Dear readers, with this article I would like to briefly introduce the W.W. Grainger stock. Founded in 1927 in Chicago by William W. Grainger, the company is one of the biggest players in the business to business (B2B) area. Furthermore, W. W. Grainger was ranked as the best B2B eCommerce site amongst the top 50 Industrial. Accordingly, the company is definitely worth a second look. With this article, I want to give you a first overview and a good basis for your own due diligence.

The business

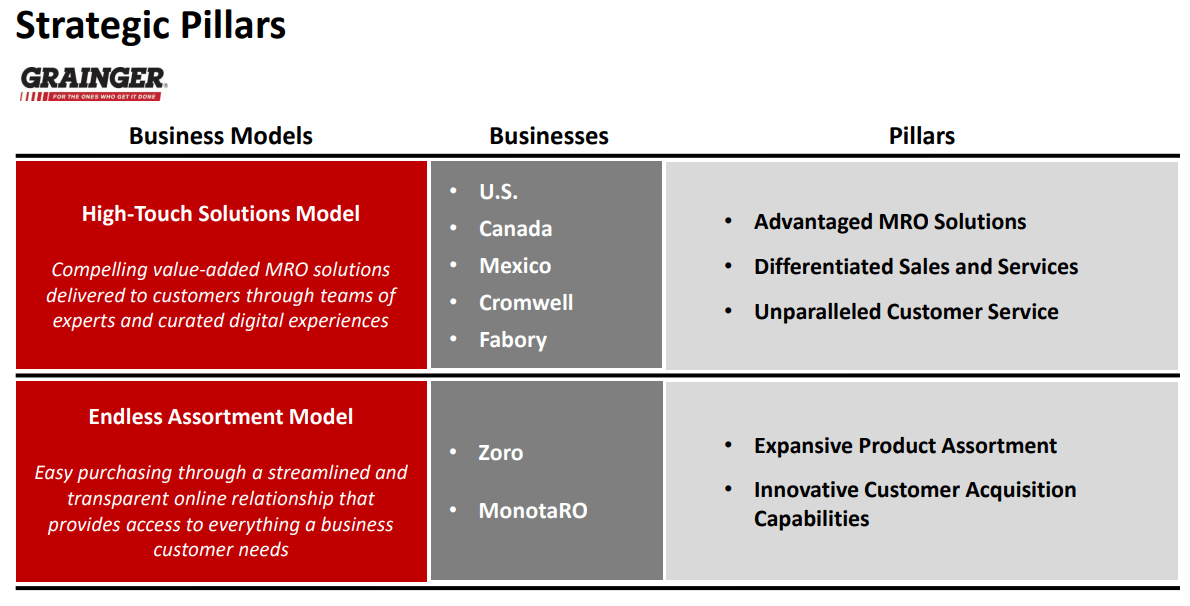

W.W. Grainger is a global distributor of maintenance, repair, and operation (MRO) and related products and services that is mainly active in the B2B area (business to business). The company provides services for many fields such as accounting & finance, communications and investor relations, business development, compensation and benefits, information systems, health and safety, global supply chain functions, security, taxes, human resources, risk management, internal audit, legal and real estate. With MonotaRo in Japan and Zoro Grainger operates purely digital business models. With its Zoro brand, W. W. Grainger operates a pure online shop in the USA, Canada, the Netherlands, and Germany. With Zoro, the company targets primarily small and medium-sized companies. Furthermore, W. W. Grainger holds a majority in the Japanese online shop MonotaRO.

Growth and profitability

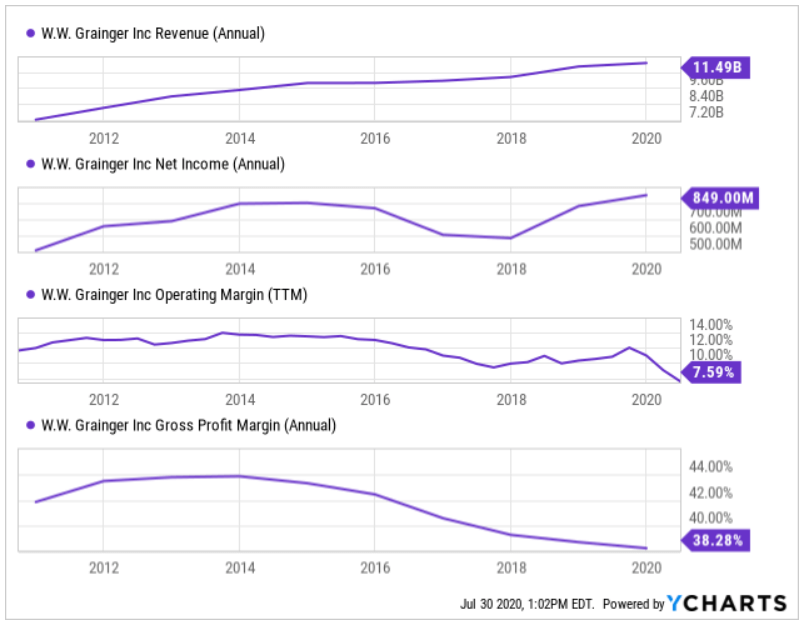

Let us take a brief look at how W.W. Grainger has developed over the last 10 years. Here we see two movements, one positive and one negative. The good thing is that the company has grown operationally and was able to increase revenues and net income considerably. In particular, revenue has grown very steadily from $6 billion in 2009 to $11.4 billion in 2019. Also in 2020, the revenue should increase slightly to $11.6 billion. At the same time, however, the company has obviously lost profitability. Both operating and gross margins have declined in recent years.

In the short and medium-term, margins will probably continue to fall. This is what Tom Okray (Senior Vice President and CFO) and D.G. Macpherson (CEO) said in the company’s last earnings call. According to the statement, the current lower than expected margin in the US segment was driven primarily by three factors: pandemic-related headwinds, tariff fuel cost inflation, and the impact of the company’s rescheduled national sales meeting.

Dividend Scoreboard W.W. Grainger stock

The W.W. Grainger share is particularly interesting for dividend investors. Just a few weeks ago, in July 2020, the company raised its quarterly payout by 6.3 percent from $1.44 to $1.53. With a long dividend history and a low payout ratio, the company has an excellent dividend scoreboard. Only the yield is somewhat low currently:

- Dividend Growth: 48 Years

- Dividend Yield: 1.79 percent

- 10 Year Yield on Cost: 5.3 percent

- 10 Year Growth Rate: 12.30 percent

- Payout ratio based on profit: 52 percent

- Payout ratio based on FCF: 40 percent.

Rock-solid balance sheet

If we are talking about what I think is great about the company, then that is the absolutely solid balance sheet. A debt ratio of about 33 percent is solid. But look at what a mountain of treasury stock W.W. Grainger sits on. Currently, these shares have a value of almost $8 billion. In contrast, the company has debts and liabilities of just $5 billion. So financially, shareholders do not have to worry about the company.

The W.W. Grainger stock is slightly overvalued

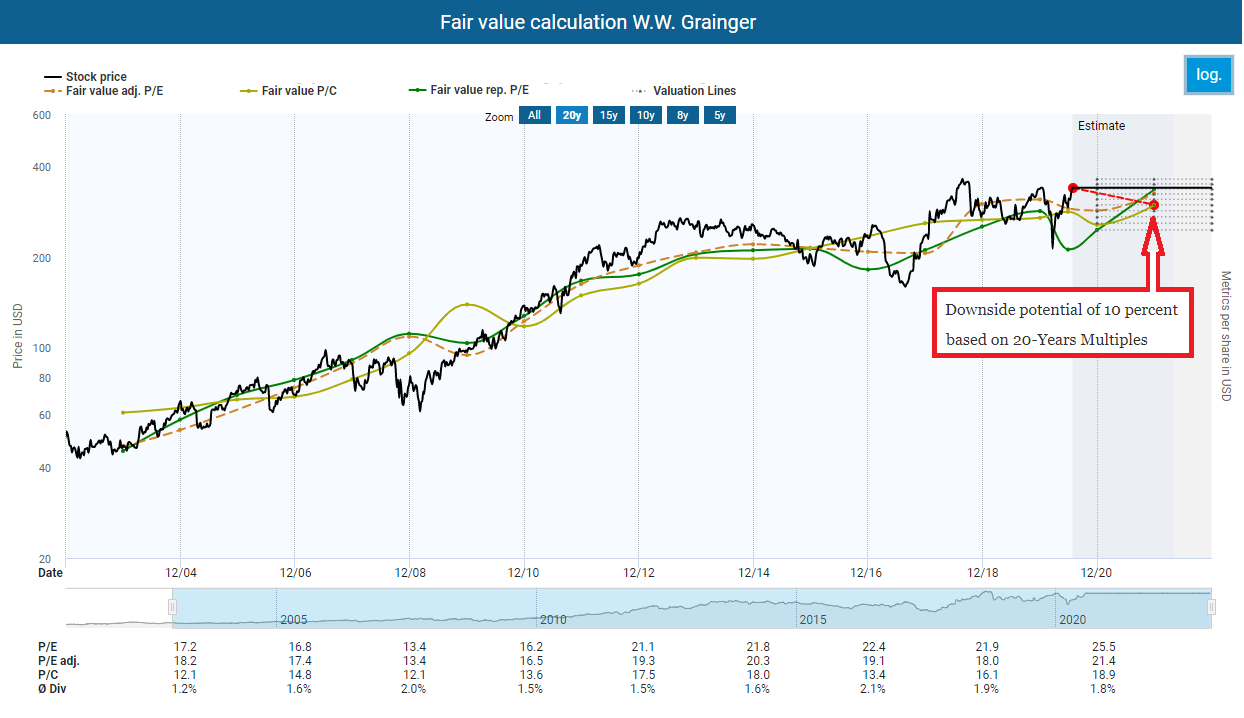

As is so often the case at present, there is one major problem with operationally well-positioned companies and that is valuation. The same goes for W.W. Grainger. If you look at the fair values based on cash flow and earnings, you can see that the company is undervalued from time to time. Currently, W.W. Grainger is again overvalued. Therefore, it might make sense to wait for a price correction (as so often with the risk that the share price will never reach the current prices again).

Time to do your due diligence

Has W.W Grainger caught your interest? Attractive dividend yields should not be the only reason to buy shares of a company. Instead, you must carry out careful due diligence before every purchase. The Internet offers you excellent opportunities in this respect.

My analyses here on the TEV Blog are an excellent way to start (click here). You can also contact me here or ask the community in the comments if they can help with your due diligence.

Otherwise, I use tools like those from Dividendstocks.cash and Seeking Alpha to do further research. You can also find me and my analyses on these platforms. We also have a small but lovely group on Facebook that you can join. We share there only fundamental analyses of companies from various sources. So there is no spamming or anything like that.

Did you like the article? Stay tuned for the following content… It is all completely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.