Welcome to The European View’s calendar of ex-dividend dates. As every week I want to show you some stocks that will go ex-dividend in the next days. I’ll also review a few companies that are currently in the focus of investors or that have an attractive fundamental valuation. Additionally, I’ll give you some insights into my retirement portfolio and share my thoughts and experiences about individual companies with you. This week, we’ll take a closer look at AT&T and Mastercard and the reasons for their different fundamental valuation.

Why dividends?

Dividends are a great thing. Even in bad stock market times, they provide a juicy cash flow per month. If you want to benefit from dividend payments as quickly as possible, you must pay attention to the ex-dividend dates. This date is the day on which shares are traded without their subsequent dividend value. Only if you owned the stocks on this day are you entitled to receive the dividend.

Why yields are a simple way to screen companies

Usually, there are always exciting dividend companies that are worth a second look. And the dividend yield is an excellent way to get an initial overview of companies that may be worth further due diligence. To help you get started, at the end of each week, I will publish the ex-dividend dates for the coming week of individual companies here in the TEV blog.

Why I handpick and double-check the ex-dividend dates

I have recently noticed that many databases do not indicate the respective numbers and dates correctly. Spontaneous dividend cuts, in particular, are only partially taken into account, or in some cases, not at all. As a result, the value of such overviews dwindles enormously.

Therefore, I’ve decided to select individual companies by hand and check the dates and dividend yields on the company websites, which means more work for me but increases the value of this section enormously, so it is worth it 🙂

Ex-dividend dates calendar for the second week of July including AT&T and Mastercard

Here we go. Besides the ex-dividend dates of AT&T and Mastercard, there are some banks this week, as well as a high-yield ETF that might be worth exploring. Below you will find an overview of next week (tip: if you use a Smartphone, hold the Smartphone horizontally)!

| Company | Payment Date | Yield | In my retirement portfolio |

|---|---|---|---|

| Monday, July 07, 2020 | |||

| Bank of Nova Scotia (BNS) | July 29, 2020 | 6.3% | NO |

| John Wiley & Sons (JW.A) | July 22, 2020 | 3.64% | NO |

| Global X Superdividend ETF (SDIV) | July 14, 2020 | 12% | NO |

| Tuesday, July 08, 2020 | |||

| AXA (AXAF) | Jully 09, 2020 | 3.95% | NO |

| Bank of China (BACHF) | August 07, 2020 | 7.5% | NO |

| Christian Dior (DIOR) | July 09, 2020 | 1.3% | NO |

| Steelcase Inc. (SCS) | July 15, 2020 | 4.5% | NO |

| Wednesday, July 09, 2020 | |||

| AT&T (T) | August 03, 2020 | 6.9% | YES |

| British American Tobacco (BTI) | August 24, 2020 | 6.7% | NO |

| Iberdrola SA (IBDRY) | August 13, 2020 | 1.63% | NO |

| Mastercard Inc. (MA) | August 07, 2020 | 0.53% | NO |

| Johnson Outdoors Inc. (JOUT) | July 23, 2020 | 0.75% | NO |

| Trinseo S.A. (TSE) | July 23, 2020 | 7.1% | NO |

| Thursday, July 10, 2020 | |||

| City Office REIT (CIO) | July 24, 2020 | 6% | NO |

| Toronto-Dominion Bank (TD) | July 31, 2020 | 5.1% | NO |

| Verizon Communications (VZ) | August 03, 2020 | 4.4% | NO |

| Friday, July 11 2020 | |||

| Bank Ozk (OZK) | July 20, 2020 | 4.8% | NO |

| Hormel Foods Corp. (HRL) | August 17, 2020 | 1.9% | NO |

| Marvell (MRVL) | July 29, 2020 | 0.7% | NO |

| Universal Corp. (UVV) | August 03, 2020 | 7.7% | NO |

What’s interesting this week?

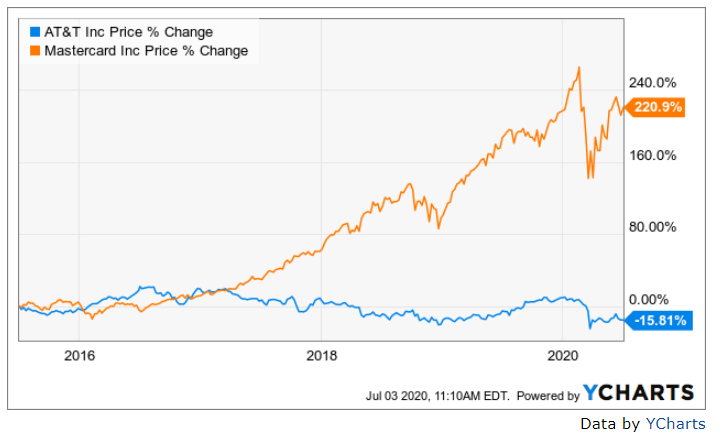

This week AT&T and Mastercard, among others, are going ex-dividend. I bought shares of AT&T many years ago. Mastercard, on the other hand, was fundamentally always too expensive for me. Nevertheless, if we only look at the course price development, Mastercard would have been the better choice. Even the high dividend yield of AT&T does not change the significant underperformance of the company.

That’s being said, it is impressive how much the valuation of the two companies falls apart. While AT&T is a bargain in all fundamental aspects, Mastercard is overvalued by almost 100 percent. On the other hand, there are good reasons for this disparity in valuation.

AT&T

If we look at AT&T in a historical context, the company is undervalued in terms of adjusted earnings since 2017. The same applies to cash flow. If AT&T would climb to the fair share price based on the adjusted profit, shareholders would now make a profit of almost 30 percent. We, therefore, have enormous upside potential for the company. Added to this is a current dividend yield of nearly 7 percent, and right now, AT&T distributes only just over 50 percent of its cash flow in dividends. Since AT&T also has relatively reliable cash flow streams, the dividend should be relatively safe, despite COVID-19.

Mastercard

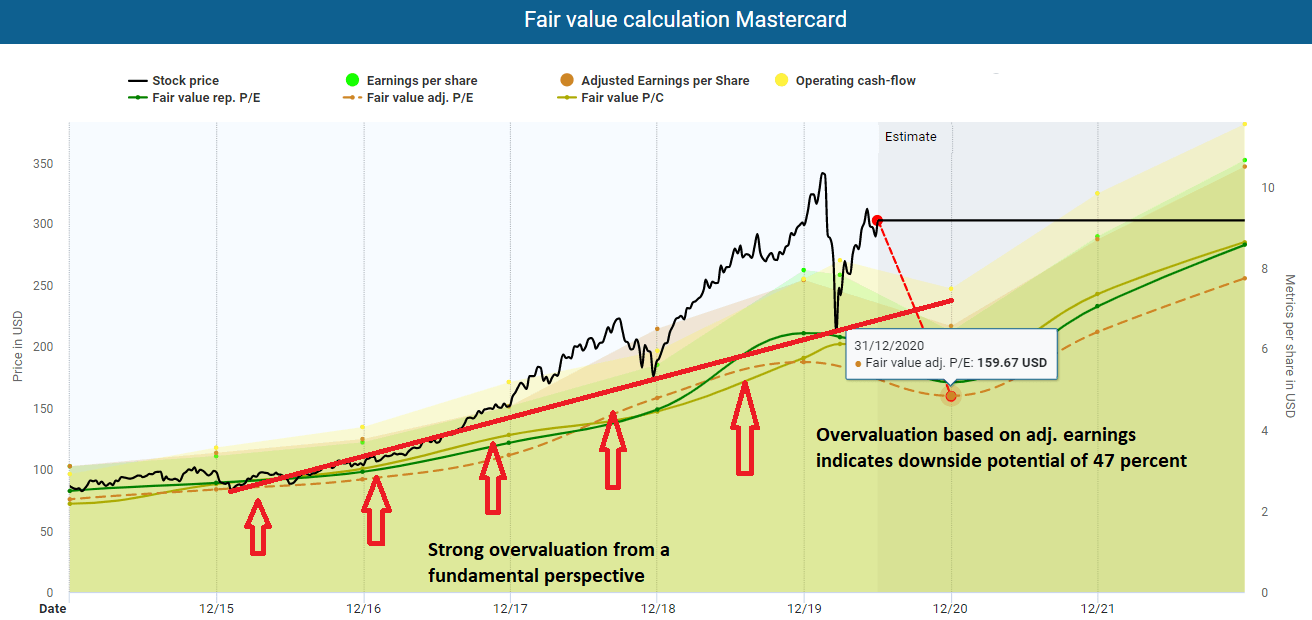

The situation is entirely different with Mastercard. The Mastercard stock is overvalued in terms of adjusted profit and cash flow since 2016. Only at the time of the COVID-19 crash was there a short window of opportunity for investors, in which the share price slipped halfway into the fair valuation. If the company were to return to its fair value based on adjusted earnings, the share price would have to fall by almost 50 percent. A look at the fair value based on cash flow (green line) also reveals a high downside potential.

Another point is the dividend yield of Mastercard, which is only half a percent. However, the company only has a payout ratio of less than 25 percent and an average 5-year growth rate of 24 percent. Investors can profit enormously from the growth of the dividend, while AT&T has only increased its payouts by a few percent in recent years. Interestingly, ten years ago, the dividend yield was just as high as it is today. Nevertheless, investors who have not sold their shares since then have a yield on cost of over 7.5 percent today (!), which shows once again that dividend increases are more important for long-term investors than the initial yield.

Taking business model, growth pace and balance sheet into account

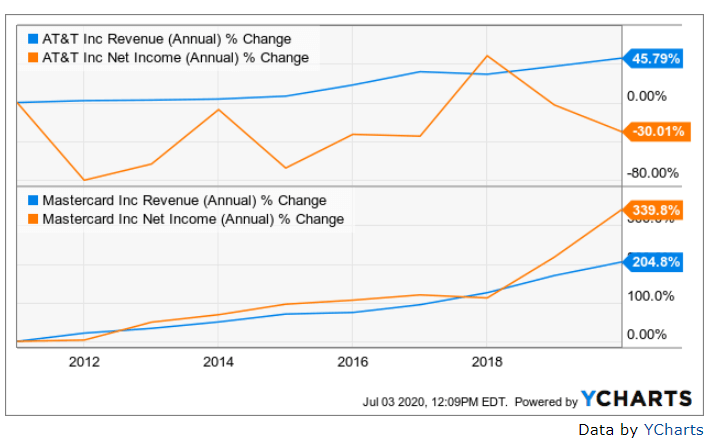

Both companies show excellently how important it is to look at individual key figures in context. Of course, you have to keep in mind that both companies operate in entirely different areas and industries. You also have to take into account that Mastercard is growing strongly, while AT&T has hardly shown any organic profit and turnover growth for years. Instead, the company is struggling with the losses of its TV subscribers.

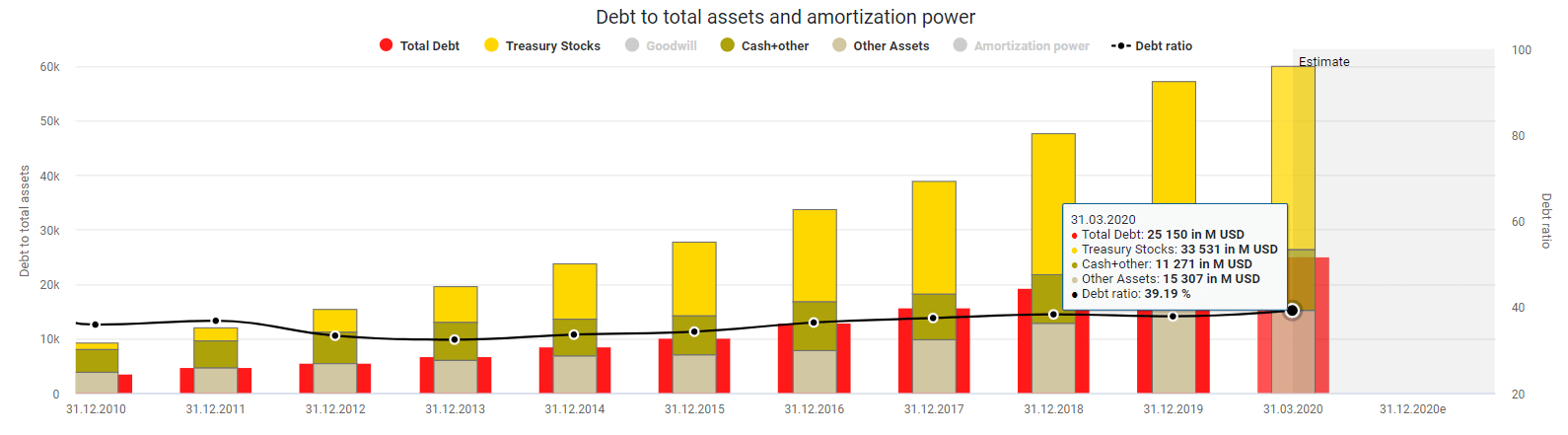

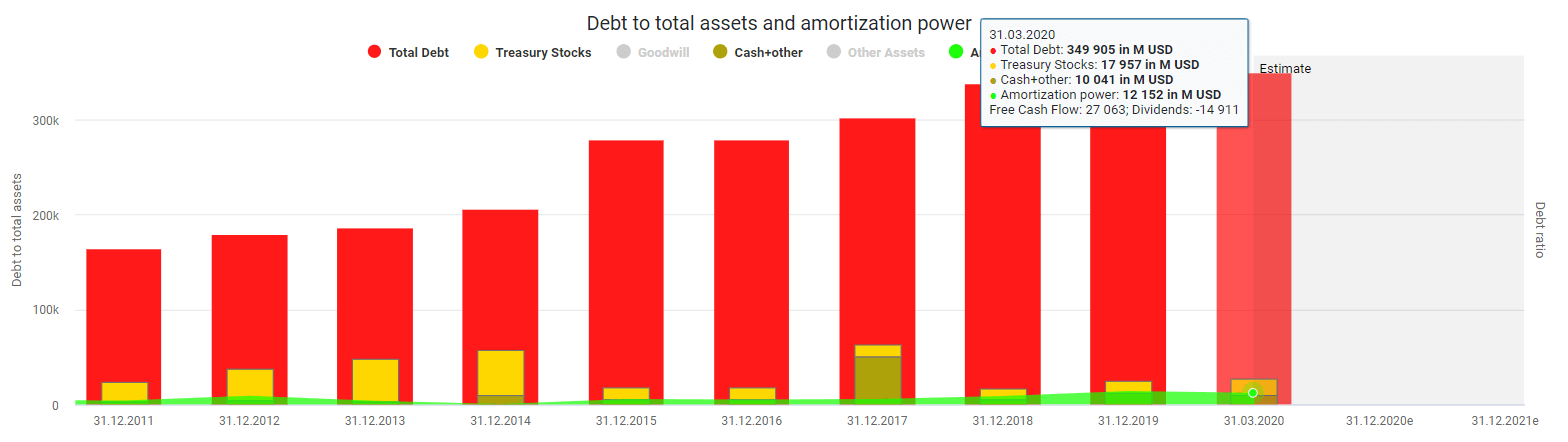

Financial stability is equally important. As you can see here, Mastercard has an excellent balance sheet. The company only has a debt ratio of less than 40 percent. Besides, it is sitting on a big pile of its shares, which it has repurchased massively in recent years.

After the $85 billion the situation acquisition of Time Warner, the situation is different at AT&T. The company has a debt ratio of over 60 percent, which is still not dramatic, but yet less comfortable than with Mastercard. Above all, the debt is pretty high compared to the existing cash and treasury stocks. Consequently, AT&T still has a long way to go to become debt-free, which, of course, lowers the intrinsic value of a share and justifies a discount.

Take home message

This week we have seen from our ex-dividend companies AT&T and Mastercard that companies should never be selected based on only one valuation method. The analysis of companies goes far beyond that. Just keep in mind: A low P/E ratio might be a warning sign, and a meager dividend yield does not necessarily have to be an exclusion criterion for an investment, even for income investors. I missed the time window for Mastercard. Next time I hope to make my move!

Time to do your due diligence

Has a company caught your interest? Attractive dividend yields should not be the only reason to buy shares of a company. Instead, you must carry out careful due diligence before every purchase. The Internet offers you excellent opportunities in this respect.

My analyses here on the TEV Blog are an excellent way to start (click here). You can also contact me here or ask the community in the comments if they can help with your due diligence.

Otherwise, I use tools like those from Dividendstocks.cash and Seeking Alpha to do further research. You can also find me and my analyses on these platforms.

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

That said, feel free to let us know if a stock has been overlooked or you know of a stock that is particularly attractive and where the ex-dividend date is coming up.

Is a stock here attractive for you? If so, let the community also know and write a comment.

You can also share this post with your favorite network:

[…] bought Mastercard stocks ten years ago with a modest dividend yield of 0.5 percent even then, has a yield on cost of 7 percent today and is thus on a par with AT&T, including high price gains. Nevertheless, there are good […]