conservative Investors

These developments are turning some of the stock markets into casinos where adventurers chase wealth, and conservative investors seek bargains. The more prices fall, the more greed and fear take over the stock markets. The volatility is enormous in such phases.

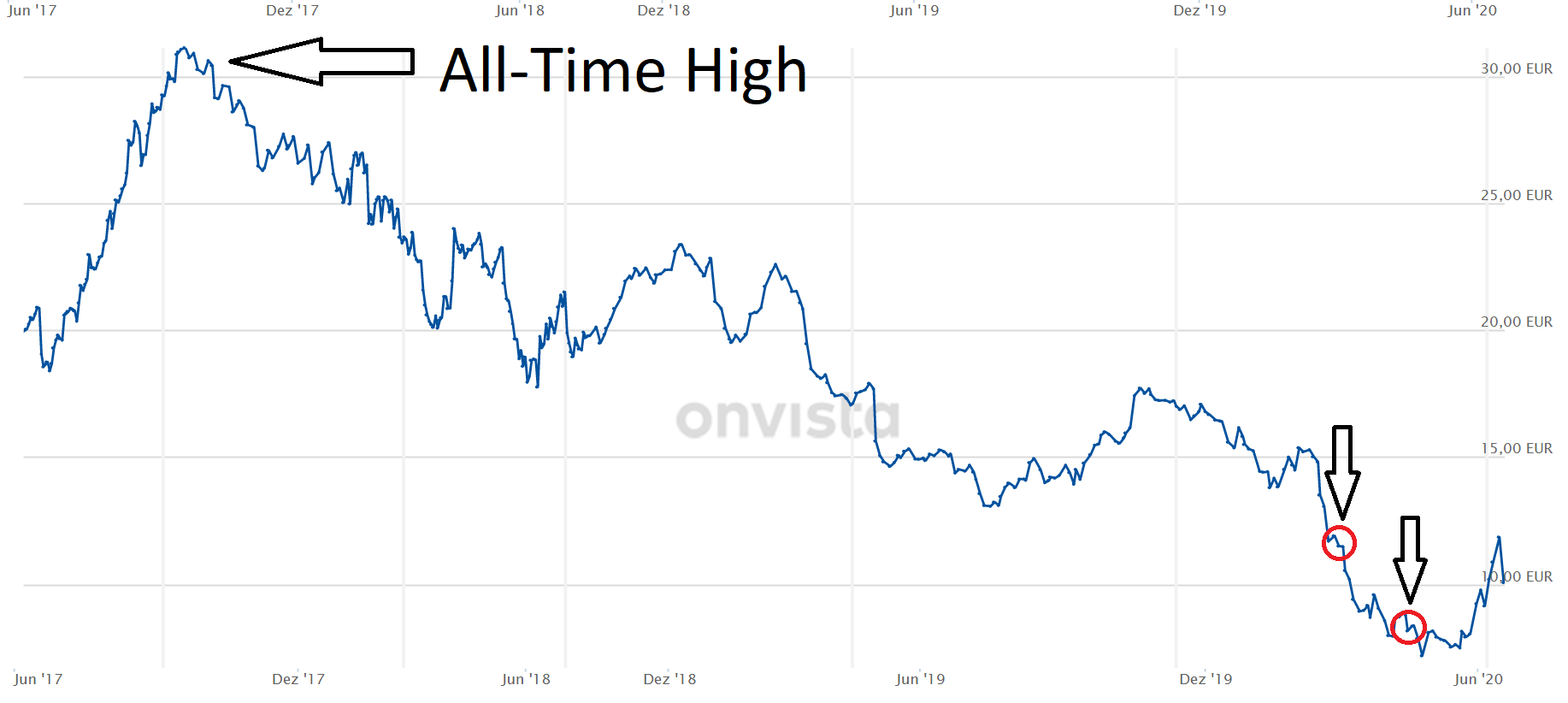

Billionaire Heinz Hermann Thiele and Lufthansa

In the wake of the COVID-19 crisis, the German entrepreneur and billionaire Heinz Hermann Thiele (the Mr. at the picture above) invested massively in the faltering aviation giant Lufthansa. Thiele began buying the shares when they had already fallen to around €12 per share. On March 6, the Group reported a stake of just over 5 percent. As the share price continued to plummet, Thiele doubled its stake. On March 10, he finally held just over 10 percent of Lufthansa and thus became its largest shareholder.

But that was not all. Just three months later, in mid-June, the billionaire increased his stake once again and now holds 15 percent of Lufthansa shares. The purchase price of the shares was approximately €10.5. The average purchase price of all shares should be in the same range. Of course, you should never take past prices as a benchmark, but if Lufthansa should recover, the price could explode. I admire Heinz Hermann Thiele. He’s got guts. He buys when the guns are blazing.

Warren Buffett and Bank of America

Thiele is not the only one who uses such times of crisis and stock market crashes to hunt for bargains. In 2011, when the Bank of America was suffering heavily from the consequences of the financial crisis and was in urgent need of liquidity, Buffett was ready to help. In return for his $5 billion investment, he received 700 million preferred shares with a hefty 6 percent dividend. He also secured the right to convert his preference shares into ordinary shares at a fixed price of $7.14. Buffett exercised this option in 2017 and realized a book gain of more than $10 billion.

My COVID-19 investments

I myself also used the COVID-19 crisis to buy more shares of first-class companies. I took advantage of the first COVID-19 crash and increased my shares in the aristocrats Leggett & Platt and VF. Corp. and built up new positions in Johnson & Johnson and Archer Daniels Midland.

Other companies I bought were Munich Re, Cisco, Henkel, Iron Mountain, and Unilever. Even if things go downhill again, I will keep the companies and not sell them. I love to invest my money in companies with a conservative and defensive business. Their dividends give me a juicy cash flow with which I can buy more shares if prices continue to fall. But I also invest in promising industries like cloud computing.

Time will show us how right we are with our decisions. Whatever investment you decide on, I wish us all the best!