The Church & Dwight stock has been an excellent investment in recent years. Unfortunately, the almost constant rise in stock prices meant that investors rarely had the opportunity to buy at a reasonable price. Nevertheless, investors who bet on Church & Dwight’s quality and bought the stock have been rewarded with an average annual return of over 15 percent over the past 20 years. Including dividends, the total return in USD amounts to almost 2,000 percent.

However, the stock has recently lost momentum and is trading around 15 percent below the all-time high of about USD 96. Accordingly, many investors are asking themselves whether the Church & Dwight stock is a bargain now. In this analysis, we take a look at what the recent price losses are all about and whether you are currently catching a good entry point to profit from long-term rising dividends and profits with Church & Dwight.

The business model: How Church & Dwight generates money

Church & Dwight is a manufacturer of household and personal care products founded in 1846. While in the early decades baking powder was sent by mail, today a wide range of products is sold, and the company has reached a market capitalization of almost USD 17 billion. Church & Dwight divides its business into the three segments “Consumer Domestic”, “Consumer International” and “Consumer International”, whereby the segments are sometimes broken down into further sub-segments, and you can find individual brands in several segments at the same time.

The „Consumer Domestic“ segment

The “Consumer Domestic” segment comprises household and personal care products sold in the U.S. domestic market and accounts for 42 percent of total sales. Within this segment, household products are responsible for 54 percent, and personal care products for 46 percent of segment sales.

Church & Dwight still owes a large part of its sales to the versatile applications of baking powder. You’ll find it, for example, in neutralizing odors (as so-called deodorizers) in refrigerators and freezers, as a cleaner for kitchen and cooking appliances, as a bath additive, a dentifrice, a deodorizer in animal husbandry (keyword cat litter), and as a pH stabilizer for swimming pools.

Particularly well known is the ARM & HAMMER brand with its catchy logo, under which Church & Dwight markets numerous baking powder-based products. The segment’s product range also includes the brands Spinbrush (toothbrushes), Waterpik and Orajel (mouthwash and oral care products), Xtra (laundry detergents), bathroom cleaners (OxiClean), First Response (pregnancy and ovulation tests), the depilatory brands Nair, Flawless, Finishing Touch, Trojan (condoms), and Vitafusion and Zicam (nutritional supplements).

The “Consumer International” segment

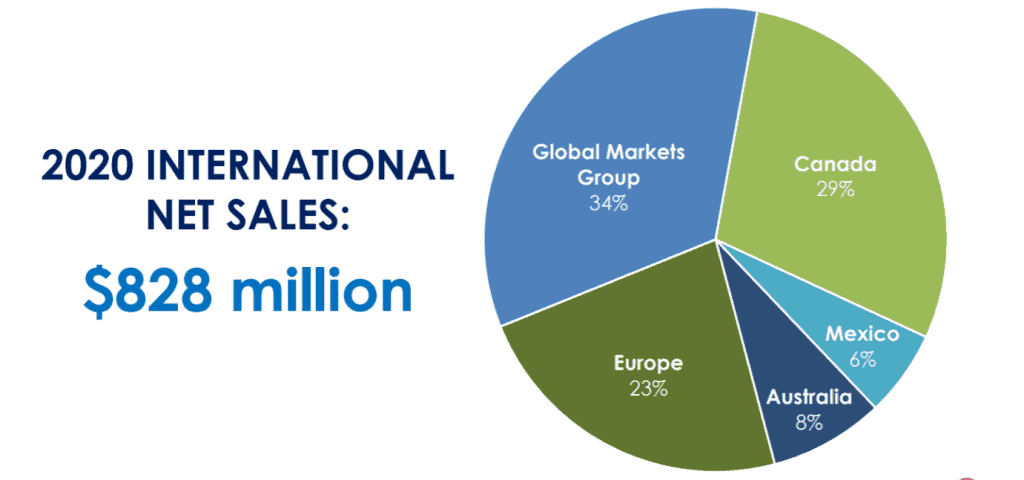

The “Consumer International” segment bundles Church & Dwight’s international business, which most recently accounted for 17 percent of total sales. With 6 percent growth in 2020, it made a disproportionately high contribution to the organic growth of 3 percent. In total, Church & Dwight supplies its products to 130 countries. The largest market apart from the USA is Canada, with a 29 percent share of sales, followed by Europe (23 percent), Australia (8 percent), and Mexico (7 percent).

The “Specialty Products” segment

The “Specialty Products” segment is relatively small. It accounts for 6 percent of sales. It is also divided into further sub-segments. Those are “Animal and Food Production Products”, “Specialty Chemicals” and “Specialty Cleaners”.

In the “Animal and Food Production Products” business unit, Church & Dwight markets a broad product portfolio of nutritional supplements, prebiotics, and probiotics for livestock, which are used in particular milk production.

The “Specialty Chemicals” division comprises the production of potassium carbonate. Church & Dwight’s customers use it to manufacture products such as acid protection agents in the pharmaceutical sector or so-called carbon dioxide release agents in fire extinguishers. The “Specialty Cleaners” segment comprises cleaning products used for industrial or commercial applications, for example, in hotels, restaurants, or other facilities such as office buildings.

The strengths of Church & Dwight’s business model

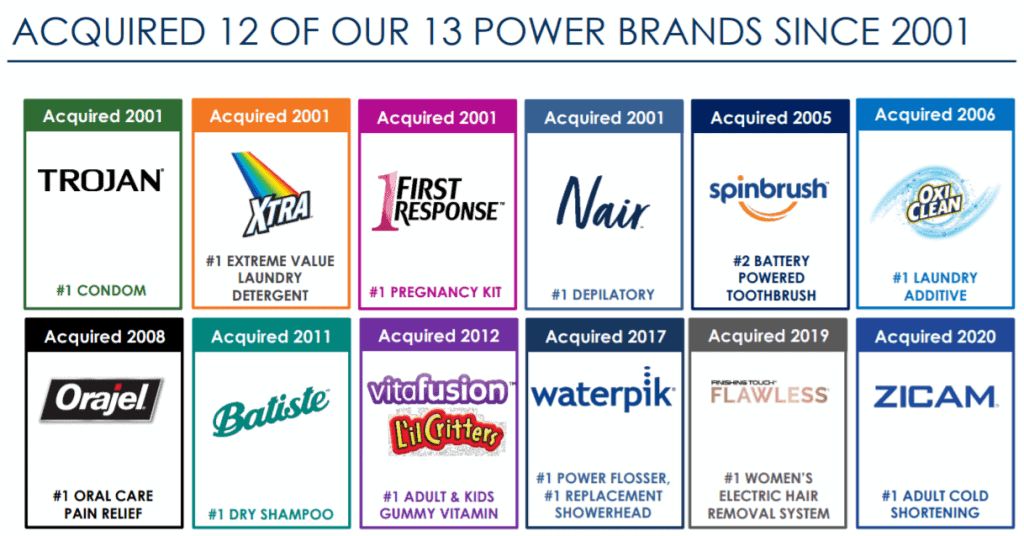

One reason for Church & Dwight’s success is its broad product portfolio, which includes everyday goods that enjoy constant demand and benefit from many applications. The company’s primary focus is on its so-called “13 Power Brands,” which together account for 80 percent of sales and profits.

Even though Church & Dwight’s products are not as well known in Europe as they are in the USA, the brands have considerable appeal, ensuring high customer loyalty and stable sales. In terms of market share, Church & Dwight is the market leader with its “Power Brands” in several product categories on its home market.

I see the flexibility of consumer goods companies to buy growth through acquisitions and integrations of other brands at any time if they have a strong balance sheet as a sector-specific strength. For example, they can replace low-growth brands with high-growth brands to respond to changing consumer needs. At Church & Dwight, this approach has worked remarkably well in recent decades, with 12 of the 13 power brands resulting from acquisitions.

Investor presentation

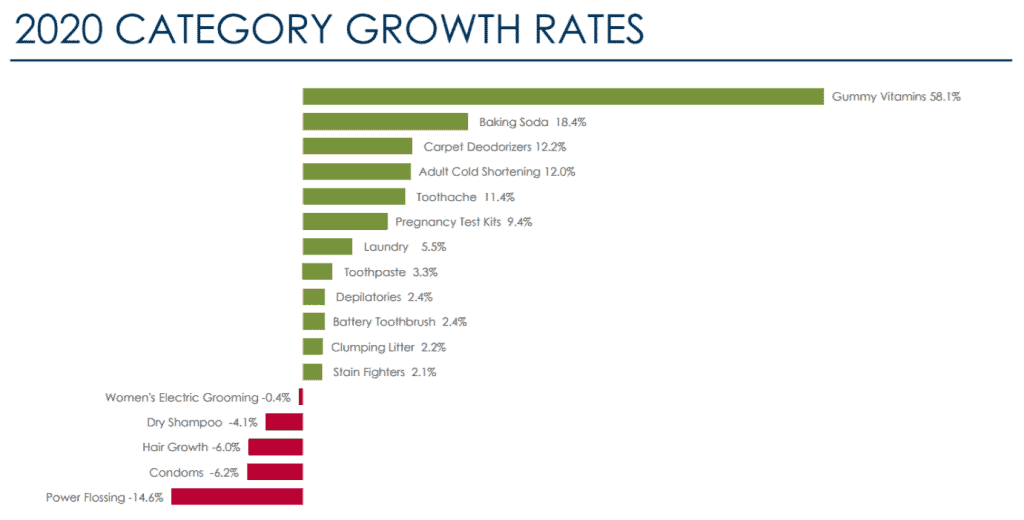

Church & Dwight’s business model is accordingly not only diversified but also crisis-proof. Some business units and product categories have even benefited from the COVID 19 crisis. Vitamin products and detergents, in particular, posted substantial gains, offsetting losses in other product categories. For defensive-oriented investors, this balance should be a particular plus.

Likewise, compared with other consumer goods manufacturers such as Procter & Gamble, shareholders of Church & Dwight have less reason to worry about so-called “private label” manufacturers. Church & Dwight competes with manufacturers of such private labels in only five of 17 product categories.

Church & Dwight’s revenue development: perfection on the verge of boredom

Church & Dwight’s growth is impressive, as over the past two decades, the company has been able to increase its sales from USD 795 million in 2000 to USD 4.9 billion in 2020. Remarkably, the financial crisis and 2020 have not left any significant dents in the flawless growth line running from bottom left to top right. It is likely that growth will continue in the coming years. Analysts expect Church & Dwight to achieve sales of USD 5.7 billion in 2024.

How does Church & Dwight plan to grow in the future?

Weaknesses often accompany the strengths of consumer goods companies like Church & Dwight. While shareholders benefit on the one hand from the crisis-proof business model with stable demand, the growth potential in already developed markets is severely limited. Sales of household or personal care products may be steady, but they generally grow only weakly. Also, the risk of migration to equivalent competing products limits the pricing scope.

International and e-commerce as growth catalysts

For further growth, Church & Dwight must expand accordingly. It has room to maneuver, particularly concerning the international markets, where disproportionate growth can be expected in the event of weak market penetration. Further potential is offered by the e-commerce sector, in which Church & Dwight was able to make substantial gains, especially in the Corona year 2020. For example, the share of e-commerce in total sales rose to 13 percent. Compared to 2015 with 1 percent, this is an impressive increase and offers the opportunity to take market share from less online-savvy competitors.

Great balance sheet

Finally, management has the option of buying growth through acquisitions of, particularly successful or profitable brands. Church & Dwight has the financial means to do this. For example, measured against the interest-bearing debt of USD 2.3 billion, the debt ratio is relatively low at 24 percent. Besides, Church & Dwight holds shares worth more than USD 2 billion, which it could use for an acquisition at any time.

How profitable is Church & Dwight?

As with sales growth, there is no reason to complain about profitability. Church & Dwight shines with consistent earnings and cash flow growth. Although reported earnings per share are expected to decline slightly from USD 3.12 to USD 3.05 in 2021 after a 15 percent increase in 2020, on an adjusted basis, management expects respectable growth of between 6-8 percent. By 2024, analysts even expect reported earnings to rise to USD 3.70.

Part of the profit increases is due to a increased profitability. With a stable gross margin, Church & Dwight has been able to increase its operating margin and net margin strongly over the last ten years, from 17.38 and 10.46 percent respectively in 2010 to 19.17 and 16.05 percent last year. In the coming years, analysts expect the operating margin to rise to over 21 percent.

Is Church & Dwight’s dividend safe?

Church & Dwight pays out dividends quarterly and has increased them over the past 21 years, in some cases at a respectable rate. For example, the quarterly dividend rose from USD 0.04 in 2000 to USD 0.2525 now. After the latest increase from 0.24 to 0.2525 USD, shareholders receive 1.01 USD per share per year. This amount corresponds to a dividend yield of 1.2 percent at the current share price of around 81 USD. Over the past ten years, Church & Dwight has raised its dividend by a respectable 16.8 percent annual average. If we look only at the last five years, the average yearly growth was still 7.4 percent. However, the previous increase in February 2020 was 5 percent, which is below the multi-year average.

Payout ratio supports further increases

Given the relatively low dividend yield, substantial increases would be welcome. Fortunately, with a payout ratio of 33 percent on earnings and 26 percent measured by free cash flow, there is sufficient scope for further dividend increases. Analysts expect the annual dividend to increase to USD 1.08 per share in 2021, which is an increase of almost 7 percent and in line with the past five years. Given the forecast earnings and cash flow development, I consider an increase of this amount to be realistic.

The dividend yield is only in the middle to lower third of the various long-term corridors

The dividend yield is only in the middle to lower third of the various long-term corridors of the last few years, despite a satisfactory dividend increase due to the share price gains in recent years. In this respect, I would like to see a little more courage for higher increases.

Is the Church & Dwight stock favorably valued?

The graph below shows what an almost perfect investment the Church & Dwight stock has been in the past. In parallel with its flawless operating performance, the stock price has advanced to new heights along with its fair valuation. Even if we set the fair value at an adjusted P/E of 22, corresponding to the historical average, the stock has been mostly overvalued since 2014. As has so often been the case in the past, the stock price is several years ahead of Church & Dwight’s operating results. Despite the recent setback, there is short-term downside potential of 7% at the current fair value.

Conclusion: Church & Dwight – Still expensive after setback

The Church & Dwight stock has been a solid investment over the past decades, and in retrospect, every minor setback close to the fair value turned out to be a buying opportunity. Currently, such an option seems to be looming again. However, investors must be aware that they are still paying a premium to the fair value when buying Church & Dwight stocks, despite the recent price declines.

Likewise, the dividend yield of 1 percent is only within the historical average. Many aspects could justify the premium. We have excellent management, constant growth, and further growth potential. Each shareholder must decide for himself whether this is sufficient for an investment. An alternative is a stock savings plan. This way, you already have a foot in the door with smaller investments. Furthermore, you can profit from dropped prices through additional purchases in the event of a further correction.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.