The Diageo stock is one of the few British dividend aristocrats. It delivered its shareholders an average annual return of over 11 percent over the past decade. Therefore, it is not surprising that price gains. Rising dividends attracted even more shareholders. This lifted the stock price into fundamentally questionable spheres. However, the stock price has corrected significantly from the high of GBP 35.04 reached in mid-2019. The Corona pandemic hit Diageo hard in the first half of the year. But even before, we only saw moderate revenue development. Whether the signs are now pointing to growth again and if you can expect rising prices and dividends as in the past, you can find out in this free Diageo stock analysis.

The business model: How Diageo generates money

Founded in 1997 through the merger of Guinness Brewery and Grand Metropolitan, Diageo is one of the world’s largest spirits groups with over 200 brands. Below we give you an overview of the most important brands and Diageo’s business model.

More than just beer

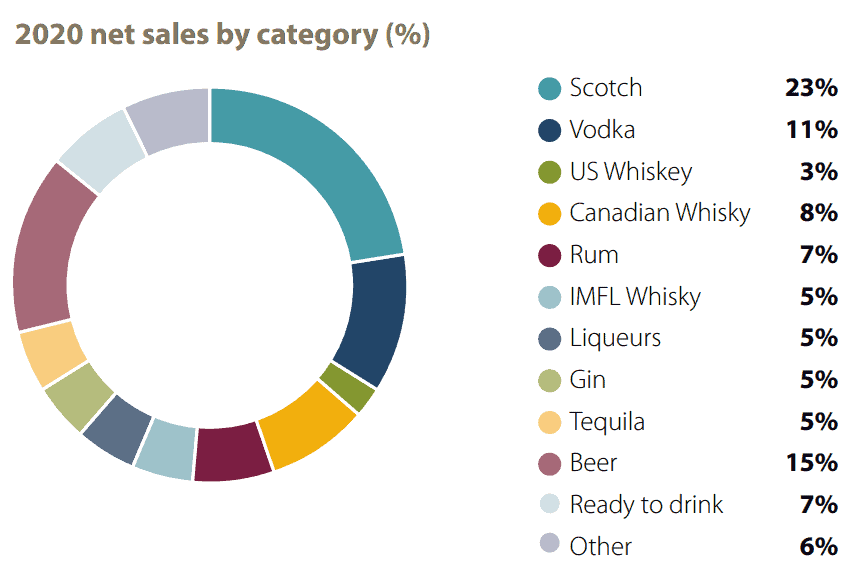

No bar that is well-equipped can run without high-proof beverages from Diageo’s portfolio. In addition to the “Guinness” beer brand, the company owns world-famous brands such as Johnnie Walker (whiskey), Smirnoff (vodka), Captain Morgan (rum), Baileys (liqueur), and Tanqueray (gin). Diageo generates the majority of its sales with whisky from Scotland. The peaty and iconic Lagavulin from the Island of Islay and Talisker from the Isle of Skye are well known. Together with 28 other whisky brands, they account for 23 percent, or almost a quarter, of total sales.

The beer segment contributes 15 percent of total sales. The classic Guinness is joined by the equally well-known brands Harp, Kilkenny, Senator, and Tusker. The third-largest product category is vodka. Here, Diageo generates 11 percent of its revenue with the Cîroc, Ketel One, and Smirnoff. The remaining categories account for the rest of the revenues. As you can see in the overview below, none of them accounts for more than 8 percent of total revenues.

The strengths of the business model

Diageo’s product portfolio is very strongly diversified into different categories of alcoholic beverages, allowing Diageo to operate independently from the development of individual brands and categories, which gives the business certain stability in many markets, for example, in view of the sharp decline in beer consumption. Besides, the many well-known brands ensure a high level of customer loyalty and thus stable market shares at the same time.

Global footprint

Another strength is the company’s global footprint. Diageo is neither dependent on individual markets nor a single region. While North America is the most important region for Diageo, accounting for 39.5 percent of total sales, the regions of Europe (including Turkey) with 21.9 percent, Asia and the Pacific with 19.3 percent, and Africa with 11.5 percent are also significant. With operations in more than 180 countries and over 150 offices, Diageo has built an infrastructure that enables it to respond quickly to developments and consumer behavior changes.

“Global Brands,” “Local Stars,” and “Reserve”

Diageo’s regional flexibility and diverse brands enable a corporate strategy that divides its product offering into three segments: “Global Brands,” “Local Stars,” and “Reserve.” With global brands such as Johnnie Walker, Smirnoff, Baileys, Captain Morgan, Tanqueray, and Guinness, Diageo generates more than GBP 16 billion, or almost40 percent of its total sales. The brands belonging to the “Local stars” and the “Reserve” each generate around 20 percent of total sales. With the “Local stars,” the company aims to address the local markets, while Diageo targets the luxury segment with the “Reserve” category, offering spirits that are not high-proof but also high-priced.

Many different brands as revenue generators allow Diageo to sell stumbling or slow-growing brands on the one hand and to respond to changing consumer needs with acquisitions and takeovers on the other. Diageo recently bought actor Ryan Reynolds’ Aviation Gin brand for GBP 466 million (circa USD 610 million), adding North America’s fastest-growing gin brand to its portfolio.

Diageo in times of COVID-19

That Diageo’s alcoholic beverages are nevertheless not a sure-fire success was something shareholders had to realize during the Corona pandemic, as it neatly screwed up the 2020 fiscal year ending in June. Diageo distinguishes between the off-trade and on-trade channels. The on-trade channel means sales to customers where the beverages are consumed in bars, restaurants, or clubs, all affected by various lockdowns. On the other hand, the off-trade channel refers to sales to supermarkets or licensees of the different brands. The off-trade channel coped much better with the consequences of Corona.

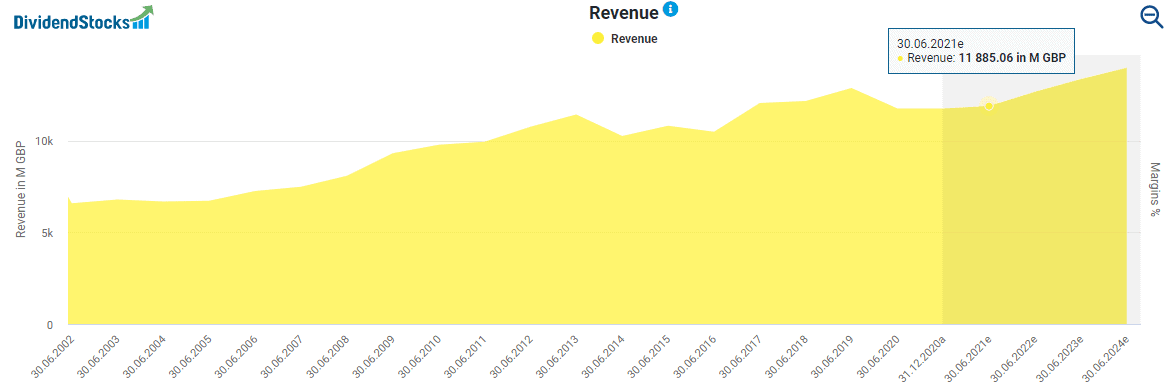

Revenue fell 9 percent

Overall, revenue fell 9 percent to GBP 11.75 billion due to closed bars, restaurants, and canceled events. For fiscal 2021, analysts expect a slight improvement in sales to GBP 11.88 billion and a stronger upward trend in subsequent years. There is some evidence to suggest that Corona’s long-term revenue growth will be short-lived. From GBP 6.5 billion in 2002, sales had almost doubled to GBP 12.9 billion just before Corona.

Diageo’s profits and cash flows also slumped

Because of the Corona-related slump in sales, Diageo’s profits and cash flows also slumped. Above all, earnings were only GBP 0.6 per share in 2020. Compared with the previous year’s profit of GBP 1.3, this represents a decline of 55 percent. However, in the current financial year, which already ends in June, the situation is expected to improve significantly. In the following year, Diageo might even reach pre-crisis levels. After that, things start to look up further.

The impact of Brexit on Diageo’s stock

While the Corona pandemic had a painful impact on business performance, Brexit is likely to have less critical implications. Diageo sells all over the world and only generates about 6 percent of its revenues in the U.K. Of some concern to shareholders is a potential trade restriction between the U.K. and Ireland, resulting in tens of millions of pounds (GBP) in additional costs for Diageo. However, given total revenues of just under GBP 12 billion, not too much is at stake here either.

The stock price was also mostly unimpressed by the respective developments in the dispute over a trade agreement between the U.K. and the E.U. on the whole, which indicates that the outcome of Brexit negotiations plays a rather subordinate role for the long-term success of the business. When the Brexit vote was announced in June 2016, Diageo stocks rallied, rising to an annual high of almost GBP 20, as many shareholders hoped for positive effects from the British pound’s potential devaluation. As a globally active British company that reports in GBP, Diageo could even indirectly benefit from Brexit. However, this is somewhat hypothetical. It might be that the pound will appreciate inversely after the Brexit is completed.

How secure is the Diageo dividend?

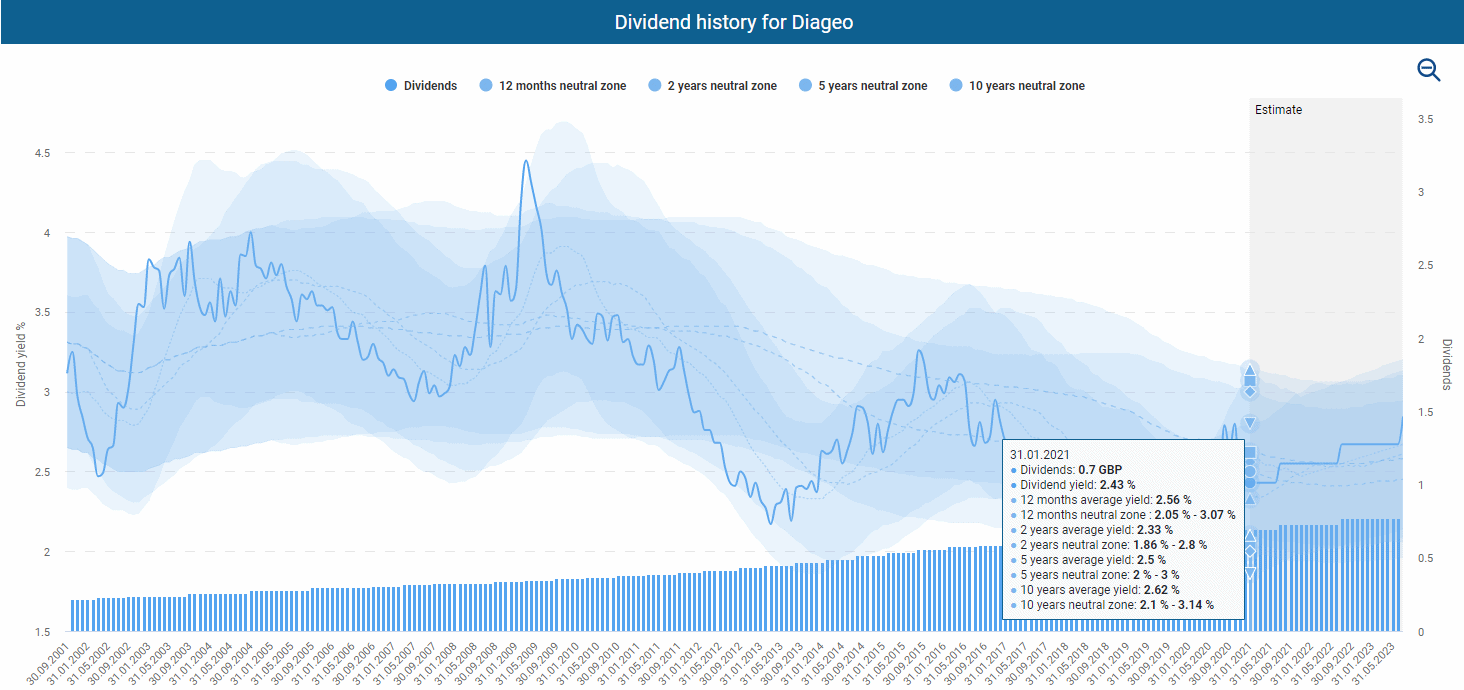

Diageo belongs to the illustrious circle of dividend aristocrats that have increased their payouts to shareholders every year for at least 25 years. Since 2000, the dividend has increased from £0.2 to now £0.7 per share. Dividend payments are made as interim and final dividends semi-annually in April and October, with an amount of GBP 0.2741 and GBP 0.4247 in 2020. The ratio of distributions is generally 40:60, and Diageo most recently increased the interim dividend by 5 percent in early 2020, representing a 2 percent increase in the full-year dividend. At the current stock price of GBP 29.14, this results in a dividend yield of 2.23 percent, which is in line with recent years’ longer-term trends.

Analysts expect Diageo to pay a dividend of GBP 0.73 per share to shareholders next year, which would represent an increase of just under 4 percent. That would put the increase in line with increases in past years. There is currently no scope for larger increases either. On an annualized basis, Diageo has to distribute more than 100 percent of profit and free cash flow to shareholders for the dividend. This is related to the drop in sales because of Corona. Once the business has returned to normal, payout ratios should again settle at 50 and 60 percent. However, you should not expect a dividend turbo with annual double-digit growth rates in the future. On the other hand, Diageo is characterized by reliable dividend increases, which is a plus, especially for shareholders with a long-term perspective.

Is the Diageo stock fairly valued?

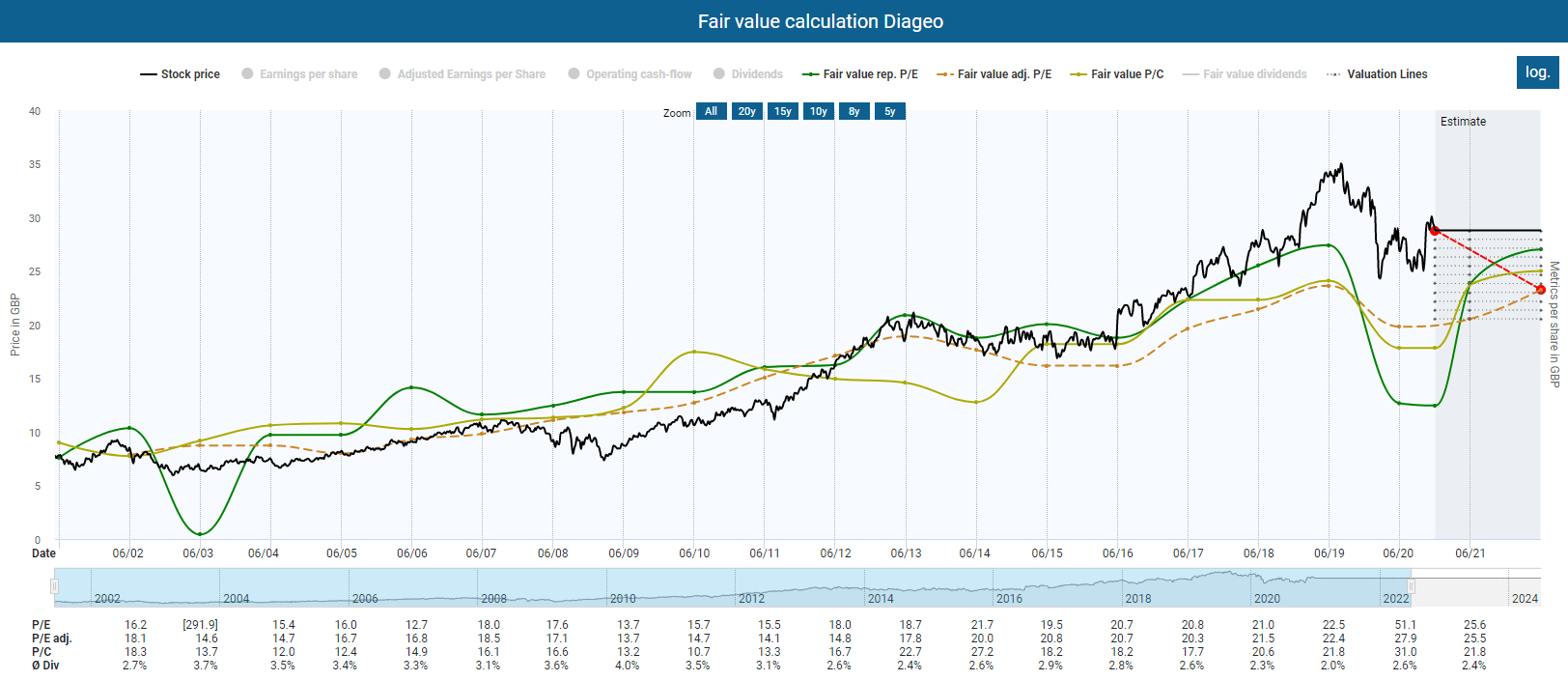

In recent years, Diageo has been perceived as a quality company for which shareholders had to pay a premium price, justifying the relatively high multiples(e.g. P/E ratio above 20) for an instead moderately growing company. However, in the graph below, you can see that even companies like Diageo go through phases of undervaluation. So I think it’s unwise to ignore historical averages, as stocks tend to return to those values over the long term. Even if we assume a significant improvement and a return to old earnings in 2023, Diageo´s stock currently appears overvalued.

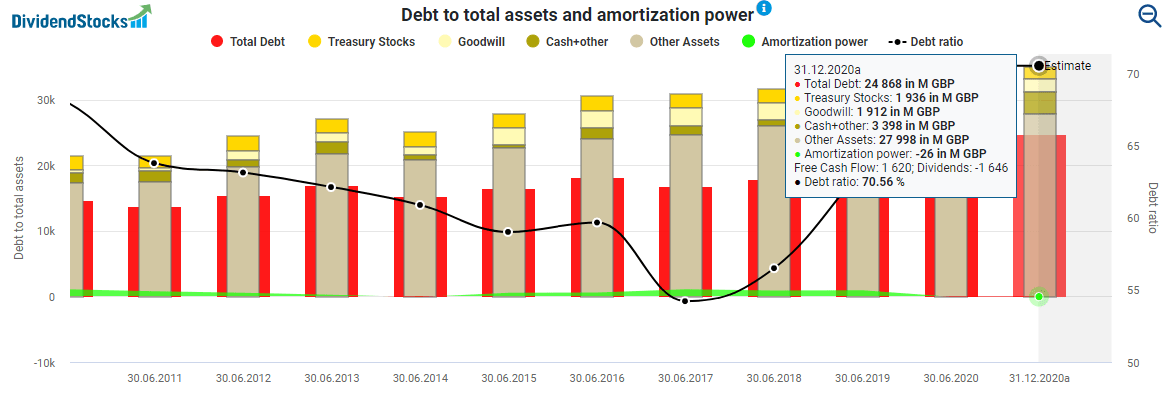

Another negative aspect is the debt ratio of over 70 percent, which is too high for my taste. The debt, including all liabilities of almost GBP 25 billion, was offset by an amortization power of not even GBP 1 billion in recent years. Although borrowed capital is cheaper than ever, I would like to see an improvement here in the medium term.

Conclusion Diageo stock analysis: Expensive and no longer to everyone’s taste

Diageo has an excellent portfolio with strong brands and can look back on a reliable sales and earnings performance. Furthermore, shareholders benefit from annual dividend increases and a respectable dividend yield of over 2 percent at the moment. While the stock is below its 2019 all-time high, the fallout from the Corona pandemic continues to plague Diageo. While I added some more Diageo stocks to my retirement portfolio in August, I am currently refraining from further purchases due to the current valuation level and high debt ratio. Conversely, it is uncertain whether the stock price is going to fall significantly again to offer a better entry point. Anyone interested in Diageo shares as of now can buy in smaller tranches via a savings plan.