Welcome to a new overview of upcoming ex-dividend dates. Like every week, I want to show you some stocks that will go ex-dividend in the next days. I’ll also review a few companies that are currently in the focus of investors or that have an attractive fundamental valuation. Additionally, I’ll give you some insights into my retirement portfolio and/or share my thoughts and experiences about individual companies with you. Today I will talk a bit about the latest developments of the TEV blog and about two particularly successful companies. Enjoy 🙂

Why yields are a simple way to screen companies

Dividends are a great thing. Even in bad stock market times, they provide a juicy cash flow per month. If you want to benefit from dividend payments as quickly as possible, you must pay attention to the ex-dividend dates. This date is the day on which shares are traded without their subsequent dividend value. Only if you owned the stocks on this day are you entitled to receive the dividend.

Usually, there are always exciting dividend companies that are worth a second look. And the dividend yield is an excellent way to get an initial overview of companies that may be worth further due diligence. To help you get started, at the end of each week, I will publish the ex-dividend dates for the coming week of individual companies here in the TEV blog.

Why I handpick and double-check the upcoming ex-dividend dates next week

I have recently noticed that many databases do not indicate the respective numbers and dates correctly. Spontaneous dividend cuts, in particular, are only partially taken into account, or in some cases, not at all. As a result, the value of such overviews dwindles enormously.

Therefore, I’ve decided to select individual companies by hand and check the dates and dividend yields on the company websites, which means more work for me but increases the value of this section enormously, so it is worth it 🙂

Because I’ve been asked about it by some of the readers: I don’t, of course, decide my investments based on whether a company goes ex-dividend or not. This overview is simply a way to screen companies regularly. By double-checking the current dividend yields, I scan the business development of companies more or less once a quarter and see if anything significant has changed in the companies. In the end, however, comprehensive due diligence always decides whether I invest or not.

Ex-Dividend Dates (35th calendar week)

As always, you’ll find some handpicked exciting ex-dividend dates below.

| Company | Payment Date | Yield | In my retirement portfolio |

|---|---|---|---|

| Monday, August 24, 2020 | |||

| Brunswick Corp. (BC) | September 11, 2020 | 1.48% | NO |

| Equifax Inc.(EFX) | September 15, 2020 | 0.95 | NO |

| Johnson & Johnson (JNJ) | September 09, 2020 | 2.7% | YES |

| Prudential Financial (PRU) | September 17, 2020 | 6.37% | NO |

| Tuesday, August 25, 2020 | |||

| ACCO Brands Corp. (ACCO) | September 18, 2020 | 3.8% | NO |

| YUM! Brands (YUM) | September 11, 2020 | 2% | NO |

| Sun Life Financial Inc.(SLF) | September 30, 2020 | 3.9% | NO |

| S&P Global Inc. (SPGI) | October 10, 2020 | 0.75% | NO |

| Ritchie Bros Auctioneers (RBA) | September 16, 2020 | 1.38% | NO |

| Wednesday, August 26, 2020 | |||

| Barnes Group Inc. (B) | September 10, 2020 | 1.64% | NO |

| China Mobile (CHL) | September 10, 2020 | 5.6% | NO |

| Thursday, August 27, 2020 | |||

| Analog Devices Inc. (ADI) | September 09, 2020 | 2.1% | NO |

| Corning Incorporated (GLW) | September 30, 2020 | 2.73% | NO |

| Evercore Inc.(EVR) | September 11, 2020 | 3.7& | NO |

| The Kraft Heinz Co.(KHC) | September 25, 2020 | 4.52% | NO |

| NextEra Energy Inc. (NEE) | September 15, 2020 | 2% | NO |

| Flowers Foods (FLO) | September 11, 2020 | 3.2% | NO |

| NetEase (NTES) | September 18, 2020 | 1.65% | NO |

| Parker-Hannifin (PH) | September 11, 2020 | 1.71% | NO |

| Whirlpool (WHR) | September 15, 2020 | 2.6& | NO |

| Friday, August 28, 2020 | |||

| Barrick Gold Corp. (GOLD) | September 15, 2020 | 0.93% | NO |

| Dover (DOV) | September 15, 2020 | 1.8% | NO |

| Nike (NKE) | October 01, 2020 | 0.9% | NO |

| Union Pacific Corp. (UNP) | September 30, 2020 | 2% | NO |

| FactSet Research Systems (FDS) | September 17, 2020 | 0.85% | NO |

| Newell Brands (NWL) | September 15, 2020 | 5.5% | NO |

| Stag Industrial (STAG) | September 15, 2020 | 4.5% | NO |

| Fortune Brands Home & Security (FBHS) | September 16, 2020 | 1.15% | NO |

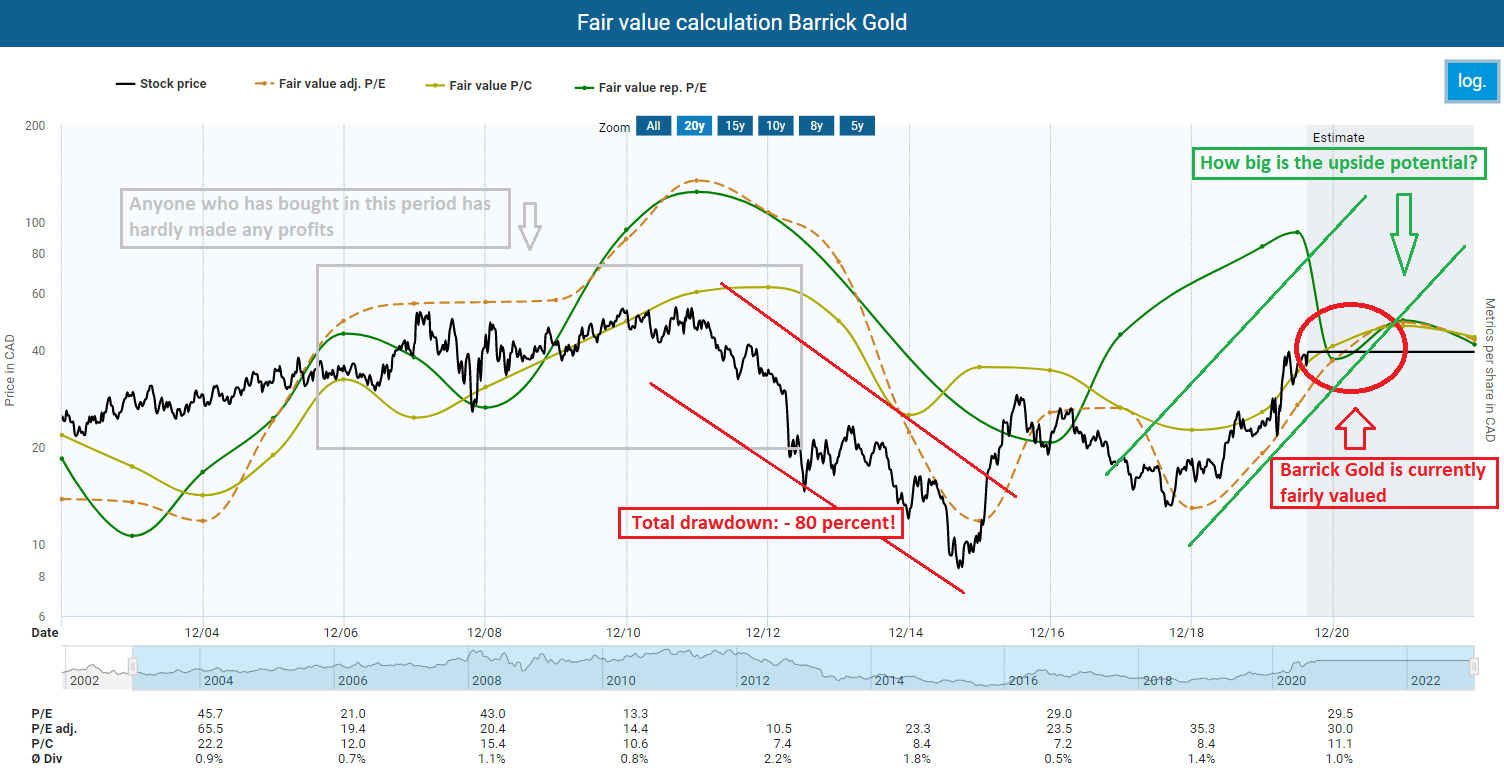

Gold Gold Gold Gold and why I don’t invest in Barrick Gold or similar stocks

As you may know, in this section, I like to write about general topics that are currently relevant and, at best, concerning the companies that go ex-dividend. A development that mainly affects the Canadian company Barrick Gold is the rally of the gold price. The price per ounce rose above USD 2000 – a new record. Investors have been arguing for years about the advantages and disadvantages of investments in gold.

Did Buffett change his opinion about gold?

A naysayer, for example, was Warren Buffett. Warren Buffett had been skeptical about gold in the past, also because unlike dividend stocks, it does not offer a payout. This is one of Buffett’s famous quotes:

[Gold] gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.

Market participants were all the more astonished about Berkshire Hathaway’s 1.2 percent stake in Barrick Gold. According to its quarterly 13F filing, Berkshire Hathaway bought more than 20.9 million shares of Barrick Gold, worth roughly USD 563 million. But whether Warren Buffett changed his mind here is not entirely clear. Todd Combs and Ted Weschler, who are to run Berkshire in the future, or other managers may have made the purchase.

Will I invest in gold now?

I will at least not change my investment strategy just because of the current developments. I don’t follow every hype. The rally is great, especially for those who invested early. But I simply look for cash flows for the future and invest in companies that promise me such things. As I have said before, I am not necessarily looking for an above-average return (if I wanted the best possible performance, I would invest in ETFs). Companies like Barrick Gold, whose entire business model depends solely on the price of one commodity, are nothing to my long-term buy and hold approach. Look at the fundamental development of the company, which doesn’t look good.

Johnson & Johnson

Compare the long-term development of Johnson & Johnson. I feel much more confident with such companies in my portfolio. They might be more tedious but still bring an excellent return. I love it when the share price is close to its historical multiples and slowly but steadily increases. I do not need adventures. The steady cash flow of such excellent companies is enough for me.

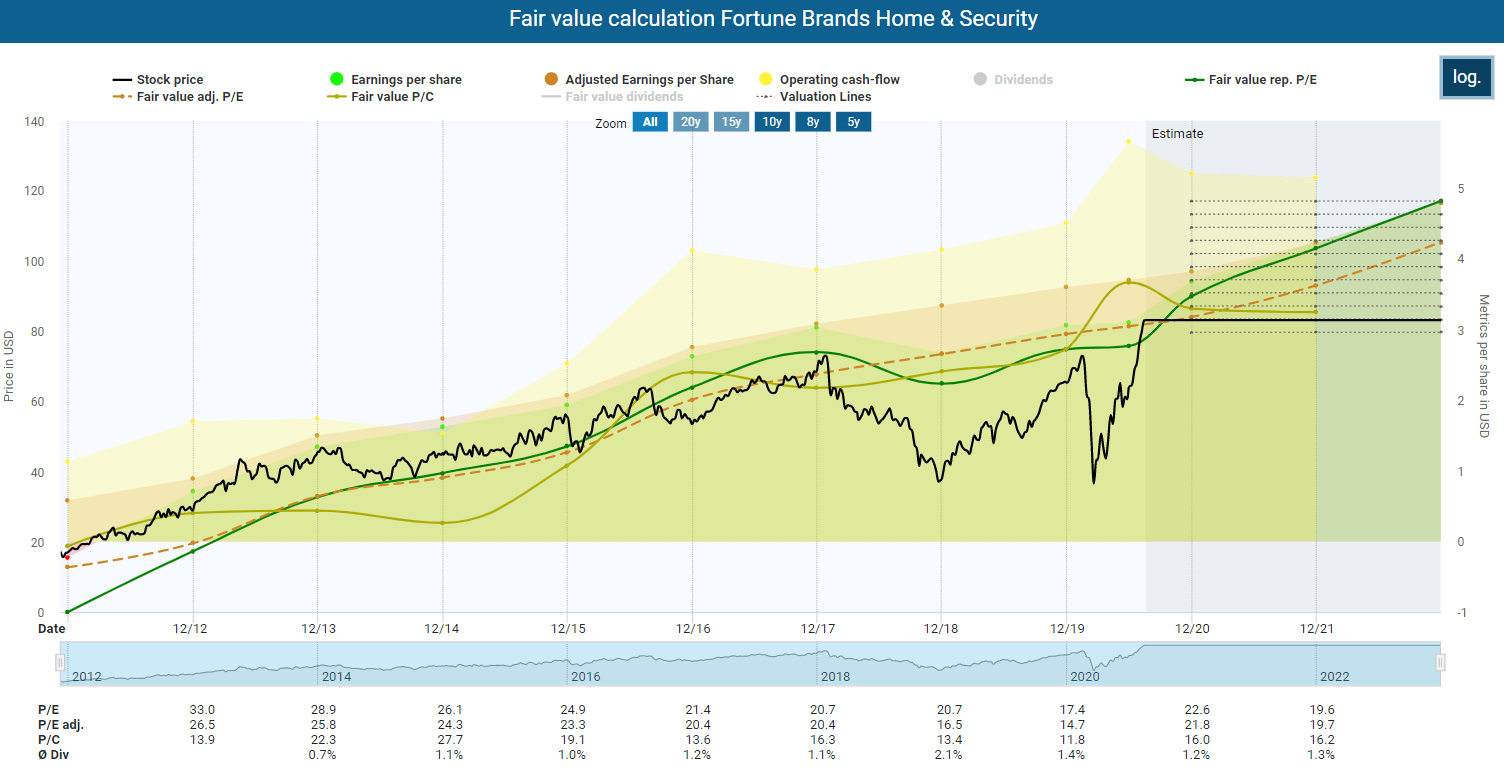

Fortune Brands Home & Security

Fortune Brands is a household and security consumer goods company. It was formed after the spin-off from Fortune Brands, Inc. Did you know that the roots of the company go back to 1890? Fortune Brands was once part of the American Brands company. American Brands, in turn, was initially called American Tobacco Company. The American Tobacco Company restructured itself into a holding company in 1969 and sold the tobacco division to British American Tobacco in 1994.

Business model

Fortune Brands’ Global Plumbing Group (GPG) is a multi-brand, multi-channel, and multi-geographic plumbing company. The Group manufactures, assembles, and distributes faucets, showers, accessories, tubs, sinks, waste disposal, and sanitary products in North America, China, New Zealand, South Africa, and Europe. The brands include Moen, Perrin & Rowe, Riobel, ROHL, Shaws, and Victoria + Albert

The segment for doors and security offers various products. These include fiberglass and steel entry door systems and urethane millwork products such as locks, security devices, and containers, as well as outdoor performance materials used in decking, railing, and fencing products. The iconic Master Lock and SentrySafe brands, for example, are known worldwide for their expertise in locks, security devices, including electronic security products and security containers.

The vast majority of MasterBrand Cabinets’ sales come from two key channels: kitchen and bathroom retailers as well as stocked cabinets and vanity products.

How did things go in the past?

Let’s take a look at how Fortune Brands Home & Security has developed. In short, the development is extremely positive. The company has massively increased its earnings per share. In 2011, earnings per share were minus USD 0.23. In the meantime, however, they have reached USD 3.1. Massive share buybacks, which spread the profit over fewer shares, have also contributed to this. Since 2013, the company has reduced its shares from 171 million shares to 138 million shares. But the company is also convincing beyond such gimmicks. The revenue rose from USD 3 billion in 2011 to an expected USD 5.7 billion this year. Thus, the revenue has almost doubled in 10 years. Besides, Fortune Brands Home & Security generates massive cash flow. Free cash flow has more than quintupled in the last ten years and is now at just under USD 5 per share. Also, the company has consistently increased its margins in recent years. The company is accordingly, profitable.

Young dividend payer

Due to its founding history, Fortune Brands Home & Security is still a very young independent dividend payer. The dividend scoreboard is still quite attractive:

- Dividend Yield: 1.15%

- Dividend growth: 8 Years

- Payout ratio: 25%

- 5 Year Growth rate: 12.89%.

Only the initial yield is somewhat too low. Anyone who was courageous and bought shares during the Corona crash could secure a yield of 2.7 percent, for example. That is more than twice the current dividend yield.

Fair value calculation

I’m sure you already know. A company growing so fast can’t come cheap. It’s true, Fortune Brands Home & Security is no bargain. But it is also not really overpriced. From a fundamental point of view, you get the shares at a fair value. Due to the expected growth, the shares should become even more valuable in the future. However, in the past, the company has been much cheaper.

Time to do your due diligence

Has a company caught your interest? Attractive dividend yields should not be the only reason to buy shares of a company. Instead, you must carry out careful due diligence before every purchase. The Internet offers you excellent opportunities in this respect.

My analyses here on the TEV Blog are an excellent way to start (click here). You can also contact me here or ask the community in the comments if they can help with your due diligence.

Otherwise, I use tools like those from Dividendstocks.cash and Seeking Alpha to do further research. You can also find me and my analyses on these platforms. We also have a small but lovely group on Facebook that you can join. We share there only fundamental analyses of companies from various sources. So there is no spamming or anything like that.

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

That said, feel free to let us know if I have overlooked an attractive stock or you know of a stock that is particularly attractive and where the ex-dividend date is coming up.

Is a stock here attractive for you? If so, let the community also know and write a comment.

You can also share this post with your favorite network: