Do you know this feeling? Everywhere on the Internet, at work, on the subway, people are currently talking about how much money they have made with stocks in the last few months. Meanwhile, your portfolio has performed quite well but remains far from having 500 percent or even 1000 percent gainers. So why are people making more money with stocks than you or I? Well, let’s look closely here. There is a lot to suggest that you will still be successful in the long run, even if you think otherwise when you see the other investors’ results.

Don’t get fooled by the numbers

Numbers are numbers, aren’t they? Not really. As always in life, everything is relative. In fact, numbers, despite their objective nature, are often misleading. And many of the legendary stories about other investors’ stock gains quickly vanish into thin air when you take a closer look at the numbers.

Don’t confuse book profits with real profits

First of all, you should not confuse book profits with real profits. Book profits can go as fast as they come. Especially in bubble-like hypes, it isn’t easy to find the right exit and secure profits. Anyone who brags about their book profits is by no means sure that they will end up with those book profits as cash in their bank account.

Just take Keith Patrick Gill as an example. He is also known as DeepFuckingValue/Roaring Kitty, who played a not-so unimportant role in the GameStop Short Squeeze Drama at the beginning of 2021. When the GameStop stock corrected, Keith Patrick Gill saw book losses of USD 15 million in just one day. So yeah, there might be people who are making more money with stocks than you do, and that in a short time, but that doesn’t necessarily mean that they see those gains as cash in their bank accounts.

Don’t confuse the percentage gains with the absolute (book) profit

And then some people brag that they are already 2,000 percent up. While I am calculating how many thousands of USD/EUR in dividends they could get by buying shares of 3M with these profits, they then announce that they want to double their 200 USD/EUR stake once again. In the end, they had invested only 200 USD/EUR, which has now grown to an impressive 4000 USD/EUR, but that is not an amount that should make you jealous. It’s a gamble that paid off. Cool thing.

Your daily fluctuations can be far above these amounts if you have a heavy portfolio. Is that a reason for you to walk down the street and show off? Certainly not. So if you’re in the stock markets for the long haul, your 10 percent gain with solid and conservative stocks may be worth more in absolute terms than a 2,000 percent gain with a gambler who speculates with small amounts.

Don’t confuse “timing the market” with “time in the market”

We must always be aware that our or others’ short-term (book) gains are, in the end, a matter of luck of the right timing. Even if we see other investors who have achieved great performance in a short period of time, these investors are rarely able to continue the performance for long. There is a simple truth: timing the market correctly is impossible in the long run. As I said before:

Over the long term, it is impossible to predict the exact course of the stock markets. It is, therefore, possible that investors will miss the best days, and then their returns will be quite poor. In most cases, such investors then perform worse than the broader market.

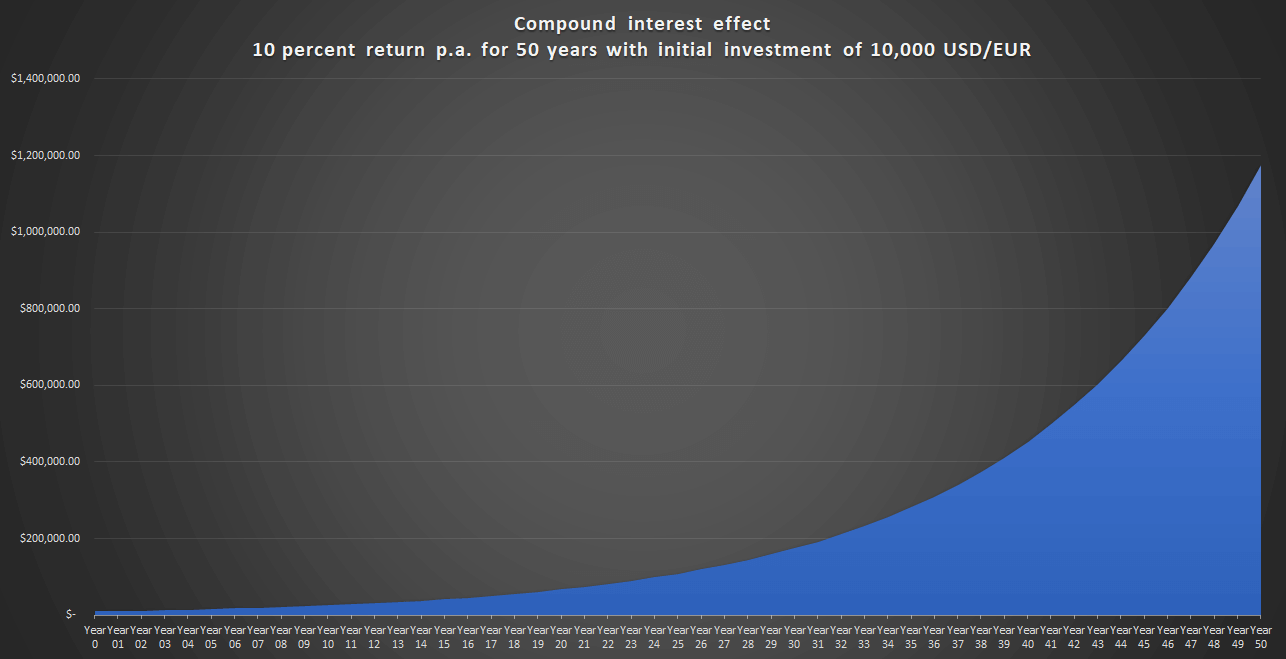

After all, in the end, time in the market is the essence of most of our returns. The reason for this is the compound interest effect. Below you see the results of investors who invest 10,000 USD/EUR once and keep the shares in his/her depot. If these investors earn a 10 percent return per year, then after one year, they will have 11,000 USD/EUR. And now the magic happens.

In the second year, they get another 10 percent on the 11,000 USD/EUR. But this time, the gain accumulates to 1,100 USD/EUR instead of 1,000 USD/EUR as in the first year. And so the gains increase year after year. After 50 years, the investors have more than 1 million USD/EUR without lifting a finger.

Of course, you should keep the following things in mind here:

- You probably won’t get an annual return of 10 percent.

- You need to factor in the impact of inflation, which nibbles away at your profits and reduces their purchasing power.

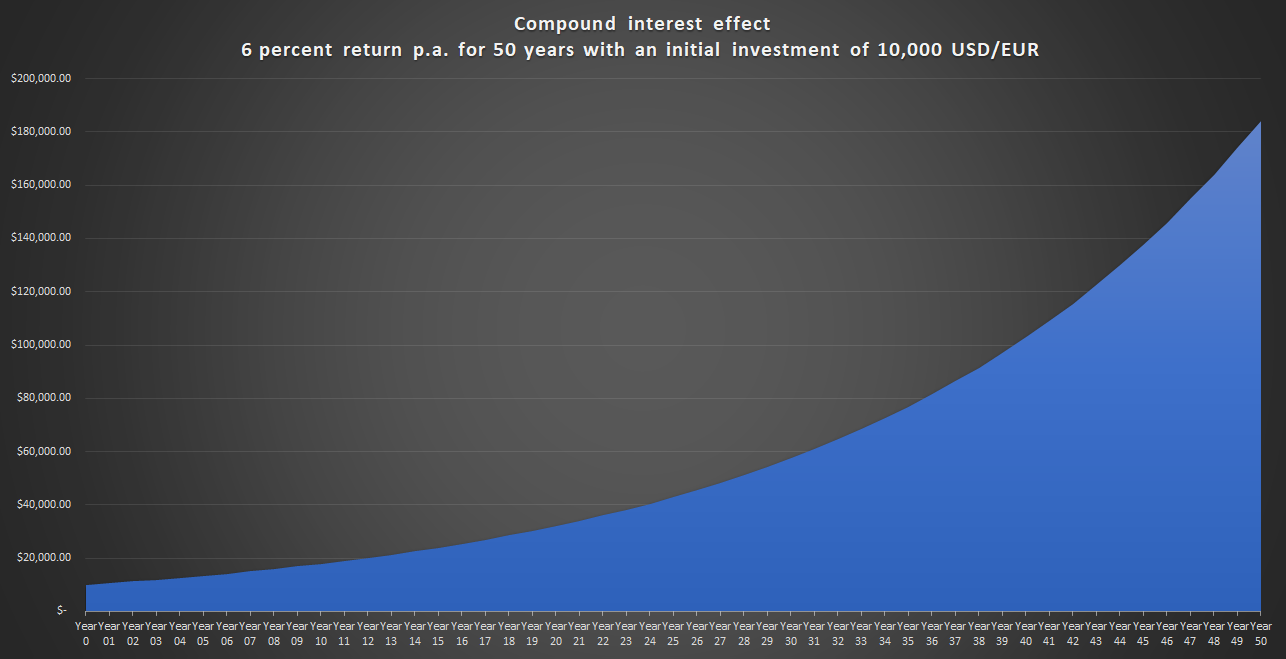

- In the end, you can expect a historical average return of between 5-7 percent.

Therefore, the above picture is primarily intended to show you the power of the compound interest effect, which always works, whether with annual gains of 10 percent or only 6 percent. Furthermore, we will see in a moment how you can boost the return even with a yearly return of 6 percent. But even just this 6 percent on a one-time investment, with the help of the compound interest effect, adds up to a nice sum in the end. And that’s precisely the point. We want to let time work for us and not try to find the exact moment for the best investment.

Don’t let your mind trick you

Many times we let our brains trick us. It’s human. Nevertheless, it helps to be aware of the traps our brain set for us. Especially in social bubbles or echo chambers, such cognitive flaws can cause great harm if they lead to wrong financial decisions.

Be aware of recency bias when looking at your underperformance

Do you remember the 10 percent market decline in 2015? Or 2018? Those were turbulent times, I can tell you that. Between October and December 2018, the S&P 500 lost 20 percent. Crash prophets had already started to proudly count their gold nuggets and predicted for the 10th time the collapse of the financial system since 2007. CNN wrote in big letters, “2018 was the worst for stocks in 10 years“. Today, the events are no more than a footnote in the S&P 500’s history.

The phenomenon that we tend to perceive these events differently today than we did back then is called “recency bias.” Our brain puts much more importance on current events than on historical ones. That may be an advantage from an evolutionary point of view as the decisive factor for my survival is the hunger I have now and not my cold from five years ago.

Conversely, we should be aware that the events we describe as dramatic today will be seen quite differently five years from now. That’s why I’m not worried about an underperformance today. It’s just a small time frame. In five years, I won’t remember this hassle. So why should I bother today? In the course of my investment career, I have seen a number of stocks in my portfolio that were down 50 percent and then turned positive. These include Dialog Semiconductor (unfortunately sold too early), Hugo Boss, Tanger Factory Outlet, and Publicis.

A quick dive into survival bias – The tale of the forgotten failures

When you see all the people who seem to be making more money than you in stocks, don’t overlook the losers. What did you say, they don’t exist? Of course, they exist. Just because they don’t brag about their losses doesn’t mean they don’t exist. Don’t confuse the lack of proof of existence with evidence of non-existence. And don’t get fooled by the survival bias. This is a cognitive bias in which we tend to tune out the failed experiences. The idea can be simply verified with a mental experiment.

Imagine we give 10,000 apes each day two bananas.

One banana has a green mark, and one banana has a red mark. The banana stands for the share price prediction of a company XY. The red marking represents a short position, the green position represents a long position. Each ape is assigned an investor. The investor will take either a short or a long position depending on which banana the monkey eats first. In the evening, each investor closes his or her position.

The following day, the whole game starts all over again. However, this time, only the ape-investor tandems that made a profit on the previous day are allowed to play, i.e., only those who were correct with their short or long position. Let’s assume that the apes have a 50:50 ratio with their choice of banana, so 50 percent each reach for the banana with the green marking and 50 percent for the banana with the red marking.

So with each run, we will eliminate 50 percent of all tandems from the game. They have failed and will no longer play a part in this experiment. After one round, we have 5,000 tandems left, then 2,500, then 1,250, and so on. In the end, we will have a handful of highly successful tandems. Would you nevertheless put money on one of the tandems? Why should you?

The experiment suggests that all our shining lights and role models were only those who were most fortunate not to be among the forgotten failures.

In the end, the performance of the average investor is disappointing

At this point, followers of a particular strategy often attach a graph that confirms the outperformance of their strategy. Let’s take the Dividend Growth Investing approach as an example. Advocates of this strategy, like me, then refer to a chart that proves that such a strategy outperforms in the long run. But this is circular reasoning and proves nothing as past performance is not indicative of future performance.

On balance, the performance of investors has been disappointing. According to J.P. Morgan, the average investor gained just 2.9 percent per year in the mega bull markets from 2001 to 2020. Investing in an ETF would have been a far better decision.

Time and antifragility

We have seen above the poor performance of the average investor. Over time, all investors will come closer to this average. While there will be investors who are slightly above it, there will be investors who have performed even worse. But in the end, hardly any investor will have managed to achieve above-average returns every year from 2001 to 2020. And with every year, there are more of these forgotten failures.

Time allows evolutionary mechanisms to take effect here as well. Little by little, time exposes the unsuitable strategies that may have been successful for a few years but ultimately failed. A portfolio invested for the long term and broadly diversified also makes use of this effect, only it takes a little longer to have an impact. In such a portfolio, for example, an ETF, time will automatically weed out all the bad companies and let the good, strong, and successful ones prosper.

With “time in the market”, investors automatically benefit from this evolutionary mechanism. Their portfolio becomes antifragile without lifting a finger. So, in the long run, these investors, with their broad investment style, have a good chance to be more successful than the typical investor.

Therefore, time is an excellent tool in many ways. It helps us to show which of the new-fangled theories or methods are bullshit and what has been able to withstand all the falsification attempts. Time smoothes out excitement. It also helps us reduce complexity by peeling away fragile elements and leaving antifragility. And time teaches us to be patient.

There are no shortcuts

Everything I have said above can be broken down into a simple heuristic that has so far not been falsified as a universal decision-making aid: “There are no shortcuts“.

The fact that shortcuts rarely work is due to the way Mother Nature works. In nature, everything runs according to a program: trial, error, failure, second/third or even millionth attempt, success. Without the attempt, and often without the failure, it doesn’t work. We can’t simply bypass all the errors and mistakes when we strive for something new and unachieved.

This is another reason why we should not be distracted by the performance of others. Whenever you think that all the people are making more money with stocks than you, just remember that there are no shortcuts in life.

And when someone claims to have found one, we should let time decide whether a strategy is really superior. In most cases, it will turn out to be BS.

Understanding our approach to investing

My readers and I share the same way of investing. Not everyone likes that. That’s okay. As I will explain below, many strategies work for different people. If we wanted the simplest possible way to gain an average performance, we would invest in a global market ETF. But we don’t because we all have different goals and strategies to achieve our goals. Besides, investing is not a competition. Everyone has to choose the strategy they feel happy with.

Our fundamental view

When we see other investors with their fat short-term profits, we need to stick to our approach as we are not looking for the path to quick wealth. We don’t do that because we don’t chase the quick money since we try to avoid the risks that come along with that. We believe that it is impossible to build this wealth quickly and without risk. That is why we have a fundamental approach focused on the long-term quality of our investments. When I buy shares in a company, it’s because I want to become an owner. I don’t bet on being able to sell the share to another investor at a higher price. I want to become the owner of a good business, and I don’t want to overpay for that. Period.

Our quantitative approach – making more money by using the compound interest effect

Besides that, I would like to become the owner of many companies. Therefore, I buy shares of many companies. And I don’t buy them only once, but I buy them whenever I have free money, which increases the base of my capital and the leverage of the compound interest effect.

The mistake of not leveraging the compound effect

It is, therefore, a mistake not to use leverage. And this is precisely what many investors do when they realize their first high profits. They don’t use the profits to increase leverage but use them to buy cars, TVs, or other things. In doing so, they lose this leverage.

The far better way is to increase the leverage by continually putting new capital to work for us. Above, you have seen a graph of how a one-time investment develops over 50 years with an annual return of 6 percent. In the end, our one-time investment of 10,000 EUR/USD had grown to an amount of over 180,000 EUR/USD.

Now imagine adding 4,000 EUR/USD per year to that over the next 50 years. Thus, after 50 years, we would have invested capital amounting to 200,000 USD/EUR in addition to our initial investment of 10,000 USD/EUR. The compound effect has increased this amount to over 1.3 million EUR/USD.

This performance shows you the following:

- The long-term approach is crucial even if you partially underperform compared to other investors. The most significant gains come from the compound interest effect, which only unfolds its effect after years or decades.

- Besides, a further boost will come if we continue to invest capital in excellent and profitable companies. We lose this leverage when we consume capital or even take profits to buy expensive luxury goods, etc.

The difference between always having to be right and being allowed to be wrong

Investors with a strong outperformance often use aggressive strategies as well. The problem, however, is that as opportunities increase, so do the risks. That is simply a fact. This idea is the basis of the considerations presented in this section. My thesis is that someone with a high overall risk should rather not be wrong too often, while someone who takes a lower risk is allowed to be wrong here and there. Let’s go into some detail.

Every stock picker makes mistakes

Every stock picker who invests in stock markets for a few years has already made mistakes and anyone who says otherwise is lying.

We must acknowledge that we are imperfect and certainly do not know the future. Accordingly, misconceptions and mistakes are entirely normal and cannot be prevented.

Warren Buffett was completely wrong in his assessment of Amazon or Apple. His investment in IBM was also rather unfortunate.

These things happen to the best of us. Bill Ackmann, for example, completely miscalculated his investment in the pharmaceutical company Valeant and made a loss of more than 3 billion USD with money that did not even belong to him but to the investors in his hedge fund Pershing Square Capital.

We are allowed to do things that are not always the most right decisions

If mistakes happen to even the best investors on this planet, then we will make them too. The key to long-term success is to limit the exposure of one’s assets to the risk of an ultimate loss.

We diversify. That allows us to be wrong here and there. We didn’t put all our assets into Bitcoins or Apple or Amazon shares decades ago. That may hurt now when we see the profits of other investors. However, even though I just called these decisions wrong, they are not mistakes in a strict sense but rather natural and inevitable when we pick stocks. The decision not to invest in Bitcoin ten years ago was not the very best decision. And it’s okay that we made such wrong/not the very best decisions. These are not real mistakes which I’ll discuss below.

The decisive factor besides time – we have to avoid making the really wrong decisions

So it may hurt when we see other investors’ gains. But we can not overlook the underlying risk of such investment decisions. When we make particularly risky investments for our assets, we are not allowed to be wrong very often. From my point of view, a wrong decision is mainly the following: irreversible losses.

Irreversible losses are the actual yield killers and thus the real mistakes in investing. Not achieving the very best return isn’t a mistake. It is, as I said, just not the very best return. You can see the impact of wealth-destroying events or mistakes in the chart below.

Such events significantly impact the overall performance, even for investors who have a higher return because of their risky strategy. Let’s assume that a few high-risk investors achieve an annual return of 10 percent. As in the example above, the initial capital was 10,000 USD/EUR, and the yearly investments 4,000 USD/EUR. But with only three extreme events of losing 50 percent of the assets twice and 25 percent once, the investors did worse after 50 years than those who achieved only an annual return of 6 percent.

Conclusion

What can we learn from this section?:

- Strong performance is inevitably always accompanied by a substantial risk. Risks that affect the sum of the assets can adversely affect the total return.

- Those who take a high risk do not necessarily have a better performance in the long run, even if it looks like it initially.

- It’s not a mistake if you haven’t made the best decisions. Real mistakes are only decisions that lead to irreversible losses. Investors who take high risks depend on not making such mistakes. Investors who do not take this risk are allowed to make “wrong decisions” (i.e., not the best decisions).

I keep preaching it: for me, investing is not a competition

Let’s move on to another point that I find very important but often very difficult to comply with. Investing is not a competition. That is an essential statement. It’s not about how your neighbor performed this year or last year. Investing means wealth management, and here the first rule is: don’t lose money (see above). But if you start comparing yourself like in a competition or even want to win, the first rule then is to beat your opponent. With this change of perspective, however, you become vulnerable to mistakes.

That’s why we instead focus on our performance. That doesn’t mean we are uncritical. Of course, we reflect on our strategy. But just because tech stocks are currently rising particularly strongly and other investors are achieving high returns with them, I don’t sell my dividend pearls to put more capital into tech stocks as well.

So when people are making more money, be patient

I know it can be hard to see that other investors are making more money. It’s especially annoying because you’ve been investing for years or even decades, you read annual and quarterly reports, and you only invest in companies with a reasonable valuation. And then you see that a Twitter post by Elon Musk is enough to shoot shares to the moon, regardless of the underlying business.

Frustration is normal in such situations. I can only suggest staying calm and patient. Your companies will not become worse than before just because the value of other companies increases.

I follow the rules of simplicity

I like that investing is quite simple. Look for good, profitable companies. Compare their profits and cash flow per share to their share price. Are you willing to pay the share price for the profits? If so, you’ve found a potential investment. If not, then leave the stock, even if it continues to rise in price. Spontaneously, I would summarize the rules of simplicity as follows:

I don’t try to outsmart the market

In the long run, we are not better than the market, so we should not pretend to outsmart others, which means that a broad-based attempt at market timing will not work in the long term. That’s why I don’t even try to base my wealth management on such a strategy.

I do my due diligence

Everyone needs to do their due diligence before making investment decisions. It is very simple. These are your assets and, therefore, your responsibility.

There was never a free lunch so I won’t chase after it

It is easy to assume that all other people are making more money with stocks than you. But still, remember, nothing is given for free in life, certainly not on the stock market. There is no such thing as a free lunch. We don’t know how share prices will develop in the medium term. Shares that only rise can fall just as quickly.

So don’t try to pretend that profits on the stock markets are guaranteed. You become an owner of companies, and that is always risky.

It’s relatively simple, yet so hard, especially in times of greed or fear.

In this sense, I wish you the very best,

Man, I am so pissed with this bull market. I literally pray for bear crash market, please God, 50 % cheaper :)) Good read , thanks, FOMO is our enemy, gotta think like busienss owners and be patient.

Haha, indeed. It’s awful that almost everything is overpriced and at the same time knowing that you’ll lose in the long run on the sidelines.

yes, we are in a downturn– who knows how long– finding your blog this morning will help me be more level my thinking and actions. Thank you!

Inflation is really on the high rise and its not getting funny.