Hello and welcome to my fundamental Microsoft stock analysis. As you may know, many investors had already turned away from Microsoft stocks at the turn of the millennium. And indeed, with the burst of the dotcom bubble, it took almost ten years for the share price to find the bottom of a year-long downward and sideways trend. Since then, however, the company has once again become an investor darling. If you have remained loyal to the company over the years, you can enjoy impressive price gains and dividends. For example, the Microsoft share price has increased by double digits almost every year since 2011. In recent years, the share price has risen even by over 30 percent per year. This year, the share performs extremely well despite COVID-19 as well.

Given this development, however, many investors worry that this growth will eventually come to an end. Non-invested investors, on the other hand, have been standing on the sidelines for years, waiting for a price setback to allow them to find a cheap entry. In this analysis, we want to address whether the price gains are sustainable, whether further growth is possible, and whether it is still worthwhile to buy Microsoft shares at the current level.

As always, I would appreciate it if you could give me short feedback in the comments below or share this post if you liked it or had the opportunity to pick up some valuable thoughts.

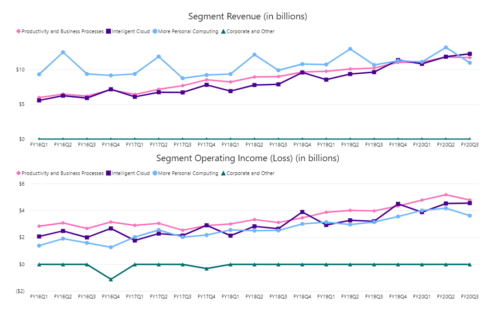

Microsoft’s three growth segments

Let’s first take a look at what Microsoft does for a living. Because by now the company is much more than just Windows and Office. Microsoft has divided its business into three segments: “Productivity and Business Processes”, “Intelligent Cloud” and “More Personal Computing”.

“Productivity and Business” segment

The “Productivity and Business” segment primarily includes the classic business with the popular Office products, Skype, and Microsoft’s social network LinkedIn as well as the associated offerings Talent Solutions and Marketing. The “Dynamics” product line introduced in 2016 is worth mentioning here too. This product line includes several software applications and services that provide businesses with various ways to analyze and manage their data, resources, and customer relationships.

The “Productivity and Business Processes” segment was and still is an essential component of Microsoft’s success. With the introduction of subscription-based licensing of office services in 2011, the company not only massively increased sales but also improved profits. Instead of buying the product only once, customers are now “allowed” to purchase a new license for the same product every year.

„Intelligent Cloud“ segment

The second segment, “Intelligent Cloud”, continues the success of the first segment. Here Microsoft offers its customers a wide range of cloud-based services, all of which address the extremely fast-growing cloud computing market. Microsoft’s market share in terms of revenue in the cloud sector is impressive at 18 percent. Only Amazon, with 33 percent, can be happy about an even bigger piece of the cake. On the other hand, Microsoft’s lead over Google in third place is quite comfortable at ten percentage points and underlines Microsoft’s important role in this market.

–> Click Here For The Best Winner Stocks For Cloud Computing With Or Without Dividends <—

“More Personal Computing“ segment

The third business segment is the “More Personal Computing” division. Microsoft bundles both hardware and software here. In addition to the Windows operating system, the segment includes the surface tablet and the Xbox game console with all associated products and services such as games, additional subscriptions, advertising, and accessories. For 2020, the highlight in this segment will be the new Xbox Series X console, which marks the beginning of the new console generation and which Microsoft will probably release in time for the 2020 Christmas business. The new Xbox could bring a little more momentum back into the segment, as revenues and operating income have recently declined somewhat here.

Better margins give hope

Although revenue growth has never been a problem for Microsoft, investors had turned their backs on the company, primarily due to the many years of declining margins. It has taken a long time, but it seems that Microsoft has found a sustainable way to improve profitability. The trend is pointing upwards. Microsoft now achieves an operating margin of 37.4 percent. Furthermore, the net margin has even doubled since 2018 and is currently over 30 percent. Besides, the increase in the gross margin is a sign that even if sales stagnate, the company has more profit left over with which to invest in further growth or reward shareholders with higher dividends or share buybacks.

Is Microsoft’s dividend safe?

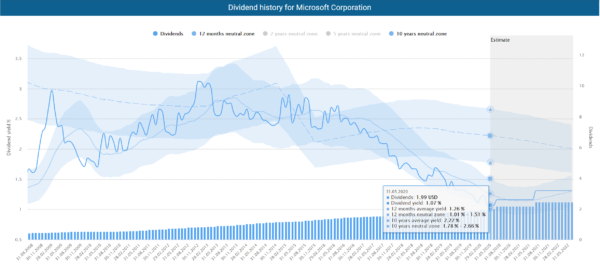

The Microsoft share has now become a favorite of many dividend investors. Not without any reason: with average dividend growth of 13 percent in the last ten years, 10.45 percent in the previous 5 years, and a remarkable 9.8 percent last year, you can benefit enormously from the compound interest effect. Nevertheless, Microsoft does not belong to the illustrious circle of dividend aristocrats. A company is only considered a true aristocrat when it has increased its dividend every year for 25 years without interruption. Microsoft is still a long way from that, as the company has only managed to increase its dividend for 16 consecutive years.

The strong share price performance had rather negative effects on the dividend yield. The current yield of just 1.09 percent is not far from its historic low. However, as you can see with our Dividend Turbo tool, Microsoft was never a so-called “high yielder”. The average yield within a 10-year corridor is also a rather modest 2.2 percent.

You should also note that these figures indicate the initial return, i.e., the return that investors achieved when they bought the property. But if you look at the yield on cost, i.e., the return that investors achieve with their initial investment, a different picture emerges. For investors who invested in Microsoft ten years ago, the current yield, based on the initial investment, is over 7 percent. You can see from this that in the long run, it is not the initial return that is important, but the dividend increase.

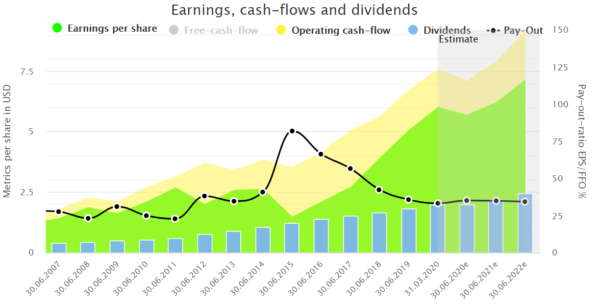

In recent years, Microsoft has been able to increase its payouts every year by a constant double-digit or high single-digit percentage. Whether Microsoft will maintain this rate in the coming years is difficult to estimate, given the COVID-19-related uncertainties. An important key figure is the payout ratio. This figure shows you how much of a company’s profit or free cash flow a company has to provide in order to pay a dividend to its shareholders.

The lower the payout ratio, the more financial leeway the company has to increase its dividend in the future while also investing in further growth. Usually, a ratio below 50 percent is a sign that a company will continue to increase its dividend in the future regularly. Microsoft meets this requirement. With a current payout ratio of approximately 35 percent, the management has sufficient leeway for further increases. Another good sign is that the ratio has fallen in recent years. Even with a constant profit, Microsoft could increase the dividend by 20 percent and would still be far below a payout ratio of 50 percent.

Is Microsoft overvalued?

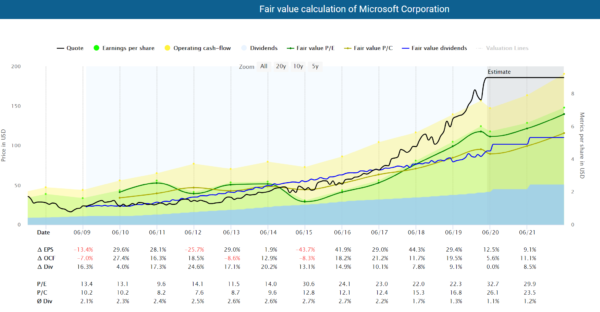

Although the high share price gains were accompanied by strong growth in sales and profits, Microsoft’s fundamental valuation has nevertheless increasingly distanced itself from the development of the operating business in recent years. As you can see in the dynamic share valuation below, the share price reached its fair valuation in mid-2014. Since then, the share price has been rushing further and further away from its historical valuation. This is the case in relation to both profit and cash flow development. Even the COVID-19-related volatilities on the global stock markets could not have a lasting effect on the development of the share price. Although according to forecasts, Microsoft will also suffer losses in profit and cash flow, the share price continues to rise.

You may now be wondering whether the share price has now run into a bubble. And indeed, other key multiples such as the very high price/book value ratio of over 12 and a price/free cash flow ratio of over 32 indicate an overvaluation.

However, you have to bear in mind that such high multiples are no guarantee for falling prices in the future. The share price has been rising for years despite an alleged overvaluation. It cannot be ruled out that it will continue in the same way in the future. For example, price stability compared to broader indices such as the S&P 500 or Dow Jones is a sign that the market believes the company is capable of further growth and might even see Microsoft as a defensive investment for uncertain times. So far, the effects of the Corona crisis have indeed been limited for Microsoft. The company has even seen increased demand for its products in its “Intelligent Cloud” and “Personal Computing” segments. This shows that Microsoft’s services and products are now essential to the everyday lives of many people, which certainly justifies a certain valuation premium.

Conclusion: With Microsoft stocks on cloud seven

The Microsoft stock is proof that a long-term investment approach and patience are elementary conditions for success on the stock market. Those who lost their trust in the company too early can now look back on almost ten years of missed returns. Investors who have remained loyal to the company are conversely happy to see substantial price gains and high personal dividend yield. One man’s joy is another man’s sorrow. Many shareholders stand on the sidelines and have been waiting in vain for years for the right moment to enter the company. But even in times of COVID-19, the share price hardly drops. Stable operational growth, strong positioning in future markets, and increasing profitability support the share price and may drive it further.

If you would like to invest in Microsoft but are deterred by the historically high valuation, the cost-average effect could be a viable solution. By buying shares at regular intervals over a longer period, you don’t have to worry about market timing and can profit from long-term price and dividend increases. This procedure can be very easily implemented with a savings plan.

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.