The Novo Nordisk stock is a basis investment for many long-term and conservative investors, as dividends and stock price gains have added up to a decent return of more than 280 percent over the past ten years, equaling an average annual return of 14.5 percent. In particular, Novo Nordisk’s strong position in the diabetes market makes it look like a safe bank for many shareholders, who are willing to pay a hefty price per share, which is currently close to its all-time high of DKK 452(73.73 USD). In this fundamental Novo Nordisk stock analysis, we check whether you can expect further price gains and dividend increases for the Novo Nordisk stock.

Diabetes

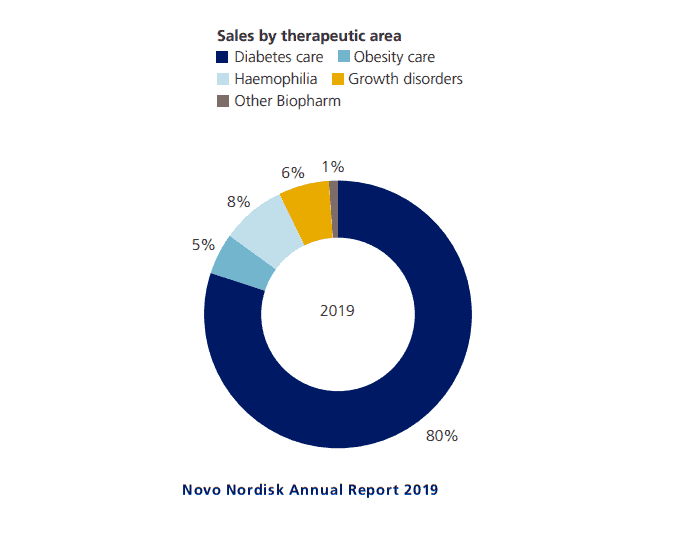

The largest business area is diabetes. Here, Novo Nordisk generates 80 percent of total revenues, which makes it the clear global market leader. Diabetes is a disorder of human carbohydrate metabolism, with type 2 diabetes being the most common, accounting for 90 percent of all diabetes cases. Novo Nordisk combats the symptoms of this disease with various drugs and devices. Devices such as “insulin pens” aim to supply insulin to people living with diabetes, enabling them to live mostly normal life with the disease. Novo Nordisk also offers drugs that regulate insulin balance or insulin secretion. These include, in particular, the GLP-1 agonist, which stimulates the pancreas to secrete insulin.

Hemophilia

Another pharmaceutical area is the blood coagulation disease hemophilia. In this disease, which is usually hereditary, blood clotting is impaired. People affected by the disease, therefore, bleed for longer than people with intact blood clotting. The hemophilia business accounts for 8 percent of total revenues. Novo Nordisk develops and markets pharmaceutical products and maintains the HaemCare platform, where people affected by hemophilia can find information on living with hemophilia and its treatment options (using Novo Nordisk products).

Obesity

A business segment created more by accident is tackling obesity. Novo Nordisk noticed that many patients lost weight during the treatment with its diabetes drug Semaglutid. This finding led to the creation of a new business unit, consisting of a portfolio of anti-obesity drugs. The drug Saxenda is now the most widely sold anti-obesity medication and had a market share of 32 percent in 2019. However, its share of group revenue is still low at just 5 percent.

Growth disorder

Growth Disorder is responsible for 6 percent of total revenues. Novo Nordisk markets and develops products such as injection devices as together with matching hormone therapies to treat, for example, growth disorders due to other underlying diseases or hormone deficiency.

Prospects and weaknesses of the business model

Novo Nordisk is benefiting from growing prosperity globally, which has the negative side effect of causing severe widespread diseases such as obesity and diabetes. People who have diabetes, for example, have an eight-year shorter life expectancy and a 150 percent higher risk of stroke. These widespread diseases are a plague to society and also a mega-market for Novo Nordisk.

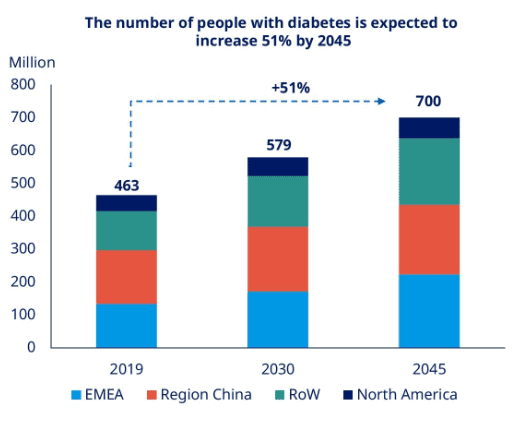

The fact that diabetes-related revenues will continue to rise can be seen from several developments. For example, the total number of people suffering from diabetes 2 has been growing for decades, with no signs of this trend abating. Most people with diabetes 2 now live in Asia, particularly in India and China, with a rapidly growing middle and upper class. Besides, the number of young people with diabetes-2 is increasing, which also indicates a continuing dynamic in growth.

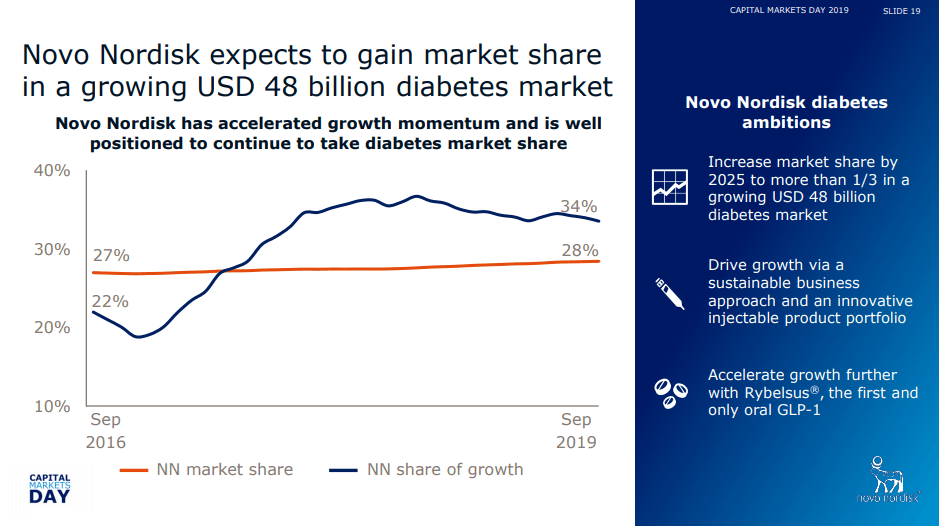

Novo Nordisk expects the number of patients to be treated to increase by 4 percent annually over the next five years. However, management not only expects the market to grow but also expects to increase its own market share from the current 28 percent to 33 percent over the next five years. Novo Nordisk intends to achieve this with new and innovative therapy forms such as orally ingestible preparations for controlling insulin release.

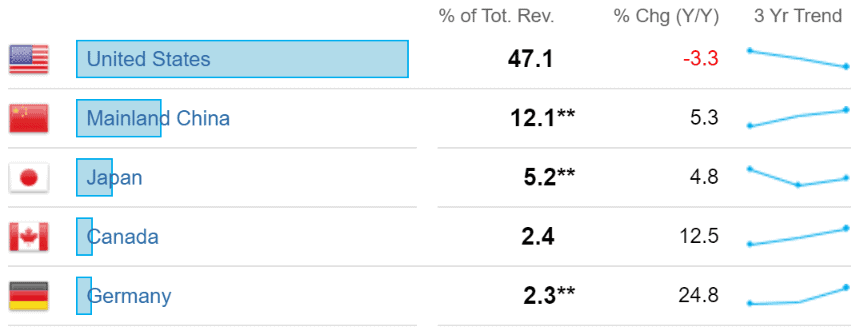

The opportunities are primarily in the markets outside North America, where Novo Nordisk already generates more than half of its revenues. In particular, the regions of Japan and Korea (5 percent of revenues) and especially China (11 percent of revenues) with their rapidly growing middle class offer high growth opportunities.

However, it is a misconception that an increasing number of diabetes 2 cases will inevitably lead to rising profits at Novo Nordisk because Novo Nordisk’s business model does have its weak points. For example, in the most important market, the U.S., the company has to negotiate the prices of its drugs with so-called pharmacy benefit managers such as CVS Health, which leads to intense competition and price pressure from its biggest competitors Sanofi and Eli Lilly.

That Novo Nordisk is vulnerable here is shown by 2016, when the stock price plummeted by almost 40 percent due to strong price pressure. Closely related to the competition is pressure to innovate, caused in particular by expiring patents. In the long term, however, Novo Nordisk has coped well with these challenges. All in all, the company’s experience and strong market positions mean that it is ideally placed to continue benefiting from the adverse side effects of global growth in prosperity in the future.

Novo Nordisk accelerates its growth

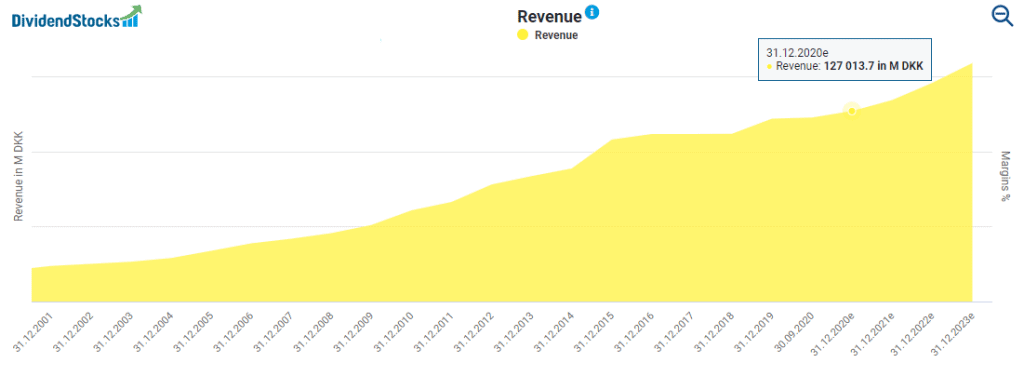

Looking at the period from 2016 to 2018, one can see that not even market leadership in a growth market guarantees increasing revenues. During that time, Novo Nordisk’s revenue stagnated at DKK 111 billion, mainly due to price pressure in the US. It was only last year that growth picked up again and, according to forecasts, will gain momentum in the coming years. In 2023, revenues are even expected to reach DKK 159 billion.

Recently, not even the Coronavirus pandemic harmed the momentum, further underlining Novo Nordisk’s defensive business model. In fact, revenue increased by 6 percent in the first three quarters. The fact that advanced GLP-1 products posted strong growth of 29 percent and expanded market shares of 3 percent highlights the Danish company’s ability to innovate. Management also raised its guidance for the current full year and now expects revenues and profit growth of 5 to 8 percent.

How profitable is Novo Nordisk?

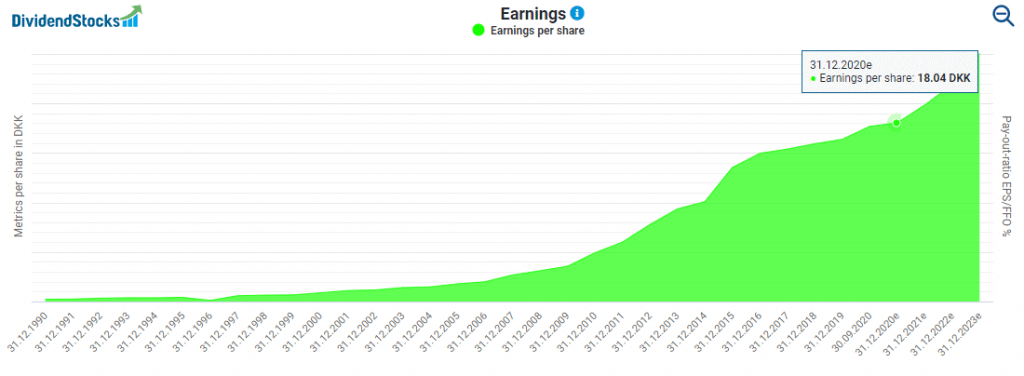

Novo Nordisk is scoring with rising profits. For example, earnings per share are expected to rise from DKK 16.38 in 2019 to DKK 18.04 in 2020. The forecasts also project profit growth in the coming years. By 2023, earnings per share are expected to rise to DKK 25, which corresponds to a growth of almost 40 percent relative to the current level.

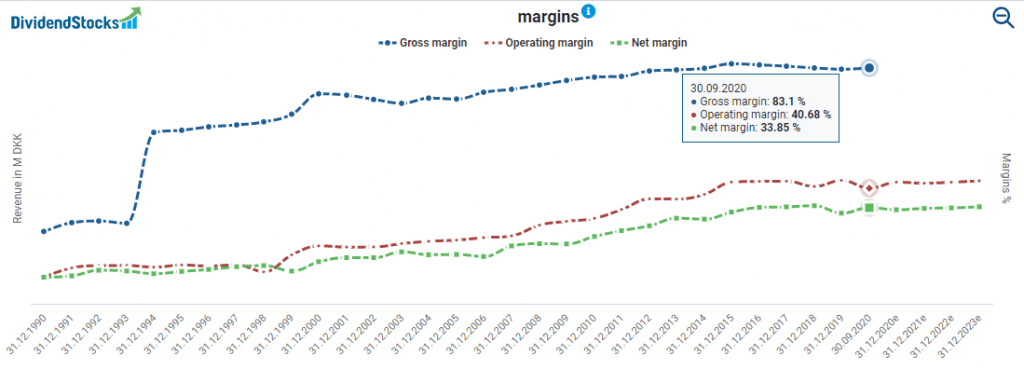

Over the last 15 years, Novo Nordisk has also increased margins. In particular, net margin and operating margin have shown strong growth. Since 2014, however, margins have remained slightly volatile at a high level. Novo Nordisk is an excellent example to show that a company’s margins cannot rise forever. Thus, future earnings growth depends primarily on rising revenues.

How safe is the Novo Nordisk dividend?

Novo Nordisk has increased its dividend by an average of 12 percent within the last five years. Dividend payments are made semi-annually in March and August and amounted to DKK 5.35 and DKK 3.25 in 2020. At the current share price of DKK 426.2, this corresponds to a dividend yield of 2.02 percent, which matches the long-term average over the last ten years.

Analysts expect Novo Nordisk to pay a dividend of DKK 9.63 per share to shareholders next year, which would represent an increase of almost 12 percent. That is a lot but management has enough leeway for such an increase. In 2020, the payout ratio was only 54 percent of free cash flow and 50 percent of profit. Thanks to the reasonable payout ratio with reliably rising revenues and profits, even a higher payout seems safe to me.

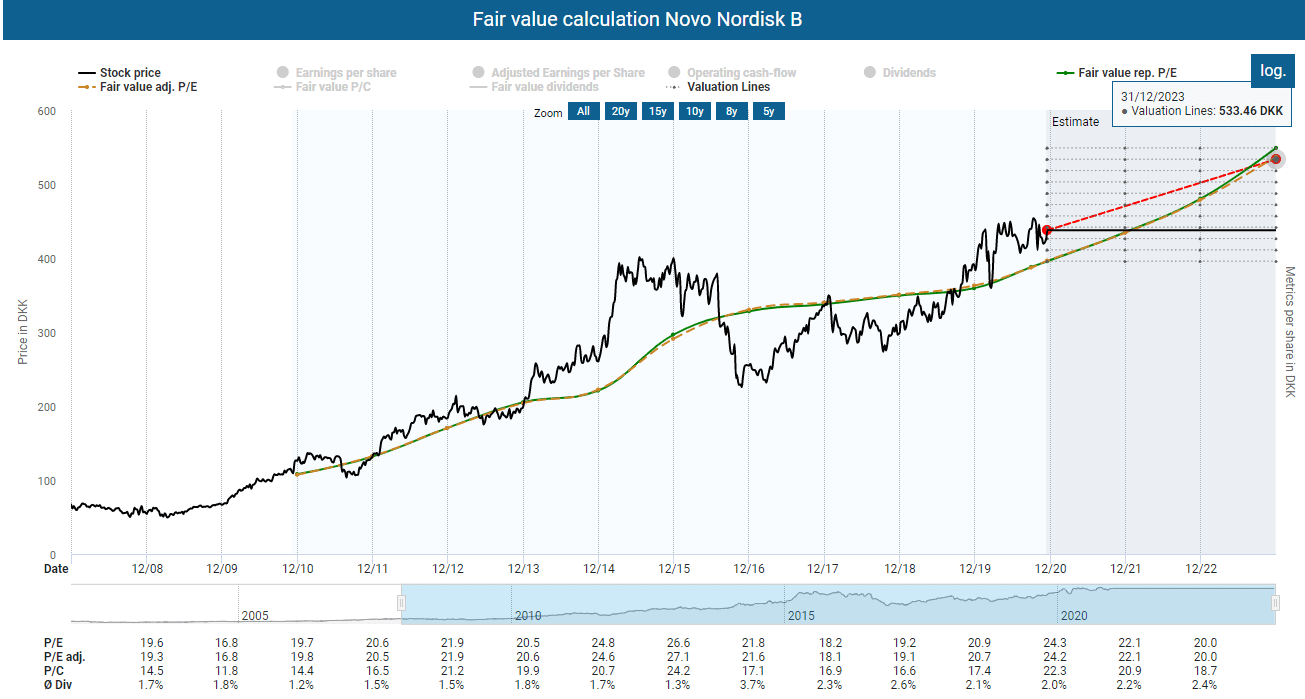

Is the Novo Nordisk stock fairly valued?

Since 2019, the stock price has also risen in the wake of resurgent growth, which has caused Novo Nordisk´s stock to now appear overvalued. Multiples such as an adjusted P/E ratio of over 20 and a P/C ratio, together with the only “average” dividend yield, indicate a high stock price. Furthermore, the rapid rise of the stock price in 2014 and the subsequent slump in 2016 nicely shows how sensitive the stock price reacts to negative news when the stock is clearly overvalued.

The market has already priced in part of the expected earnings and revenue growth. However, there is still room for growth. If we look at the fair values for 2023, there is a potential upside of 26 percent based on the expected adjusted earnings, which corresponds to an annual yield of just under 8 percent, including dividends.

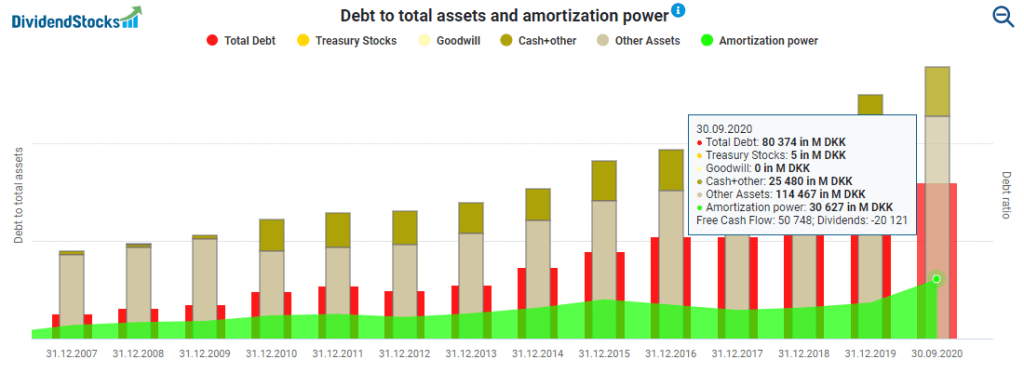

Part of the reason for the increased stock price of Novo Nordisk is likely its solid balance sheet. Although the debt ratio of over 57 percent sounds not that impressive, the debt of DKK 80 billion (including all liabilities) is pretty nicely offset by an annual amortization power of DKK 30 billion. Additionally, Novo Nordisk has a cash pile of over DKK 25.4 billion, equivalent to over EUR 3.3 billion. Enough for one or two acquisitions and enough to address the debt pile in a reasonable manner.

Conclusion: The Novo Nordisk stock still has room for further growth

There have been more favorable times in recent years to add Novo Nordisk stocks to your portfolio or to increase your position. Although rising profits also support the recent price increases, they have somewhat outpaced the stock’s valuation. However, if the momentum of earnings growth continues or even accelerates, the stock should reach its fair value in a few years, and the price will continue to rise as a result. Whether you will get another opportunity for a more favorable entry until then is difficult to assess. From my point of view, shareholders with a long-term investment horizon still have the opportunity to add Novo Nordisk stocks to their portfolio at a very reasonable price, which is why increased my position in Novo Nordisk in November.

hi mate, thanks for this nice article. May I have a question please – where did you find these information about debt of 80 BN DKK? I mean, I am looking at data from 2019, total liabilities were 68 BN DKK and pure debt is tiny portion of it. Checked in some other sources, they have almost no debt at all? Ca 10 BN USD in total liabilities, but this is not debt, not all of it. Not quite sure where this info comes from in your article . Also – do they fill in SEC 10-k filing? This is Danish company traded in NYSE, so not sure (tried to find it in EDGAR site but can’t find it)

Hi Hess, many thanks for coming by.

The 80bn DKK is the current status of total liabilities. The graphs I am using are based on FactSet Research System data.

You can also find the 80bn DKK in the balance sheet for the third quarter…

https://www.novonordisk.com/investors/financial-results.html –> 3Q —> financial workbook —> sheet “BS Q3”

I hope this helps!

All the best

ok, thanks a lot. So this is not debt sensu stricto, but rather all obligations, Most of them, more than 50 % of these liabilities are “provisions”, which, as per their finacials, are actually “Provisions for sales rebates” in the US (reduces gross sales to net sales). I am not fully familiar with IFRS standard, but this is regular business liability, not any interest bearing debt. Next biggest portion of these liabilities are “other laibilities” – dont have much time to analyze their annual statement now, need to read more in some free time, but this doesnt look like debt either, more like employee provisions etc. Other liabilities are trade payables, tax paybles, etc. Their debt is way lower. Borrowings, which seems to be the only interest bearing debt is only ca 4 BN DKK< which is ca 600 MM USD only. Which is super low. In any case – thanks for your input, much appreciated.

“So this is not debt sensu stricto, but rather all obligations”

Correct. The “total debt” number includes all liabilities/obligations.

Your comment brings definitely more light on the matter and supports the thesis that Novo Nordisk stands on extremely stable ground financially. Many thanks for that!

The “total debt” number includes all liabilities/obligations. – ehm, no, that is not quite correct. I do not want to split hairs, but in financial accounting debt does NOT equal all liabilities. Yes, liabilities bind the business in a certain way, but they should not be presented as debt (not all of them). Only interest bearing liabilities (borrowings, loans etc) are “debt” per se and such debt is used in calcualtions for long term debt to capitalization etc. Anything else on liabilities side are just obligations as in every business – trade payables are not “debt” in financial accounting, it is just some amount billed to a company by its suppliers. It may be confusing, I know, but there is pretty clear difference here. Not trying to be smart, sorry (some time ago I have also used to think all liabilities were debt, but that is not correct)

To say it other way – all liabilities include total debt. But total debt does NOT equal all liabilities. Sorry, maybe I was not clear 🙂 Cheers!

You are totally right here and that was the reason why I used “”. I referred to the graph/picture in the article which used the term “Total Debt”.

From an accounting point of view, it is more accurate to refer to total liabilities (which is also how it is reported in the financial reports). Thank you for taking the time! I will be more careful with these terms in the future 🙂

You are doing great job and sorry for tryign to be smart here. I knew Novo Nordisk, but never treated them as a potential buy (dont know why to be honest). To me they are expensive now, but I have added it to my watchlist (must also analyze Danish dividend taxation, in my country this is complex issue, each country dividend has different rules for internal taxation). Thanks again for this nice article!