While tech stocks are breaking record after record, classic consumer goods and dividend stocks such as the Procter & Gamble stock seem more boring than ever. However, in recent years Procter & Gamble has impressively demonstrated how much yield power such a massive tanker can have once it comes to speed. The Procter & Gamble share price has risen by 95.8% since the interim low in April 2018! Over the year, shareholders have achieved a return of more than 30 percent per year when buying around the low. And even those who were unlucky enough to buy the stock at the interim high at the end of 2014 can still enjoy a double-digit annual return, including the dividend.

If you don’t want to miss any new articles or analysis, you can easily follow me on

or Twitter.

After the recent near doubling of the share price, shareholders are naturally asking themselves whether Procter & Gamble, as one of the oldest companies listed on the stock exchange, still has enough oil in its tank to continue providing such dream returns. In this analysis, we deep-dive and check if it´s still worth to buy Procter & Gamble or whether it is better to sidestep the stock.

The business model: How Procter & Gamble generates money

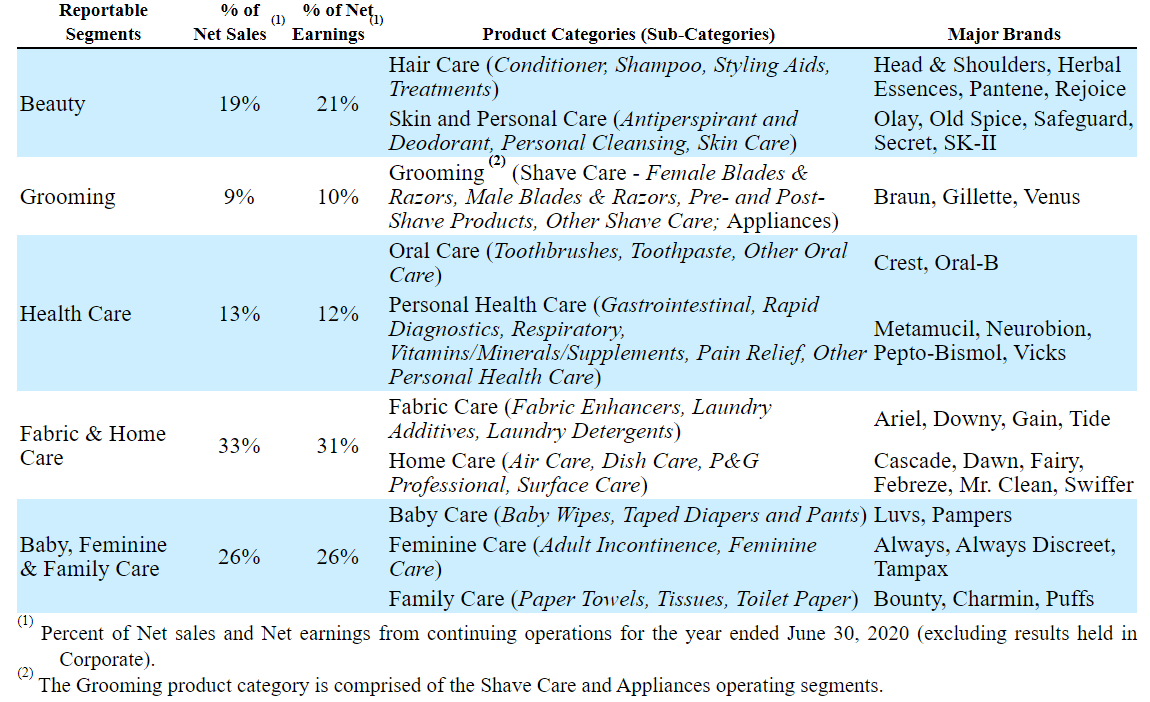

Founded in 1837, the company is a consumer goods giant. You’ve probably seen dozens of its products in the supermarket and even used them in your home. Procter & Gamble has divided the group into five segments, which mostly all cover everyday products. These products include toothpaste, home care products, personal care products, and toilet paper. These products enjoy a constant demand. Consumers buy such products even in economically challenging times. Accordingly, Procter & Gamble’s business model is crisis-proof, which is a great advantage, especially for risk-averse shareholders. As you can see in the chart below, the segments contribute relatively evenly to revenues and earnings, so Procter & Gamble is not heavily dependent on individual product groups.

Strong brands

Besides, the chart shows another reason for the company’s success. Procter & Gamble does not “just” sell everyday products but also has strong brands in its portfolio (e.g., Pampers, Head & Shoulders, Febreze, Ariel). In Procter & Gamble’s current portfolio, an impressive 23 brands generate annual sales of over USD 1 billion, and another 14 brands generate annual sales of at least USD 500 million.

These brands ensure high customer loyalty and recognition, which gives the company high market shares. For example, Procter & Gamble is the market leader in hair care products with a global market share of over 20 percent. It also secures the market leadership in blades and razors with a 60 percent market share and holds over 50 percent of the female epilator market. Procter & Gamble is also a leader in the oral care segment with a 20 percent share of the market, where it holds second place. To maintain this market power in the future, the company spends more than USD 4 billion on advertising annually in the USA alone. Worldwide it is almost USD 10 billion, making Procter & Gamble one of the companies with the highest marketing expenditures.

Procter & Gamble can sell weak brands and buy strong brands

Nevertheless, shareholders have been concerned in the past that the business success of the giant could suffer from the competitive pressure of smaller and more agile start-ups. Investors also feared a loss of market share from the private labels of large retail groups such as Walmart. However, Procter & Gamble’s portfolio is quite flexible. For example, it can sell faltering and only weakly growing brands such as the Pringles chip brand or entire business units and buy growth through acquisitions. So far, Procter & Gamble has been able to use this method to respond to changing consumer needs promptly. Likewise, brands that reach the magical sales threshold of more than USD 1 billion have more than doubled since 2000.

Procter & Gamble reports organic growth again

As you can see from Procter & Gamble’s long-term revenue development, the company has increased its revenues from USD 24 billion to USD 70 billion since 1990. Even if this development does not come close to that of growth engines like Amazon or Alphabet, it shows that even ancient companies can still grow despite their age.

A tough phase of consolidation

Only in the years from 2007 to 2016 did Procter & Gamble go through a more extended period of consolidation, which resulted in a significant decline in revenues, which was because Procter & Gamble concentrated on the particularly high-growth brands and reduced its brand portfolio by 90 to 100 brands. In this context, the company sold more than 43 brands to Coty for USD 12.5 billion.

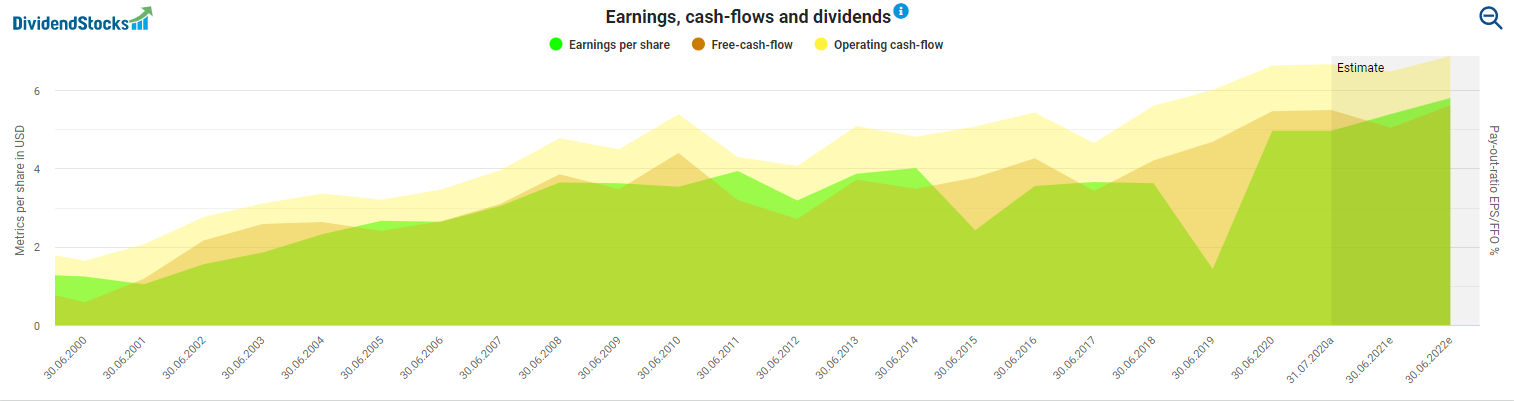

It is now clear that the consolidation was a complete success. In 2019, Procter & Gamble grew in 9 out of 10 product categories and in all regions where sales were made. Additionally, the company’s 2019 revenue growth of 6%, the highest organic growth rate since 2006, pulverized its growth forecast, which predicted only 3-4%. The development of profit and cash flow also shows you how sensible the focus on high-growth brands was. Despite the sales of many brands, profit and cash flow are at record levels.

The USD 8 billion Gillette gap

You should not let yourself be influenced by the slump in earnings in the last financial year. Procter & Gamble booked a write-down of USD 8 billion for the Gillette shaving brand, which had an extraordinary impact on the balance sheet. The write-down was due to lower shaving frequency and increased competition from new business models. In particular, Dollar Shave Club – now acquired by Unilever – is attacking the market leader with its attractive subscription model and was able to take a substantial share of the market. The Gillette brand’s write-down left Procter & Gamble the only notch in an otherwise extraordinarily stable margin development. While the net margin in 1990 was still 6.65 percent, it is currently over 18 percent. The gross margin also increased by 11 percentage points in the same period and now stands at an impressive 50 percent.

This puts the margins several percentage points above those of its major competitor Unilever. The British-Dutch company only achieves a net margin of 11 percent and is also well behind Procter & Gamble with a gross margin of 44 percent.

Is the Procter & Gamble dividend safe?

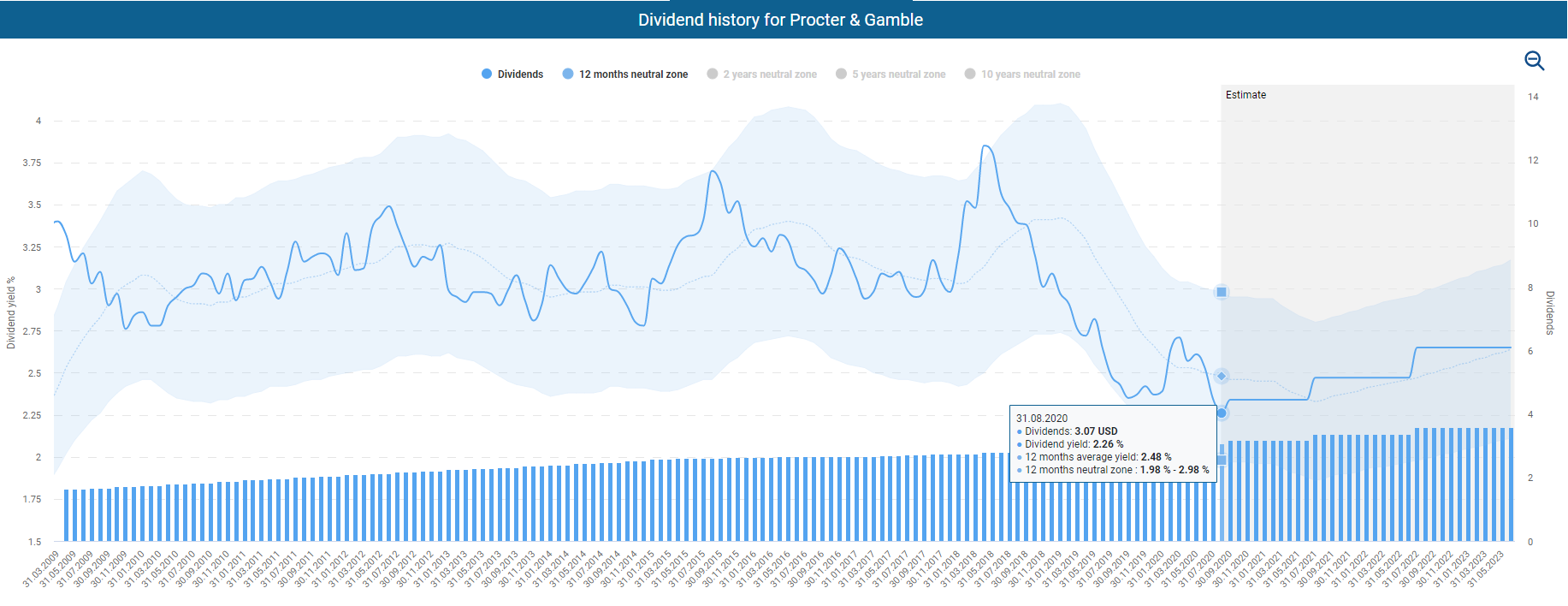

With a dividend rising for 64 years, the Procter & Gamble stock belongs to the illustrious circle of dividend aristocrats. Moreover, for many shareholders, the company is something like the mother of all dividend stocks. Last but not least, Procter & Gamble is one of the dividend payers who have even increased their hikes. While Procter & Gamble was content with an annual increase of around 3 percent in recent years, the company increased its annual payout by an impressive 6 percent in April in the midst of the corona crisis, thus sending out a clear signal of its strength.

Fans of high dividend yields will be disappointed at Procter & Gamble, however. As a result of recent share price increases, the current dividend yield of 2.2 percent is historically low. On the other hand, those shareholders who were courageous enough to buy with a dividend yield of almost 4 percent during the weakness of the share price in 2018 can be happy.

Although the dividend yield is historically low at the moment, the dividend including further increases seems to be secured, which is ensured not only by the excellent prospects for further growth but also by the healthy payout ratios concerning earnings and cash flow. Procter & Gamble is only distributing 60 percent of its earnings and 55 percent of its cash flow to shareholders, leaving sufficient room for further increases.

Is the Procter & Gamble stock fairly valued?

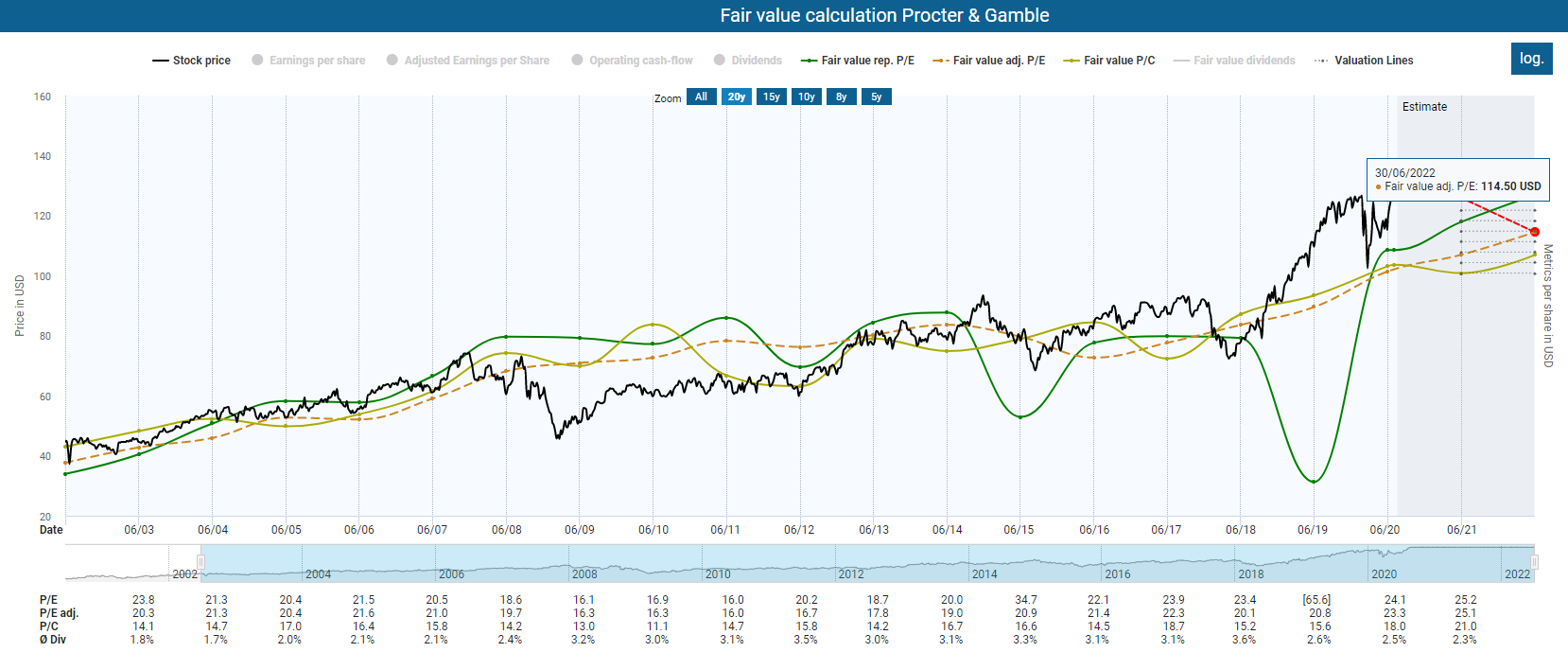

What the extreme price increases and the historically low dividend yield already indicate is confirmed by a look at the fair-value calculation: The Procter & Gamble stock is overvalued. From a value investing perspective, Procter & Gamble is currently not a buy. It is almost irrelevant what period we use to calculate the historical multiples. Based on the historical P/E ratio and price/cash flow ratio, there is downside potential of more than 10 percent compared to the current fair value. The adjusted P/E ratio of 25 also indicates a significant overvaluation of the Procter & Gamble share.

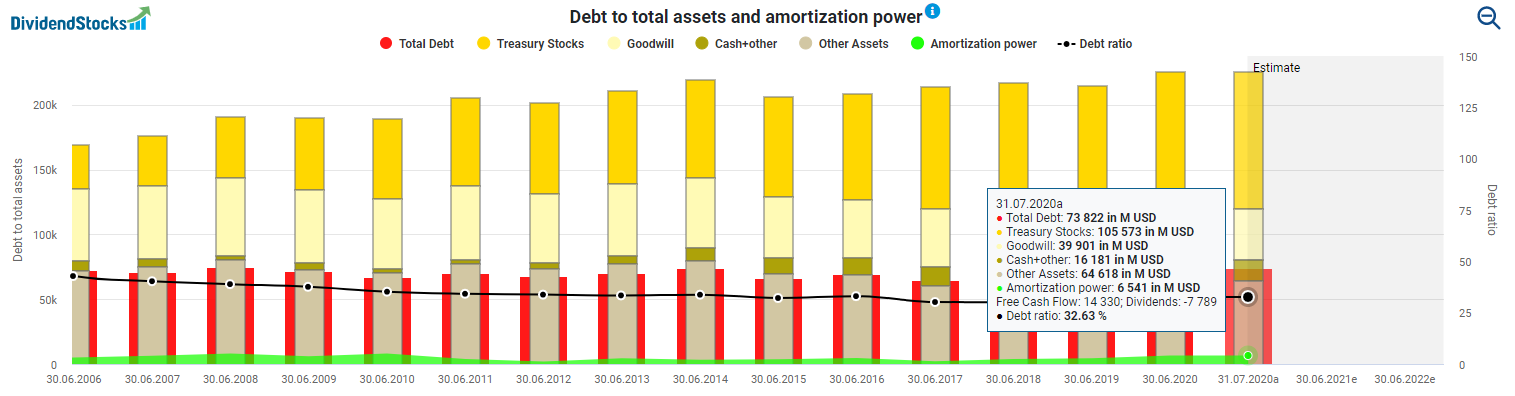

Although Colgate-Palmolive, with an adjusted P/E ratio of 26.7, also has a lofty valuation, its competitor Unilever, with an adjusted P/E ratio of 20 and a dividend yield of 3 percent, shows that there is another alternative. Conversely, a look at the balance sheet reveals a further strength of Procter & Gamble, particularly in comparison with Unilever. If you consider that Procter & Gamble recently went through a consolidation phase, a debt ratio of 32.63 percent is impressive. The share buybacks of approximately 2.46 percent per year have also meant that Procter & Gamble now has more than USD 100 billion worth of its shares.

Conclusion: Procter & Gamble stock – too expensive to buy

In retrospect, when investors kept their hands off the Procter & Gamble stock out of fear of stagnating sales and increasing competitive pressure, this was the best time to put the stock into their portfolio. Anyone who had the courage to buy the stock during a period of fundamental undervaluation can now enjoy high price gains and a relatively high dividend yield of over 3 percent. This is exactly the reason why I do not want to sell any of my shares. For everyone else, the train seems to have already left the station. In the meantime, the share has reached the highest valuation level in the last twenty years, which speaks against investing in my opinion, despite the recent strong organic growth. If you would like to invest in Procter & Gamble stock despite its high valuation, a stock savings plan is an option. In the event of a setback, you can profit from the falling share prices.

Did you like the article? Stay tuned for the following content… It is all entirely for free! Enjoy!

If you don’t want to miss any new articles, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.