I welcome you to a new episode of my Dividend Diary on the TEV blog with this little intro. Is there anything better in the financial world than a dividend income? Well, I guess not. And so in September, I was again pleased to see a substantial increase in my dividends. I also used this month to add more shares and stocks to my portfolio. As always, in my monthly reports, I will give an update on my purchases. I document my monthly dividend income and the changes in my broadly diversified retirement portfolio. Here, I show you which companies have generated juicy cash flow for me each month and which stocks went into my basket. Besides, I analyze how the month has performed compared to the previous year. In the best case, my dividend income has increased.

As you know, I take care of my wealth management. To keep things simple, I have built three pillars:

- Active income.

- Passive income.

- Conversion.

Dividends fall into the last two categories. They are passive because I no longer have to work to receive the payments. Furthermore, they also contribute to the conversion because I reinvest the dividends and thus increase my passive income through dividends for the future.

My monthly dividend income in September:

This month I have received payments (before taxes) from the following companies:

- Fresenius (15,46 EUR)

- Johnson & Johnson (6.32 EUR)

- Archer Daniels Midland (6.31 EUR)

- Unilever (9.17 EUR)

- IBM (15.34 EUR)

- 3M (8.28 EUR)

- Realty Income (3.07 EUR)

- Royal Dutch Shell (6.34 EUR)

- V.F. Corp (10.28 EUR)

- Logitech (42.90 EUR)

- Qualcomm (9.03 EUR)

- Publicis (13.59 EUR)

- PepsiCo (5.85 EUR)

- Broadcom (10.37 EUR)

- Imperial Brands PLC (4.21 EUR)

- Reckitt Benckiser Group (11.75 EUR).

The total dividend income in September was: EUR 178/appr. 209 USD

Dividend income check

Now let’s see how the performance was compared to the previous year. Last year, I received only EUR 116.4 in dividends in September, which represents an increase of almost 53 percent. Thus, September is my second best month this year after May. Yeah!

In total, I have received almost EUR 1,300 this year. That is already more than I received dividends for the entire last year. Let’s hope that the development in the last quarter of the year will continue like this. The overall development is as follows:

Stock purchases in September for more dividend income

In September, I bought more shares of great companies so that the dividends will continue to rise in the future:

- Cisco Systems (14 shares)

- Automatic Data Processing (9 shares)

- Munich Re (4 shares)

- Amundi Index MSCI Emerging Markets UCITS ETF DR (D) (25 shares)

- Archer-Daniels-Midland (19 shares)

In the following, I will briefly explain why I bought these companies. Please do not expect a fundamental analysis. I will only mention some aspects per company that might be of interest to the readers. Maybe you will find inspiration for your investment. In case you disagree, feel free to write your opinion about my purchases in the comments.

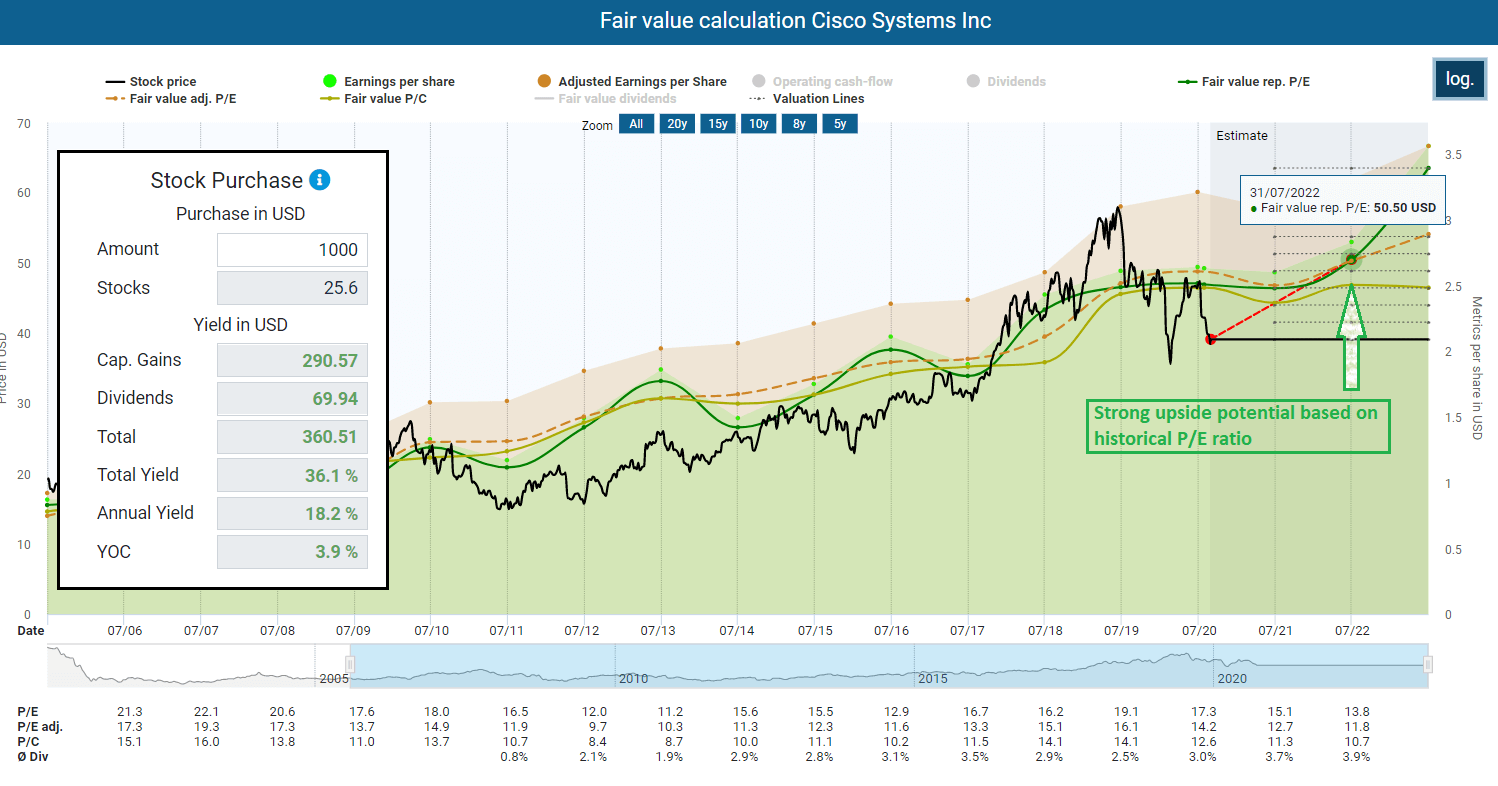

Cisco was the first company I bought in September. I took the opportunity after the devastating quarterly results when the share price fell sharply. The results for the fourth quarter were relatively stable, at least compared to expectations. Cisco generated more profit and more revenue (-9.5% Y/Y) than analysts had expected. But what broke the share price’s neck was the outlook and a closer look at the figures for the fourth quarter. Cisco now expects EPS of USD 0.41-USD 0.47 EPS for Q1, compared with an analyst consensus of USD 0.75; revenue is also expected to decline by between 9 percent and 11 percent.

Cisco has a future

If you look at Cisco’s business segments, I wouldn’t say that they have no future.

- The Infrastructure Platforms segment consists of Cisco’s core networking technologies of switching, routing, wireless, data center products, and software products and services. These products and services are designed to work together to deliver networking capabilities and transport and store data.

- The Applications segment consists of offerings that utilize the core networking and data center platforms to provide their functions. The segment offers primarily software products and services, including software licenses and SaaS and hardware.

- Cisco primarily provides hardware and software (cloud) based products and services for network security, cloud and email security, identity and access management, advanced threat protection, and unified threat management products within the Security segment.

- The Other Products segment primarily includes Cisco’s cloud and system management products.

The problem is that Cisco is still heavily dependent on its hardware-based Infrastructure Platform segment. This segment is responsible for almost 60 percent of consolidated revenue and slumped by 16 percent in the last quarter. Cisco still needs a while here to enter the digital age. There is a certain bittersweetness that the company has not succeeded in selling its online meeting platform Webex better during the COVID-19 related lockdowns, which is where the old design and the not intuitive handling takes its revenge. Even in my firm, we use Microsoft Teams and Zoom, although we have hardware from Cisco, and Webex is also in our “tech portfolio”. But Webex is not used very much by colleagues and clients.

Cisco may be a value play at current levels

But this is only one aspect that I would not overestimate. The company is in the midst of a transition to (cloud-based) software products and subscriptions, which takes time. But Cisco is making progress here. As the company reported, software subscriptions now make up 78% of Cisco’s software revenue, and remaining performance obligations continued to grow strongly in the last quarter.

So we have a situation that I love. Companies that are being beaten down even though they are still making a lot of money, and their business still has a future. These aspects result in great value opportunities. Think of Procter & Gamble, Walmart, or even Microsoft and Apple. They were all written off by investors, even though they were obviously in a state of upheaval and communicated this. A look at the fair value calculation confirms this impression.

So I am patient. During this time, the dividends give me a nice premium for the waiting time. The dividend scoreboard looks healthy and promising for investors with a long term investment approach:

- Dividend yield: 3.69 percent.

- Years of dividend growth: 9 Years.

- Payout ratio: 46.8 percent.

- 5 Year growth rate: 13.27 percent.

- 1 Year growth rate: 3.62 percent.

The German company is the biggest reinsurance company. With its subsidiary Ergo Group, the company is also active in the direct insurance business. Munich Re was on my watchlist for a very long time (for many years, to be honest). It always seemed too expensive, and so Allianz remained the only insurance company in my portfolio for a long time. But then the corona crash came, and I could finally get my first stake. Despite an excellent performance with double-digit price gains, the portion of Munich Re shares in my portfolio fell to 1.6 percent due to other additional purchases and share price gains. After my repurchase, the share is around 2.7 percent, which I can live with quite well.

Reasons for my purchase of Munich Re

The reason for my purchase is that the share price has lost some percentages again. Many investors are afraid that Covid-19 will cause damage to the company. They also fear that falling interest rates will put a heavy strain on the investment business. And indeed, profit, revenue, and cash flow will slump in 2020. It is also not clear how the coronavirus will behave in winter and whether other lockdowns are necessary.

As always, one man’s fear is another man’s opportunity, and the perspective only depends on the right approach. Insurance companies have an ancient and conservative business. It exists, and it will always exist. And so there will always be reinsurers. Many material events can, of course, cause a few bad years. But what happens then? Insurance companies raise premiums. It is probably a business that could be run by an idiot. Munich Re easily meets the 100 percent Solvency II capital ratio required by the law. The Solvency II capital ratio requires a level of equity capital at which, in the next twelve months, non-compliance with the solvency requirements can occur at most as a result of a shock event that occurs statistically every 200 years. Munich Re’s ratio is usually far above 200 percent.

Usual fundamental metrics are useless

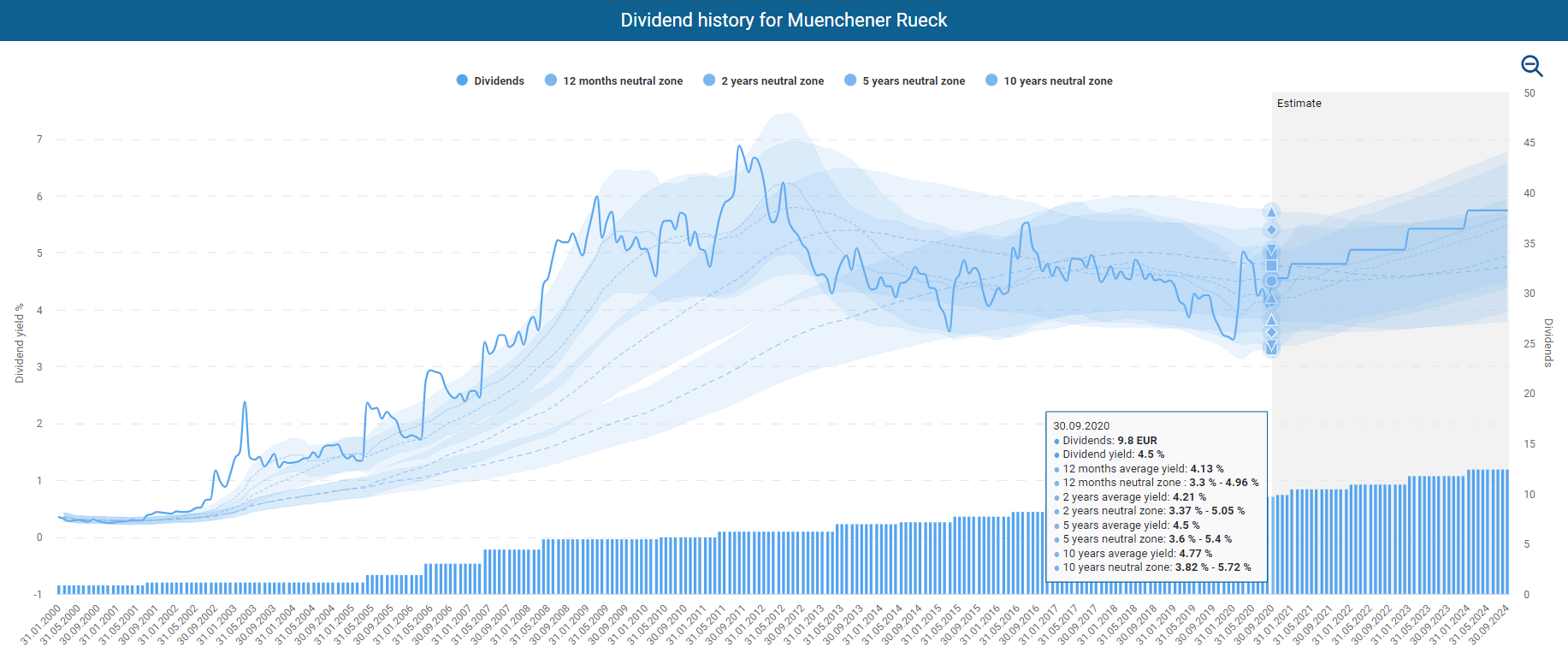

So let us speak about fundamental metrics. I am a fan of the fundamental valuation of stocks considering historical multiples. However, there is a problem at Munich Re because the historical multiples based on profit and cash flow are entirely useless. In individual years, damage events have strongly influenced the results, increasing the P/E ratio. To calculate a fair value here is, therefore, really difficult.

The dividend is decisive here

Because these metrics are useless for Munich Re, I look mainly at the dividend. While Munich Re is not a dividend aristocrat with 25 years of dividend increases in a row, it has not cut its dividend since 1970. For a European company, this is undoubtedly a considerable achievement. The current yield of 4.5 percent is also above or at least at the multi-year corridor level, and that was and is the decisive benchmark for me here.

As you can see above, the company does not increase the dividend every year. But with an initial yield of 4.5 percent, I can live with that. The company’s far-sighted dividend policy matches my conservative investment style, which aims for a long-term return. This approach is also underlined by the way CFO Christoph Jurecka justified the recent 6 percent dividend increase (which was too little for some investors) in the earnings call:

We never said it’s going to proportionally follow the earnings increase from €2.3 billion to €2.8 billion. But due to the fact that the lower boundary of the dividend, that we never had to reduce it in the past. So this floor pretty important to us. We cannot just increase it proportionately because we have to make sure also at a level of safety as a downside protection. Therefore, under proportional dividend growth, I think we delivered on that. And so I don’t see any lagging behind here, I must say.

Besides, the company is keeping the share price stable by massively buying back its shares. In the last seven years alone, Munich Re has repurchased almost 40 million of them, representing 22 percent of all outstanding shares. Furthermore, Munich Re is a company with excellent ratings:

- Fitch: AA (very strong) / stable outlook

- Moody’s: Aa3 (Excellent) / stable outlook

- S&P Global Ratings: AA- (very strong) / stable outlook.

Thirdly, I bought my second ETF this month. As you know, I already own one ETF that tracks the MSCI USA Financials Index (I wrote about it here).

Why should I invest in an ETF?

There is hardly anything in investing that is as important as risk protection. The first step is due diligence. However, we are dependent on companies being honest, not glossing things over, etc. So we need information that we may not even have. The greatest independence, therefore, creates broad diversification. This is also true in geographical terms. Apart from Tencent, I have never had a company in my portfolio that was not from Europe or North America. With the Amundi ETF, I am changing that.

The Amundi Index MSCI Emerging Markets UCITS ETF DR

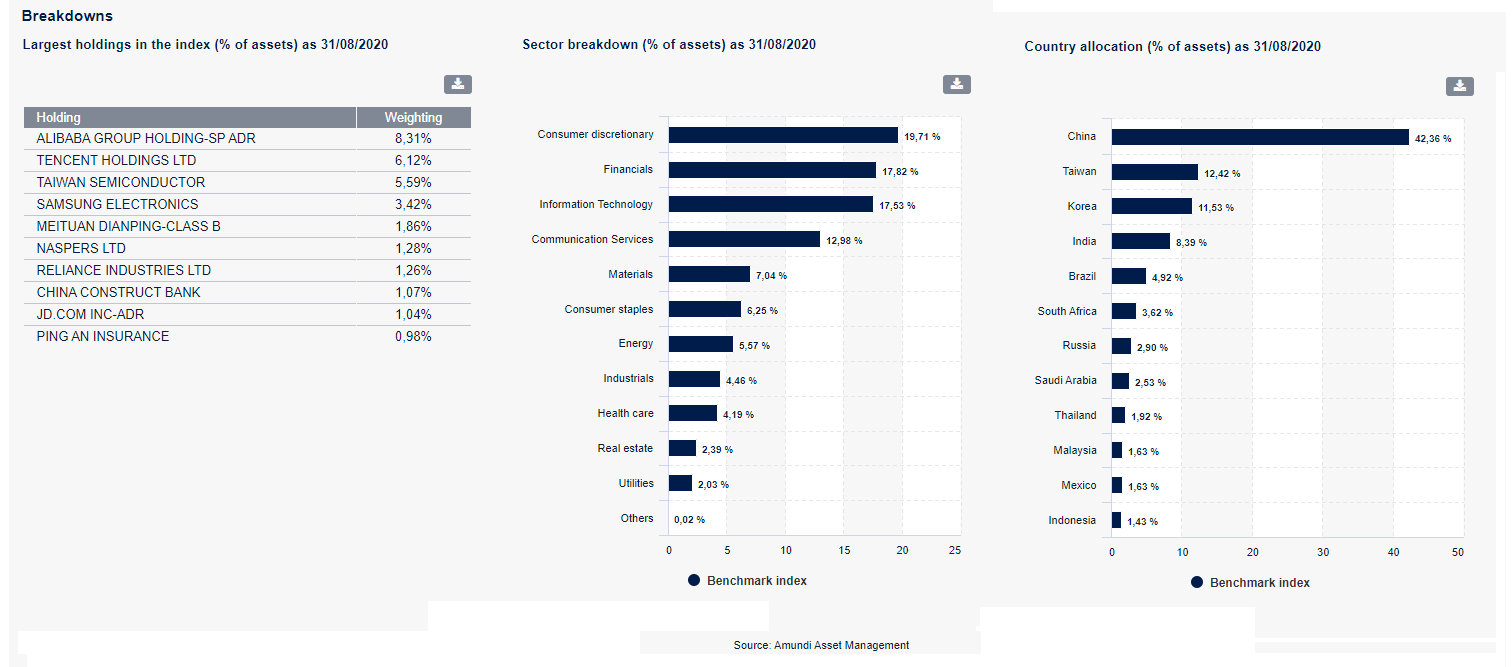

The ETF invests in stocks with a focus on emerging markets. The dividends in the fund are distributed to the investors annually. The objective of this Sub-Fund is to replicate the composition of the MSCI Emerging Markets Index. Therefore, this ETF allows you to invest in appr. 1,383 stocks. The fund currency is EUR, and its replication method is physical (full replication). The payout is usually in November and was in 2018 at 0.91 EUR and 2019 1.17 EUR. A reasonable payout distribution of approximately 1 EUR in 2020 would result in a yield of 2 percent. The total expense ratio amounts to 0.20% p.a.

The “D” in the name means “distributing”. That means you get a dividend. If you choose the C-variant, the ETF reinvests the dividends for you. Austria, Germany, Spain, Finland, France, Hungary, Italy, Luxembourg, Netherlands, Singapore, Sweden, the United Kingdom, Ireland, and Portugal. Even if not all investors can use the Amundi ETF, there are plenty of other ETFs that track the MSCI Emerging Markets Index.

With the ETF, I am suddenly invested in Alibaba, Taiwan Semiconductor (was on my watchlist), Samsung, Naspers, etc. Although Tencent is also part of the ETF, this does not matter, given my portfolio size. Like my other ETFs, I will increase the Amundi ETF at regular intervals. However, I plan that the ETF will take a larger position. In the end, it should take up between 15 and 25 percent of my total portfolio. Thus, I still have to buy some shares.

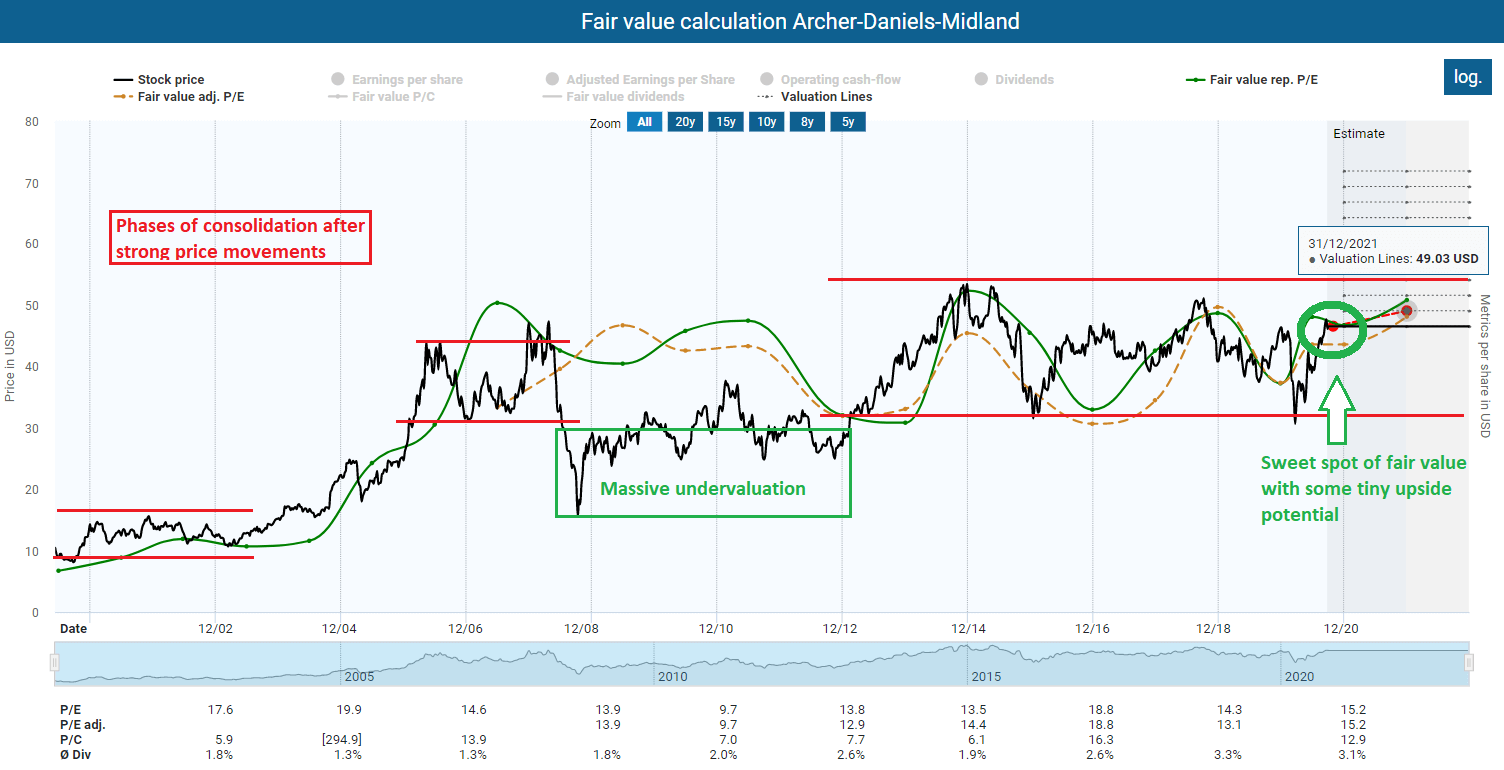

Archer-Daniels-Midland is the epitome of boredom. ADM is one of the largest processors of soybean meal, soybean oil, palm oil, ethanol, fructose syrup, and baking flours. The company operates more than 270 plants and 420 crop procurement facilities worldwide that process cereals and oilseeds into various products used in food, beverages, industrial products, and animal feed.

I also used the Corona Crash at ADM and built up the first position. As with Munich Re, the gains are in the double digits now. With the purchase of further shares, my stake has a satisfying size. At the same time, ADM is still below 2 percent of my total portfolio, so I have more room for further additional purchases. The reason for my purchase was the fundamental valuation of ADM. The company is currently in a phase of long-term consolidation. It is neither strongly undervalued nor strongly overvalued. During the Corona crash, I got shares very cheap, now they are a bit more expensive, but this is no reason for me not to buy more.

Also here, the dividend scoreboard is still convincing:

- Dividend yield: 3.13 percent.

- Years of dividend growth: 26 Years.

- Payout ratio: 46.8 percent.

- 5 Year growth rate: 7.84 percent.

- 1 Year growth rate: 3.25 percent.

Watchlist for October

Next month, there will be some additional purchases of shares. I am relatively flexible here. Either I buy new positions, or I increase my shares in existing investments.

The following companies are on my watchlist in particular:

- Microsoft (MSFT)

- Mayr-Melnhof Karton AG

- Bayer

- Sysco (SYY)

- AT&T (T)

If you look at my report from last month, you will see that none of the companies I bought (except for Cisco) were on my watchlist. Why is that? Is the watchlist nonsense, and in the end, I only do what I want anyway? Yeah, a little bit. I don’t have a fixed system for my stock purchases, and that’s one thing I have to consider changing.

However, I have an extensive overview of many companies that I look at from time to time. The companies on the watchlist are mostly companies that I have currently examined particularly carefully, where substantial changes are imminent or which are in my focus for other reasons.

They are present to me in some form, which is why I put them on the list and perhaps monitor them a little more closely than other companies. But it often happens that I invest in other companies, after all. And so it happens that I buy other companies because it seems convenient at that moment.

Hello TEV, I received dividends from O and REML in September.

I am looking at more O, T, MO and OZK. We’ll see how the budget goes!

Thanks for the comment, Timothy. I also want to address your comment on my post from last month:

“I am VERY new at this and am trying to build up my portfolio, with the goal of acquiring various higher yielding/more consistent producers. Since the above note, I’ve added KO and BTI. My next purchases, I think, will be T, MO and OZK.

Any further comments/suggestions would be appreciated Vic. From you, too, TEV.”

It is a great thing when you try to manage and increase the value of your assets. Investing in stocks is probably the best way to go. You know, of course, that stocks also have a risk. You become the owner of a company, and you are directly involved in its success and failure.

This is one side. The other side is that shares are traded on markets. By this, I do not mean the stock market, but a general market for investing. The buyers in this market are looking for returns. When there was still interest, dividends were very unattractive from a risk/reward perspective. Why should I bear the entrepreneurial risk when I have three percent interest on the bond coupon? That has now changed. People buy stocks because there are no alternatives, which leads to higher prices and lower dividend yields. In a world like this, high dividends are, therefore, a particularly strong warning sign because it means that many investors here do not want to take on the entrepreneurial risk because it is too risky for them – even in a world of a low-risk aversion. For this reason, I would always strongly diversify my portfolio. To rely only on high yielders means taking a (far) above-average high risk. KO is a good compromise between long-term stability, long-term safety and long-term return in my eyes.

All the best!

Thanks TEV, appreciate the direction. When you say to “diversify your portfolio” do you mean diversifying within the stock market (i.e., portions in Growth, Dividend, IPO and Defensive stocks, like that) or diversifying outside of the market (some in the stock market, some in real estate, or something like that)? I am trying that within the market (KO, SU, AAPL, MKC, among others) with more to be done as I investigate/learn further.