Now it has happened what I already announced in my last Bayer stock analysis: Bayer has cut its dividend, which is likely to hurt investors who have bought Bayer shares in recent years in particular. This article takes a first look at what investors can expect from Bayer stock after the dividend cut and whether the poor price performance in the last months is justified. The article is meant to be a snap evaluation of the current situation. I will update it in the next few days and especially take into account the earnings call transcript.

Last quarter / full-year 2020 was ok

Bayer has published its figures for fiscal 2020. As a result, Bayer’s share price fell by several percent. Overall, the figures were okay but also had some rather dark sides, which do not only concern the reduced dividend. So let’s take a brief look back at the last fiscal year.

Sales remained virtually unchanged, growing by only 0.6 percent. Adjusted earnings (or core earnings) of EUR 6.39 were also on par with the previous year. But: EPS (not adjusted) was minus EUR 10.68 (compared to EUR 4.17 last year). Bayer thus slipped deep into the red. Investors have to look back a long time to find anything comparable at Bayer. The last time Bayer had a negative EPS was in 2003 when the company finished the year with an EPS of minus EUR 1.83.

Overall, the loss (EBIT) amounted to EUR 16.169 billion. This loss was due to exceptional items amounting to EUR 23.264 billion (previous year: EUR 2.813 billion), mainly because Bayer built up reserves for legal disputes. Free cash flow also decreased to EUR 1.3 billion (2019: EUR 4.2 billion) due to almost EUR 4 billion litigation-related expenses.

Losses aren’t surprising

In total, however, these expenses/costs were not surprising. Bayer had already built up high reserves for legal disputes in recent quarters, resulting in a loss (EBIT) of more than EUR 10 billion in 2Q 2020.

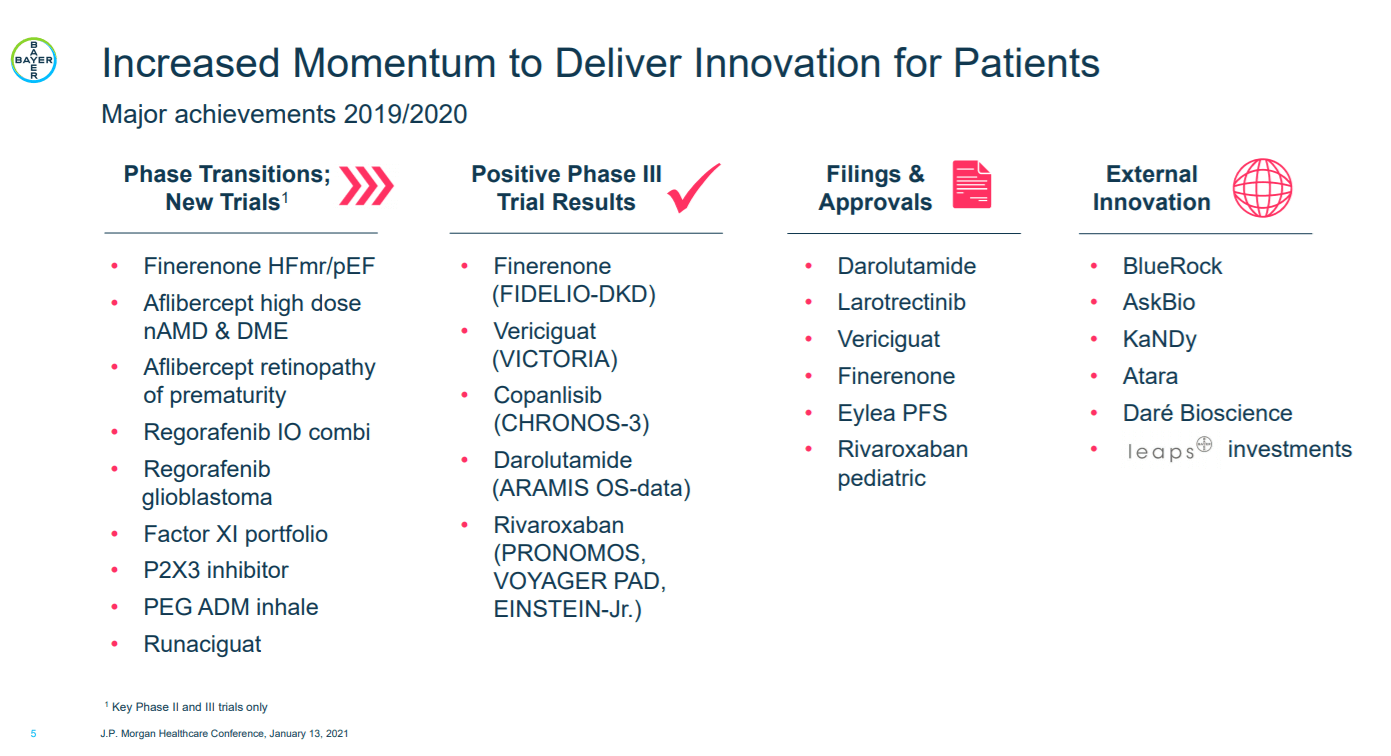

The pharma pipeline gets bigger (that’s good)

Bayer’s pharmaceuticals business deserves special mention. In 2020, Bayer completed more than 25 acquisitions or collaborations in the pharmaceuticals sector alone. Bayer’s pipeline was a critical point here for many years. One problem was the expiring patent for the blockbuster drug Xarelto (anticoagulant) in 2024. Bayer is increasingly strengthening its activities in cell and gene therapies, which are expected to become much more important in the future. Of particular note is the collaboration with Curevac and the acquisitions of Bluerock in 2019 and AskBio. Accordingly, the pipeline is well filled.

Dividend cut (that’s bad)

According to Bayer’s dividend policy, the company will distribute 30 to 40 percent of core earnings per share to its shareholder each year. The company announced that it would pay a dividend of 2.00 euros per share this year. That’s a cut of almost 30 percent and already hurts existing shareholders quite a bit.

The dividend cut isn’t a surprise

Like the EBIT loss, the dividend cut is no surprise. Already in my last analysis of the Bayer stock in October last year, I announced that this would happen:

Based on Bayer’s latest forecasts, I expect core earnings of about EUR 6.20 in 2020. Considering a payout ratio of 33 percent, Bayer would pay a dividend of EUR 2.05 per share, which corresponds to a 25 percent cut. But even with the reduced payouts, a return of over 4 percent would still be attractive at the current share price. Only older shareholders are likely to be upset (and rightly so).

Et voila, here we are now: We have a core EPS of EUR 6.40 and a dividend of EUR 2.80 per share, which means that the dividend yield at the current share price is approximately 3.8 percent.

Debts (the surprisingly good thing)

The development on the debt-side is also positive. Bayer reduced net financial debt by 11.8 percent year on year to EUR 30.041 billion. Bayer thus appears to be on the way to reducing its debt somewhat.

Updates regarding legal disputes

Regarding the glyphosate litigation in the United States, Bayer announced that it had reached an agreement with plaintiffs’ counsel on a class plan intended to manage and resolve future glyphosate cases. The plaintiffs’ counsel filed a motion for preliminary approval of the class agreement. Well, Bayer announced such an agreement already last year, which should have settled 75 percent of the ongoing proceedings. That settlement would have been a fair deal for Bayer shareholders. But then it became doubtful whether parties could conclude the settlement in this way. The responsible judge expressed his skepticism about the proposed treatment of future claims.

So now, Bayer came up with a new proposal, which is now subject to court approval. According to Bayer,

the class plan is intended to be one part of a holistic solution designed to provide further closure to the Monsanto Roundup™ litigation. Approximately 90,000 current claims in the Roundup™ litigation overall are covered by settlement agreements or did not meet the settlement program eligibility criteria. The company continues to negotiate with plaintiffs’ counsel to reach agreements in the remainder of current cases.

Therefore, we can state that the process risks still exist and that there has been no real progress here. Investors need to know what they are doing here. The number of lawsuits and the possible amount of damages in the US legal system could, at least theoretically, drive the company to ruin. Just do the math. Bayer has almost 100,000 pending lawsuits, and three California juries already ruled that Bayer must pay billions of dollars in combined damages. Therefore, as long as the settlement does not include future claims, things will remain rocky.

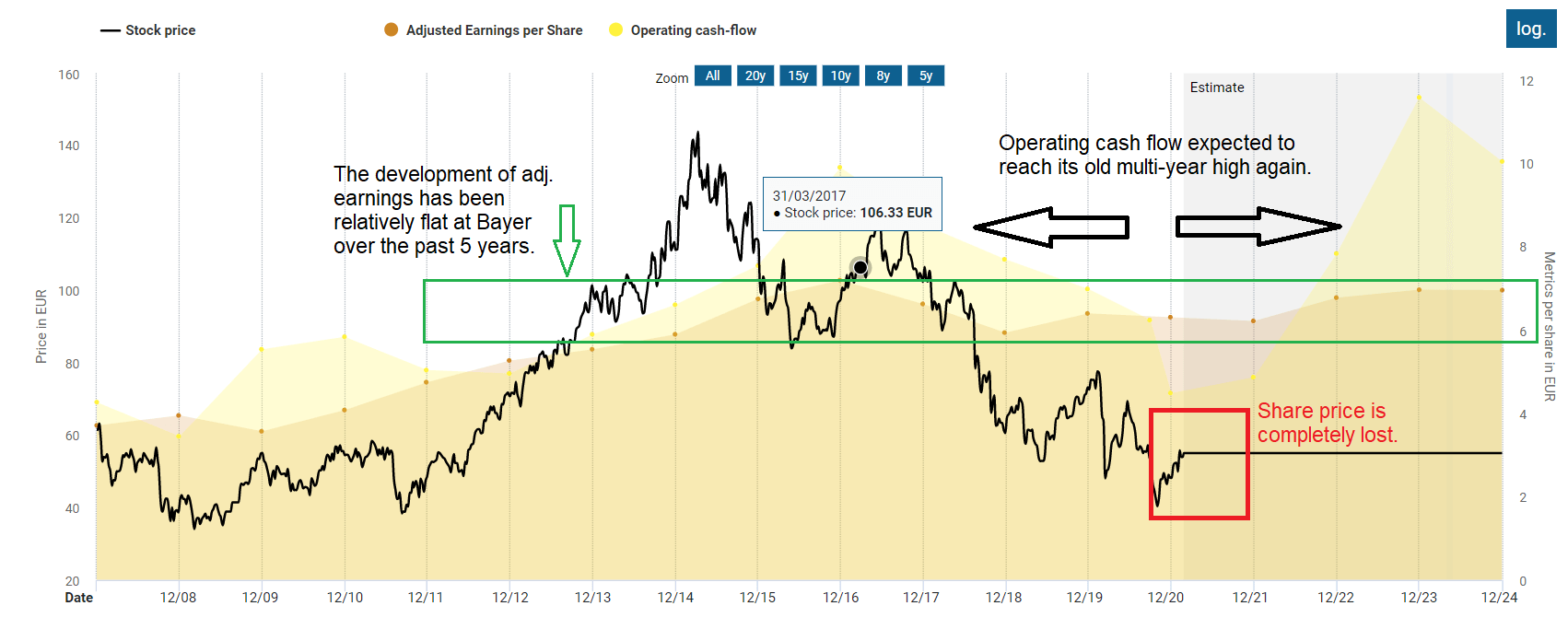

The share price performance remains extremely disappointing. While many investors are making extreme profits on risky gambles and tech stocks, investors in the Bayer stock have to endure a lot of suffering. The share is now more than 60 percent away from its previous high. The interesting thing is that adjusted earnings have hardly changed since these highs. Operating cash flow is also expected to reach the old highs in the coming years. However, Bayer’s share price is entirely unimpressed by these numbers.

The stock market always sees the share price in context, and currently, the risks seem to outweigh the opportunities. Besides, you should not overlook the number of outstanding shares. Those have increased from 840 million in 2015 to 981 million at present, diluting earnings per share and dividends.

Is the Bayer stock after the dividend cut a buy?

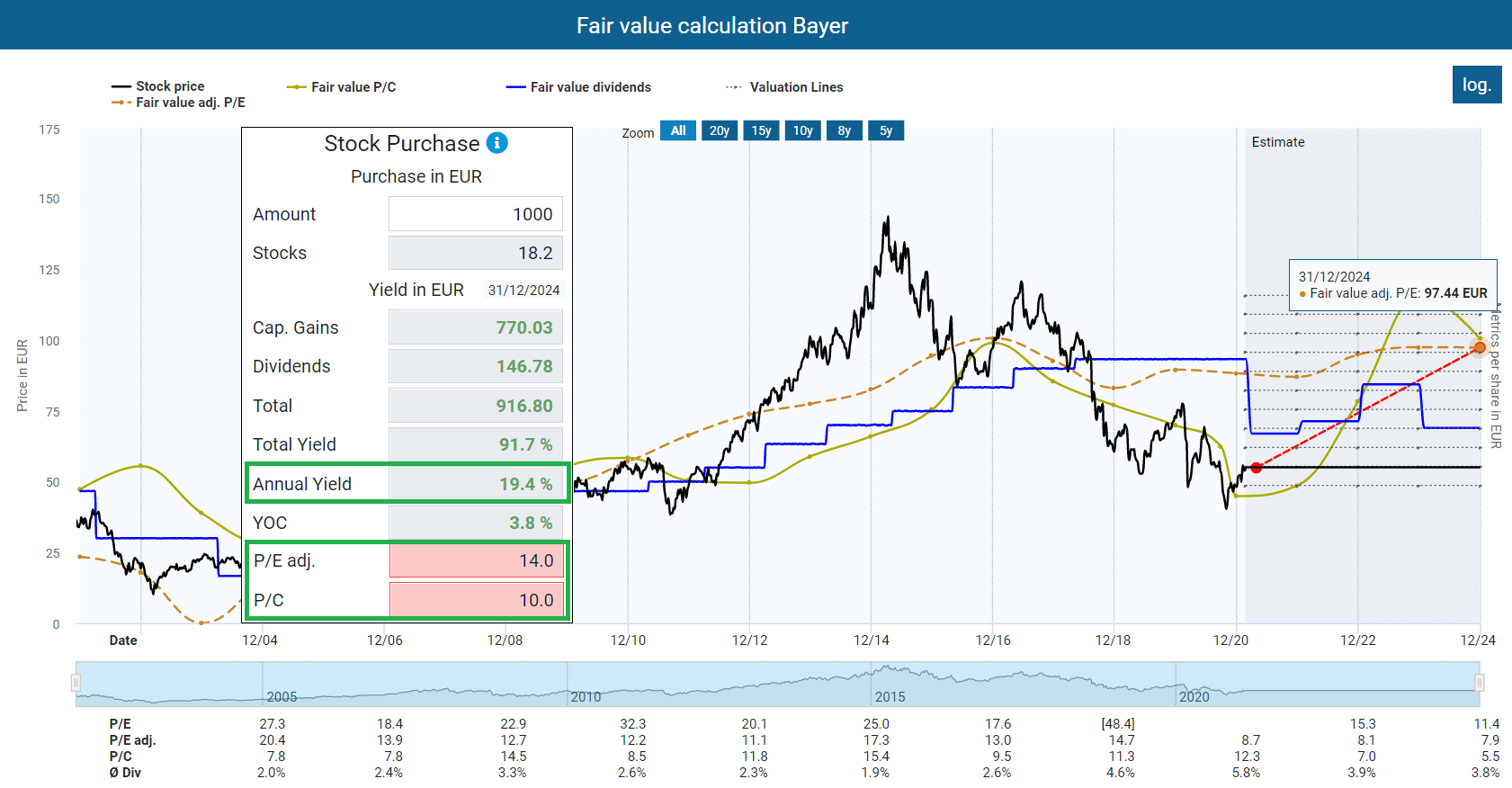

Is the Bayer stock still a buy after the dividend cut? From a fundamental point of view, yes. I assumed an adjusted P/E ratio of 14 and a P/C ratio of 10 as a fair value for the Bayer stock. If we look at the expected earnings and cash flows for 2024, we see an annual upside potential of almost 20 percent – based on an adjusted P/E ratio of only 14!

Do you agree that the Bayer stock is undervalued?

The FY 2020 numbers were actually within the range of expectations. I am therefore somewhat surprised that the market was so taken by surprise. Well, it seems that the TEV-Blog community knows more than Mr. Market 🙂

Nothing has changed for me in terms of the actual investment thesis. I have invested less than 1.6 percent of my capital in Bayer shares and therefore hold the shares. In the long term, of course, I hope that profits and dividends will rise again. Bayer is quite well-positioned in growth areas such as gene therapies and crop sciences. Likewise, the stock is currently very cheaply valued, so there’s no reason to give another investor a bargain by selling my shares.

Has Bayer caught your interest after the dividend cut, or do you agree that the Bayer stock is undervalued? Be aware that attractive dividend yields should not be the only reason to buy shares of a company. And as I stated above, it is not unlikely that Bayer will cut the payouts next year. The same applies to individual metrics such as PE ratio or P/C ratio. Always look at such numbers in context. My analyses here on the TEV Blog are an excellent way to start your research (click here). You can also contact me here or ask the community in the comments if they can help with your due diligence.

–> Click here for more analysis <–

Bayer is part of my diversified retirement portfolio. If you enjoyed this article and wish to receive other long-term investment proposals or updates on my latest portfolio research, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

Today I have taken a large position in Bayer stock. And as always, when everything is fine, there will be no more such great prices. Or? Let’s see, time will tell …

Indeed, there are no gifts / free lunches on the stock market. I wish you good luck with your investment!

It’s really crazy… the market cap of Bayer is USD 60 billion. The Monsanto price was USD 60 billion. One might think that it can hardly go lower (unless the legal risks materialize), but who knows 😀

Proper risk management is decisive here.