When the New York Times published a major headline about the Wirecard scandal, even the last investor understood that something historic had happened. Wirecard, the company that first acted as a tiny house bank for operators of porn and gambling sites and then rose to become Germany’s flagship tech company, failed to prove on-balance sheet cash holdings of nearly €2 billion. The accounting scandal said a lot about how people and investors deal with fraud and fraud allegations. It is interesting to see how quickly the lines between the culprit and victim camps can change.

There are many good reasons to mentally engage your enemy. The first one is that fraud or fraud-like acts can have damaging consequences for one’s wealth. Secondly, I am definitely not arrogant enough to assume I am immune to fraud. So it is better to approach this enemy and know its mannerisms.

But it is less about fear and more about understanding. Knowing how fraud works and what methods fraudsters use is thus a first way to protection. In a guest article for the TEV Blog, a fraud analyst chose the following introduction that fits excellently:

In Japanese basketball, you learn first defense, the rest comes of its own. The reason is easy: this way you learn to become being more creative in offense, too. … Defense is more important than offense: it’s easier to lose something than to win something. The same occurs in investment. Therefore, we talk about tricks how you can get defrauded.

In this article, I would like to address the Wirecard accounting scandal. It is also about fraud, about victims and culprits but from another angle and from my perspective.

If you want to learn more about fraud and fraudster’s techniques, I highly recommend the short article here on the TEV Blog on the five main techniques that are mainly used to commit fraud.

The advantage of being biased when writing about an accounting scandal

To play with open cards from the beginning: I also held some shares and documented the reasons for my purchase on SeekingAlpha. To sum it up, it was a bet:

Wirecard also fulfills enough conditions to put such accusations on fertile ground: rapid growth, a complicated network of subsidiaries with a complicated business model. With such a combination, even small inconsistencies in the balance sheet can have an severe impact on the stock market. So that’s the bet and the risky part every investor needs to know. A bet on the fact that in the end there were some mistakes that do not affect the fundamental position of the company.

It was a bet that I lost. That’s the way it is.

That makes me an interesting person for this article. I am biased because I have put my capital into the investment and I lost most of it. Conversely, I am not upset about it. I recognized the possible fraud as possible fraud and bet against the fraud scenario.

The fact of being affected by the scandal is, in this case, more of a benefit than a disadvantage because it shows two things.

First, I was mentally prepared for the worst-case scenario. If you know you might get busted, you’ll feel less bad when it happens. You save your face, so to speak. Second: In the end, it always comes down to one’s own risk management. Those who manage their exposure to risk are not less likely to fall victim to fraud, but they can limit the possible damage to their total wealth.

No accounting scandal without Captain Hindsight pointing out the obvious

The day the bomb exploded, and Wirecard admitted that some cash might be missing, the Internet was full of people and commentators who had known from the beginning that Wirecard would go down. It was an ugly mixture of gloating and bragging that rolled down my news feed.

Of course, one could say that whoever did not buy the stock based on the reports and accusations published in the “Financial Times“ was right.

But in the end, and as I said before, these people just have won a bet. Congrats on that! But as a funny side note: these Captain Hindisghts didn’t even make a profit with their “we knew it before” attitude.

So the first thing is that it’s always easy to understand such scandals and frauds in retrospect. Yet, the period just before the meltdown is the most interesting, because, after the fraud, the victims cannot undo the damaging event. And at that time it was not necessarily so obvious, as the following considerations show.

The fifth street-situation

Before the meltdown, the Wirecard camps were heavily divided.

We can think of the situation as a poker game where all but one card (“the river” or “fifth street”) is exposed. Similar to the poker players who don’t know the last uncovered card, no private investor had a unique opportunity to obtain more information than other investors.

So before we all saw clear, the individual facts about the possible scandal contradicted each other, like the many possibilities of what the last card in our poker game could be. There were lobbyists for Wirecard and audited annual reports. These have created trust among investors and shareholders. On the other side, we had the Financial Times, short-sellers, and all their arguments.

At this time, it was impossible for the average investor to filter out the truth from all the unfiltered information.

If you want to sum things up, you could say that every potential investor had to ask the same thing: “Are the accounts correctly audited, or is the ‘Financial Times’ right?”. Is the fifth street card a good card or a bad card?

So the facts in their contradictory existence were clear. And what did the market say? Despite persistent rumors of accounting fraud, the market capitalization was still almost €10 billion in May. Not bad for a company whose worthlessness was obvious.

From a May 2020 perspective, the stock was massively undervalued if the allegations were false and massively overvalued if they turned out to be true. It was only a question of how investors took advantage of this situation. To be clear, it was never a question of proper due diligence but one of each investor’s willingness to take the risk of betting on the wrong scenario.

Taking a voluntary risk is not a bad thing and has nothing to do with greed

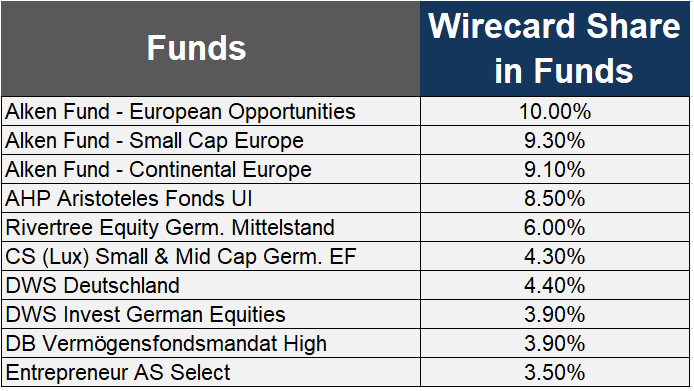

Some media or commentators said that many investors were far too greedy and closed their eyes to the risks and accusations against Wirecard. Indeed, individual funds such as DWS and Alken held many Wirecard shares at the end of May 2020. In some cases, Wirecard accounted for 10 percent of these funds:

One fund manager who held many Wirecard shares in May 2020 was Nicolas Walewski, the founder of Alken Asset Management. He graduated from the famous Paris Ecole Polytechnique.

Tim Albrecht, who manages funds at DWS (an asset manager belonging to Deutsche Bank), also held on to Wirecard stock the entire time before the meltdown. Both managers have an excellent track record. And both were terribly off track with their Wirecard investments.

But were these managers and all the others too greedy? Well, that thinking is a little too short, though. We don’t know that these investors invested out of greed. Investors such as Nicolas Walewski or Tim Albrecht were possibly aware of the risk because the problems and allegations were public all the time (see above).

The problem probably lay more in the weighing up of opportunities and risks. But this does not necessarily have anything to do with greed.

An accounting scandal that is based on naivety

More critical than greed might have been the following aspect: Naivety. Of course, you can criticize that too. But the accusation then goes in a completely different direction. No one would have chosen certain harm out of greed. The decisive factor was always the hope that things would turn out well in the end.

I’ll show you what I mean in the following points.

We play the investing game because we assume that everyone plays by the rules

Investment takes place in a space defined by rules. We have a system of order that only works as long as everyone sticks to it. Mutual trust and a straightforward arrangement of cause and effect only prevail as long as the order is maintained.

Think back to the poker game. In such a game, each player usually assumes that both the dealer and the other players are not cheating. On this basis, each player decides how much to invest, i.e., whether to raise or leave the game.

Back then, Wirecard was already confronted with first suspicions and allegations. A spectator from outside (the honorable Financial Times, and some short-sellers papers before that) shouted into the crowd several times that the dealer was not playing fair. There were indications and reasonable arguments that led to individual players leaving the game (the Wirecard share price had already collapsed by 50 percent).

The players who remained at the table continued to have confidence that the dealer dealt the cards fairly. It’s naive, but it has nothing to do with greed.

Greed is by its very nature to want to achieve a specific goal at the price of morality. In the case of Wirecard, many investors continued to play because they trusted that in the end, everyone would play by the rules or that there would only be minor violations. In retro perspective, it was naive in any case, but not necessarily greedy.

It is okay to be naive as long as we recognize the naivety and its possible consequences

Naivety is not a bad thing in itself. It is just the absence of experience. If I have had no previous experience with fraud and therefore have faith that the people around me play by the rules, I am either lucky or have a healthy knowledge of human nature. Both would be good things.

There is no reason to walk around suspiciously, suspecting the worst intentions of every person we meet. Of course, that’s no reason to leave the front door open while you’re at work either. But that is the crucial point. I can assume that no one would clean my apartment while I am out of the house. And yet, I can lock the door to be on the safe side if I’m wrong.

One is about how I see the world (naivety), the other is about hedging if I’m wrong (locking the door). Risk management is the key. I try to protect myself against the risks that arise if I should be wrong with my assumptions (the unexpected).

So it’s about the risks that I don’t know and therefore don’t expect. I think this approach makes more sense than looking only at the risks that I know and that are already within the realm of the expected. The latter is a rather sad case of unrecognized naivety as those who think they are protected against all risks have not yet experienced the unexpected.

Those who know the risk of their naivety and protect themselves against the risk of being wrong, end up driving safer than those who believe they have armed themselves against all possible dangers.

The fine line between the culprit and the victim camps

There is a simple principle in criminal law. We must protect from fraud precisely those who are particularly vulnerable because of their lack of insight or naivety.

But we often see the opposite. You may have heard things like: “Why does the old lady have to be on this dark street with so much cash?”. These are typical social reflexes that can be found repeatedly in dealing with criminal law.

The intention is to make the victims complicit in the crimes they have suffered, which is a gross error of judgment. Such sayings ultimately indicate that we can no longer expect our teammates to play by the rules. When we have reached such a state in the stock markets, you should sell all your stocks because chaos will reign.

But if we want to live in a world where everyone plays by the rules, then we must also assume that everyone plays by the rules. If every player assumes that the other player is lying, no one will play honestly. Hence, a certain amount of naivety is necessary to keep the system alive.

That said, we shouldn’t move this fine line between the culprit (the rule-breaker) and the victim (the one who trusts the players to follow the rules) thoughtlessly. Holding the victim of fraud responsible for the fraud because of his or her naivety is, therefore, methodologically the completely wrong approach.

Additional considerations in dealing with an accounting scandal

In addition, there are other considerations in dealing with an accounting scandal, especially when looking at the typical patterns in how the public reacts to them.

It is easy to raise the suspicion of fraud, but it is more difficult to prove it

It is quite common, that the public starts to throw accusations in every direction. We see the same patterns of thinking and concluding: something bad has happened. The people or institutions that are supposed to prevent such things did not prevent it. Therefore, either they must be idiots or they are in conspiracy with the culprits.

In the Wirecard accounting scandal, the public quickly accused the German financial regulator BaFin or the auditing firm Ernst & Young of gross negligence. The situation was further complicated by the fact that some BaFin employees had themselves traded shares in Wirecard.

But does that prove anything other than a breach of professional duty? This does not automatically mean that BaFin was grossly negligent in failing to prevent the scandal. Just a reminder: gross negligence means causing damage, although the occurrence of the damage was or would have been recognizable to the culprit. Just keep in mind that the failure of individual parts of a system or their involvement in a conspiratorial fraud makes the system a victim, not a culprit.

Furthermore, there are judgments in several cases in which investors have sued Ernst & Young. All claims have been rejected. Why? The claimants have not been able to sufficiently prove that the auditors at Ernst & Young made false statements intentionally.

So just because the Financial Times has already done extensive research and published indications of balance sheet fraud does not necessarily mean that BaFin or Ernst & Young have been asleep the whole time. As a legal professional, I can tell you that it is easy to raise the suspicion of fraud, but it is more difficult to prove it.

Of course, the Wirecard scandal was really stunning. It has such accompanying anecdotes that it is tempting to see larger forces and powers at work. And yet, we have to admit that it is still possible that the players involved in such a scandal have all fallen for their own naivety.

Confusing the principle with the exception

If people call for consequences too quickly, they may destroy a well-functioning system. Because one thing is sure: an accounting scandal is an exceptional event. The outcry, outrage, and ripples that follow these events alone show how rare they are.

That implies that in most cases, the control and security mechanisms are effective. So we should not confuse the exception to a principle with the principle.

Confusing both could have negative consequences. A higher level of control could make it more difficult for smaller companies or fast-growing enterprises to concentrate on their operational business. There must be a balance between supervision and excessive bureaucracy.

Conclusion

In the end, we see at Wirecard’s accounting scandal what we have already seen before (Enron, etc.). Nobody is safe from fraud. Investors also can’t rely 100 percent on referees and watchdogs. I don’t mean that in a blaming way. In case of doubt, auditors or the authorities can always be fooled with fake documents, etc.

While we can analyze which control mechanisms have failed and then take targeted action, we have to accept that this wouldn’t give us any guarantee.

In the end, proper risk management is crucial to survive such scandals and frauds without taking too much damage. The good thing is that investors can control their risk management. So while they are free to believe that a particular stock is the best stock in the world (naivety), they should still spread their capital across several horses.

And for one or the other, it may certainly also be relieving to know that naivety is not necessarily a bad trait. I am naive sometimes. That’s not bad, but ignoring one’s naivety definitely is.

Danke für den guten Beitrag, ich persönlich habe auch Geld bei Wirecard verloren und bin gespannt wie es weitergeht.

Vielen Dank, Thomas! Das bin ich auch. Es haben sich leider viele Investoren böse verbrannt. Hoffentlich war das Risiko bei allen breit genug gestreut.