In today’s fundamental stock analysis, I look at the Alibaba stock to see if an investment could be an option for you or not.

Introduction

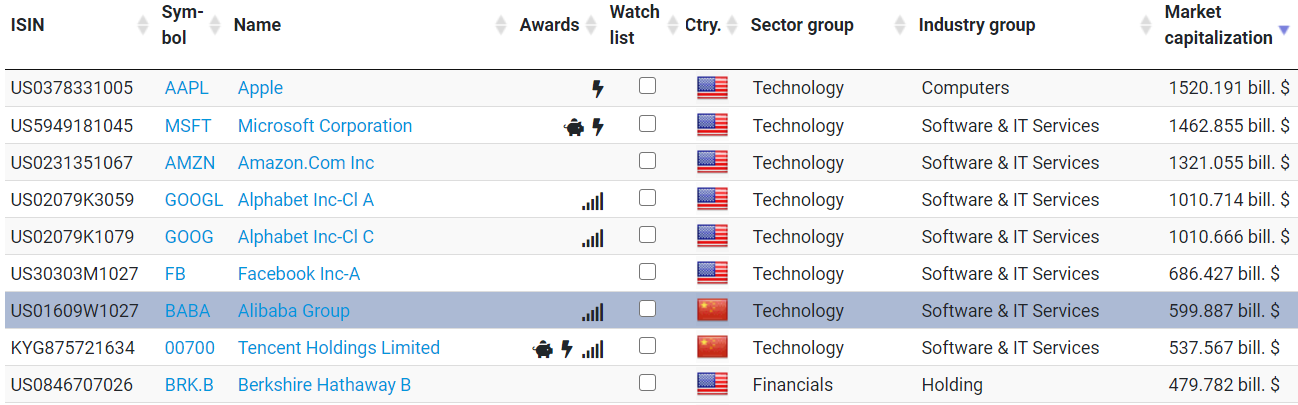

The days when the Alibaba stock or other Chinese Internet giants like Tencent or Baidu were considered insider tips for investors are long gone. Both China and its big flagship companies have become significant players in our globalized world. Reflecting their outstanding importance, Alibaba and Tencent are among the top 8 companies with the highest market capitalization in the world, ahead of Warren Buffett’s Berkshire Hathaway:

After my recently published Tencent stock analysis, Alibaba is now the next promising company from the circle of “BAT” man stocks.

As always, I would appreciate it if you could give me short feedback in the comments below or share this post if you liked it or had the opportunity to pick up some valuable thoughts.

Alibaba’s business model

I often see Alibaba being compared to Amazon. However, this view is too short-thought. Instead, you should look at the companies in isolation and compare at most where both giants face each other as direct competitors. As with Tencent, Alibaba cannot be reduced to a single business. The footprint the company leaves behind in the digital world is deep, and accordingly, the individual markets in which Alibaba is active are diverse or even confusing.

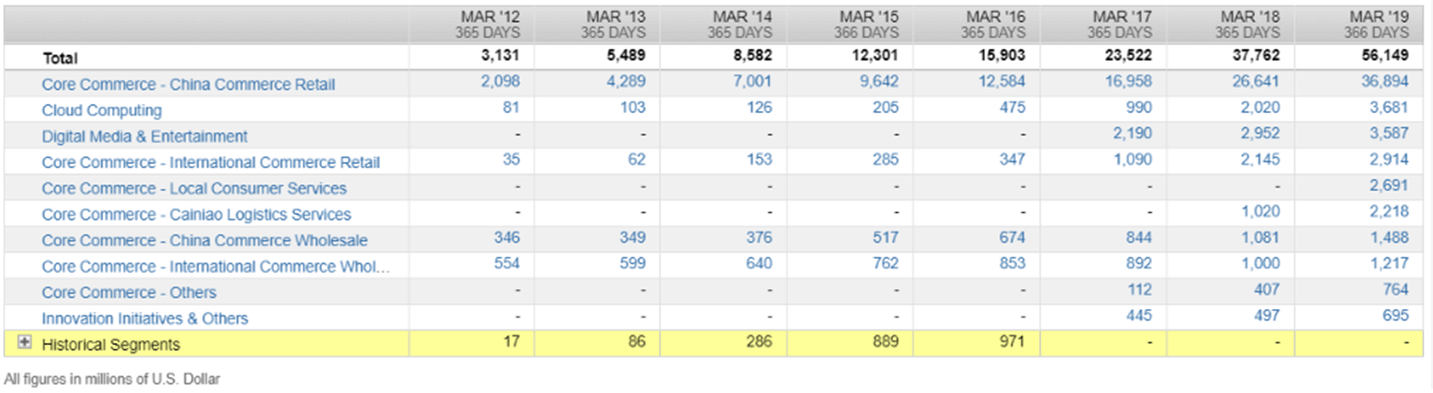

In such cases, the first thing I look at are the reports of the US Securities and Exchange Commission (SEC). If these are not available, I take the respective annual reports. There you will find brief details of the company’s business segments and their performance. There, you can see, that Alibaba divides its business into four main segments, of which the core commerce segment is subdivided down into different sub-segments, which are ordered by region (China and international) and buyer (commercial [wholesale] or private [retail]):

Behind these segments are innumerable individual activities (and usually also websites), so that a closer look is necessary to understand the business activities.

The “Core Commerce” segment

In the main segment, “Core Commerce”, Alibaba bundles all national and international platforms in retail and wholesale. Measured by the GMV scale (Gross Merchandising Volume), which is important for the industry, Alibaba is the world’s largest retailer with its platforms.

In addition to the national platform 1688.com, which addresses the Chinese market, Alibaba offers the largest B2B platform in the world with its internationally oriented platform Alibaba.com that is used by commercial sellers in more than 190 countries. B2B refers to “business-to-business” and means that sales on this platform are not made to end consumers, but to commercial sellers. B2B is also called “wholesale”.

In the B2C sector (Business-To-Consumer or also “retail”), Alibaba has created national and international sales platforms with Tmall and Alibaba, on which merchants sell their products directly to end consumers. Here you can already see a big difference to Amazon. Alibaba itself does not sell any products and therefore does not need any logistics centers or staff for this segment. If you’re looking for a Chinese equivalent to Amazon, JD.com would be a better choice for you.

TAOBAO Marketplace, on the other hand, is a marketplace where private individuals and at least smaller merchants can sell their goods directly to other private individuals. TAOBAO is, therefore, more in the C2C area (Consumer-To-Consumer) and can be compared primarily with eBay. The platform hit a nerve with the Chinese citizens right from the start. TAOBAO came to the Chinese market in response to eBay’s expansion plans and ousted the American competitor within three years, despite eBay’s outstanding size.

The importance Alibaba holds in the e-commerce sector can be seen on the so-called Single Day. Since 2009, the consumer madness, based on Black Friday, has always taken place on 11.11. of every year. The volume that Alibaba handles via its platforms is gigantic. In 2019, the company already reached the $1 billion mark after only 68 seconds. After 24 hours, the company reported sales of $40 billion and thus a new record.

The “Cloud Computing “segment

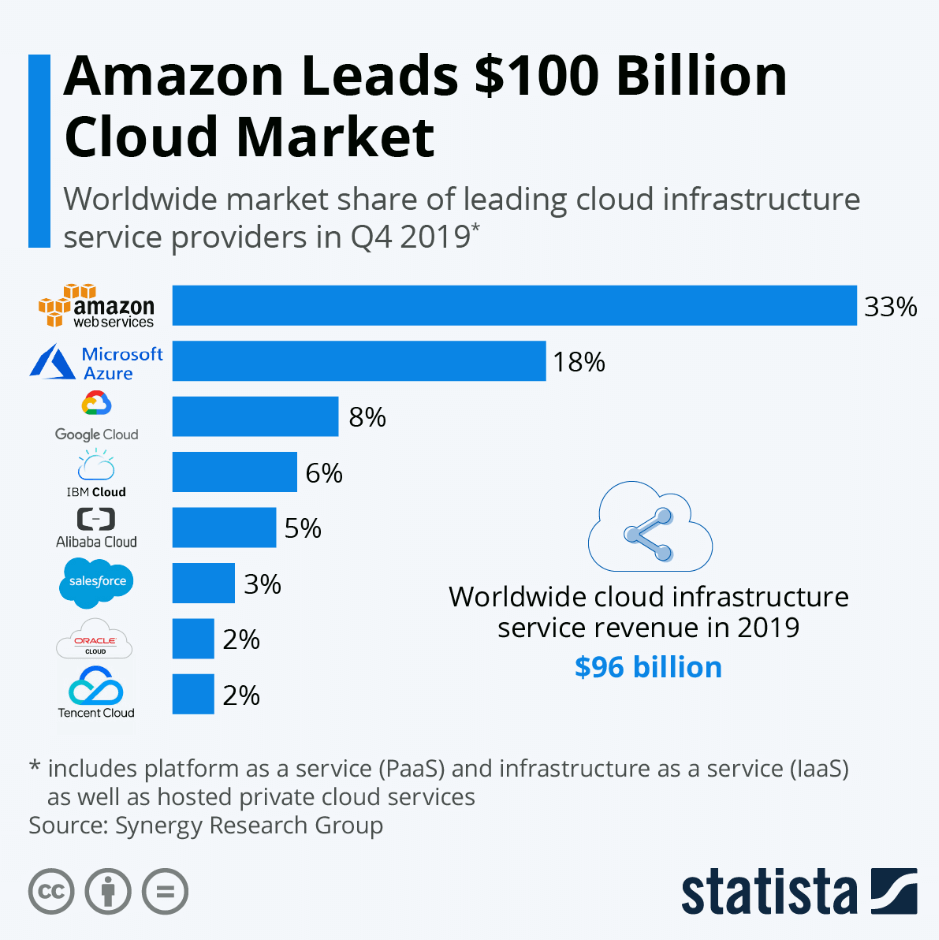

Alibaba has also become an integral part of the promising cloud computing market. In the field of IaaS (Infrastructure as a Service), in which Alibaba provides other companies with the infrastructure for cloud computing, the company defends its third place worldwide. In China, Alibaba is even a clear market leader in this segment. But if you also take into account the area of PaaS (Platform as a Service), which includes additional software in addition to the infrastructure for cloud computing, Alibaba is only in fifth place worldwide behind Amazon, Microsoft, Google, and IBM.

Alibaba’s position as a chaser in the cloud segment explains why its cloud business is highly deficient because Alibaba is putting a lot of money into the business to reduce the gap between itself and its competitors.

The “Digital Media and Entertainment “segment

The “Digital Media and Entertainment” segment is attractive. Alibaba intends to use the insights gained from the “Core Commerce” segment and the data technologies used to offer consumers additional content from the media and entertainment sector. To this end, Alibaba can draw on its “Youku” platform, the third-largest video platform in China, and its “UC Browser”, which is widely used mainly on mobile devices.

The “Innovation initiatives and others “segment

With the fourth segment, “Innovation initiatives and others”, Alibaba has created the space to develop further service offerings and products for the digital economy. The range is broadly diversified. Of particular interest is the smart speaker Tmall Genie, which, according to the company, is the number one smart speaker in China and is binding consumers even more closely to the company.

Ant Financial – An ant as a unicorn

With the financial company Ant Financial, Alibaba even holds a unicorn (start-ups with a market capitalization of one billion USD) in its portfolio that is not consolidated in Alibaba’s balance sheet. Ant Financial, which also includes Alipay, offers extensive financial services. With a market value of between $150-$200 billion, Ant Financial is considered the most valuable start-up in the world. According to rumors, Alibaba is preparing the IPO of its jewel, which should bring the company some more cash.

Business growth

Now that you know what markets Alibaba is active in, we can dive into the fundamental analysis of the company. In a first step, let’s take a look at whether and how strongly Alibaba has grown recently. This aspect is particularly important because the company does not pay a dividend, and investors can only benefit from the company’s success through the profitable growth of the business and the associated price gains.

Revenue, earnings, and cash flow

Alibaba’s revenue growth is impressive. From just $3 billion in 2012, it has grown to over $73 billion today. Revenue has increased more than twentyfold in that period. Besides, it is expected to rise to $90 billion in one year:

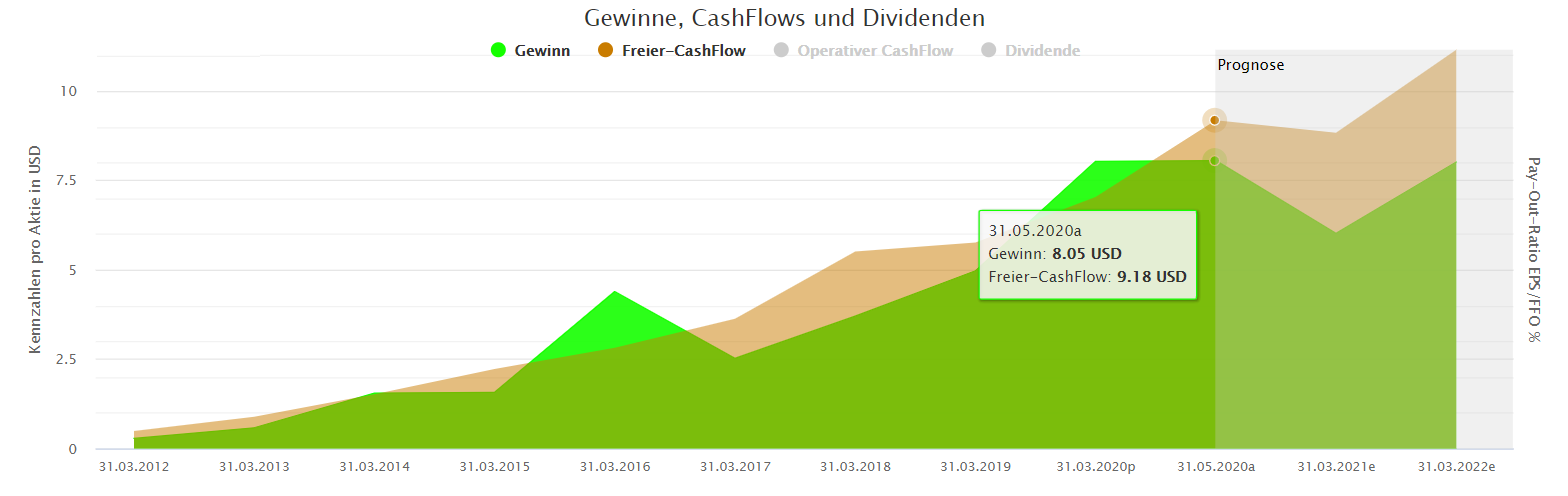

Earnings and free cash flow of the Alibaba stock have also risen sharply in recent years. Since 2012, earnings have grown from $0.28 per share to $8.05. Free cash flow has increased from $0.49 per share to $9.18 per share, respectively.

The devil is in the details

But be careful, these numbers are worth a second look. After all, the entire earnings growth is based on only one of the company’s four segments. But first, I would like to draw your attention to another aspect. Contrary to the trend towards ever more extensive share buybacks, Alibaba is diluting the profits of its shareholders by issuing newer shares. In the chart below, you can see the adverse effect on the overall profit of the shareholders. For example, in 2020, earnings of $0.20 per share are expected to be offset by a dilutive impact of -$0.18.

Fundamental Alibaba stock analysis: Profitability check

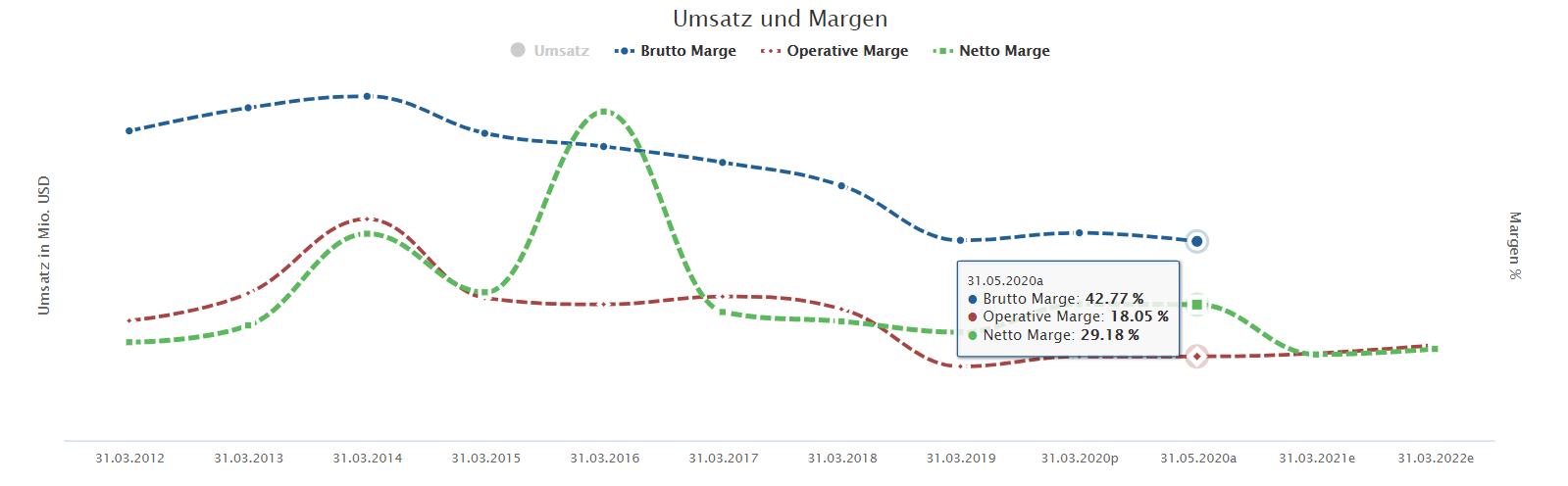

Profitability has fallen continuously in recent years. The gross margin has fallen from once over 70 percent to almost 40 percent. A clear downward trend is also evident in the operating margin and net margin.

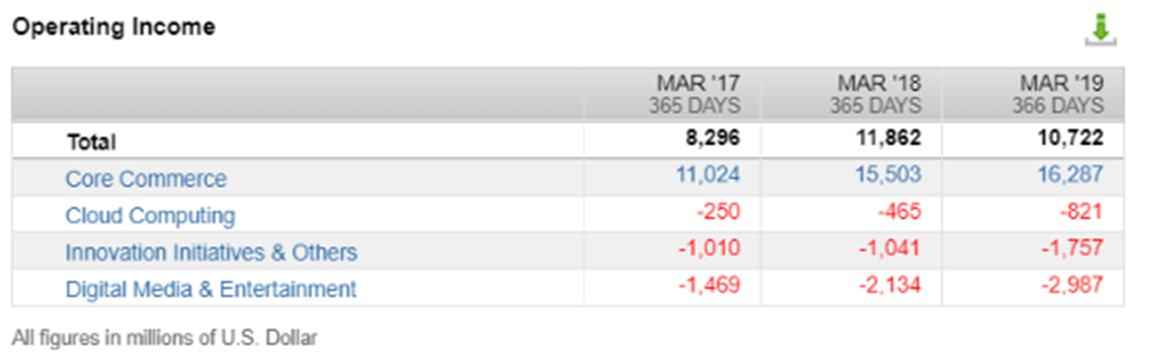

A closer look at the balance sheet will give you an explanation for this development. Alibaba is still making losses, some of them high. Only the “core commerce” segment is delivering stable profits. Surprisingly are the deficits in the cloud business, which is usually highly profitable. While the losses in 2017 were still 250 million USD, they amounted to 821 million USD in 2019. Here Alibaba is investing massively to catch up with competitors like Amazon and Microsoft.

However, in the picture above (revenue by segment), you have seen the pace of revenue growth in the individual segments. In the “Core Commerce” segment, Alibaba was able to almost triple its sales within two years, in the Cloud segment, the company even achieved an even more substantial growth by a factor of 3.6.

Still, the company is burning money massively in three out of four segments, but Amazon proves that this does not have to be wrong. It is part of the strategy of such companies to invest every dollar earned in new growth. Since Alibaba pays no dividends and receives additional money through the issue of new shares, it can afford to go this way. The increase in revenues and the increasing cash flow show that Alibaba’s management knows what it is doing.

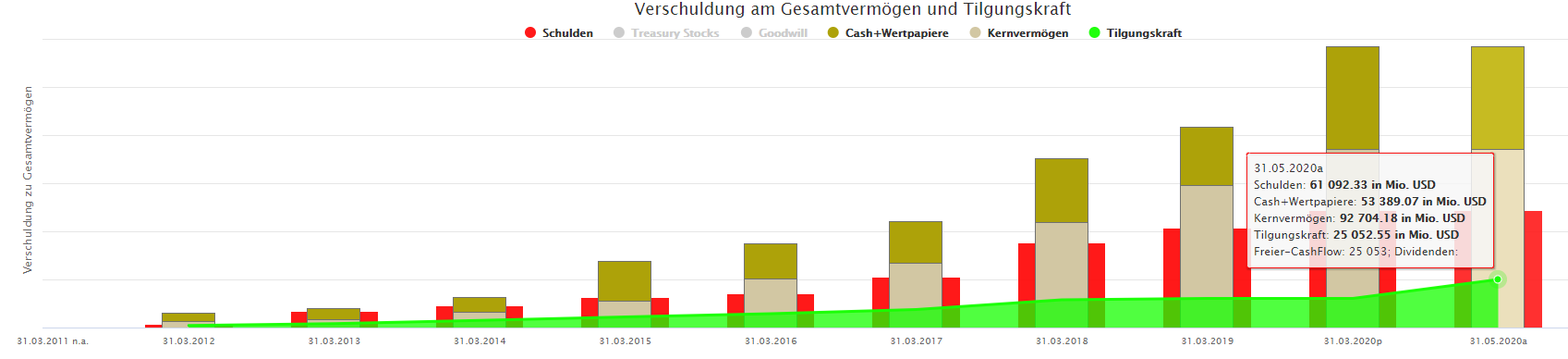

Moreover, the financial foundation is stable. The company’s current debt of $61 billion is offset by the free cash flow of $25 billion, which means that Alibaba can use its free cash flow to pay off more than a third of all its debts from a standing position, which speaks for a high repayment power.

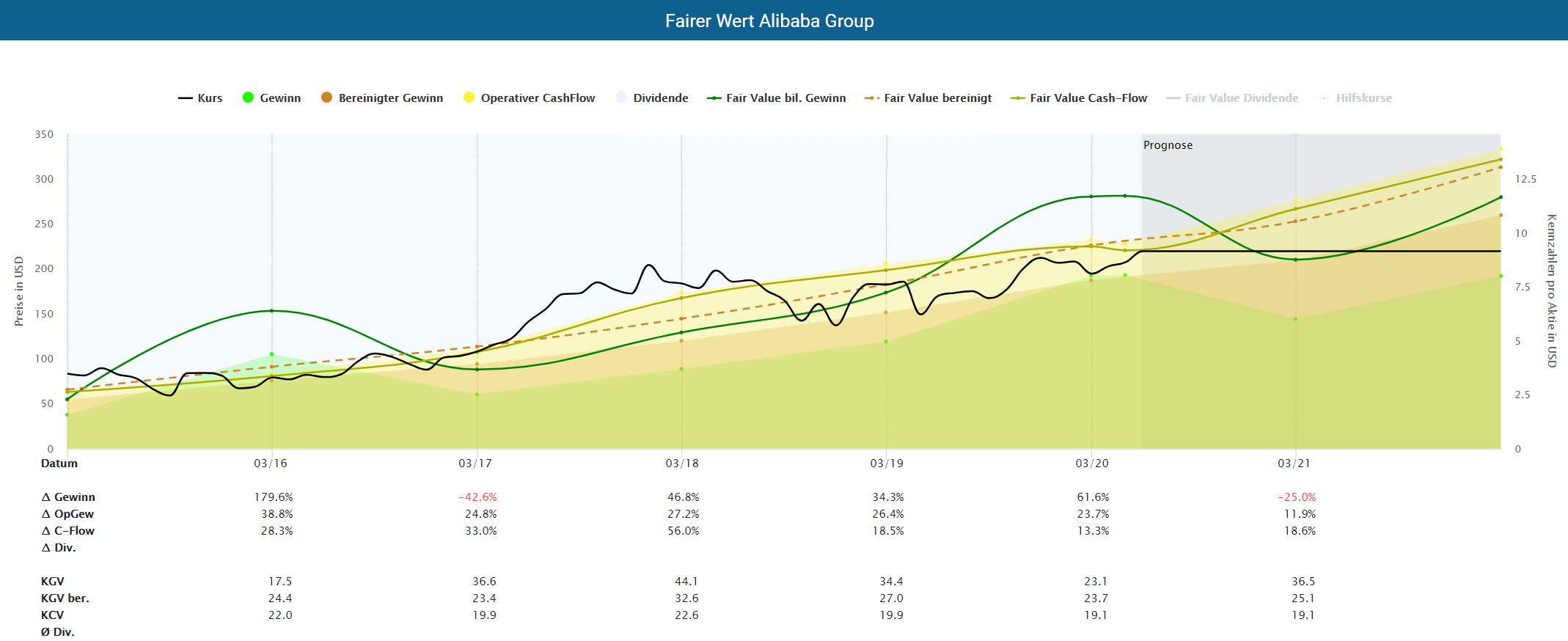

Is the Alibaba stock attractively valued?

From a fundamental perspective, the Alibaba stock currently seems fair to even slightly undervalued, in contrast to the years 2017 to 2018, when the share showed clear signs of overvaluation. Those who bought Alibaba shares at that time have hardly achieved any returns to date. Since Alibaba does not pay dividends, the price gains achieved alone are decisive for the success of the investment. Therefore, it makes sense to wait for a time window within the Alibaba share is fairly valued. According to the fair value calculation of DividendStocks.Cash, which also takes into account the adjusted profit, this seems to be the case at the moment.

A political downside risk is the trade dispute between the USA and China. Recently, the Americans had passed a bill due to the balance sheet fraud at Luckin Coffee that facilitates the delisting of foreign companies on American stock exchanges but is mainly directed against Chinese companies. Alibaba has, however, been able to reassure its investors somewhat by referring to the 20-year-long cooperation with PWC as its auditor.

Fundamental Alibaba stock analysis conclusion: Growth at all costs

The Alibaba stock is attractive for investors who can live without dividends and would like to diversify their portfolio geographically with a Chinese company. When you invest in Alibaba, you get growth in promising markets into your portfolio. After all, similar to Amazon, growth has a top priority, so you should be aware that growth comes at the expense of profit. The rapidly rising sales with declining margins illustrate the path that Alibaba has taken that also involves accepting temporary losses in some segments. Fortunately, the company can afford this strategy, so Alibaba shareholders will likely emerge as winners in the end.

–> Click here for more analysis <–

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.