Who does not seek them, the undervalued stocks that promise above-average returns? Well, the Bayer AG stock might be one of those. In this article, I will show you why the company is significantly undervalued at the moment, what upside potential it has, and what downside risks you should consider. I also look at the latest developments and discuss the risk of a dividend cut.

Bayer AG is an international company in the pharmaceutical and chemical industry with a more than 150-year history that offers an extensive range of products and services, including health care and nutrition and plastics and specialty chemicals. Bayer’s business contains three segments: Pharmaceuticals, Consumer Health, and Crop Science.

Click below to read my newest Bayer Stock update after the dividend cut

Segments

The Pharmaceuticals segment offers prescription products, especially for women’s healthcare, cardiology, and specialty therapeutics for many areas such as hematology, oncology, or ophthalmology. In the Consumer Health segment, Bayer is mainly active in markets for nonprescription (so-called over-the-counter) products for dermatology, nutritional supplements, digestive health, cold, allergy, flu, etc. The Crop Science segment is after Bayer acquired Monsanto, the world-leading agriculture enterprise with businesses in seeds and crop protection. Bayer also has an Animal Health segment. This segment develops and commercializes products and solutions for the prevention and treatment of diseases in pets. However, Bayer plans to sell this part of its business shortly (see below).

Bayer AG valuation

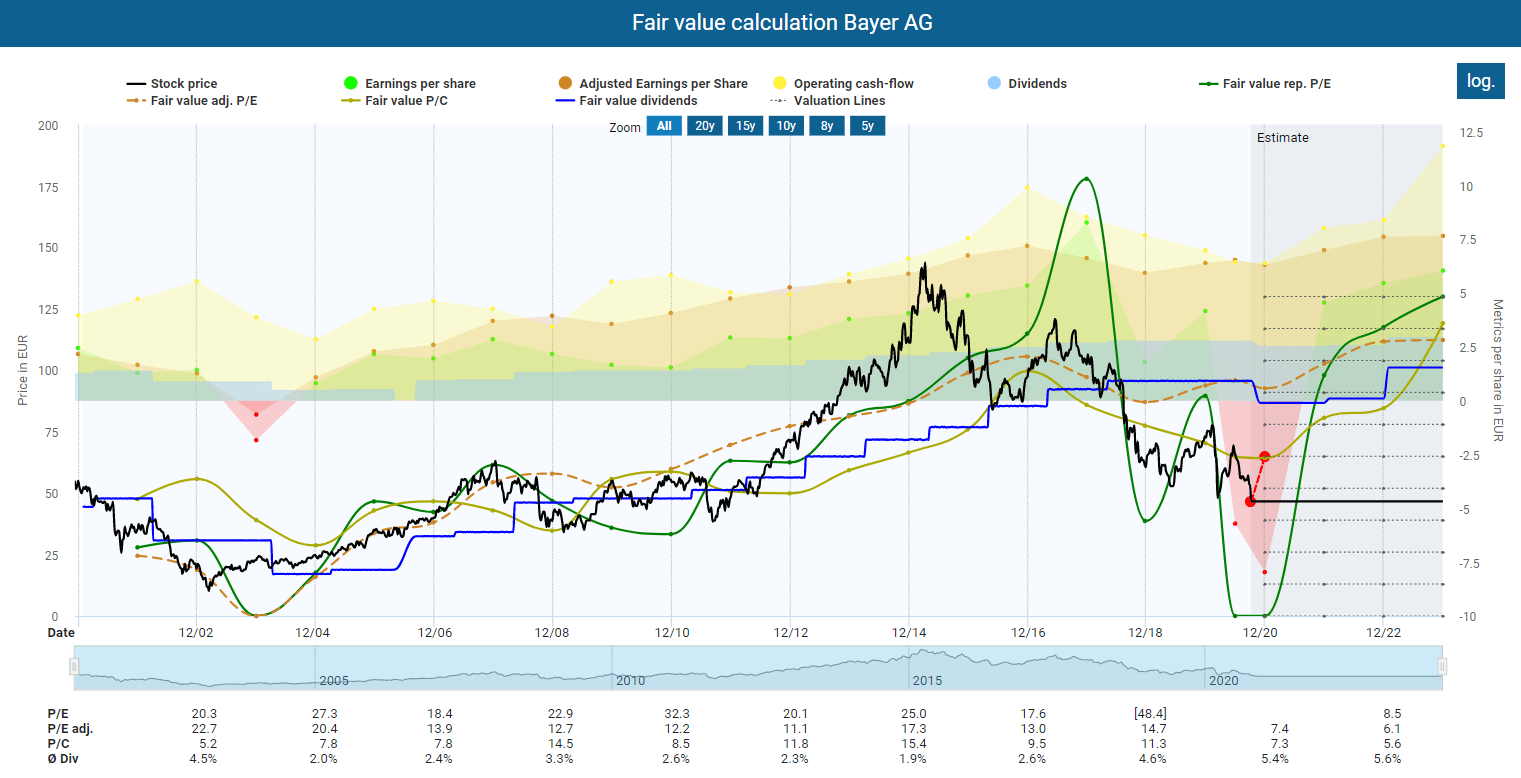

Bayer AG is currently significantly undervalued. You can see this clearly from the chart below. To explain: The chart shows the correlation between the share price and the development of earnings (reported and adjusted), cash flow, and dividend yield. I take into account the data of the last twenty years to show the most extensive possible time. As you can see, the current share price is far below its present and future (end of 2020) fair value. It does not matter whether we look at profits, cash flow, or the dividend.

The upside potential for the Bayer stock

Bayer’s current share price under 46 EUR (on the German stock exchange) is well below its fair value (side note: the all-time high is at 140 EUR). The difference to its proper value results in enormous upside potential for Bayer. If we look at what the fair value of the stock would be based on the historical average of the last 20 years for each multiple, the upside potential to the fair value (by the end of 2022) would be as follows:

- Adjusted earnings: 70 percent

- Cash Flow: 150 percent

- Historical Dividend Yield: 101 percent.

Evaluating the downside potential for the Bayer stock

Of course, every opportunity is matched by a corresponding risk. And at Bayer, there are even two significant risks. One is that Bayer is quite heavily in debt. The second risk is the legal problems the company is facing. Both risks are related to the acquisition of Monsanto. The company paid USD 62 billion in cash for the masterpiece of CEO Werner Baumann.

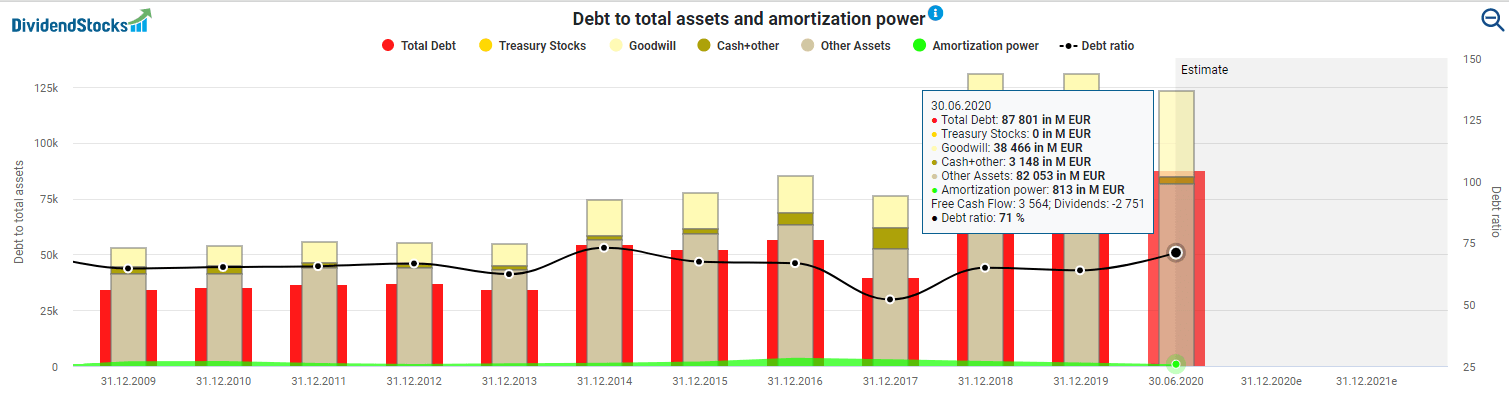

Bayer’s debt pile after the Monsanto acquisition

If we look at the current debt profile, the debt ratio is over 71 percent. That is too high in my eyes. The optimum for me is a value below 50 percent. I am also skeptical about the low amortization power of EUR 813 million per year compared to all debts (including liabilities) of EUR 88 billion.

But here we must put things into perspective. Due to COVID-19, the cash flow in 2020 is and will be very low. In the previous years, the amortization power was much higher:

- 2016: EUR 3.7 billion

- 2017: EUR 2.9 billion

- 2018: EUR 2.2 billion

- 2019: EUR 1.6 billion.

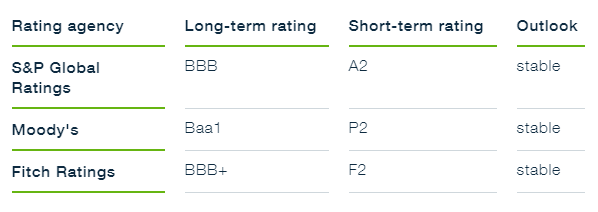

By the end of the year, Bayer will have already paid off EUR 9 billion of its total debt mountain since 2018 (more than 10 percent). The company’s rating is not the worst, either.

Besides, Bayer finally sold its animal health segment to Elanco for USD 7.6 billion. Elanco paid USD 5.32 billion in cash and the reaming USD 2.28 billion with shares. Bayer is thus concentrating on the Crop and Pharmaceuticals divisions.

Nevertheless, we have also seen that the amortization power continues to decline, while the debt ratio has even risen again recently. Last year, the debt pile (including all liabilities) was at EUR 83 billion. This year will end with a pile of almost EUR 88 billion. That is not the way I would like to see it as shareholders.

Taking legal Monsanto risks into account

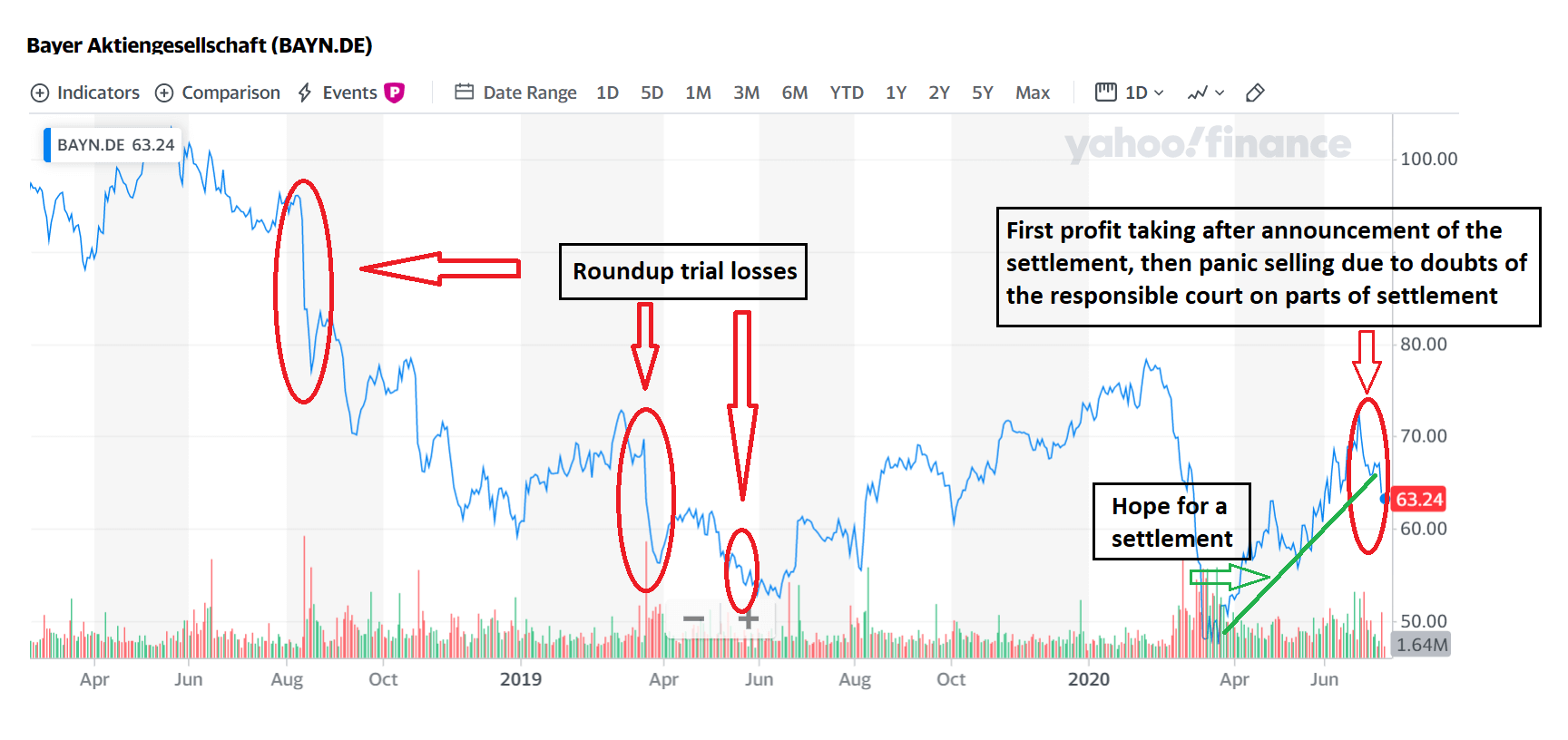

However, I do not think that the debt problem is the biggest problem for Bayer. The main risk lies in legal issues. Bayer has had to deal with massive lawsuits and has already suffered severe defeats. But then, Bayer announced a mega settlement of USD 11 billion, which should have settled 75 percent of the ongoing proceedings.

Bayer wanted to pay between USD 8.8 billion and USD 9.6 billion to end the current proceedings, including a fixed sum to cover claims that have not yet been settled and an additional USD 1.25 billion for a separate agreement for potential future claims. Bayer planned to set up a scientific panel, while legal action should continue to be possible. The scientific panel would investigate whether or not the active ingredient in Roundup causes cancer. The critical point of the settlement for future lawsuits was that if the panel determined that glyphosate was not a carcinogen, then the members of the class action lawsuits would not be able to claim damages.

That settlement would have been a fair deal for Bayer shareholders. But then it became doubtful whether the settlement could be concluded in this way. The responsible judge expressed his skepticism about the proposed treatment of future claims. I still believe that there will be an agreement in the end, as only the handling of future lawsuits is in dispute. And indeed, in the meantime, it became public that Bayer has made progress with attorneys on a changed plan concerning potential future lawsuits. The details of the revised concept could be announced as early as October.

However, the failure of a settlement about future lawsuits will cause significant uncertainty. Shareholders react very sensitively to the development of the trials.

Is the merger thesis still valid?

Bayer has presented relatively stable figures for Q2 2020. Revenue declined by only 2.5 percent. Furthermore, don’t let Bayer’s horrible EBIT of minus EUR 10.784 billion unsettle you. These are provisions for settlements built up concerning the litigations involving Dicamba, Glyphosate, PCB, and Essure. Free cash flow amounted to a strong EUR 1.402 billion.

Q2 2020 has otherwise confirmed the merger thesis. The 3.2 percent growth in the Crop Science segment enabled Bayer to offset declines in sales of Pharmaceuticals (minus 8.8 percent) and Consumer Health (minus 1.9 percent). Adjusted earnings in the Crop Science Division rose by 28.4 percent to EUR 1.3 billion due to cost synergies from the merger and higher volumes.

Bad news at the end of September 2020

At the end of September, however, the company caused disillusionment, which a very depressing outlook (all taken from a press release, which can be found here):

- Growth and cash flow generation are expected to be lower than planned and can only be partially compensated by further savings measures. Thus, Bayer now expects 2021 revenues at approximately 2020 levels.

- Furthermore, the core earnings per share in 2021 are expected to be slightly below 2020 levels.

- To face a challenging environment, Bayer wants to achieve additional operational savings of more than EUR 1.5 billion annually as of 2024, which comes on top of annual earnings contributions of EUR 2.6 billion as of 2022.

- Bayer plans to allocate the cash flow from these efforts in further innovation, profitable growth opportunities, and debt reduction.

Crop Science disappoints

What weighs much worse, however, was the announcement that the crop science business, in particular, will suffer from the consequences of the COVID-19 pandemic.

The direct and indirect effects of the pandemic will be deeper than expected on the Crop Science business. The agricultural sector, in which Bayer has a leading role, is characterized by reduced growth expectations due to low commodity prices for major crops, intense competition in soy, and reduced biofuel consumption. This is compounded by negative currency effects, some of which are significant as in the case of the Brazilian Real. This situation is unlikely to improve considerably in the near-term.

Accordingly, Bayer has to write down assets in the Crop Science business in the mid to high single-digit billion euro range. This isn’t very pleasant because it shows that Bayer may have paid too much for Monsanto. Just a reminder: Bayer paid USD 63 billion for Monsanto and is now only worth about USD 50 billion. It now appears that Crop Science cannot keep the promise that Bayer has made to its shareholders for the near future. Of course, the COVID-19 crisis has put a particular strain on Bayer here, but at the end of the day, that doesn’t change the fact that you, as the owner of the company, will not see any growth shortly and more problems have been added to the existing ones.

Does this justify such a drawdown?

The question is, of course, whether this announcement justifies such a discount. At the announcement, Bayer’s share price fell by 10 percent, although Bayer merely announced that sales, core earnings, and cash flow would remain stable or decline only slightly. The reaction seems a bit exaggerated to me. Nevertheless, it is understandable because Bayer seems to have worse problems in the Crop Science segment due to the COVID-19 pandemic than CEO Baumann thought a few months ago.

COVID-19, of course, also hit the CEO unexpectedly and was not his fault, but for the shareholders, who naturally carry a business risk with investments in stocks, these are not pleasant prospects, so they preferred to sell their shares to try their luck elsewhere.

Why a dividend cut is likely

The Board of Management intends to leave the dividend policy intact. Accordingly, the company will distribute 30 to 40 percent of core earnings per share to its shareholder each year. However, Bayer also announced that the coming years’ payouts are expected at the lower end of this corridor rather than at the upper end as in previous years.

What this means and why it implies a dividend cut, I will show you in the following. So, last year (the fiscal year 2019), Bayer had core earnings of EUR 6.40 and distributed EUR 2.8 in dividends, which equals a payout ratio of 43 percent. Based on Bayer’s latest forecasts, I expect core earnings of about EUR 6.20 in 2020. Considering a payout ratio of 33 percent, Bayer would pay a dividend of EUR 2.05 per share, which corresponds to a 25 percent cut. But even with the reduced payouts, a return of over 4 percent would still be attractive at the current share price. Only older shareholders are likely to be upset (and rightly so).

Conclusion

The number of lawsuits and the possible amount of damages in the US legal system could, at least theoretically, drive the company to ruin. Just a reminder: Three California juries already ruled that Bayer must pay billions of dollars in combined damages. Hence, as long as the settlement does not include future claims, things will remain rocky. So yes, do the math. Bayer has 100,000 pending lawsuits. Additionally, the company already lost an appeal where the court stated that Bayer has to pay USD 20 million.

I will, therefore, follow the developments closely. Furthermore, I will not add any more Bayer shares to my portfolio to diversify my risks, even if the stock seems cheap. I already have enough Bayer shares in my retirement portfolio (about 4 percent of the total portfolio). That is enough for me.

Although I still expect a settlement to be reached, there are new problems in the operating business now. What is particularly upsetting is that this affects the newly acquired business. These could even result in Bayer cutting the dividend for the first time since 2007.

Is The Bayer Stock A Buy After The Dividend Cut?

Now it has happened what I already announced in my last Bayer stock analysis: Bayer has cut its dividend, which is likely to hurt investors who have bought Bayer shares in recent years in particular. This article takes a first look at what investors can expect from Bayer stock after the dividend cut and whether the poor price performance in the last months is justified. The article is meant to be a snap evaluation of the current situation. I will update it in the next few days and especially take into account the earnings call transcript.

Last quarter / full-year 2020 was ok

Bayer has published its figures for fiscal 2020. As a result, Bayer’s share price fell by several percent. Overall, the figures were okay but also had some rather dark sides, which do not only concern the reduced dividend. So let’s take a brief look back at the last fiscal year.

Sales remained virtually unchanged, growing by only 0.6 percent. Adjusted earnings (or core earnings) of EUR 6.39 were also on par with the previous year. But: EPS (not adjusted) was minus EUR 10.68 (compared to EUR 4.17 last year). Bayer thus slipped deep into the red. Investors have to look back a long time to find anything comparable at Bayer. The last time Bayer had a negative EPS was in 2003 when the company finished the year with an EPS of minus EUR 1.83.

Overall, the loss (EBIT) amounted to EUR 16.169 billion. This loss was due to exceptional items amounting to EUR 23.264 billion (previous year: EUR 2.813 billion), mainly because Bayer built up reserves for legal disputes. Free cash flow also decreased to EUR 1.3 billion (2019: EUR 4.2 billion) due to almost EUR 4 billion litigation-related expenses.

Losses aren’t surprising

In total, however, these expenses/costs were not surprising. Bayer had already built up high reserves for legal disputes in recent quarters, resulting in a loss (EBIT) of more than EUR 10 billion in 2Q 2020.

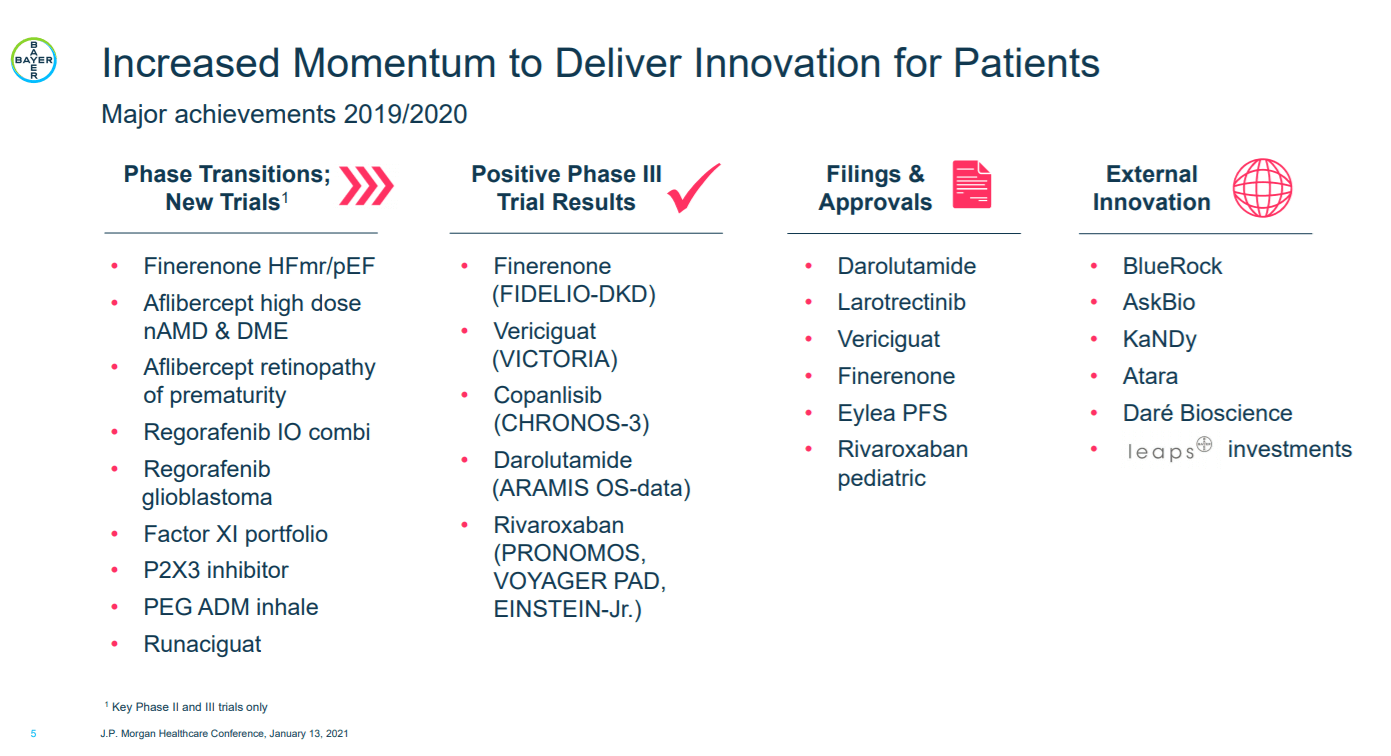

The pharma pipeline gets bigger (that’s good)

Bayer’s pharmaceuticals business deserves special mention. In 2020, Bayer completed more than 25 acquisitions or collaborations in the pharmaceuticals sector alone. Bayer’s pipeline was a critical point here for many years. One problem was the expiring patent for the blockbuster drug Xarelto (anticoagulant) in 2024. Bayer is increasingly strengthening its activities in cell and gene therapies, which are expected to become much more important in the future. Of particular note is the collaboration with Curevac and the acquisitions of Bluerock in 2019 and AskBio. Accordingly, the pipeline is well filled.

Dividend cut (that’s bad)

According to Bayer’s dividend policy, the company will distribute 30 to 40 percent of core earnings per share to its shareholder each year. The company announced that it would pay a dividend of 2.00 euros per share this year. That’s a cut of almost 30 percent and already hurts existing shareholders quite a bit.

The dividend cut isn’t a surprise

Like the EBIT loss, the dividend cut is no surprise. Already in my last analysis of the Bayer stock in October last year, I announced that this would happen:

Based on Bayer’s latest forecasts, I expect core earnings of about EUR 6.20 in 2020. Considering a payout ratio of 33 percent, Bayer would pay a dividend of EUR 2.05 per share, which corresponds to a 25 percent cut. But even with the reduced payouts, a return of over 4 percent would still be attractive at the current share price. Only older shareholders are likely to be upset (and rightly so).

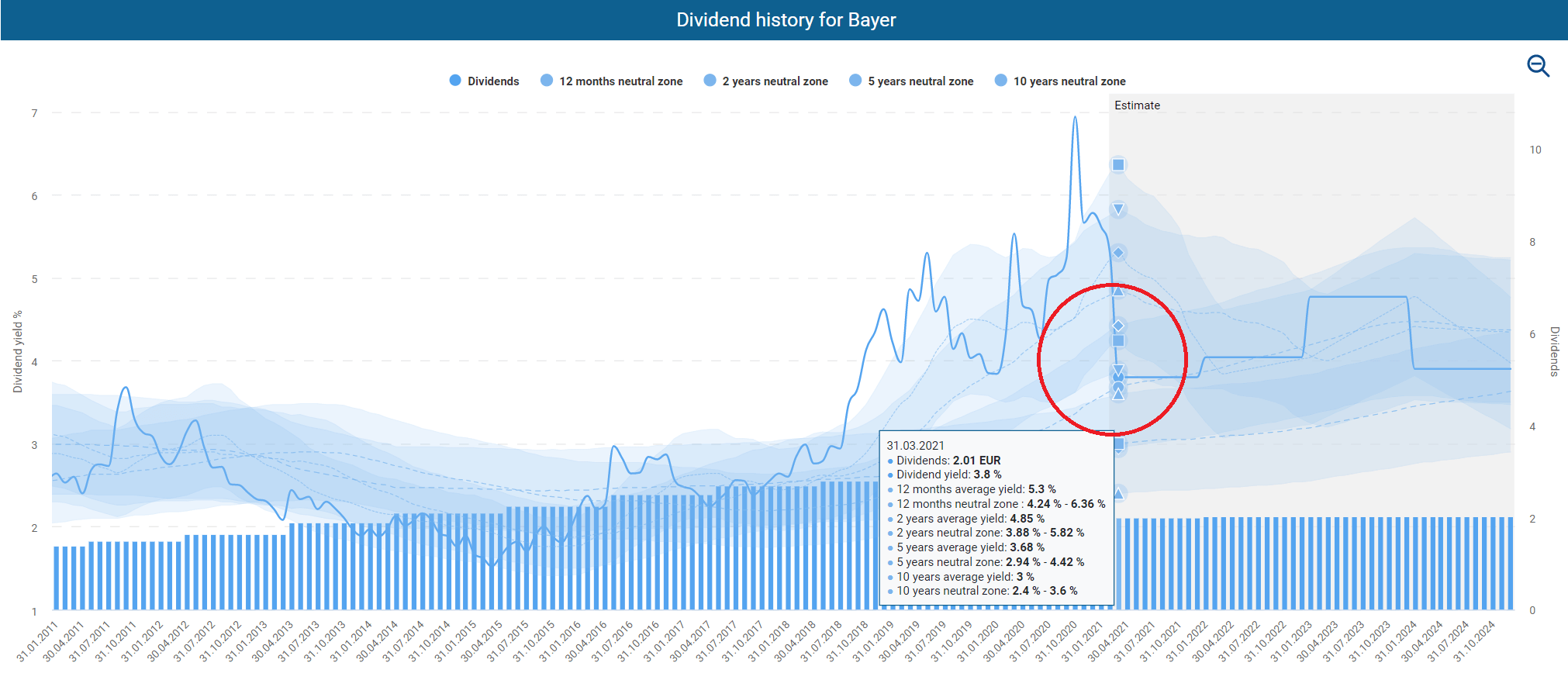

Et voila, here we are now: We have a core EPS of EUR 6.40 and a dividend of EUR 2.80 per share, which means that the dividend yield at the current share price is approximately 3.8 percent.

Debts (the surprisingly good thing)

The development on the debt-side is also positive. Bayer reduced net financial debt by 11.8 percent year on year to EUR 30.041 billion. Bayer thus appears to be on the way to reducing its debt somewhat.

Updates regarding legal disputes

Regarding the glyphosate litigation in the United States, Bayer announced that it had reached an agreement with plaintiffs’ counsel on a class plan intended to manage and resolve future glyphosate cases. The plaintiffs’ counsel filed a motion for preliminary approval of the class agreement. Well, Bayer announced such an agreement already last year, which should have settled 75 percent of the ongoing proceedings. That settlement would have been a fair deal for Bayer shareholders. But then it became doubtful whether parties could conclude the settlement in this way. The responsible judge expressed his skepticism about the proposed treatment of future claims.

So now, Bayer came up with a new proposal, which is now subject to court approval. According to Bayer,

the class plan is intended to be one part of a holistic solution designed to provide further closure to the Monsanto Roundup™ litigation. Approximately 90,000 current claims in the Roundup™ litigation overall are covered by settlement agreements or did not meet the settlement program eligibility criteria. The company continues to negotiate with plaintiffs’ counsel to reach agreements in the remainder of current cases.

Therefore, we can state that the process risks still exist and that there has been no real progress here. Investors need to know what they are doing here. The number of lawsuits and the possible amount of damages in the US legal system could, at least theoretically, drive the company to ruin. Just do the math. Bayer has almost 100,000 pending lawsuits, and three California juries already ruled that Bayer must pay billions of dollars in combined damages. Therefore, as long as the settlement does not include future claims, things will remain rocky.

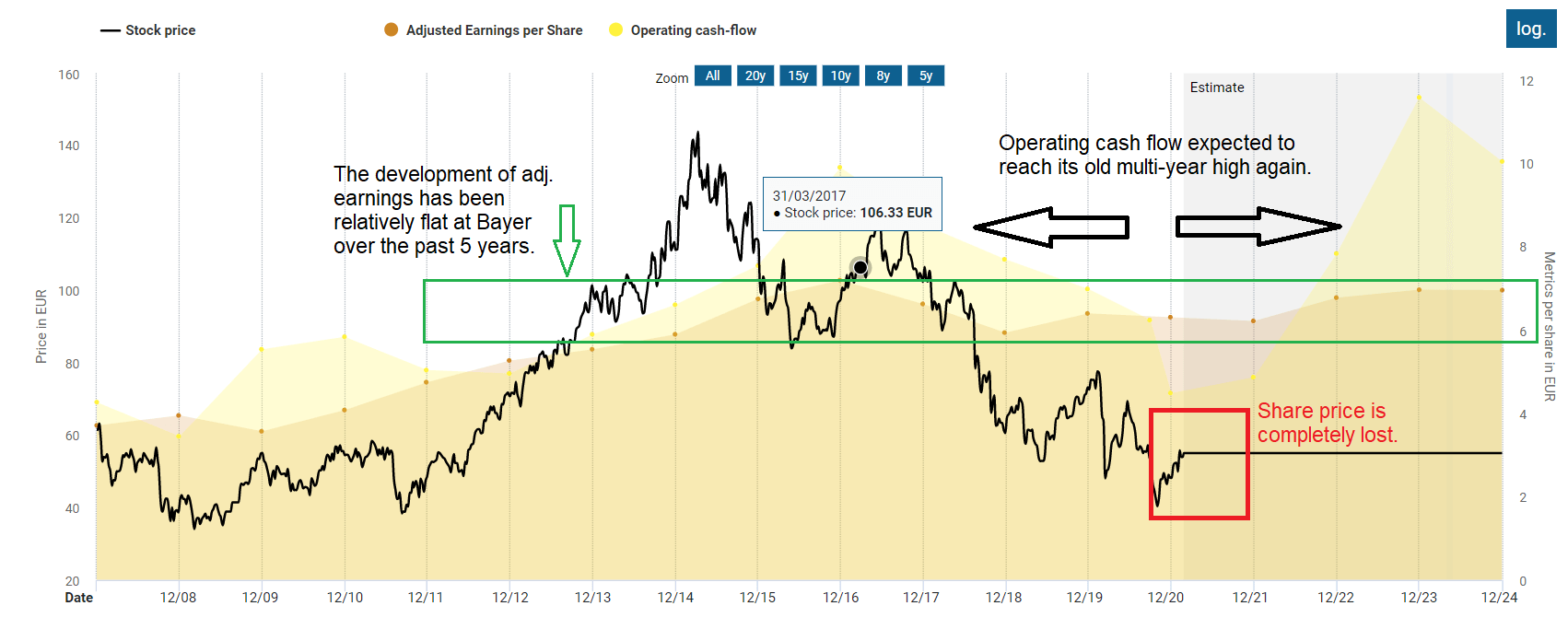

The share price performance remains extremely disappointing. While many investors are making extreme profits on risky gambles and tech stocks, investors in the Bayer stock have to endure a lot of suffering. The share is now more than 60 percent away from its previous high. The interesting thing is that adjusted earnings have hardly changed since these highs. Operating cash flow is also expected to reach the old highs in the coming years. However, Bayer’s share price is entirely unimpressed by these numbers.

The stock market always sees the share price in context, and currently, the risks seem to outweigh the opportunities. Besides, you should not overlook the number of outstanding shares. Those have increased from 840 million in 2015 to 981 million at present, diluting earnings per share and dividends.

Is the Bayer stock after the dividend cut a buy?

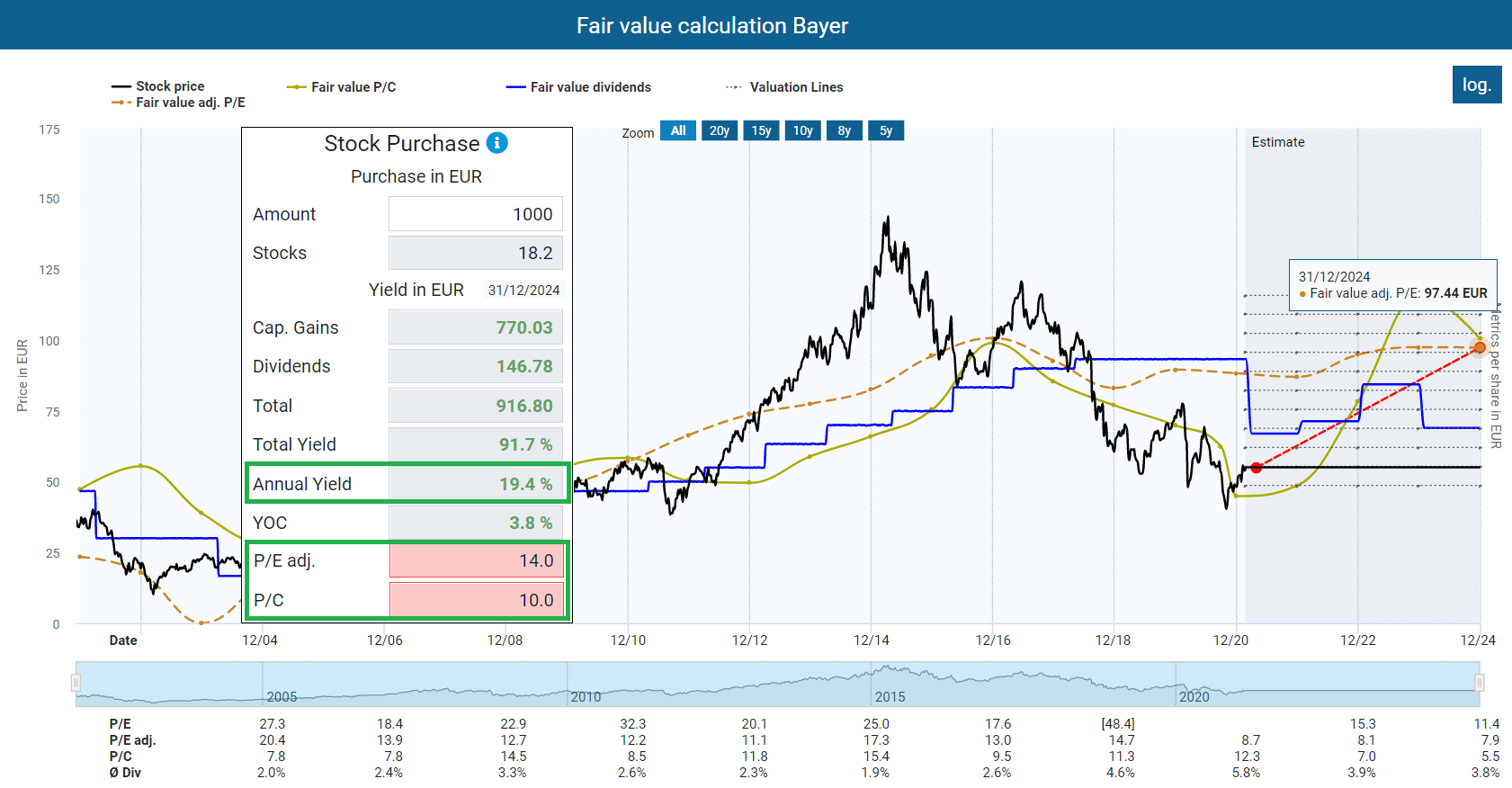

Is the Bayer stock still a buy after the dividend cut? From a fundamental point of view, yes. I assumed an adjusted P/E ratio of 14 and a P/C ratio of 10 as a fair value for the Bayer stock. If we look at the expected earnings and cash flows for 2024, we see an annual upside potential of almost 20 percent – based on an adjusted P/E ratio of only 14!

Do you agree that the Bayer stock is undervalued?

The FY 2020 numbers were actually within the range of expectations. I am therefore somewhat surprised that the market was so taken by surprise. Well, it seems that the TEV-Blog community knows more than Mr. Market 🙂

Nothing has changed for me in terms of the actual investment thesis. I have invested less than 1.6 percent of my capital in Bayer shares and therefore hold the shares. In the long term, of course, I hope that profits and dividends will rise again. Bayer is quite well-positioned in growth areas such as gene therapies and crop sciences. Likewise, the stock is currently very cheaply valued, so there’s no reason to give another investor a bargain by selling my shares.

Has Bayer caught your interest after the dividend cut, or do you agree that the Bayer stock is undervalued? Be aware that attractive dividend yields should not be the only reason to buy shares of a company. And as I stated above, it is not unlikely that Bayer will cut the payouts next year. The same applies to individual metrics such as PE ratio or P/C ratio. Always look at such numbers in context. My analyses here on the TEV Blog are an excellent way to start your research (click here). You can also contact me here or ask the community in the comments if they can help with your due diligence.

–> Click here for more analysis <–

Bayer is part of my diversified retirement portfolio. If you enjoyed this article and wish to receive other long-term investment proposals or updates on my latest portfolio research, you can easily follow me on

or Twitter.

Sharing Is Caring

Your thoughts are too valuable to keep them to yourself. Make them available to the world and the community by sharing them with us. All you have to do is leave a comment after reading the posts on the blog. Just use clear writing and clear thoughts.

Greed and more greed!

Bayer just finished yesterday the Elanco business for $6,89B like you said. They maintained the €2,80 per share and is trading at €57 today which is definitely undervalued.

I am looking for a good entry, my first, but now i am a bit confused. I did not know that correlation that you showed on the graphic about the the sensitivity price/trials sessions.

When is the next trial episode comes? If you did not have already some in your portfolio would you go in now at 56 or 57? Thanks for your analysis.

Do you know BME:ALM Almirall.? Tremendous potencial with some products already in phase3 China, and FDA approved, excellent metrics, low debt, very undervalued due corona,half price i think, solved all their past issues and pays a dividend. Anyway just sharing.

Joao Luz

Thanks for your valuable thoughts João Luz,

The figures for the 2nd quarter were in line with expectations, perhaps even slightly better. At present, however, litigation risks should continue to determine the share price. So it’s possible that it will fall even further. I am analyzing the quarterly numbers and the current situation in more depth right now. I will publish a short update on my analysis in the coming days/coming weekend here on the TEV blog.

Concerning Almirall, I don’t know the company. I’m cautious with pharmaceutical companies because I have little knowledge of pharmacy. That’s why I only buy the big ones. However, you are free to provide a more detailed review of the company here. This is what the TEV Blog is for.It is all about learning and sharing valuable thoughts 🙂

All the best

TEV

Got in today at 54.18€, 45min before close.The last time at this price was on March 31. We will have the third quarter results on November 3rd,i hope i did well. I saw the 36B debt on the bayer website! Anyway long Bayer from today. Cheers.

Welcome to the club! It could still get bumpy. I am also constantly thinking about buying more. However, my stake is already relatively large and I want to stick to my diversification rules. But maybe I will buy again in a few months.

In any case, all the best for our Bayer holdings!

Today it traded below 47 EUR.

Can you explain this in the light of the above article?

Hi PDM,

thanks for coming by.

Bayer has announced additional savings measures worth billions. It looks as if the the company is facing strong headwind from the corona pandemic (especially in its agricultural segment). Therefore, management expects earnings to decline in the coming year. That is bad, obviously but earnings per share in 2021 are likely to be only slightly below the previous year’s level. Furthermore, the company expects revenue to remain at about the same level as in 2020. I do not know if that means that the company is worth 10 percent less compared to yesterday. Stock market thinks so.

Bayer was a long term pick and it looks as if patience is necessary.

All the best,

TEV

Hi TEV,

Thanks for your answer.

It is jaw dropping what is going on with Bayer.

Bayer bought Monsanto for $63 Billion.

The entire company now is worth $53 Billion.

US courts can remain irrational longer than a German company can remain solvent.

Time will tell. This is one for investors with strong nerves I guess.

I enjoyed reading the article.

Regards,

PDM

Dear all,

I took a closer look at the news and did some math.Overall, the decline in the share price is somewhat exaggerated, but many shareholders have pulled out of the race and I can understand it somewhat. In addition, it is quite possible that we will see a dividend cut next year.Therefore, I have updated the article above a little bit. As always, you can ask questions in the comments 🙂

All the best,

TEV

Great article!

Although it’s clear, that you are highly interested in the (undervalued) Bayer stock, you do not neglect the risks and also point them out nicely – this demonstrates your professionality. Like you, I also have “enough” Bayer shares in my portfolio (around 3,5% of the total portfolio), so that’s the only reason I am not buying at the moment.

Looking forward to your next Bayer-Update.

all the best

Konstantin from finanzfunk.net

BAYER AG: SIMILAR TO BUYING VOLKSWAGEN THREE YEARS AGO?

https://www.undervalued-shares.com/reports/investment-reports/bayer-ag-similar-to-buying-volkswagen-three-years-ago/aff/9/