New week, new fundamental stock analysis. This time I’m analyzing the Nvidia stock. Enjoy!

Nvidia stock: from hero to zero and back

The Nvidia stock has been especially interesting for gamblers with hard nerves in the last twenty years. Years with exorbitant price gains of several hundred percent were followed by years in which the share price fell by 70 or even over 80 percent.

Nevertheless, in the long run, as so often, patience and the ability to suffer have paid off. Those who have had their shares slumbering in their portfolio since 2001 are now pleased with cumulative price gains of over 9,000 percent despite the financial crisis and the COVID-19 crash. After the rapid rise in the share price in recent months, however, the stock is trading close to its all-time high. The fundamental valuation has also risen into the infinite. Nevertheless, there are good reasons for this rally because the company and its products will significantly influence our everyday lives. In this analysis, I will show you whether the price gains are sustainable or whether the price of Nvidia shares has moved too far away from its fair value.

How Nvidia generates money

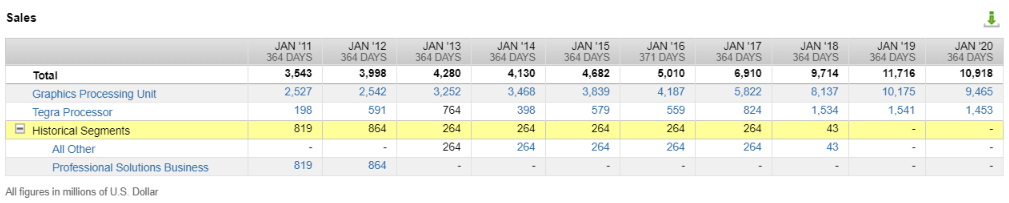

Nvidia breaks its business down into the two segments “GPU” and “Tegra Processor”. Both segments are based on Nvidia’s graphics processors (GPU=Graphics Processing Unit). For a long time, the company mainly developed graphics cards for the gaming sector. However, this has changed massively, which is one reason for the substantial price gains of Nvidia. With its two segments, the company now addresses important future markets that promise high growth for the coming years and decades.

The “GPU” segment

In the GPU segment, Nvidia offers graphics card processors for special application areas and individual target groups. The most important product field for a long time was the development of GeForce graphics cards for gamers. In the meantime, the portfolio also addresses other target groups, such as designers (Quadro) and cloud-based visual computing users (GRID). The latter area, in particular, is exciting because visual computing will open up enormous possibilities in the future and will create entirely new markets, such as virtual reality and augmented reality.

Virtual reality and augmented reality can be used to represent artificial realities or to embed virtual elements into existing reality. The areas of application for such solutions in industry (construction & assembly), e-commerce (preview of glasses, furniture, clothing), and games (Pokemon Go) are enormously diverse. In addition, large data centers require more and more computing power to master IT disciplines such as artificial intelligence or Big Data. The computing power of the Nvidia GPUs is also needed here.

The “Tegra Processor” segment

In the second business unit, Nvidia offers its Tegra processors. These are so-called System-on-a-Chip (SoCs) solutions. An SoC is a fully functional computer that is implemented on a single chip. The Tegra Processor unit is comparable to Qualcomm’s QTC segment products, which I have also analyzed. Similar to Qualcomm, Nvidia offers solutions for future mega markets with its processors. Worth mentioning here are autonomous driving and artificial intelligence (AI). Such chips are not only used in cars but also in drones, for example. You can also find Nvidia’s Tegra processors in the popular mobile game console Nintendo Switch from the Japanese company Nintendo.

Future prospects

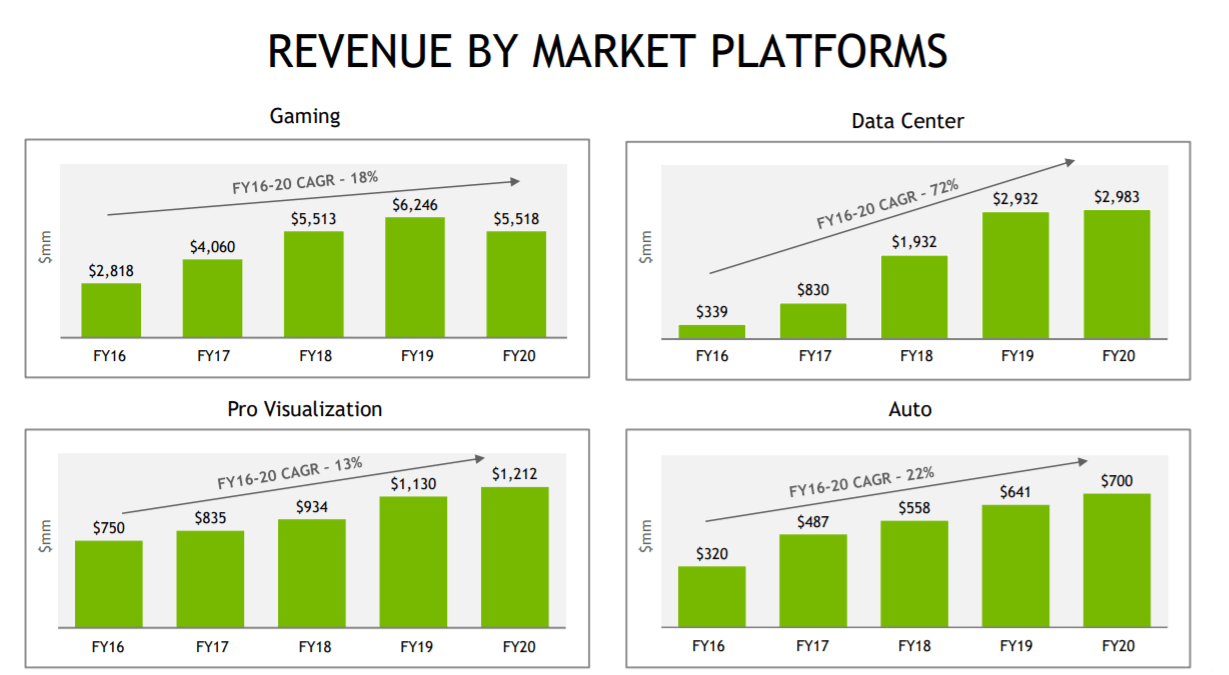

Nvidia is a significant player in strong growth markets with its graphics processors. Especially in the “data center” sector, Nvidia has grown by an annual average of 72 percent since 2016 and was able to increase its turnover from $339 million to almost $3 billion.

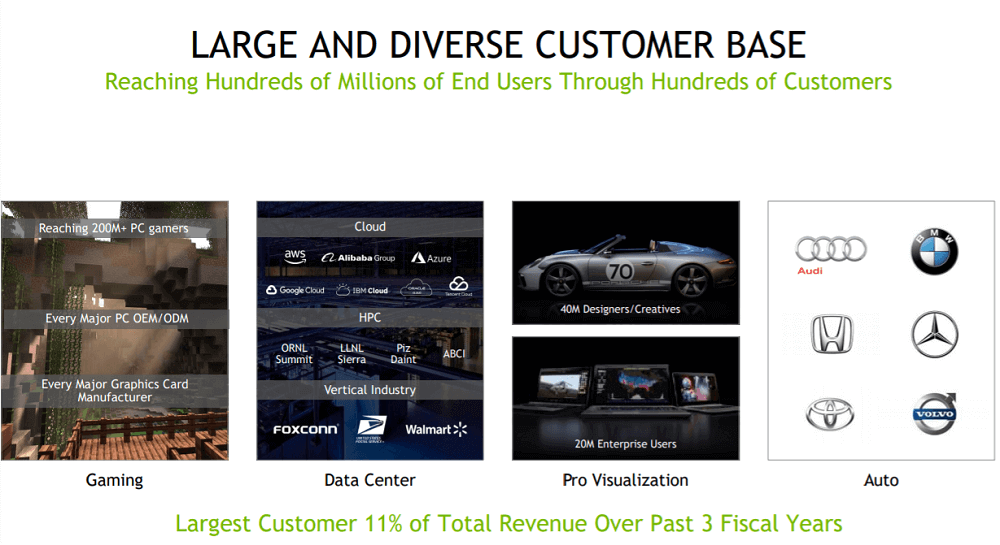

As you can see, the company and its GPU solutions have become an integral part of many areas of our daily lives. The company’s customer group is correspondingly large. With Amazon, Microsoft, Google, Alibaba, and IBM, all major players in the rapidly growing cloud-computing segment use products from Nvidia.

Nvidia has a clear advantage over companies like Intel. When the company started to develop one of the first 3D GPUs in 1993, no one could have imagined the paramount importance of GPUs thirty years later. In the meantime, it is becoming increasingly clear that GPUs’ technical architecture is significantly superior to the architecture of pure CPUs (Central Processing Unit) as offered by Intel. This is particularly true in the field of high-performance computing (HPC). I assume that GPU solutions will increasingly dominate this area. According to Nvidia, each GPU-based server replaces several CPU servers. In the future, such high-performance computers will have far-reaching fields of use, ranging from complex weather simulations to the secure and energy-saving storage and processing of data in network and data centers.

Nvidia’s success is always threatened by strong competition

The growth prospects in the individual future markets naturally attract competitors. Nvidia sees itself exposed to intense competition on several fronts at once. In the field of graphics chips and GPU-based system-on-a-chip solutions, Nvidia and Advanced Micro Devices (AMD) have been competing for decades to develop the most powerful products. In the field of autonomous driving, Intel, in particular, is a serious competitor after taking over the Israeli company Mobileye for over $15 billion in 2017.

Nevertheless, it is expected that Nvidia will continue to profit from technical progress in the future and even play a significant role in shaping it with its products. But you must be aware that the company is not a monopolist with a strong moat in any of the markets mentioned. Instead, there is a constant innovation pressure, and supposedly safe market shares can crumble with the next product cycle. For example, AMD will supply the graphics chips for both Sony’s new PlayStation 5 and Microsoft’s new Xbox.

Is Nvidia growing profitably?

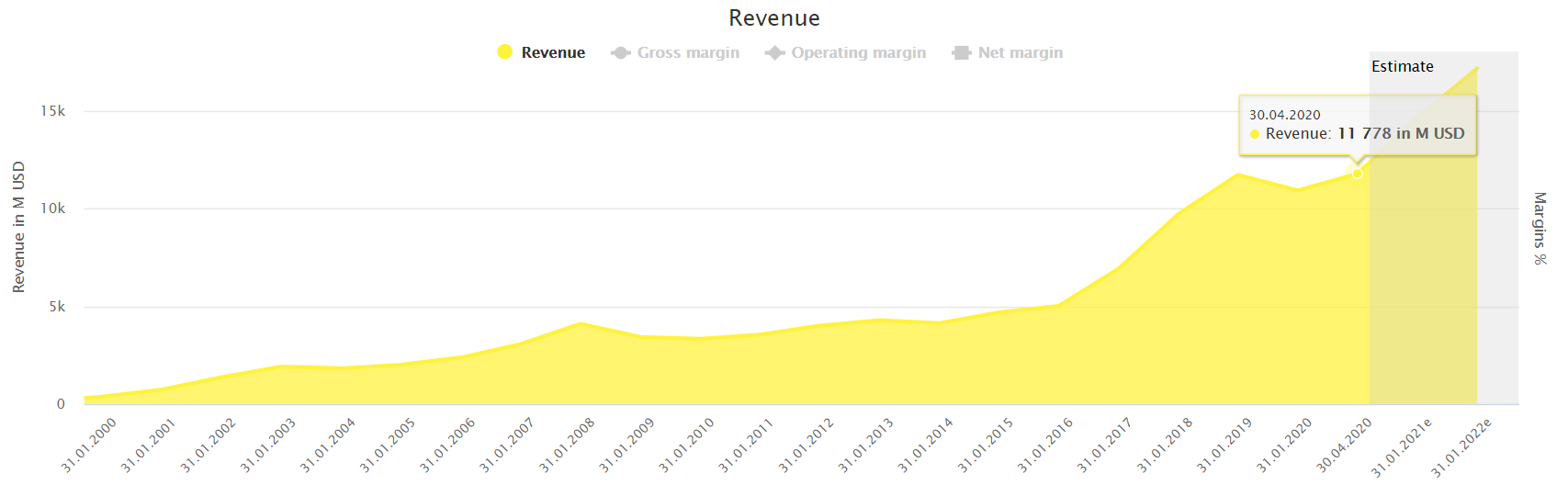

Over a more extended period, Nvidia has grown strongly. Within ten years, the company has increased its revenue from $3.3 billion in 2010 to over $11 billion in 2020. Recently, however, revenue has declined in both segments. The GPU segment decreased by 7 percent in January 2020, while the Tegra segment generated 6 percent less revenue. This was mainly due to declining sales of graphics cards for games and game consoles.

Earnings in the last financial year also recorded a drop for the first time since 2016. However, the cash flow development is excellent. Both operating and free cash flow have almost quadrupled since 2016. After deducting all operating costs, the company has a correspondingly large amount of cash on its hand. With this cash, it can pay dividends or finance share buybacks and further growth.

In its forecast, Nvidia assumes that growth will probably slow down somewhat in 2020. Margins and operating profit, in particular, are expected to decline in 2020. The coronavirus is also likely to have adverse effects on the company. It is not unlikely that customers postpone orders or the purchase of new computers with Nvidia graphics cards if economic conditions continue to deteriorate, and high unemployment rates persist. Nevertheless, growth should pick up again in the long term. Nvidia has strengthened its position as well, especially with two acquisitions in the rapidly growing data center sector by taking over Mellanox and Cumulus Networks. With them, Nvidia wants to build an entirely new business unit for its data center and network business.

You may need some patience for a high dividend yield

With a current dividend yield of 0.18 percent, Nvidia is relatively uninteresting for dividend investors. However, the company is still a young dividend payer and has only started to distribute parts of its profits to shareholders in 2013. Although Nvidia has increased its payouts every year, the rate of increase has slowed down recently. While Nvidia increased its dividend by 13.5 percent on average over the past five years, the dividend increase last year was only 4.9 percent.

Nevertheless, it is worth taking a look at the personal dividend yield (yield on cost). The personal dividend yield calculates the dividend yield based on the entry price instead of the current price. Whoever bought Nvidia shares in 2013 and, therefore, at a time when Nvidia was already one of the largest graphics card manufacturers in the world, can now look forward to an annual dividend yield of 5 percent on the invested capital. With the recent rather small increases in dividends, it could be challenging to achieve a similarly high yield on cost in the foreseeable future.

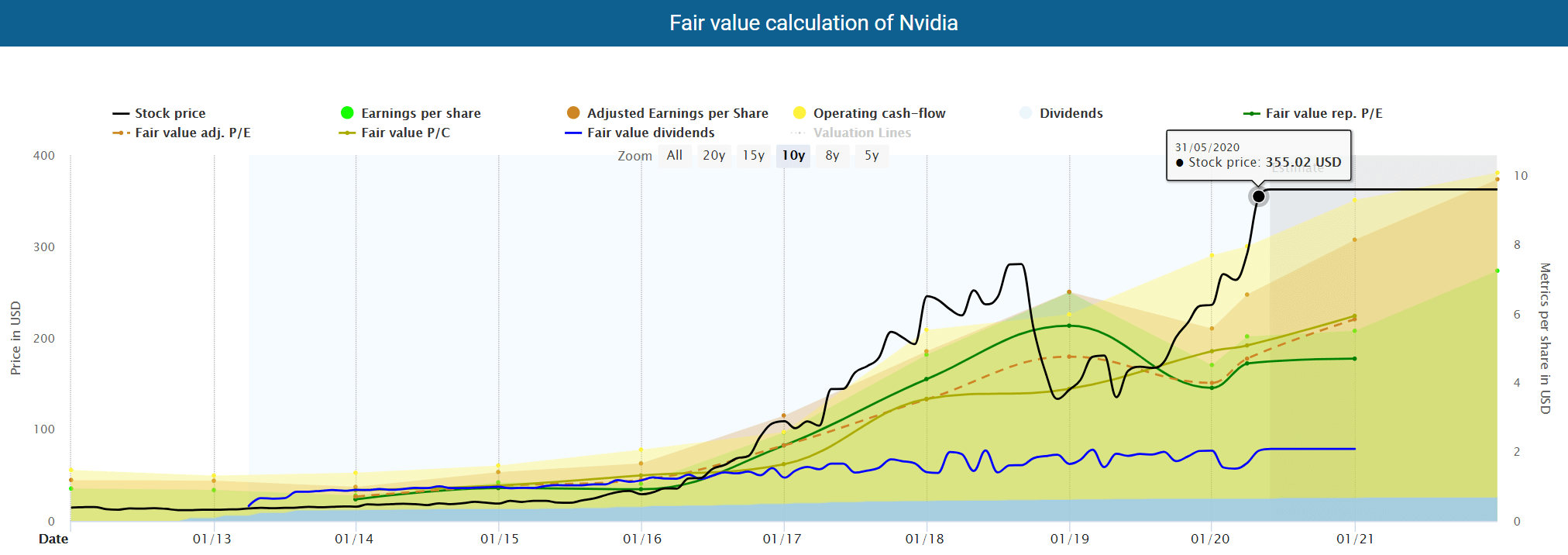

Is the Nvidia stock cheap?

One reason for the weak dividend outlook is the enormous share price gains. According to the fair value calculation of DividendStocks.Cash, which even considers the adjusted profit, the price of the Nvidia stock has completely separated itself from its historical valuation. With an adjusted P/E ratio of over 30 and a price/cash flow ratio of almost 24, most multiples indicate that the Nvidia stock is strongly overvalued.

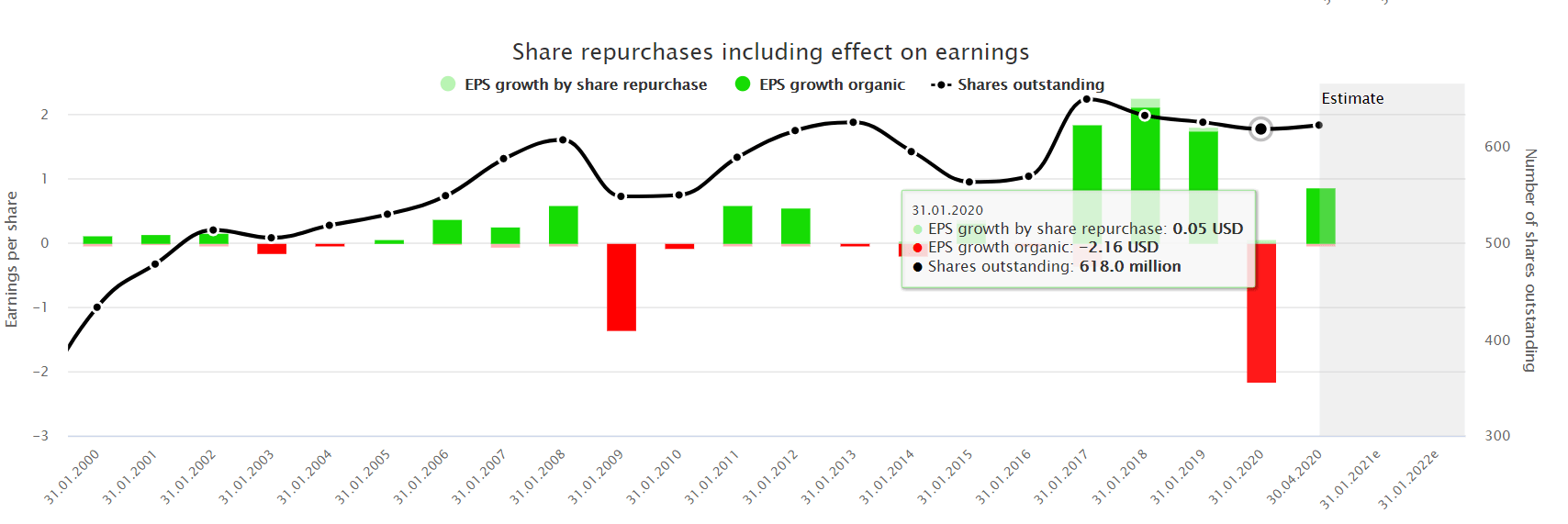

You should also know that the issue of new shares has diluted earnings per share in the past. As you can see, the number of outstanding shares has increased by over 20 percent since 2003. Since 1996, the number of shares outstanding has even more than quadrupled. If you look at the share price development in parallel, you can see that the company has been less happy with the timing of its share buybacks. For example, in 2016 and 2017, Nvidia issued new shares when prices rose, only to repurchase them a short time later at even higher prices.

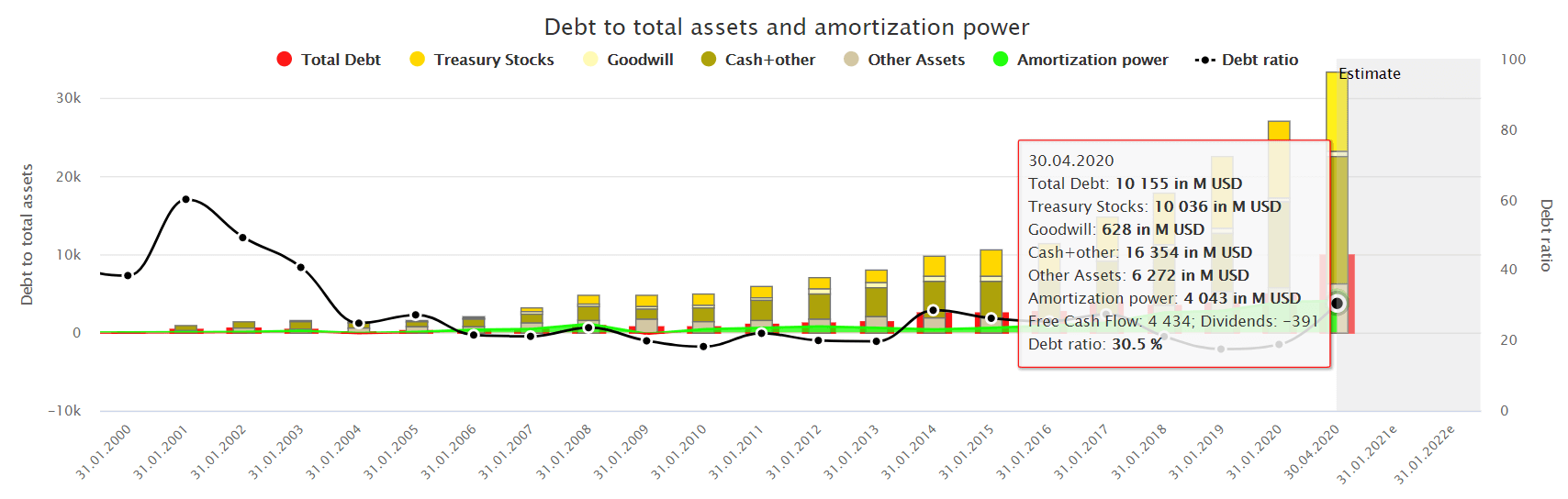

What speaks for the Nvidia stock, after all, is the solid balance sheet of the company. Thus, Nvidia could – at least arithmetically – settle almost all of its debts of nearly $10 billion with its treasury stock. Amortization power is also impressive. The company has a free cash flow of around $4 billion after deducting dividends. Accordingly, Nvidia would need 2.5 years to pay all its debts with free cash flow and would still have $10 billion worth of shares in its treasury.

Conclusion: Nvidia stock – Looks like Mr. Market is an enthusiast

Enthusiasts pay almost any price. And similar to hardcore gamers, Mr. Market seems to be a passionate fan of Nvidia. There is no doubt that the Nvidia stock is an exciting investment. It has brought its shareholders a lot of joy. Despite the corona crisis, the strong balance sheet and excellent prospects have continued to push the share price higher. With a share price near its all-time high, the question arises as to how much of future growth the market has already priced in. The adjusted P/E ratio of over 30 indicates that Mr. Market has already priced in a great deal of future potential.

That said, there have been repeated setbacks in the past in which shareholders were able to buy shares at a lower price. With weak sales development in 2020, Nvidia also shows that future growth is not a foregone conclusion. Mr. Market should be cautious. I recommend him to buy Nvidia shares at the current price only in smaller tranches and over a more extended time frame.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.