Welcome to a new report of my Dividend Diary on the TEV Blog. Here, I report the development of a cash flow-oriented investment approach that focuses on generating a passive income through dividends. Against this background, the goal is not to outperform the market but to put food on the table through a regular income via dividends.

With the Dividend Diary, I document how a cash-flow investment approach can be part of well-balanced wealth management. To keep things simple, I have built three pillars:

- Active income.

- Passive income.

- Conversion.

Dividends fall into the last two categories. They are passive because they provide a cash flow without me having to go to work. Additionally, they are an essential pillar for the conversion since they can be reinvested to generate even more income in the future. That is the Theory. Now let’s get down to practice.

My monthly dividend income in November:

This month, my cash-flow approach generated the following income through dividends:

- AT&T (26.25 EUR)

- General Mills (20.53 EUR)

- Campbell Soup (12.99 EUR)

- CVS Health (5.75 EUR)

- Bristol-Myers Squibb (17.78 EUR)

- Apple (7.87 EUR)

- General Dynamics (6.09 EUR)

- AbbVie (21.86 EUR)

- Kinder Morgan (11.70 EUR)

- Omega Healthcare (9.53 EUR)

- Procter & Gamble (12.37 EUR)

- Realty Income (3.22 EUR)

- Amundi MSCI E.M. ETF (127.20 EUR).

The total income through dividends in November (after taxes) was: EUR 283.17/appr. 320 USD

Dividend income report check

I cannot complain about November 2021. Dividend income was more than 70 percent above November 2020. In addition, the dividend income for the full year 2021 will likely be more than €1000 above the income from 2020 so chances are also good that I will see a 60 percent growth in passive cash flow on a year-over-year basis. I can therefore already say that I am satisfied with the otherwise not so great pandemic year 2021.

Stocks I sold in November

I sold all of my 11 Anheuser-Busch-InBev shares this month.

Once again, I was on the sell-side and liquidated my entire holding in mid-November. Together with Imperial Brands, it was my smallest position in the portfolio, and I didn’t see any point in holding the stock any longer. After the various dividend cuts, the stock hardly contributed to my cash flow, and the share price also performed rather badly. The poor performance was due to the high debts and the Corona crisis, which caused beer consumption to plummet worldwide.

However, I am still not entirely out of the company, as tobacco giant Altria currently also holds 10 percent of the company.

So with the sale, I was able to downsize my portfolio a bit in terms of the holding amount. As I was also more than 25 percent in the red, I wanted to fill my pot of losses a little so that I would have to pay less tax on other capital gains. Since the markets are already very high and in the event of a crash, the share will probably also go down, I used the current market phase to clean up my portfolio a little.

Stock purchases in November

In November, I bought more shares of great companies so that the dividends will continue to rise in the future. All purchases were expansions of existing holdings. So no new companies entered my portfolio.

- Emerging Markets ETF (20 shares)

- Pfizer (30 shares)

- Merck & Co. (15 shares)

- MSCI World Energy ETF (148 shares)

In the following, I will briefly explain why I bought these companies. Please do not expect a fundamental analysis. I will only mention some aspects per company that might be of interest to the readers. Maybe you will find inspiration for your investment. In case you disagree, feel free to write your opinion about my purchases in the comments.

Please keep in mind that this is only a non-representative sample of my overall asset management.

November was boring. A large part of the capital went into two of my ETFs. So I increased both my Emerging Market Holding and my shares in the World Energy ETF. The purchase of the Emerging Market ETF also directly contributed to the November dividends. The World Energy ETF will pay the dividend in December and contribute to making this year a strong cash flow year.

The last two investments were in the pharmaceutical sector. Here I bought 30 more shares of Pfizer. The timing was quite favorable from a financial point of view because shortly afterward, the new COVID-19 variant was discovered, which caused concern on all sides.

For Pfizer, however, it is becoming increasingly clear that the company, along with BioNTech and Moderna, will claim the most significant slice of the pie. It is the “winner takes it all” principle. Besides, Pfizer has licensed the rights to its COVID-19 drug, and we all know how lucrative and profitable licensing can be (#Qualcomm).

Pfizer is currently still relatively cheaply valued. The adjusted P/E ratio is only 14, and the dividend yield is around 3 percent.

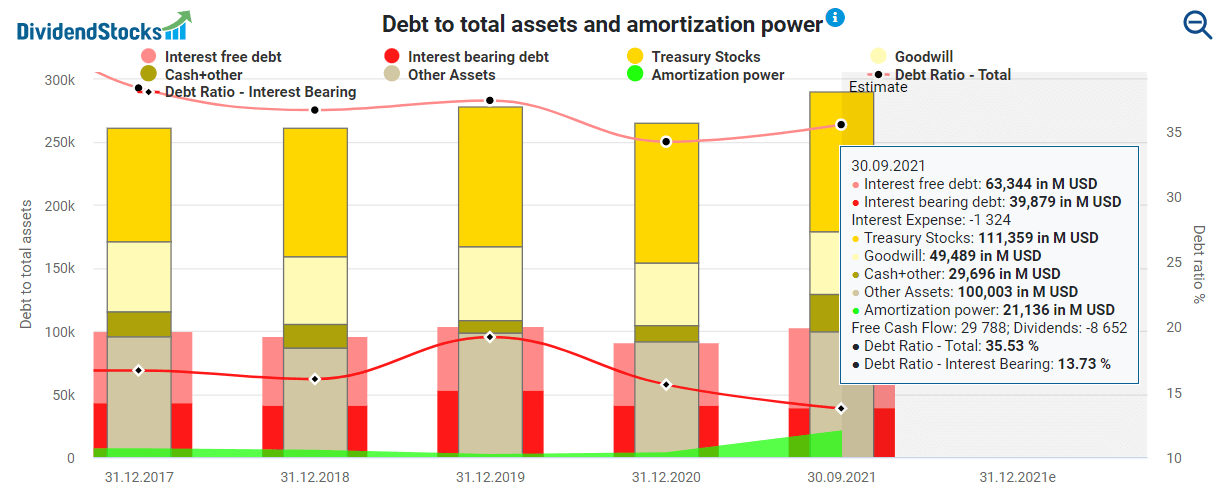

No matter how long Pfizer will continue to benefit from the COVID-19 deals, the cash will help fill the pipeline and reduce debt. For example, the debt ratio measured by interest-bearing debt has fallen to 13.7 percent from 19.22 percent in 2019. Sitting on top of the $30 billion cash is Pfizer. All liabilities combined amount to $63 billion. In this respect, Pfizer is in an enormously good position in business terms and based on its balance sheet.

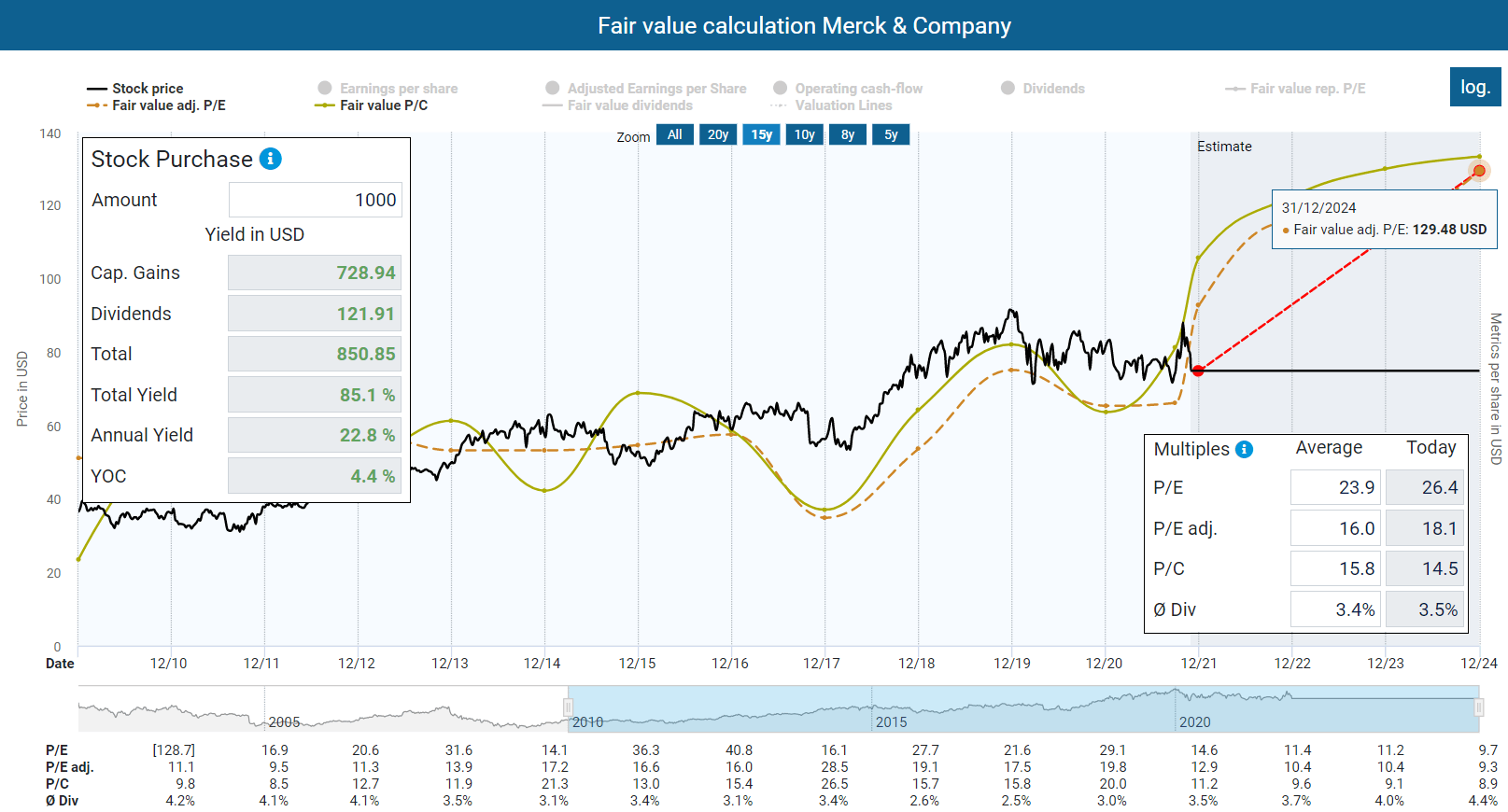

I also bought 15 more shares in Merck & Co. The decisive factor was the still existing undervaluation and the possibility that Merck could also develop drugs against COVID-19. Although this hope has been dashed somewhat, overall, the fundamental valuation is still excellent based on the expected profits in the next few years. I plan to buy more Merck.

Likewise, the company has increased the dividend by more than 6 percent which is slightly below the 5 year growth rate of 7.7 percent. I am nevertheless satisfied because this offsets recent inflation rates and the stock is doing what it is supposed to do: generating cash flow that can keep up with inflation.

Watchlist for December

There will be some additional share purchases next month. As you may know, I am relatively flexible when it comes to new investments. Either I buy new positions, or I increase my shares in existing investments.

The following companies are on my watchlist in particular:

- Microsoft (MSFT)

- Digital Turbine (APPS)

- BASF

- Johnson Outdoors (JOUT)

- Emerging Markets/Energy stocks

- Unilever (UL)

- General Mills (GIS)

If you look at my report from last month, you will likely see that none of the companies I bought were on my watchlist. Why is that? Is the watchlist nonsense, and in the end, I only do what I want anyway? Yeah, a little bit. I don’t have a fixed system for my stock purchases, and that’s one thing I have to consider changing.

However, I have an extensive overview of many companies that I look at from time to time. The watchlist contains primarily companies that I have examined particularly carefully, where substantial changes are imminent or companies that are in my focus for other reasons.

These companies are present to me in some form, which is why I put them on the list and perhaps monitor them a little more closely than other companies. But it often happens that I invest in different companies when it seems convenient at that moment.