Even a small pocket cannot prevent me from making more of it. Snowflakes of pennies can become an avalanche of monthly dividends. This is what wealth management means to me.

The way to get there is incredibly simple and only consists of adhering to the following mantra:

All I need to receive such an avalanche of wealth and fortune is (i) a lifestyle where I spend less than I earn, (ii) say more yes than no, and (iii) avoid the wrong kind of people.

These three things sound simple, and they are.

Boring but important: earnings must be higher than expenses 🫰

Expenses and income are a balance. Expenses are on one side of the scale, and the income is on the other. I can earn more or less and I can spend a lot or a little.

Spending less than I earn will result in a cash flow that opens up many opportunities. I can pay off debts and become debt-free. Furthermore, and this is the crucial point, I can invest.

Free cash can buy me shares of companies, and chances are good that I will profit from the success of the share’s underlying business.

Easy.

Saying more yes than no 👍

This second attribute is a little more subtle. Saying yes more than no does not refer to consumer spending.

Rather, it is about creating opportunities and being open to possibilities that could prove valuable in the long term. This approach, also known as serendipity, describes the phenomenon of making unexpectedly fortunate and beneficial discoveries through a positive and open attitude.

Serendipity and the concept of delayed gratification

Serendipity and the concept of delayed gratification are a perfect combination. While delayed gratification describes the ability to resist short-term temptations in favor of long-term goals, serendipity goes one step further.

Serendipity encourages us to actively seek out and say “yes” to situations that could bring us surprising and positive results in the future.

I live with an open mind and look for opportunities that move me forward. Not every path is crowned with success. But when in doubt, I try a path and see where it takes me. On the other hand, I am willing to cut back in some areas to not jeopardize my long-term goals or achieve them even faster.

I have a comfortable safety net

My existing stock portfolio and the ever-growing monthly dividend payments help me enormously. Together with my human capital, they form the pillars for a sound sleep.

But it gets even better.

Every month, I invest more capital in companies, thus increasing my future cash flow, which covers an ever-increasing share of my monthly costs.

I have now built up a comfortable safety net and it gets more comfortable each month.

In my situation, I can sometimes take a slightly greater risk if it also means I have greater profit potential. Of course, it remains important that I invest 95 percent of my assets in a diversified way and don’t put all my eggs in one basket.

Avoiding the wrong kind of people 🧟

Thirdly, it’s about avoiding the wrong kind of people. There’s a range of guys I’d rather not spend too much time with or introduce to my best friends from childhood.

Avoiding the doomer fraction

One species is the doomer.

The term “doomer” describes people who have an extremely pessimistic and negative view of the world. These people tend to constantly talk about disasters and failures, be it in relation to the economy, the environment or social life.

Such negative attitudes can be contagious and undermine one’s motivation and belief in one’s own abilities and possibilities.

Doomers spread an atmosphere of pessimism, either out of stupidity or a desire for recognition, which can severely affect their own attitude and productivity.

Constant negative comments and gloomy predictions can cause you to lose hope and give up faith in a better future.

Doomers tend to exaggerate problems and ignore solutions, which leads to them becoming passive and resigned. However, often, these people simply want to sell their own products and services.

Pessimistic attitudes will likely influence my decision-making, especially when taking risks or investing in new projects. Doomers can prevent you from seizing opportunities and hinder your progress. Doomers are constant nay-sayers and the exact opposite of those who want to use serendipity to their advantage.

Constant contact with negative people can be emotionally draining. Surrounding myself with positive and supportive people who encourage and inspire me rather than drag me down is important.

Avoiding idiots in general

Secondly, there is the idiot fractions.

People who behave irrationally or irresponsibly can significantly impair one’s own progress.

For me, “idiots” in this context are people who constantly make ill-considered or unwise decisions without considering the consequences.

Dealing with people who constantly make mistakes and cause problems can take time and energy. This time and energy could be better invested in productive activities that bring you closer to your goals.

Idiots can also damage your reputation, especially if you are associated with these people.

A bad reputation can negatively affect your professional and personal development.

Constantly dealing with unreasonable people can be stressful and frustrating. Focusing on rational and supportive people is important for creating a harmonious and productive environment.

“I’m at that stage in life where I stay out of discussions. Even if you say 1+1=5, you’re right – have fun.” – Keanu Reeves

Social media can be a big waste of time and create unnecessary stress. Therefore, I have minimized my use of social media.

Since I’ve been avoiding social media or severely limiting my use of it, I’ve noticed that I’m using my time and energy a little more wisely than before, without missing a single meaningful news item.

This does not come as a surprise, considering the bad impact of social media consumption.

Social media can easily lead to hours of scrolling through feeds without getting any real benefit. Each of those useless minutes makes me dumber and keeps me from relaxing or doing anything else useful.

It often encourages comparison with others (dazzlers, doomers, other idiots), leading to dissatisfaction and an unrealistic view of one’s life. You usually only see the positive sides of other people’s lives, which can affect your own self-esteem.

Furthermore, constant notifications and the need to stay up to date can significantly affect concentration and productivity.

Wealth management demands patience: every majestic tree once was a small seed 🌳

From the smallest seed, a tree can grow.

How?

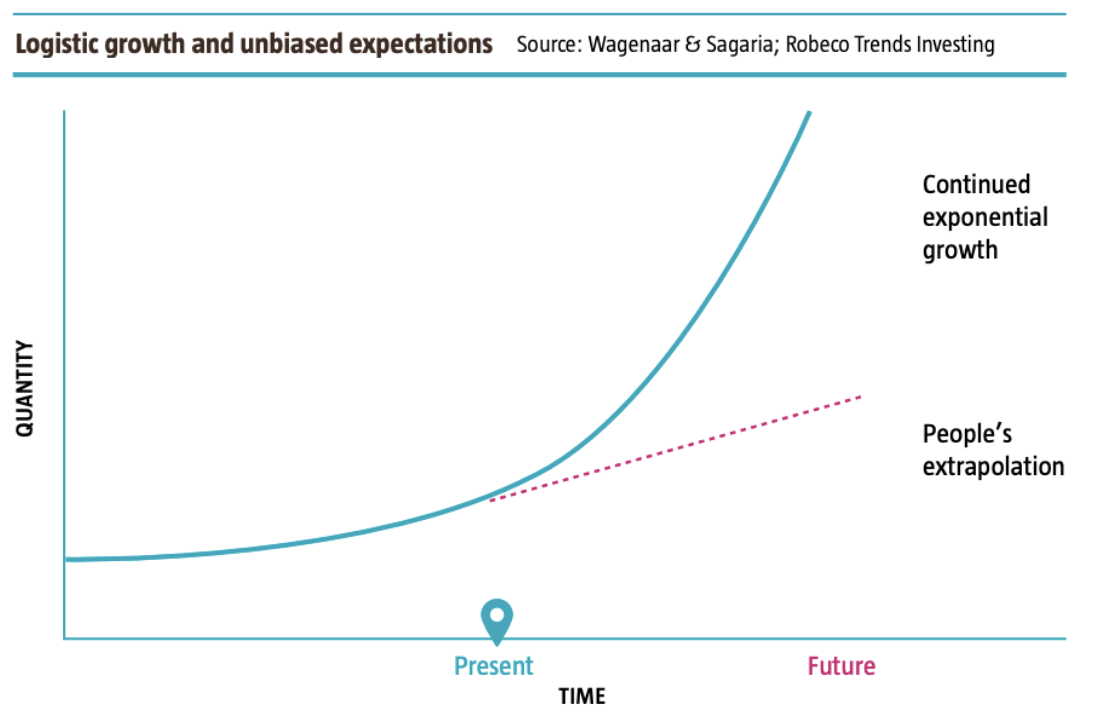

Compound interest and exponential growth are the magic words here. And the best thing is that I don’t need millions of dollars to start this flying wheel.

The human brain tends to misinterpret exponential growth. However, with exponential growth, even small investments can have a large impact over a long period.

The devine stock market is the bedrock of wealth management

For someone who ignores doomers and believes in the long-term success of capitalism and a liberal society, investing in stocks is almost inevitable.

Shares represent ownership in companies. In a capitalist society, companies are the driving force of economic growth and innovation. By investing in stocks, you participate directly in this growth and benefit from the companies’ profits.

Liberal societies promote free market economies. In these markets, companies can compete freely and realize their full potential. This leads to a more efficient use of resources and higher economic growth – both factors that increase the value of shares in the long term.

Shares offer the opportunity to participate in the creation of value in society. When companies are successful, they create new jobs, develop new products and services, and increase general prosperity. As a shareholder, you benefit directly from this value creation.

The basics aren’t hard at all. It is important to preserve existing assets, use them sparingly, and try to increase their value.

I am patient and enjoy my life. The opportunity always lies in the long term.

I laid my foundation in my mid-twenties 👶

I have been active on the stock market for so many years now that I can no longer recount the many ups and downs. The coronavirus crash dip in my multi-year performance is hardly noticeable, thanks to constant investment and good stock market performance.

And I’m still in the middle of the early game. Maybe I’ve already reached the middle game, but in any case, I still have decades ahead of me, and I can already say how important it is to invest early on.

If I had started earlier, it would have been even better 😞

So it is pretty obvious that managing wealth is not only about maintaining the status quo. Moreover, it contains an element around using conservative methods to make your money work for you.

And the sooner you start, the stronger the compound interest effect.

I would say that I was a bit lucky and started investing in my early twenties. But if I had started earlier, it would have been even better.

I only started with smaller investments of 200 EUR per month. Today, I receive multiples of this monthly amount as dividends from my companies. Over the years, the payouts will become even more extensive.

If you have more money to invest, that is great. If you have less, that’s not bad at all. You can use the savings plans of your broker to invest in the stock market every month.

How do I manage my assets? 📊

As far as my wealth management is concerned, I have built three pillars.

- Active income (which is often ignored by investors).

- Passive income.

- Conversion, i.e., letting active income work to receive passive income.

These pillars are, in turn, carried by a stable foundation that acts as the basis for my wealth management.

As I continuously learned and gained professional experience, my income increased gradually, allowing me to put even more money into the conversion cycle.

My stocks are my assets, which in turn is a big chunk of my wealth so I must refrain from doing anything stupid that could put it at risk. I therefore accept that there is neither the philosopher’s stone nor a fast way to get rich.

If someone tells me otherwise, I am extremely suspicious. On the free market, chances always (really always) correlate with risk. Otherwise, our system would not work. No one wants to give you a gift. Nothing is free, which is especially true when it comes to financial matters.

Good enough investing 😎

Releasing myself from the pressure of being the best brings deep contentment and insight into life. This philosophy also applies to investing.

The quest for the perfect investment: a frustrating endeavor

Investing can be overwhelming with its myriad strategies and analyses. Many private investors, driven by greed and the allure of quick wealth, often find themselves outperformed by the market. The belief in consistently beating the market is naive and leads to failure, as emotional decisions like panic selling and euphoric buying worsen performance.

Embracing “Good Enough Investing” as part of my wealth management

My “good enough investing” approach prioritizes simplicity and meeting personal goals over chasing maximum returns.

While I enjoy picking stocks, I acknowledge that ETFs might provide better results.

I aim to make more right choices than wrong and generate income through dividends.

My strategy is keyed by diversification, a long-term focus, and regular investments. Focusing on realistic goals reduces stress and enhances satisfaction.

Accepting “good enough” frees me from constant comparisons and unrealistic expectations, allowing for a relaxed investing experience.

The analysis of errors and undesirable developments

While I am quite happy with my “good enough investing” approach and my general wealth management journey, investing is still a journey riddled with mistakes, a truth often overshadowed by the allure of effortless gains.

I am not afraid to recognize and admit my past mistakes

Perfectionists might scoff, but true refinement comes from embracing and learning from our missteps. In the investment world, it’s easy to feel envious when everyone seems to win.

However, the real growth comes from acknowledging and correcting our errors, no matter how painful it may be.

Early on in my investment adventure, I fell prey to the siren song of high dividend yields. Companies like AT&T, with its enticing five percent return, seemed like a sure bet.

I simply neglected to consider the potential for future growth and the company’s overall health.

This short-sightedness proved costly, causing me to miss out on companies with sustainable growth potential like Microsoft. While Microsoft offered a lower initial yield, it provided substantial long-term benefits that I overlooked in my pursuit of immediate income.

Discounts are there for a reason

Another pitfall I encountered was an overemphasis on fundamental valuations.

My worst investments were often in companies that appeared cheap then, like AT&T, BASF, and Fresenius. Unfortunately, these companies failed to deliver on their promise. Conversely, while fundamentally also quite cheap, some of my best investments, like Apple and Facebook, performed significantly well.

This experience taught me a valuable lesson: while strong fundamentals are crucial, they must reflect a company’s ability to grow substantially, as was clearly the case with Apple and Logitech (at least, they had the potential), but not so much with AT&T and BASF.

“Bottom fishing” for the half-dead fishes

I also made the classic error of attempting to “bottom fish” – buying stocks at their absolute lows during market downturns. This strategy backfired.

Downturns can stretch on far longer than anticipated, and my attempts to “average down” by buying more shares at a lower price often just masked the underlying losses.

This experience shifted my focus to a long-term perspective, prioritizing the long-term health and growth potential of companies and their underlying businesses.

Don’t forget: only a Sith deals in absolutes

Today, I prioritize companies with sustainable business models and significant growth potential over those with simply high dividend yields. To put it short, I try to strike a balance between strong fundamentals and a company’s ability to grow.

Additionally, I’ve become more selective in my investments, avoiding unnecessary diversification in favor of a more focused portfolio.

Reflecting on and learning from my investment mistakes has been a cornerstone of my growth as an investor. While investing will always be a challenging and dynamic process, these lessons have empowered me to develop a more thoughtful and effective strategy.

Wealth management, to sum it up:

So basically, wealth management is all about these seven steps:

Understanding my assets and liabilities

First, I had to learn to understand my assets and liabilities. Initially, I didn’t have a clear overview, so I created a table to list everything. This included all my belongings and their values. At the same time, I broke down my liabilities, such as fixed expenses, subscriptions, and loans (e.g., to go to university) that I had to pay.

Realizing savings potential

It can be eye-opening to see how much savings potential is hidden in one’s household. While this was not a problem for me, I discovered that many people are paying high bank fees and high costs for electricity and gas.

Deleveraging

Being debt-free turned out to be excellent. I didn’t have to pay interest, and at the end of the month, I often had a small amount left over that I could invest. I always kept a positive cash flow and saved up an amount that provided sufficient liquidity for emergencies. Once I accumulated more money, I began diversifying my income sources.

Reconsidering my spending

I learned to wait and give myself time before buying expensive new items. The desire for new things was often just an initial impulse strongly influenced by my brain’s reward system. Waiting a week before making expensive purchases made me less dependent on my current mood.

I also informed myself about the product and what others said. The 30-day rule was particularly helpful to ensure I avoided unnecessary purchases. The rule ultimately says to wait 30 days until you purchase a specific volume.

Understanding my spending behavior and weak spots

It was crucial for me not to be dependent on my account balance.

I always wanted to know where I stood financially, where my weak spots were, the amount of my current income, and how much I had already spent that month.

Investing surplus money

I realized it was wise to invest surplus money in the stock market. By investing in dividend stocks, I built a passive income stream. I followed a cash flow-oriented approach, primarily investing in companies that paid dividends, but found that ETFs were the most effective investment form.

Generating additional income through dividends or side hustle

Building an additional income stream proved to be particularly important, acting like a lever. Whether through a part-time job or passive investments, having an extra income was great.

I loved your tip about looking for your savings potential and realizing it. My husband owns a company that is having some issues with handling money. I think it’d be beneficial for them to talk to a financial planner to get everything sorted out.

Thanks for your comment Eve! I am glad, you liked the article!