Like everything that lies ahead, we cannot predict the development of share prices. Over the years, I had to accept many of those realities when investing in stocks. Now, I am thankful for the journey. Even if those realities are supposedly self-evident and logical, many investors ignore them, which can negatively affect their wealth accumulation. That is why I try to base my own investment decisions on these realities as much as possible. All in all, I have ten essential key points that I take for granted and follow.

I want to begin with a self-evident reality. Nevertheless, it is either not perceived or unconsciously ignored by many investors. These investors buy companies only because they are growing and have a promising future. That makes sense because we all want to be owners of companies that get bigger. Unfortunately, the growth aspect is only one pillar on which successful investing stands. Because while a company can grow and grow, that doesn’t necessarily go hand-in-hand with an increased share price. There are endless examples of this.

While I have talked about Microsoft’s share price performance from 2000 to 2015 many times, there are other companies that also had to go through such valleys or dry periods. Cisco is such a company. Did you know the share price still hasn’t reached the price of 2000? After almost a quarter of a century, it is still 35 percent away from this historic high (April 2021). And guess what? In that time, sales have far more than doubled. Profits have even increased sevenfold.

A second reality is that the stock price reflects the value of the underlying business. This is not necessarily obvious, as there is no supporting evidence. We also see with other asset classes that the value can be completely independent of, for example, the underlying substance.

Art is an excellent example. Art’s price is tied to its recipients’ acceptance and appreciation. But unlike works of art, stocks share the company’s fate, while art pieces, on the other hand, do not share the artists’ fate. When a company dies, the function of the shares dies. A work of art lives on after the death of the painter. Furthermore, shares are not unique. They are under the arbitrary control of the company and can even be doubled or tripled at will by issuing new shares.

Of course, we can still say for stocks that the share price reflects the sweet spot where supply and demand meet. But this approach would make stocks merely products of themselves, which they aren’t. Shares are more than that because they represent rights and obligations that are forever tied to the company and its productivity. They are not just a piece of paper or a position in a portfolio. Shares are the company. And the company’s (future) well-being is the stock price’s fuel. That is why the price of a share always reflects the value of the company.

This means that we must always keep an eye on the company’s value when considering buying shares. Put another way: We must always relate the price of a share to the company’s value. If we don’t do this, we will loosen the close bond between share and company. Breaking this very bond means we are bird-free and can interpret anything into a share price. This is where my betting slip analogy comes into play, which I have described elsewhere. Here, investors buy shares because they assume that the share price will continue to rise.

For me, who wants to become an owner of companies and therefore wants to get a substance for his money and not just a coupon that might increase in value, this consideration was new. In this respect, the perspective has changed. A share is no longer the proof of ownership of a company but a kind of betting slip with which one can bet that share prices will rise. With this change in perspective, the focus has shifted significantly from investing to speculating.

In the following paragraphs, we will look at the essential implications of accepting reality #2.

We have seen above that the price of a share and the company’s value are linked. Here, the company is the actual real and thus dominant part, while the share price only gives a diffuse picture of the company, like the shadows on the wall in Plato’s Allegory of the Cave.

These distortions cause the share price and the company’s value to not always be in balance with each other. We then speak, and this is nothing new, of undervaluation or overvaluation of a share. So, taking the described link between share and the company as our premise, we can conclude that the share price cannot rise infinitely further than the value of the company or the value of the underlying business. Remember, the underlying business is the share price’s fuel.

Therefore, any further increase in the share price reduces the upside potential of a specific stock if there is no corresponding growth in the company’s underlying business at the same time.

If we understand this third reality, reality #4 will not cause any further problems. Reality #4 is only the other side of reality #3. It’s simple: anything that flies higher than it has fuel will eventually come back down.

Let’s assume that the share price increases by 100 percent while the company’s value increases by only 20 percent. We know that the bond between the share and the company is flexible. This flexibility means that such discrepancies in development are possible. Remember, we do not live in a perfect world but in a cave and have to live with all kinds of errors and distortions. With every further lead of the share price, the risk increases that the share price will flip back to the original ratio (or even further). It’s like a rubber band that we stretch.

How far the market can stretch the rubber band before it snaps back is anyone’s guess. Many market participants put the stock price and its link to the company in relation to other asset classes and their performances. The problem here is that we loosen the crucial bond between share price and business. This naturally increases the risk of distortions and errors. We start to look for reasons and causalities, but we do not know whether they (i) are causal, and if so (ii) whether they will also be causal in the future.

Accordingly, we run the risk of lulling ourselves into a reality of which we do not know whether and how long it will last. Quite banally, we can ask ourselves: What does the underlying business of a profitable company care if government bonds become more expensive or interest rates are increasing? There may be explanations and bridges some analysts are crossing. But these bridges can become thin ice. We start to spin a tale around the loosening link between share price and underlying business. And we’re beginning to depend on the market believing that story.

With such a story, the uncertainties are increasing, the risks are growing, and we are becoming more uncertain in what we believe and think we know. We will see in reality #9 that there can only be one rational decision here. Paradoxically, however, many investors act entirely differently than one would expect given these circumstances. So more on that later.

Reality #5: every outperformance is reflected and offset by an underperformance

Sad reality #5 is that not all investors will outperform the broader market. An underperformance always matches an outperformance. Both then result in the average market return. So if we are not just investing in the broad market, we need to know the risk of underperforming. We have to be aware of that. And we have to ask ourselves whether we are willing and why we are eager to take this risk. Is it because we confidently assume we are smarter than the market?

Yes, you can try to fool the market, and indeed, there is always the opportunity to make money in the stock markets, even in times of crises and recessions. But is it likely that you will be one of those who outperform? The problem is that the risk of underperformance is somewhat leveraged because we don’t know how someone will underperform. Let’s suppose the stock market consists of only ten stocks. If nine stocks achieved a return of 10 percent and one stock only made a performance of – 10 percent, then the average return of each stock in a market-wide view would still be 8 percent. One doesn’t want to be the one investor picked/scores the – 10 percent, right?

Now, if you say this one investor is a down-on-his-luck newbie, look at the following example: We have ten stocks again. During a major crash followed by years of sideways movement, nine stocks achieved a performance of – 5 percent. Another stock, however, exploded due to given circumstances in the same period. This stock gained a return of 80 percent. Here, the average return of each stock in a market-wide view is 3,5 percent. This is still okay because we didn’t lose money (excluding inflation etc.). So nine out of ten have massively underperformed. Imagine if we had only invested in these losers.

This scenario is not unlikely because only a minority of stocks is responsible for most profits, which is what US finance professor Hendrik Bessembinder has shown with his study “Do Stocks Outperform Treasury Bills?“:

While the overall U.S. stock market has handily outperformed Treasury bills in the long run, most individual common stocks have not. Of the nearly 26,000 common stocks that have appeared on Center for Research in Securities Prices CRSP from 1926 to 2016, less than half generated a positive lifetime buy-and-hold return (inclusive of reinvested dividends), and only 42.6% have a lifetime buy-and-hold return greater than the one-month Treasury bill over the same time interval. The positive performance of the overall market is attributable to large returns generated by relatively few stocks.

When stated in terms of lifetime dollar wealth creation to shareholders in aggregate, […] slightly more than four percent of the firms account for all of the net stock market gains. The other ninety six percent of firms that issued stock collectively matched one-month Treasury bill returns over their lifetimes.

Stock pickers, therefore, bear a considerable risk of underperformance. This brings us directly to reality #8. There, we will look at how devastating such underperformance can be on total returns. Furthermore, we will see which scenario we want to avoid at all costs. But before I get to that, let’s look briefly at the following aspect.

Reality #6: every party will eventually find its end & there is no “this time is different”

Every outperformance will end at some point. We should accept that as well. There will also never be an “everything is different now.” Why is that? Let’s look at how the market allows outperformance to occur in the first place.

Outperformance always goes hand in hand with a superior investment strategy. Let’s take a look at Gary. Gary is an analyst and recognizes patterns before other investors see them. He acknowledges that Company A’s stock always rises after the annual numbers are announced. The company’s management is highly conservative and consistently under forecasts. That’s why the market is pleasantly surprised by the great performance every year. So Gary buys shares of Company A every year before the annual figures are published. At some point, other investors recognize this pattern and also purchase shares before the publication. For Gary, that’s the end of the party; he has to look elsewhere for quick returns.

And so any initially superior strategy will eventually end, basically eaten up by its own performance. There is no escape from that. But the problem is that such a party rarely ends quietly. Most often, it ends with a bang. And the bang is the louder, the longer and more fierce the party went. For such a party to end, it is not necessarily critical that companies have poor operational performance. So this is where reality #1 comes into play.

While the end of each party is certain, no one knows when that moment arrives. That’s what makes it so tricky. The party is great. And everyone on the sidelines clenches their fists in their pockets as they watch the wild dance on the parquet.

Reality #7: irreversible wealth-destroying events will likely lead to underperformance

Underperformance is not something terrible per see because not achieving the very best return is not necessarily a mistake. It is just not the very best return. As private investors, however, we do not want to achieve the very best return at all costs. Since we manage our assets first and foremost, the goal is to preserve them. Only in second place is it about growing their value.

In my eyes, final/irreversible losses are the actual yield killers and thus the real mistakes. In another article, I provided the following example:

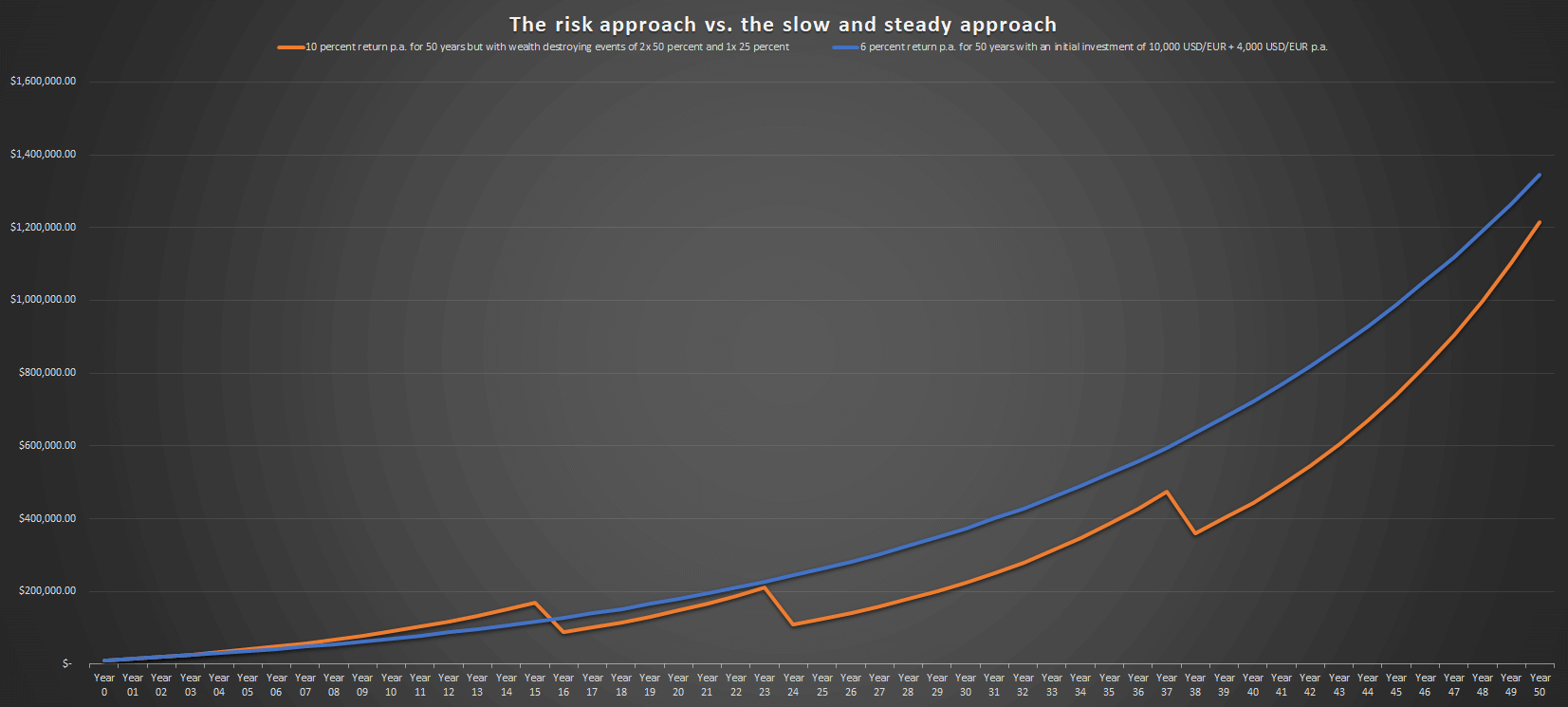

Even for an investor who has a higher return because of his risky strategy, such events significantly impact the overall performance. Not in a good way. We assume that the high-risk investor achieves an annual return of 10 percent. As in the example above, the initial capital was 10,000 USD/EUR, and the yearly investment 4,000 USD/EUR. With three extreme events of losing 50 percent of the assets twice and 25 percent once, this investor did worse after 50 years than the investor with an annual return of only 6 percent.

We must therefore try to avoid such final wealth-destroying events in the long term. Because of this reality and the risk therein, my readers and I do not leverage our investments. Buying stocks on margin is a big fat no-go.

Hedge fund manager Bill Hwang is a prime example. With his fund disguised as a family office, Hwang placed bets on stocks such as Viacom CBS, and Disney, as well as Chinese companies like Tencent and Baidu. To achieve exceptionally high returns, Hwang used substantial credit leverage. For every share Hwang held through his fund/family office Archegos, banks lent him up to 20 additional shares. Hwang was forced to close the fund after a margin call, leaving billions in damages to banks. So what good are the highest returns if they can fall to zero at any time?

Reality #8: we know nothing

Now, we come to a reality that has the potential to discredit everything I have said before. Yes, we know nothing except that we know that we know nothing. Now how does this fit with the above?

For once, we must distinguish between what we fundamentally think we know in life and what we know when we invest. The first is a philosophical question. Here we ask: What do we know, and is what we think we know real? The second is a question of proper risk management. I am referring here only to the second question. Concerning the second question, we have to take what we see or at least what we think to see for granted. I am not interested in deciding whether what we supposedly know is true and correct, i.e., whether it correctly reflects reality. That’s only the scope of the first question.

By exclaiming “we know nothing,” I am referring to the future alone. What we don’t know is what lies ahead of us. But as we invest to benefit from rising share prices and dividends, our actions are geared to the future. This is a paradox. We want to profit from the future. But we also have to admit that we do not know what the future will look like. It’s like visiting a friend without knowing if the chosen path will end at his or her house door.

The only thing we can do is to take the present and the lessons of the past as a point of reference. Here, however, we have to be extremely careful not to tear down the foundation we built on above. My sole concern here is risk reduction. That’s why I want to address the last few points before returning to reality #8.

Reality #9: usually, the more unclear the sky is, the more cautiously we fly

Above, I said that I don’t know what direction the future will take. But I don’t consider that a reason to bury my head in the sand. That would not be helpful. Besides that, I’m an optimist and think that things will go on somehow. Why else would we make daily dispositions that are only designed to affect the future (school, healthy eating, ambition at work, etc.)?

No, as I described above, accepting reality #8 helps me minimize my risk. Let’s suppose the future is on the opposite side of a canyon. Two bridges cross this canyon. One bridge is stable, the railing is rust-free, and technicians checked the statics just yesterday. A second bridge looks nasty and could also be a prop in an Indiana Jones movie. The advantage of this bridge: It is built over a narrow part of the canyon. Passing it would take only half as long as the other bridge.

We wouldn’t take the second bridge to save two minutes, right? Given the risk factors, we would opt for the supposedly safe bridge, even if we can’t rule out the possibility that the second bridge will also bring us safely to the other side. This is a straightforward but essential evolutionary consideration that is usually hard-wired into our thinking. Nevertheless, when investing in stocks, we repeatedly indulge in narratives that ignore the uncertainties entirely.

We are talking about real uncertainties here, not supposed certainties. This means that I try to exclude as many uncertainties as possible from my investment decisions and rely on an absolute minimum of supposed certainties. Therefore, the following narratives do not exist for me since they are either uncertain or only supposedly certain:

- “This time, everything is different.”

- “The comparison to other bubbles does not fit.”

- “I prefer to wait for the bottom before investing.”

- “I don’t think we’ll see the old all-time highs again for the next 10, 15 years.”

- “Low rates will keep stock markets high.”

- “Debts are no problem.”

All these considerations reduce my investment approach to one certainty. And that is the link between a company’s business and a share’s price.

Reality #10: Understanding realities #1 to #9 leads us on the right path

We see that accepting each reality has tangible consequences for investing in stocks. Therefore, I want to recap the main implications that form the foundation of my investment decisions:

- My portfolio is my business, and I don’t need it to explode, but I want it to grow sustainably and steadily, and I want to sleep peacefully. To achieve this, I try to reduce the impact of uncertainties as much as possible. Conversely, I also try not to rely on too many supposed certainties or narratives. The more uncertainties I have to accept for an investment or the more narratives I need for justification, the more confident I will not put money on it. That might not be the perfect deal, but it helps to sort out many possible distortions.

- When investing in stocks, there is only one decisive consideration for me: the link between the company’s value and the share price. The more disturbed or out of proportion this connection is, the higher the uncertainty. You could also break it down into the following: High negative difference = high risk. Low negative difference = low(er) risk. And risk is something I avoid.

- Considering the above, our profit lies already in our purchase decision. In doing so, we anchor the profit in the present and have less reason to fear the future. All this does not make investing in stocks easy. There will never be a philosopher’s stone. But I believe that accepting these realities will put us on the right path.

Wow, that were many words. May they inspire.

I was asked by an attentive reader why I used a Japanese image when I mostly write about US and European stocks. I have a simple answer: because the pic is beautiful. 🙂

[…] bear downward exaggerations simply as violently as earlier upward exaggerations. Behind that is the inventory market knowledge that what flies excessive falls simply as low. It’s no completely different for shares, as […]