For whatever reason, some methods work in at least 90 out of 100 cases. But, they work not only in the vast majority of cases. Moreover, they feel effortless, almost like going with the flow, as if there is a golden success formula.

Then, on the other hand, everyone had already experienced approaches that were as difficult and annoying as having to swim upstream.

It almost seems as if success, both in the business world and in personal life, has a very specific aesthetic. And if there were a golden formula for success, it would most likely have very simple variables everyone can follow.

Just like small steps in dancing, they add up to something aesthetically complete.

Reduction is key

We all enjoy the clean lines and structures of a tidy room. The appearance and smell of nature without pollution is a dream.

The tidy room, the untouched nature … all these things are reduced to their cores.

Imagine a clean room furnished according to functionality, for example, for concentrated work in the office or coziness in the lounge. No clutter disturbs the function.

Nature without dirt and human waste provides relaxation and a quiet and peaceful place.

Reduction means removing substance from something and thus creating lightness. What is light is mobile and independent.

And as with a tidy room and nature, reduction is also aesthetic. In short, reduction is good at its core.

This idea of reduction is found not only in the physical world but also in other areas of life. In philosophy, reducing complex ideas to their fundamental principles can create clarity.

In our modern world, which is often characterized by abundance and sensory overload, reduction helps us focus on what is important and eliminate unnecessary baggage. It allows us to create an aesthetically pleasing and functional space in our homes, nature, or thoughts.

Successful strategies are often reduced in their complexity. They get by without a lot of frills. Without tricks and gimmicks.

Berkshire Hathaway’s webpage is an affront

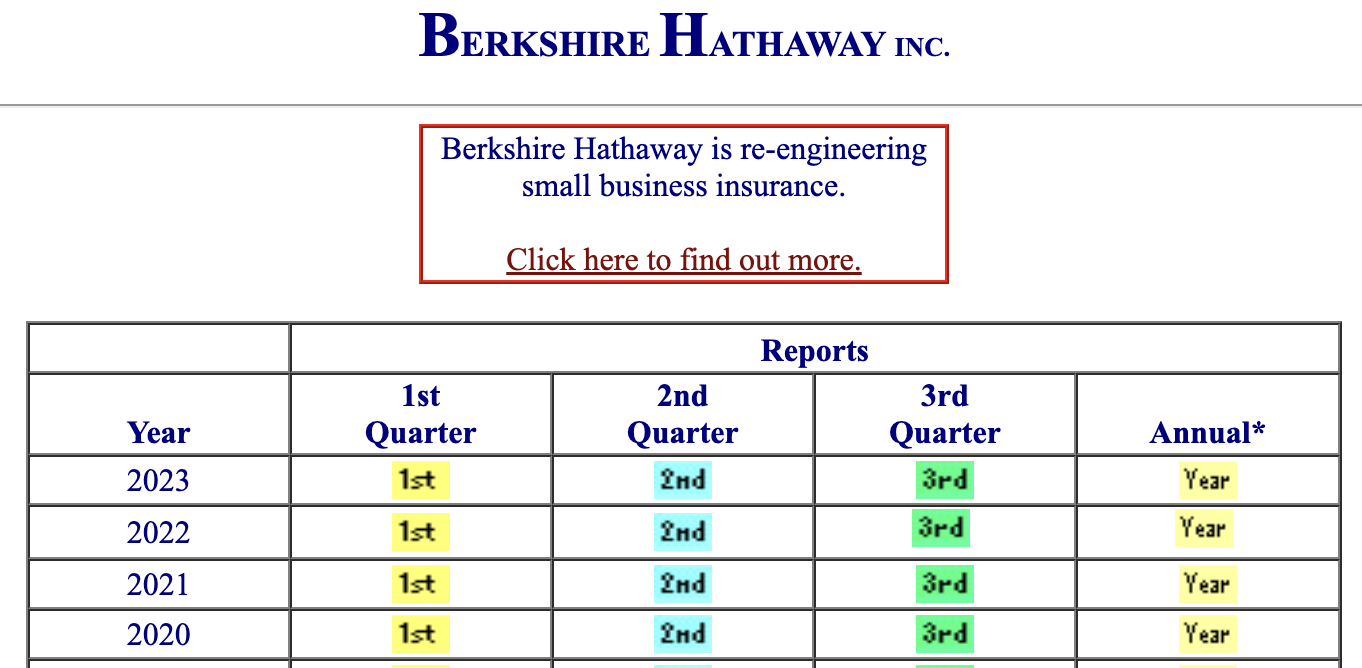

Take a look at the Berkshire Hathaway website, for example, and the simplicity with which it presents the individual quarterly reports.

The Berkshire Hathaway website is so reduced that it almost seems under-complex. At first glance, it resembles an affront to one’s viewing habits.

In short, the site feels like a museum. If I didn’t know who owned this site, I wouldn’t have guessed in three long winters that it was one of the most successful investment companies in history.

Despite its out-of-this-world appeal, it serves its purpose. The site is extremely functional. I can find what I’m looking for immediately. For example, I don’t have to click through menus to read the quarterly report for the second quarter of 1995. I only have to scroll twice, and I’m there.

Reduction is lindy

Reduction is also lindy.

The term “lindy” comes from the world of complexity theory and means that something that has already lasted a certain amount of time is likely to continue to exist – like the construction site right outside your bedroom window or on the highway you use to get to work every day.

Once established and stable, reduced elements endure. In nature, we can find many examples of reduction’s longevity and resilience.

An ecosystem that is balanced and reduced to its essential elements can often cope better with short-term disturbances. A forest landscape in its natural state can cope well with insect infestations or temporary weather extremes. But not so monocultures.

Another example of the long-lasting nature of reduction can be found in architecture. Historical buildings have often shown astonishing longevity in their aesthetics. Classic architectural elements are considered monumental testaments to ancient architecture and proof of the effectiveness of reduction in creating durable structures.

In technology, we also find numerous examples of the long-lasting nature of reduced systems. Simple, well-designed products and platforms like touchscreen smartphones often have a longer lifespan and greater adaptability to changing conditions than complex and cluttered alternatives.

Why I prefer reduction over disruption

With the start of the new millennium, Amazon has triggered a revolution in retail. The Seattle-based company has massively driven online retail forward, and the effects on traditional retailers were dramatic. Traditional retailers were forced to adapt to the changed market conditions, and those who failed to do so had to close their stores.

Amazon has also shaped other industry sectors, such as cloud computing, logistics, and entertainment, through its wide range and efficient services.

A company like Amazon is often described as a disruptor. Many start-up founders in the early 2000s also dreamed of finding an idea that would completely disrupt a market.

Amazon has disrupted numerous industries through innovative business models and technologies. But disruption was less the decisive criterion.

The real driving force behind Amazon’s success was not so much the disruption itself but rather a decisive element:

Reduction!

Jeff Bezos reduced, the disruption came on its own

Amazon could only become this force of nature because Jeff Bezos massively reduced complexity.

By automating, increasing efficiency, and providing a seamless user experience, Amazon has helped simplify processes and more effectively meet customer needs.

This has resulted in customers spending less time and effort shopping and enjoying greater choice and convenience. This has been completed by the “customer first” principle or, as the longer version goes, “thinking customer experience backward.”

In other words, reducing the right elements and structures automatically leads to a disruption of existing systems.

Thinking in first principles

Reducing complexity is an element that can be found in many successful companies or people.

We see it at Amazon and Berkshire Hathaway.

Another example is Tesla founder Elon Musk. You can think what you like about Elon Musk, but as an entrepreneur and visionary, he has been a pioneer in many ways.

He is known for his “first principles” approach. First-principles thinking is an approach to problem-solving based on the fundamental principle of breaking a problem down into its basic components to understand it from the ground up rather than relying on analogies or already established solutions.

The idea of reduction and the concept of first principles are effectively one and the same approach.

We can overcome existing assumptions and limitations by breaking a problem down to its most basic components. Instead of being guided by preconceptions or the status quo, reduction allows us to ask the question “Why?” and rethink from there.

Respecting the quadrants of knowledge

Officially, Berkshire Hathaway does not make any forecasts for the company’s financial performance in the future. This is unusual in the financial world, especially considering that with banks, brokers, and analysts, we also deal with a multi-billion dollar industry that looks at numbers and analysis.

Warren Buffett and his late partner Charlie Munger are and were known for avoiding short-term forecasts and speculation, focusing instead on the company’s long-term performance.

And what happened, happens, and will most likely continue to happen.

Despite the lack of official forecasts, many analysts and financial institutions publish their own forecasts for Berkshire Hathaway. These forecasts are based on various factors, such as analyzing the company’s past performance, current economic conditions, and the outlook for the industries in which Berkshire Hathaway’s portfolio companies operate.

Educated guesses behind walls of disclaimers and liability limitations

Just think about it…

While those with the best overview do not dare to make forecasts, every third analyst considers himself/herself enlightened enough to publish forecasts on operating performance.

Of course, such analysts are paid to make supposedly educated guesses, which they hide behind thick disclaimers and disclaimers of liability.

However, anyone who hides a statement behind a disclaimer would not bet all the money they have saved and their grandmother’s pension on this statement. The value of such statements is therefore often low and investors should therefore keep analyses and purchase recommendations out of their investment decisions as far as possible (keyword reduction).

Skin in the game

The difference between Warren Buffett, Charlie Munger and Wall Street analysts is that the latter group has no skin in the game.

Most of Warren Buffett and Charlie Munger’s wealth is in Berkshire Hathaway, which means that they feel the consequences of their decisions firsthand.

It simply makes no economic sense for them to lure investors into their shares with flowery promises in the short term and ruin their reputation as serious businessmen and partners to their shareholders.

Analysts can say what they like without taking responsibility for their statements. They are not the investors’ partners but employees of their agencies or banks.

This symptom of the very common principal-agent disease is a big problem for inexperienced investors, as they have a lot at stake with their private assets.

Quadrants of knowledge

Managers like Charlie Munger or Warren Buffett know that they are in the dangerous world of the third and fourth quadrants of knowledge when it comes to forecasts.

| 1. Known-knowns | 2. Known-unknowns |

| Things we are aware of and understand | Things we are aware of but don’t understand |

| 3. Unknown-knowns | 4. Unknown-unknowns |

| Things we understand but are not aware of | Things we are neither aware of nor understand |

In the first quadrant, for example, forecasts are pretty reliable. When a child is born, we can confidently say that it will probably never reach a height of more than 2.20 meters. In a desert, we can confidently say there will be no underwater world to marvel at for the next 5 to 10 years.

However, things we do not understand or are not aware of are subject to a high degree of uncertainty. Politicians or managers should not make predictions about when a virus will be defeated.

Similarly, we should not make overly bold predictions about a company’s operating performance when we are unaware that the company is embroiled in an accounting scandal.

So as soon as we go beyond the first quadrant and enter the realm of the other quadrants, forecasts or predictions are more complex.

Better to convince in the long term than make short-term flowery promises – how Allianz disappointed me

Making consistently correct statements and predictions in quadrants two to four is almost impossible.

That’s why I find it somewhat dubious when companies like Allianz 2021 dazzle investors by promising to increase the dividend by at least xy percent over the next five years.

Of course, this is not a promise to which I, as a shareholder, am entitled.

The caveat in the form of a disclaimer follows the promise on its heels.

So far, Allianz has kept its word and significantly increased its dividends every year, and as a shareholder, I am naturally pleased about this.

But that means nothing for the future. There is no certainty that the dividend will rise by the five percent mentioned yearly – regardless of the announcement, and Allianz knows that.

I would have preferred it if Allianz had never published this letter. In the end, it shows that, when in doubt and without any necessity, management would rather break a forecast than ensure a clean track record. Berkshire Hathaway is different.

What success elements do Berkshire Hathaway, NATO and the US armed forces have in common?

Investors in Berkshire Hathaway value the company’s long-term and conservative management.

Berkshire Hathaway has become a beacon in the investment world thanks to its consistency and reliability. For decades, investors have made the pilgrimage to the annual meetings in droves to listen to the wisdom of Charlie Munger and Warren Buffett.

Avoiding wrong decisions

Such a status is not earned based on the number of correct decisions. Rather, it is about minimizing the number of wrong decisions. I can be right a hundred times, but one blatant mistake can destroy everything.

Many of Berkshire Hathaway’s management methods are antifragile and thus reduce the risk of such blatant mistakes. And a particular element of this management can also be found in NATO and the US armed forces.

What does all this tell us?