In this fundamental Hormel Foods stock analysis, we will check whether Hormel Foods is on the right track and whether you can expect further increases in stock price and dividends in this stock analysis.

Hormel Foods stock is anything but an old piece of ham in the long run. Investors have made more than 17,000 percent gains on the stock over the past 40 years. And even within the last ten years, the iconic breakfast meat “SPAM” producer brought it to a cumulative total return of 273 percent, representing an annual return of 15.2 percent.

In recent years, however, Hormel Foods stock has faced headwinds. In the period from 2016 to 2017, for example, the stock lost a full 30 percent in value. Even though Hormel Foods has recovered its losses and with a stock price within reach of its all-time high of USD 52, the company has to fend off competition and industry-typical risks and adapt to the changing needs and dietary habits of consumers.

The business model: How Hormel Foods generates money

Among the major food producers, the manufacturer of food and meat products, founded in 1891, plays a somewhat minor role with a market capitalization of USD 22.5 billion (Nestlé, for example, brings it to USD 267.1 billion). But that is not meant negatively. In fact, Hormel Foods has successfully built a niche and steadily expanded it over the decades. Hormel Foods divides its business into four segments: “Grocery Products,” “Refrigerated Foods,” “Jennie-O Turkey Store,” and “International & Other,” whereby you can find individual brands in several segments simultaneously.

„Grocery Products“

In the “Grocery Products” segment, Hormel Foods bundles the manufacture and sale of long-life food products predominantly sold in retail stores. This segment is responsible for 24 percent of total sales. The best-known brands are the breakfast meat “SPAM” and the peanut butter SKIPPY.

„Refrigerated Foods“

“Refrigerated Foods” includes branded and unbranded pork, beef, chicken, and turkey products that Hormel Foods supplies to delis, retailers, and other commercial customers. Overall, Hormel Foods’ “Refrigerated Foods” segment accounts for 54 percent of total sales.

„Jennie-O Turkey Store“

The “Jennie-O Turkey Store” segment generates nearly 14 percent of total sales. Here Hormel Foods sells “Jennie-O Turkey Store” brand turkey products, which date back to the company of the same name acquired in 1986 and which now operates as a subsidiary of Hormel Foods. The customers are mainly in the retail and foodservice sectors.

„International & Other“

The “International & Other” segment essentially comprises the international business activities of Hormel Foods. It is the smallest segment and is responsible for just 6.4 percent of sales. Hormel Foods uses joint ventures and individual strategic foreign sites in Australia, Brazil, Canada, China, Japan, and the Philippines for its global activities. Hormel Foods exports its products to international customers but also uses its supply chains in some cases.

Challenges and outlook

A weak point in Hormel Foods’ business is its strong focus on the U.S. market, where Hormel Foods generates about 94 percent of its sales. The change in the regulatory environment regarding “meat production” and meat processing and possible tax increases on meat products could severely affect Hormel Foods. Hormel Foods could reduce its dependence on the U.S. market through international expansion. However, the existing value chain and intense global competition make this endeavor difficult.

Establishment of an efficient value chain

A problem for international expansion is the establishment of an efficient value chain. Hormel Foods, for example, relies on long-term, predictable supply contracts for pigs, of which it buys more than 95 percent from other companies. Although its subsidiary Jennie-O Turkey Store can produce almost 80 percent of its total turkey demand, in this case, Hormel Foods also bears the risk of fluctuating food prices. Likewise, a drop in turkey prices can squeeze profit margins. Shareholders felt the impact of such fluctuations firsthand in 2017 when a 60 percent drop in turkey prices caused profits in the Jennie-O Turkey Store segment to plunge 24 percent.

With the segment contributing nearly 25 percent of total earnings at the time, this adversely impacted the total profit growth. That dependence appears to have fallen, not least because of wildly fluctuating turkey prices and sales volumes, as Jennie-O Turkey Store now contributes only about 10 percent of the company’s profit.

Hormel Foods’ strategy is to establish strong brands and develop new products to offset the impact of price fluctuations in upstream commodity markets. Brand strength is a crucial aspect of this. For example, Hormel Foods brands hold the number one or two spots in sales in more than 35 categories.

Dependence on individual customers

Another critical point is a specific dependence on individual customers. In 2020, for example, Walmart was responsible for 14.6 percent of sales (in 2019, it was “only” 13.5 percent). In some individual segments, Hormel Foods generates more than half of its sales with just five customers. For example, just five customers are responsible for 44 percent in the Grocery Products segment, 35 percent in the Refrigerated Foods segment, 54 percent in the Jennie-O Turkey Store segment, and still 15 percent in the “International & Other” segment. Due to the high level of focus, the loss of a significant customer can quickly impact total sales.

Changing eating habits of consumers

Besides, Hormel Foods is directly exposed to the changing eating habits of consumers. The renunciation of meat and the trend toward vegetarian or fresh products are particularly explosive for companies like Hormel Foods. But the management has recognized the signs of the times and is responding to this trend with meat-free products, which it groups under the “Happy Little Plants” brand.

Hormel Foods is also expanding its portfolio of Healthy Living/Wellness brands. These include Valley Fresh (without glutamate, gluten, preservatives, or artificial ingredients), Vital Cuisine (protein shakes, meals with a specific nutrient composition), and Natural Choice (minimally processed products without artificial ingredients in the low-price sector).

Can Hormel Foods continue to grow its revenues?

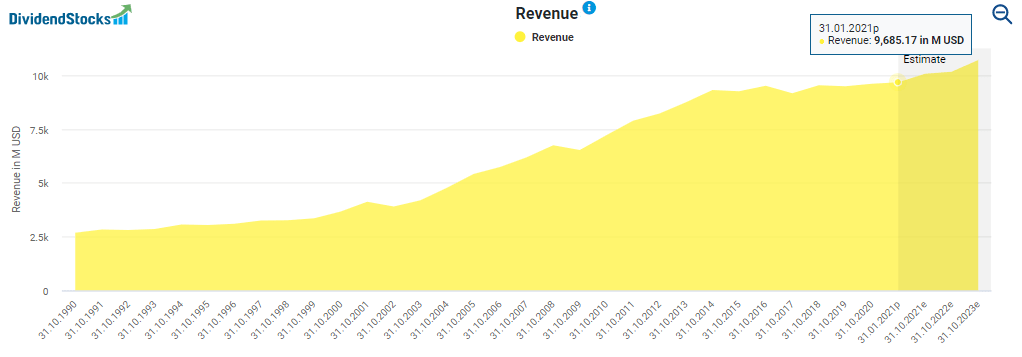

Hormel Foods has grown enormously in recent decades, increasing revenue from USD 2.68 billion in 1990 to USD 9.6 billion in fiscal 2020. More recently, however, growth has mostly stalled. In 2014, for example, sales were only slightly lower than today at USD 9.3 billion.

Only the Refrigerated Foods segment has grown over the last three years. The other segments showed hardly any growth or have even shrunk, such as “Jennie-O Turkey Store”.

However, at least in the most recent quarter, all segments increased and contributed to the growth of 3 percent. The 7 percent increase in sales in the “Grocery Products” segment was particularly noteworthy. In the coming years, Hormel Foods intends to grow further. Analysts expect sales here to rise to USD 10.719 billion in 2023.

New growth thanks to Kraft Heinz?

New (price) growth for Hormel Foods stocks is expected to come from Kraft Heiz’s nut business, which Hormel Foods plans to acquire, including the “Planters,” “Cheez Balls” and “Corn Nuts” brands, for USD 3.35 billion. This sum represents more than 10 percent of its market capitalization. Sales of the acquired brands amounted to USD 1 billion in 2020. These brands are expected to provide Hormel Foods with synergies worth USD 50-60 million by 2024, improving margins and cash flows. The acquisition price is nevertheless steep, as Hormel Foods paid nearly 17 times EBITDA of circa USD 220 million. Whether the salty nut snacks, which are rather considered unhealthy, are in line with the current “trend” can also be doubted.

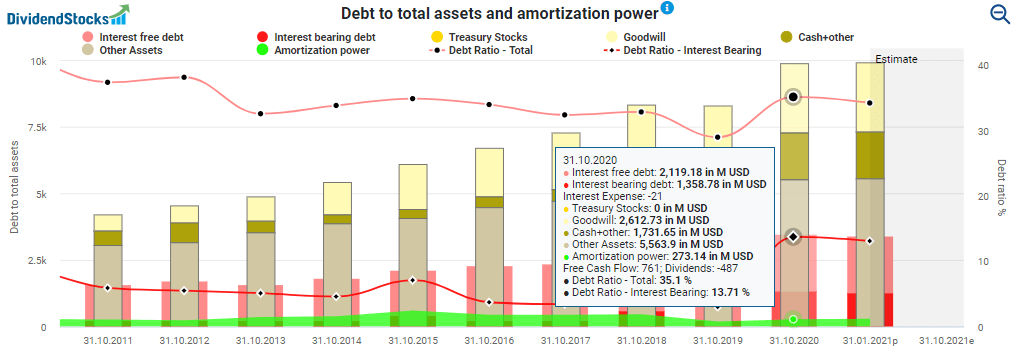

Conversely, Hormel Foods can diversify its product portfolio with the largest deal in its history and further reduce its dependence on meat products. Financially, Hormel Foods is in a strong enough position to handle an acquisition of this magnitude. The debt ratio, taking all liabilities into account, is currently at a low 35 percent. Also, Hormel Foods has cash and cash equivalents of USD 1.7 billion, which already covers half of the purchase price.

How profitable is Hormel Foods?

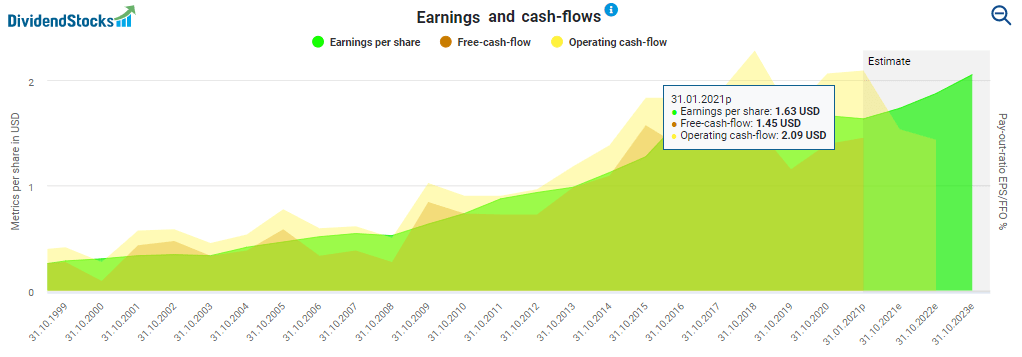

As with sales, Hormel Foods has also lost ground in terms of profitability in recent years. While earnings per share were still USD 1.86 in 2018, they were only USD 1.66 most recently. However, analysts expect earnings to rise again to USD 1.95 per share by 2023.

The profit decline was primarily caused by declining margins, which the company attributed to the challenging turkey rearing environment for “Jennie-O Turkey Store”. Margins are expected to recover in the coming years.

Is Hormel Foods dividend safe?

Hormel Foods pays out dividends quarterly. It has increased them at sometimes decent rates over the past 54 years. This tradition puts it in the illustrious circle of dividend aristocrats. Those noble companies have increased their dividends every year for the past 50 years. The quarterly dividend, for example, increased from USD 0.0219 in 2000 to USD 0.245 now.

After the latest increase from $0.2325 to USD 0.245, shareholders will receive USD 0.98 a year per share, which equates to a dividend yield of 2 percent at the current stock price of around USD 47/48. Over the past ten years, Hormel Foods has increased its dividend by a respectable 16 percent on an annual average basis. However, you should note that the rate of growth has steadily declined in recent years. While the yearly increase was still 10.7 percent in November 2019, the increase amounted to only 5.4 percent in November 2020.

However, with a payout ratio of under 60 percent, there is still room for further increases. Analysts expect the annual dividend to increase to USD 1.06 per share in 2021, an increase of 8.1 percent, which would again be above the previous year’s level. The graph below shows that Hormel Foods stock has a current dividend yield of 2 percent, which puts it in the upper third of the long-term corridor over the past ten years.

Is the Hormel Foods stock favorably valued?

Even though the slightly above-average dividend yield indicates undervaluation, we can see that Hormel Foods stock is currently overvalued as measured by reported and adjusted earnings. If we assume that, despite a material change in the earnings profile, stock prices will track their historical valuation over the long term, the expected adjusted earnings for fiscal 2023 are still subject to a 10 percent risk of a setback. If we consider only the expected earnings for 2021, the fair value difference is even close to 30 percent. The last time Hormel Foods was so clearly overvalued was in 2016. Back then, this resulted in a sharp correction that lasted into 2017.

Conclusion: Hormel Foods stock analysis– expensive and risky at the same time

Hormel Foods has a strong product portfolio and the impressive dividend history of a dividend aristocrat. The current dividend yield is even above average from a historical perspective. However, in my view, the fundamental valuation does not adequately reflect the fundamental challenges of the business. Changing eating habits and industry-typical risks such as dependence on commodity prices are challenging. The focus on the U.S. market can also cause nasty surprises. It is also possible that shareholders will regard the acquisition of Kraft Heinz’s nut products as too expensive and strategically not ideal, which could also put pressure on the stock price. For these reasons, the Hormel Foods stock is currently too costly and risky for me to buy.

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts. You can also share this post with your favorite network: