It is not so easy to find chances for reflection in order to detect investment mistakes. Reflection requires time, muse, and a certain amount of suffering. Because if you reflect properly and, above all, honestly, you will come across your own mistakes relatively quickly.

Investment mistakes happen and reflection is necessary

In my opinion, mistakes are unavoidable and happen even to the greatest perfectionists. You will allow me this side remark: people who call themselves perfectionists have simply not recognized that they either need more time than others or are not capable of reflection, i.e., they do not see their own mistakes. In other words: a product does not become better by the fact that a perfectionist created it. Think about it.

Conversely, reflection is necessary, because this is the only way to recognize and correct mistakes. Unfortunately, however, we tend to prefer not to see or recognize these mistakes or misconceptions. Because in the first moment, the “shit, mistakes were made” is painful. Often, we seek the mistakes or at least their cause in other people.

So reflection is tedious, counterintuitive, and often hurting. But simply repeating mistakes or allowing them to run their course is, in the end, much worse.

In short, reflection and error analysis are simply part of the process if I want to improve myself and they are also part of a life in harmony. Now, the TEV blog is a lot about finance and investing. So, what are my biggest mistakes in this regard?

Mistakes lead to painful and substantial underperformance

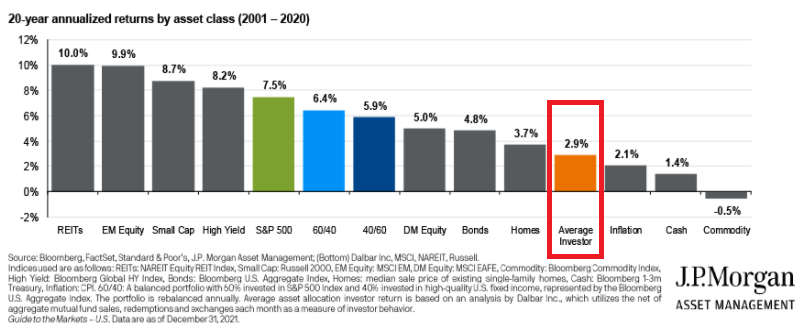

I’ve been thinking a lot about my mistakes in my investment decisions and a few clear points have emerged. The funny thing is that hundreds and thousands of investors made the very same mistakes. This also explains the poor performance of retail investors. The following chart is a bit old, but it’s still relevant.

So to really learn and become better than the average retail investor, you have to admit your mistakes and try to learn from them.

So let’s get right into it.

Too much focus on the yield

The biggest mistake, in retrospect, is that at the beginning of my journey, I looked too much at the current dividend yield. I am happy with my journey so far, but I would have been much more successful and faster if I had focused more on dividend growth companies instead of buying high-yielders. However, I was blinded by AT&T’s dividend yield of over 5 percent instead of choosing Microsoft’s dividend yield of 2.2 percent.

I was simply blinded by the amount of the quarterly distributions

Of course, it was also important to me that the company’s distributions are covered by cash flow and profit, but if I’m honest, I was more concerned that the dividend is at least secure. I didn’t pay that much attention to the potential for further increases.

Especially – and hey, I know I’m not breaking news – for young investors, it’s important to let time work. It may take time for a compounder with a yield of 2 percent to get to a yield on cost of 4 or 5 percent through increases over the years. But those are precisely the companies I want. These are the stocks that not only bring avalanches of dividends in the long run but also the corresponding share price growth.

What is my remedy to stop making these mistakes?

I have adjusted my strategy slightly. I no longer look primarily at the dividend yield for new investments. More decisive for me is the payout ratio and the growth potential based on earnings, cash flows, and fundamental business prospects. This doesn’t save me from poor decisions, but it does change the fundamental focus of how I buy shares in companies.

Too much focus on fundamentals (this one is tricky)

After many years of investing, I have also come to the conclusion that the focus on fundamental valuation is partly(!) exaggerated. My worst investments are mainly those that were valued cheaply at the time (AT&T, BASF, Fresenius, 3M). Some of these stocks have been in my portfolio for years and oh wonder, they are still (partly including dividends) substantially in the red.

Conversely, my best performers, such as Apple or Logitech were also bargains

But the truth includes other examples, such as Apple or Facebook (Meta). I bought Apple shares with a P/E ratio of 10. So yeah,I would never buy shares without considering the fundamental valuation. Because in the end, the fundamental valuation shows us how many dollars we pay for the cents of profit.

The only reason for putting cash into any kind of investment now is because you expect to take cash out; not by selling it to somebody else because that’s just a game of who beats who.

For me, the above quote is the absolute core statement of why I invest the way I do. I want to live from the fruits of my garden, and I don’t want to sell a tree. But it is even more critical that I do not pay more for the tree I buy than it gives me back in fruit within a certain period of time.

Conversely, the tree should also be healthy, strong, and vigorous. Such a tree is not cheap or more expensive than a half-moribund apple tree that has never produced an apple in its life.

So what kind of rhyme can I make out of this contradictory mixture?

Even good companies can be valued cheaply, and there are often good reasons behind this. In Apple’s case, it was the dependence on iPhones; in Meta’s case, it was the dependence on advertising revenues. Conversely, with AT&T, there was the fantasy that a vertical streaming giant would emerge with an incredible amount of data from its customers. In retrospect, we’re all smarter and know that Apple has partially broken free from dependency, Meta is fueled by the Metaverse and AI, and AT&T simply missed all the flowery promises.

So, is value investing dead?

No, I’m not saying that. It’s just far more complex than simply looking at long-term multiples and buying stocks when they are below average.

Instead, it’s about identifying the reasons for multiples’ deterioration and whether they affect the company’s core business. If the company is active in a poorly performing market, has a high level of debt, and does not have any other form of moat, then I prefer to keep my hands off the stock from now on.

In the long term, companies must also be able to compete in the market and grow

As I described in another article, there is no value without growth.

It is challenging for companies to grow when they operate in markets that do not make it easy. The tobacco and the oil sector have a hard time. IBM has missed out on the cloud business.

That doesn’t necessarily make the investments in the companies bad decisions or mistakes. Nevertheless, my mistake was that I paid too little attention to the growth criterion. Business growth is just as significant as the aspects we investors usually associate with value.

Bottom fishing – ignoring trends

When investing, I constantly look at the current development of the share price. Especially with fallen shares, it is often the desire or hope to catch exactly the low point of a price setback or to catch this relatively close.

Of course, I always add the disclaimer that you can not time the market, and there is the risk of reaching into a falling knife.

Nevertheless, bottom fishing included many investments where I invested capital in a negative trend. Unfortunately, we often underestimate how long downtrends can last. Conversely, we underestimate the tenacity of uptrends. Then, we wait on the sidelines for the one setback that may never come.

So, when you have capital stuck in a downtrend, investing more money to cheapen the purchase price seems tempting. This “averaging down” is gross nonsense, in my view. There is no shortcut. The return on initially invested money will still be negative regardless of how much I throw into the basket.

Furthermore, a bear market can last a long time. From its high in 1929, it took almost three years for the S&P 500 to bottom. Averaging down can consequently be a somewhat longer project. The question is whether investors have the capital and the mindset to stay in the “I am averaging down” business for such a long period.

Conclusion – how I try to avoid making the same investment mistakes

I haven’t wholly overturned my strategy. It basically works for me, and I am happy about the monthly dividend cash flow I get from my stocks. Investing for me is like a hobby that costs a lot of money (almost 50 percent of my active income), but also yields a lot of money. And as it is with a hobby, you change a few set screws here and there, ponder, read, try and see how it goes. Now, I don’t stick to the following anchor points like a slave, but I do adhere to them more than before.

More focus on the operating business and its future viability

For one thing, the most important thing for me is the operating business and sustainability of a business model. For example, I would no longer invest in tobacco companies these days. My positions in Altria and Imperial Brands remain in my portfolio, but I don’t buy any more shares because of the high dividend yield.

Based on my current strategy, I would not have bought BASF or Bayer shares back then, either.

In case of doubt, (a little) less focus on fundamentals and dividend yields

In addition, I focus less on fundamentals. For example, I invested the capital I generated from selling my Logitech shares and the resulting profits in Cboe Global Markets, Williams-Sonoma, AAK, Extra Space Storage, and Balchem. The stocks were relatively highly valued except for Extra Space Storage and Williams-Sonoma. They had historically below-average dividend yields, so there was much to suggest that they were fundamentally overvalued.

More concentration – in case of doubt, I say no to a stock

No more diworsificaton! Another focus is to concentrate my portfolio a bit more and to sell companies that, in my view, have no added value compared to other companies. Why do I need Reckitt Benckiser when I have Unilever, Procter & Gamble, and Kimberly Clark in my portfolio?

That’s why I say no to a stock more often, even if it looks tempting. I don’t have to pass all the eggs from all the chickens in one basket. One or two eggs from each chicken is sufficient.

Do I expect to outperform by doing this? 🙂 Rather not, I continue to assume that I would do at least as well with a World ETF. As described above, it’s more about developing your strategy, learning from mistakes, and having fun. My portfolio is my business, and I don’t need it to explode, but I want it to grow sustainably and steadily, and I want to sleep peacefully.