Qualcomm is not far from its pre-Covid19 high. If Qualcomm breaks through the USD 96 per share barrier, it will mark a new all-time high. I expect the company to break this mark this summer. But what does that mean, given the downside risks that exist, which of course not only affect the global economy but also companies like Qualcomm? I have bought the company again and again after price setbacks. As a result and due to the price increases, the company is now one of my five most significant positions, with just under 3 percent of my broadly diversified retirement portfolio. Given Qualcomm’s share price performance, it is time to pause for a moment and reflect on my investment in the Qualcomm stock with this analysis.

Where are we now, and what’s behind us?

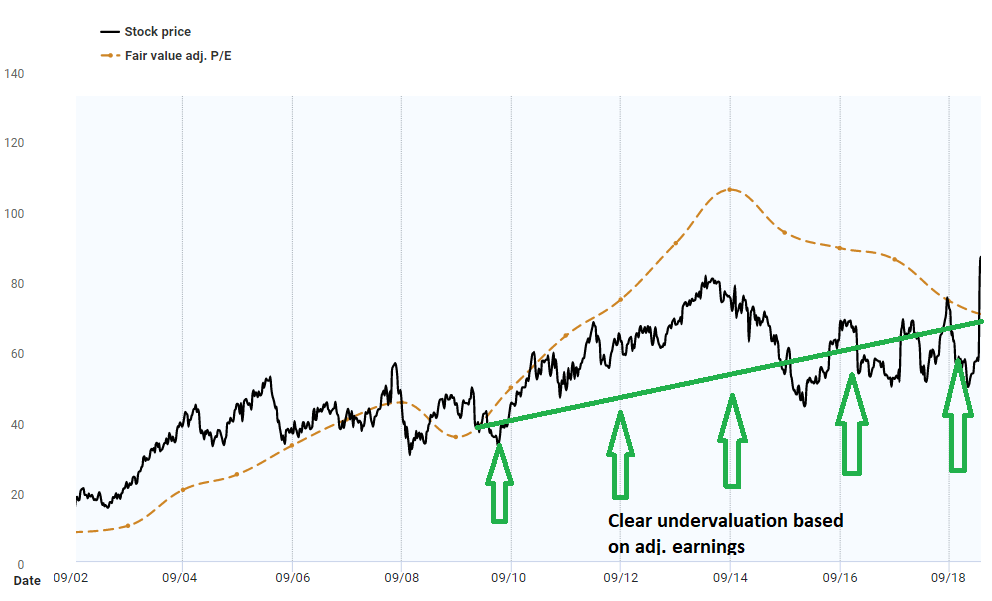

The past few years have not always been easy for Qualcomm investors. The problems the company was facing were like a greasy soap opera, as I have already summarized in another analysis. On the one hand, we had failed takeovers on several fronts and a very tough battle with Apple. On the other hand, Qualcomm has a very close relationship with competition authorities and worldwide. All this is more or less over now. In the end, all takeover attempts failed, Apple and Qualcomm got along, and most of the proceedings with competition authorities were brought to an end. Of course, all this had left its mark on Qualcomm’s share price. As a consequence, the company was traded at an extreme discount for several years.

One can also see that the discount was also due to a somewhat stagnant development of revenues, free cash flow, and net income. Only recently, in 2019 in particular, have the numbers recovered and increased.

What lies ahead?

So that was the past, short and sweet. Now let’s turn to the future. The future holds great promise for Qualcomm, and it all starts with a number and a letter: 5G. I’ve written a lot about Qualcomm’s prospects and Qualcomm’s products in these markets (you can read it here, here, and here). To sum things up, here is my conclusion from one of my slightly larger Qualcomm analyses:

If Qualcomm manages to transfer even a portion of its existing monopoly position to other markets created by the introduction of 5G, investors can look forward to golden times. In addition to the traditional wireless market, management has focused on the promising automotive sector and the IoT sector and has introduced the first products and services for these markets.

If we do not want to get lost in the microcosm of details, this conclusion hits the heart of my investment thesis. For me, an investment in Qualcomm was always about the technological edge that the company has developed over several cycles. I assumed that the company would take this lead in 5G, and there were enough signs that it would.

And after all these years of undervaluation, the market has recognized this potential as well. The result, however, is that Qualcomm is now overvalued in terms of adjusted earnings. At a fair value based on adjusted earnings of approximately USD 74 per share, there is downside potential of almost 20 percent.

One only has to look at the current development of case numbers in the US and the withdrawal of an economic opening in many states. Besides, you should expect that current expectations regarding future profit development are too optimistic because of COVID-19. Current trends in the number of people infected indicate that any significant reopening of the economy could lead to a sensitive spread of the virus. This could lead to renewed restrictions and relapse of a total standstill of the economy.

Will I sell my Qualcomm stock?

Qualcomm is overvalued now. The dividend yield is also meager by historical standards.

If you invest in the company now, you will get less than a few weeks, months, or years ago. In this respect, I was right when I pointed out in March that a price of USD 75 per share is probably one of the last possibilities to get the stock so cheap. While the price fell a little further in the course of the COVID-19 crash, we are now already 20 percent above my buy rating. But that doesn’t mean I’m going to sell my stock. There may be reasons to sell shares even as a long-term investor, but in my opinion, overvaluation is generally not one of them. Why should I?

Qualcomm has excellent growth prospects and pays a good dividend. If you bought the stock in mid-2016, at a time when it was massively undervalued (see above), you now have a yield on cost of about 6 percent. Why give up this comfortable situation just because an overvaluation justifies a price correction that may never come? In the end, this is just an attempt to time the market, and we all know that it is almost impossible to predict the best possible time to buy or sell stocks.

Should COVID-19 worsen, Qualcomm will be able to withstand it. Admittedly, the current debt ratio of 90 percent is a bit high, but Qualcomm has a lot of cash on hand and generates high cash flows. Additionally, the dividend payouts of USD 3 billion per year is covered twice by cash and cash equivalents. That’s why I think we could consider the dividend as safe, even if the economy is terrible for a few more quarters.

Conclusion

After a long time, I give Qualcomm only a neutral rating because the key metrics point to an overvaluation. The overvaluation and possible deterioration of the economic situation in the wake of COVID-19 reveal an immediate downside risk of approximately 20 percent. Nevertheless, I will not sell my Qualcomm shares, even though they account for almost three percent of my portfolio.

Don’t get me wrong; a fundamental valuation of a company is crucial for me. And as we have seen at Qualcomm, it makes sense to wait until companies are undervalued. However, this does not mean that I automatically sell in case of overvaluation. If the basic strategy of the company is still good for me, I will, of course, keep the shares. I then simply wait with additional purchases and invest my money in other companies with a better fundamental valuation. And that’s my approach to Qualcomm. I keep my stock long-term, but I’m not buying any more right now.

–> Click here for more analysis <–

Qualcomm is part of my diversified retirement portfolio. If you enjoyed this article and wish to receive other long-term investment proposals or updates on my latest portfolio research, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.