I recently had an interesting discussion with another private investor about investing and the current stock price developments. We didn’t address value investing in particular, but after our conversation, I wondered whether the idea of value investing might be dead these days. So I’ve been thinking a little bit about this topic in the last few days and thought that this would be an excellent opportunity for an article on the TEV Blog. I would like to address the following aspects in particular:

What is value investing?

Most people are certainly familiar with the exact definition of value investing. Nevertheless, it is useful to say a word or two about the meaning of value investing before we discuss whether value investing is dead. To put it simply, value investing is about a very basic idea of investing, namely becoming the owner of a company that generates more value than you originally put into it.

This thinking is part of our world and strongly connected to the way investors or capitalists think. In our profit-oriented, capitalist society, investors naturally don’t want to throw their hard-earned money out the window. They want value for money and a decent profit. And they see investing as a trade (in terms of a business as in the stone age). They get something (value), they give something in return (their capital), i.e. quid pro quo.

This giving and taking must be in proportion. Investors pay money to become a shareholder in a company. Accordingly, value investors focus on the value of an asset, which they receive for the purchase price. And here, they look at the difference between the value of the asset, the so-called intrinsic value, and the price they pay for it. Hence, the higher the difference, the better the deal.

Why do people say that value investing is dead?

Using this value strategy sounds simple. In practice, however, things aren’t as easy as they seem. There are even many people who go so far as to say that value investing is dead. In the following, we take a closer look at the most common arguments.

Efficient Market Hypothesis (EMH)

Many investors who argue that value investing is dead, point to the so-called Market Efficiency Hypothesis (“EMH“), which is a mathematical-statistical theory developed by the financial sciences. It was above all Louis Bachelier, Paul Anthony Samuelson, and Eugene Fama, who formed and represented the very popular and often cited EMH. According to the EMH, asset prices already reflect all available information. Thus, there can be no difference between the intrinsic value of an asset and its price.

Thanks to the internet, it is possible to know everything necessary about a company or a share. If you are not an insider (attention: potential criminal liability!), then you can assume that you know as much as any other market participant.

In terms of the factual basis, therefore, there is equality of arms between all market participants. And here it is entirely plausible to say that since everyone knows the same quantity, there is no lead or advantage. The market participants simply determine the price of a share based on the current level of information, so this price must necessarily reflect the actual value.

The random walk of stocks

The Random Walk Theory is closely related to this. It states that the future prices of assets are like the random steps of a drunk person and are not predictable. Accordingly, the question of outperformance(!) depends solely on luck.

But how does this relate to the EMH? Well, according to the EMH, information includes not only all current knowledge, but also all future expectations about the business success of a company. And here comes the crucial point. According to the EMH, only new information can influence share prices. But these are not known and random, like, exactly, the erratic steps of a drunk person.

There are hardly any brokerage costs for transactions and retail investors are storming the markets

Another aspect is the low transaction costs when buying stocks. The low costs make it possible to buy and sell stocks quickly without having to pay hefty commissions to the broker, which contradicts the “buy and hold” concept of value investors.

Why should you wait until the market recognizes undervalued companies when you can simply sell stocks at a (small) profit after a short time. After the discount brokers flooded the market, it is easy for investors to trade stocks with no or low commissions. From time to time, there are hyped stocks that are bought in extreme phases of exaggeration, especially by young traders. We know now that private investors can trigger price explosions, which applies in particular to shares that are already volatile anyway, such as penny stocks. Such herd-driven hype ensures that stock prices, in general, are less based on fundamental value data, but follow the herd that is more or less blindly investing.

So all this leads to the following question: why should you use value investing to pursue an investment strategy whose points of reference are no longer relevant for investing? To be honest, I have a clear opinion on this. But I will tell you more about it further below because it describes my investment approach, and I do not want to jump the gun here. So let us turn straight to the next argument, according to which value investing should be dead.

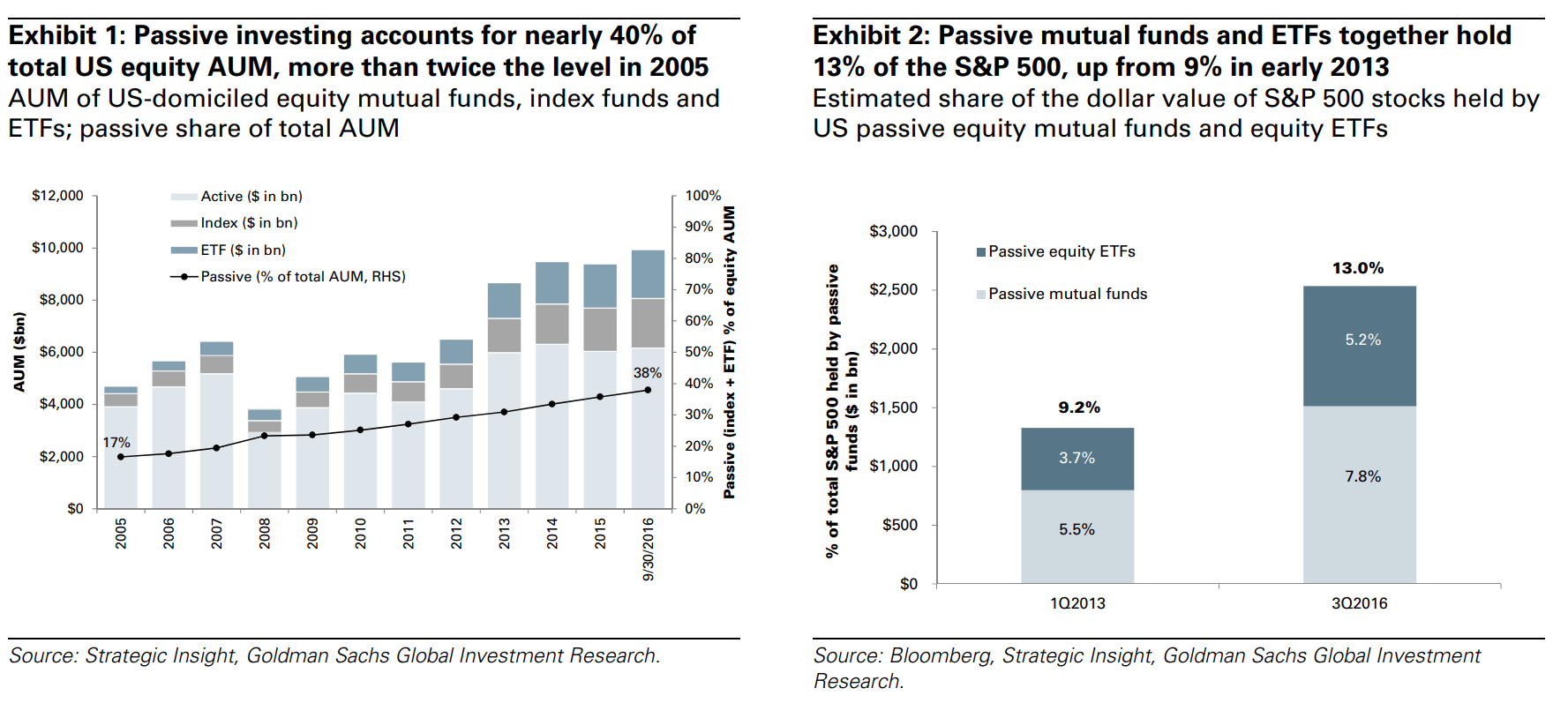

Besides, it is a common argument that ETFs (exchange-traded funds) would also support rising share prices. Likewise, these ETFs eliminate the need for stock picking, as they hold stocks across the market and have now reached such a weighting that there are no longer any real undervalued stocks. According to Goldman Sachs, more than 40 percent of all investment assets in the United States were already passively managed in 2016. Goldman expects the trend towards passive forms of investment to increase further in the future. Furthermore, the withdrawal of active investors had led to share prices moving more in unison than before. According to the bank, this should lead to the fact that membership in an index is more relevant to the share price performance than corporate performance.

Investors are now buying stocks based on their expectation of future price movements

We have now dealt with several arguments that support the thesis that value investing is dead. The investor with whom I had this discussion drew an interesting conclusion from these circumstances. He says that investors are now buying stocks not based on their fundamental valuations. Instead, they are buying stocks only based on the expectation of future price movements.

Here, trends would emerge for individual stocks, which would continue to strengthen. They last as long as the market is convinced that the trend will continue. Indeed, this consideration changes the entire meta of investing, as investors are no longer concerned with the business development of a company. The only decisive factor would then be the investors’ expectations of further price development.

Value investing is not dead because…

With having heard all these arguments, let me briefly present my perspective. It is my very personal opinion and describes my investment approach. I am not saying that I am outperforming the broader market. With my cash flow-oriented approach, I don’t want to achieve that at all. Note: If I wanted to make the best possible performance and development of my assets, I would probably simply invest in an ETF.

Overall, I think we need to distinguish several aspects.

- Firstly, the performance of stocks is linked to the economy and the economic conditions of a company.

- Besides, it is, of course, the case that a stock is also an asset class that behaves relative to other asset classes.

- Thirdly, EMH was tested… and falsified.

- Investing in ETFs also has its downsides.

- Furthermore, there are always advantageous and less advantageous periods for the purchase of companies. The (probably impossible) art here is to choose the right company more often than the wrong company. But just because the odds of being successful with stock picking are tiny does not mean that value investing is dead. Let’s dive into these different aspects in more detail.

Let’s go! 🙂

Stock prices and the economy are still linked

So, we have heard the argument that the share price development depends on the expectations of the market participants and less on the economic situation. I think that’s pure nonsense. Shares are participations in companies. Shareholders are the co-owners of these companies. In doing so, they invest in an entity whose success in the market determines whether it continues to exist or not. Accordingly, a successful company with growth prospects is worth more than a faltering company in a falling economic market.

Those who buy companies only because they expect prices to rise are speculating on these rising prices. This is where my betting slip analogy comes into play, which I have described elsewhere. Here, investors buy shares because they assume that the share price will continue to rise:

For me, who wants to become an owner of companies and therefore wants to get a substance for his money and not just a coupon that might increase in value, this consideration was new. In this respect, the perspective has changed. A share is no longer the proof of ownership of a company but a kind of betting slip with which one can bet that share prices will rise. With this change in perspective, the focus has shifted significantly from investing to speculating.

In the end, such investing boils down to a self-fulfilling prophecy. As long as investors assume that the price will rise and therefore buy shares, the price will rise. But this has nothing to do with investing. It is like gambling.

A stock is also an asset class that behaves relative to other asset classes

Indeed, there are currently few alternatives to stocks for private investors, which, of course, drives investors into the equity markets and is supporting the current rally. But that can change as other asset classes such as bonds, overnight deposits or gold become more attractive.

Investors need to understand that businesses also have “coupons”. These coupons may perform poorly compared to the coupon of other asset classes. Why should an investor invest in a company that has a cash flow yield of just 3 percent when he or she could also invest in a high-grade bond with a yield of 5 percent.

The sentiment towards equities as an asset class can therefore tilt. As an investor, I do not want to base my investment decisions on the current trend. I want to sleep peacefully at night. And I can do that best when I know that there are outstanding companies in my portfolio. Their price may fluctuate, and so will my net assets. But as long as my companies are profitable every year and let me participate in their cash flow, I am happy and satisfied.

EMH was tested… and falsified

Let’s also dig a bit more into the EMH which I really like. It illustrates something very obvious: investors are rarely better than the market because they never actually have a knowledge advantage. If they think a stock is undervalued, they are automatically betting against the market. Yet history shows how bad investors are at beating the market.

However, and this is the flip side, the EMH, even if it is widely promoted in different forms, could not yet be fully confirmed. Eugene Fama’s article “Efficient Capital Markets, A Review of Theory, and Empirical Work“, published in 1970 in the Journal of Finance, is noteworthy because it made the EMH operational.

Such operationalizability is particularly valuable for science because it allows a thesis to be tested and verified. And here we go. As soon as there was a falsifiable thesis, the very thesis was shortly falsified. There have always been developments such as the financial crisis, where the predictions of the EMH have not come true. Likewise, the EMH cannot explain phases of apparent overvaluation like the dot.com bubble in 1999.

Does this mean that outperformance is possible for private investors? I think so because markets can obviously also be inefficient. But it is very unlikely that individuals will succeed. Conversely, the falsification of the EMH shows that value investing is not dead, especially when it comes to avoiding risk. Value investors have passed the bubbles while the EMH has failed.

Investing in ETFs also has its downsides

Investing in ETFs is a terrific thing to do. Investors can thus easily link their returns to the returns of the global economy. With just one investment, they can passively invest in thousands of stocks.

But this effect comes with a downside. Share prices also provide information about a company’s health. Correspondingly, a decrease in the share price indicates that there is a problem. How important this information function can be, becomes apparent when a company is poorly managed. If the share price is no longer relevant, mismanagement can be hidden for a very long time. According to Goldman Sachs,

the decline in the shorter-term information content of share prices heightens the importance of the responsibility that boards, and particularly their independent directors, have to closely monitor and evaluate fundamental corporate performance.

AllianceBernstein even stated that passive investing is worse than marxism. However, I do not want to go into the rabbit hole of passive vs. active investing. At least, I think we can agree that the rise in passive investing provides a reason for value investing with regard to risk management (without saying that active stock picking or value investing brings more return automatically). An investment strategy of this kind requires extensive due diligence and not just blind buying. Value investing is not primarily about the share price and its information function, but about the intrinsic value of a company and thus avoiding bubbles.

In bubbles, equality of arms is painful

When it comes to bubbles, there is no equality of arms. Newcomers meet experienced analysts, naive people meet “greedy bankers”, financial pornography meets reputable consultants in family offices, and so on. The individual market participants differ not only in their skills and capabilities, but also in their motives (long-term or short-term, short or long, risk-averse or risk-orientated, and so on).

This clash of professionals and amateurs, anglers and geologists, greed and nativity, and different levels of knowledge and experience can cause prices to move away from the intrinsic value of the respective assets. The perfect examples are the bubbles that have occurred from time to time in various asset classes. Just take the cryptocurrency crash of 2018 as one example. Some currencies have fallen by over 80 percent. This crash was more severe than the bursting of the dot.com bubble. We want to stay away from these bubbles and hypes.

There are advantageous and less advantageous periods for the purchase of individual companies

So if I can be the owner of an excellent company, I am not interested in the maximum return within a short period of time. Instead, I want to pay a price for a company that is appropriate. Only I can say what amount is reasonable for me and what price I am willing to pay.

And in doing so, I am guided by the principles of value investing. A company that costs less today than a few months ago can turn an overpriced hype into an attractive buying opportunity and vice versa. Microsoft, Apple, and Walmart are excellent examples of this. Anyone who bought here at a time of undervaluation can now enjoy massive price gains and dividends. Besides, these companies show that it is also worth holding shares, even if the share price doesn’t rise for a while.

However, there are also less advantageous times to buy specific companies. Just take a look at the current price levels of Walmart, Apple, and Microsoft. You can see that you don’t get the same today as you did a few years ago. For the same intrinsic value, you now have to put much more money on the table. Currently, this is much more than you had to pay in the past years or even decades.

Times may change, but value remains value

Even if times change, I think one thing always remains the same. Quality will prevail in the end, even if it is expensive now and then. Nevertheless, I am not willing to pay any price. After due diligence, each investor must decide for himself which price is appropriate. But what is completely wrong is to buy shares because you believe that the price will continue to rise. This is how Warren Buffett and Charlie Munger described this approach:

The only reason for putting cash into any kind of investment now is because you expect to take cash out; not by selling it to somebody else because that’s just a game of who beats who. […] Investment is putting out money to get more money back later on from the asset and not by selling it to somebody else but by what the asset itself will produce.

In this sense, no matter which investment approach you choose, I wish you only…

…all the best,

TEV!